ENTA - Enanta: Deep Losses In FY 2022 Look To Be Justified Given Macro Landscape

Summary

- The market's punishment of Enanta Pharmaceuticals, Inc. during FY22 has been quite heavy.

- Despite two attempted snap-back rallies, Enanta Pharmaceuticals stock was rejected at resistance levels on each attempt.

- The macro-landscape has created a more challenging funding environment for capital markets.

- Recent clinical trial developments by Enanta Pharmaceuticals could prove to be key inflection points in 2023, and investor positioning also reflects this.

- Net-net, we rate Enanta Pharmaceuticals, Inc. a hold.

Investment Summary

As we draw near the close of FY22’ many investors are focusing on rebalancing equity portfolios for the new year. The overarching question in our circles has pertained to what 2023 has in store for the medical technology (“med-tech”), biotech, life sciences, and the broad healthcare universe. Unfortunately, the past 12–18 months hasn't been so kind to the broad sector, resulting in a large selloff of many names. Here I turn to Enanta Pharmaceuticals, Inc. ( ENTA ), a company that incurred heavy losses in 2022 [Exhibit 1], despite whipsawing in a combination of upside/downside volatility during the year.

Here I'll discuss our investment findings for ENTA and relate this to our findings on the macro-landscape, itself now a labyrinth for investors to navigate through. Net-net, we rate ENTA a hold.

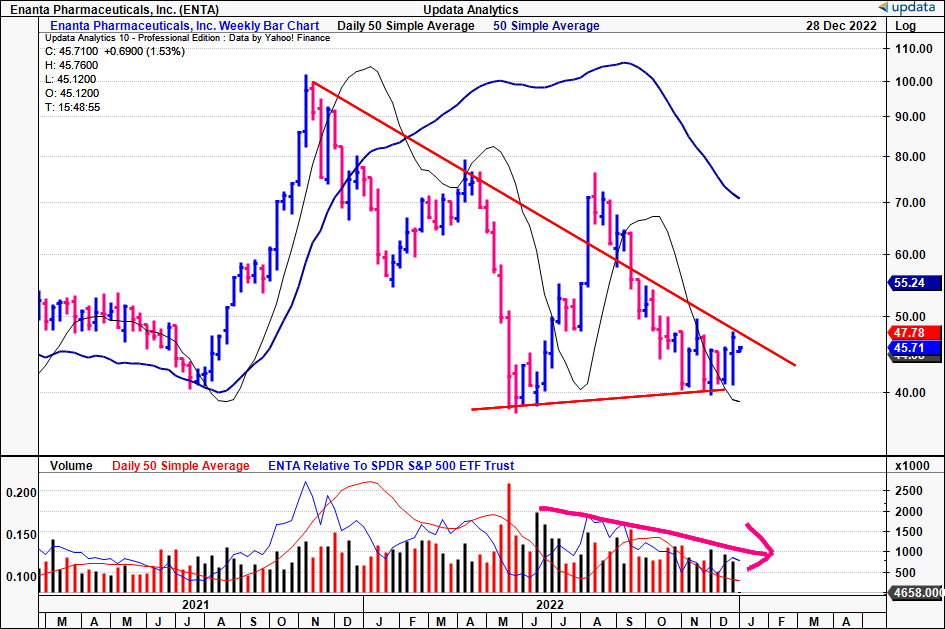

Exhibit 1. Despite 2x attempted rallies over the past 12-18 months, ENTA hasn't managed to break above key resistance levels.

It's found support at the levels seen below, nevertheless, volatility has been extreme in this name as you can see.

{kind=link}

Key factor— Market fundamentals still point to quality, deep value

There are numerous economic and systematic headwinds plaguing global equity markets at present. The domineering theme of inflation seems to have rotated to that of rising government and corporate yields, reduced equity risk premium and a surging cost of capital. This, as global liquidity dries up, whilst investors now command a higher risk premium across the board as it relates to risk assets. As a result, in equity markets, factors of value have caught a strong bid across 2022, as investors reposition to align with short-duration stocks delivering predictable, sizeable cash flows in real terms.

You can see in the chart below the spread of the growth/value axis, that’s widened in the final quarter of FY22’, as a reflection of this. Adding to that, the distribution of potential outcomes now leans increasingly to some form of economic recession as the base case in 2023. What this means for growth-focused stocks such as ENTA remains to be seen. Nevertheless, with the factors mentioned above, the macro landscape when looking ahead isn’t near as supportive as it was over the past decade.

Exhibit 2. Value/growth axis continues to widen in the final portion of 2022.

Data: Updata

In addition, you’ll see in Exhibit 3 that Treasury yields at the longer end of the curve continue to rally, compressing equity valuations. This sets the discount rate higher for companies relying on cash flows priced out into the future. For Enanta Pharmaceuticals, Inc., this also presents as a challenge looking ahead, as securing external financing [equity, debt] is now becoming increasingly expensive.

Moreover, as mentioned, the risk premium investors demand [especially on equity capital] is equally as pricey. Not to mention, the impact on asset valuations, and ENTA’s corporate value looking ahead. It isn’t producing net operating profit after tax (“NOPAT”) nor generating a return on its invested capital. Hence – for the time being anyway – it could face difficulty in funding its long-term/future growth initiatives without external capital in our opinion. Alas, without the support from the capital markets or return on its investments, it’s difficult to see a situation where ENTA re-rates to the upside on fundamentals alone, by estimation.

Exhibit 3. Treasury yields continue to lift, compressing asset valuations for risk assets.

Data: Updata

Catalysts to move the needle for ENTA

What could potentially see ENTA catch a bid in FY23 on the other hand is the momentum it is building around its clinical pipeline. With respect to its Covid-19 pathway, ENTA recently mentioned it initiated the SPRINT phase 2 trial to advance its EDP-235 compound. The randomized, double-blind, placebo-controlled study ("RCT") will enroll 200 patients demonstrating Covid-19 symptoms. Note, inclusion criteria is that patients are not at increased risk of developing more severe symptoms, and haven’t received a Covid vaccine.

In the trial, dosages will be assigned using either a 200mg or 400mg regime of EDP-235 once daily via oral administration. This follows from its Phase 1 EDP-235 study that demonstrated tolerability at the 400mg level. Specifically, that dose was shown to produce in vitro potency levels that were “ 6-fold and 13-fold” above the concentration that resulted in 90% inhibition of the viral replication. For reference, this is known as EC90.

For the SPRINT phase 2 trial, ENTA will be investigating safety and efficacy as the primary outcome measure, with secondary endpoints evaluating pharmacokinetics and dosage protocols for subsequent clinical studies. Regarding the rationale behind the 200/400mg regime, according to management on the last earnings call:

“ In other studies of protease inhibitors, the viral load decline has been similar between high and standard risk populations. Thus, we believe enrolling from a larger pool of standard risk patients will be a more efficient way to collect this information. We are aiming to report results from SPRINT in the first half of 2023.”

Hence we expect the SPRINT trial to be a potential catalyst into the new year, should the company convert on its pipeline growth here.

Moreover, as recently as October, ENTA announced it has initiated its Phase 2b RCT for its EDP-938 compound, investigating the N-protein inhibitor in patients diagnosed with respiratory syncytial virus ("RSV"). Specifically, the 180 patient cohort will focus on those with RSV who are at risk of developing further complications, and present with comorbidities such as congestive cardiac failure ("CCF"), chronic obstructive pulmonary disease ("COPD"), or asthma.

The study will examine patients who receive an 800mg dose of EDP-938 or placebo for 5 days, with a follow-up period at 28 days. The primary endpoint will check time to resolution of RSV, and will be objectively measures using the Respiratory Infection Intensity and Impact Questionnaire ("RiiQ") symptom scale.

Q4 financial results illustrate lack of risk premium

Turning to the company’s latest set of quarterly numbers, we’d note there are several data points worth discussing. Note, ENTA also reported its FY22 full-year results in November, but I'll be mainly focusing on the fourth quarter earnings in this section. For a deeper look at the company's full-year results, you can see the company's 10-K by clicking here.

First off we saw that Q4 revenues pulled in to $20.3mm, down from the $23.6mm reported last year. The breakdown of this included a royalty revenue from net global sales of AbbVie’s MARVIET label. The royalty tier that covers the arrangement between ENTA and AbbVie can be seen in Exhibit 3 below. To us, the royalty stream on its own isn't sufficient to provide liquidity to finance ENTA's pipeline conversion. Especially given the measures it took this year to use up additional liquidity.

To illustrate, ENTA ended the quarter with ~$249.2mm in cash and marketable securities. Of this amount, only ~$44mm was booked as on-balance sheet cash. For the 12 months, ENTA realized a net decrease in cash of $9.85mm, after an $84.78mm cash burn from operations. However, it also realized $54.9mm and $20mm from the purchase/sale of marketable securities and increase in proceeds from the exercise of stock options, respectively. In our book, questions arise on the sustainability of these measures to increase available capital. Nevertheless, management remain confident that its current position and cash balance will provide sufficient runway for operations into FY24.

Exhibit 3. Details of royalty tier associated with cumulative calendar year net sales as it relates to ENTA's agreement with AbbVie.

Data: ENTA FY21 10-K, pp. F-17–F-18; see: "Collaboration Agreements"

Moving down the P&L, ENTA's OpEx came into $47.4mm for Q4, down from $57.3mm the year prior. This was primarily due to a 28.8% YoY decrease in R&D investment to $34.8mm. For the full year, R&D expense was also ~$10mm lower at $164.5mm. It pulled this down to a net loss of $26.3mm or $1.27 per share [diluted], roughly in-line with the previous year. Switching to FY23 guidance, ENTA projects its R&D expense to increase by ~40% YoY at the upper end to $230mm. It made no mention on forecasts surrounding royalty revenue as per the Exhibit above.

Valuation and conclusion

Given the lack of revenue and earnings, the predictability of ENTA's future cash flows its quite low in our opinion. Hence, we turned to several other measures in order to guide price visibility for the coming periods.

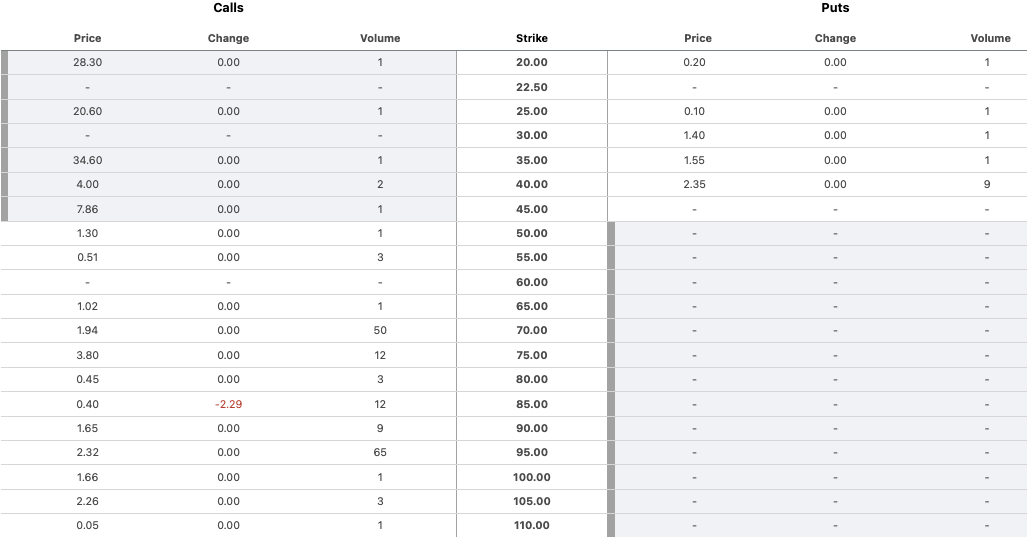

First, checking the ENTA options chain, we saw an incredibly deep options chain where the price ladder for calls extends from $20–$110 for contracts expiring in January 2023. Similar positioning is observed in April 2023 calls.

For those looking at Exhibit 4, you'll notice that the bulk of call volume is centered around the $70 and $95 marks respectively.

This could mean one of two things; either investors are speculative of a rally to the $70–$110 range, or are hedging a large short exposure of the underlying stock. With 5.77% short interest, this could very well be the case.

Exhibit 4. ENTA options chain, calls and puts expiring January 2023. Calls stacked with volume concentrated in $70–$110 strike range. Note: only in the money calls are shown.

Data: Seeking Alpha, ENTA, see: "Options"

{kind=link}

In addition, we wanted a set of objective measures to fold into the market outlook for ENTA. Using Seeking Alpha's quantitative factor grading for ENTA, we can achieve just that. You'll see below that the stock is rated highly in terms of valuation. Although, it does trade at 60x forward EBITDA and 3x book value. Nevertheless, this must be factored into the investment debate.

Exhibit 5. ENTA quantitative factor grading, rating the stock highly in terms of valuation

Data: Seeking Alpha ENTA quote page

Finally, looking at our point and figure studies, there's targets to a $52 range, suggesting the stock could re-rate to that level. To us, this corroborates a neutral view, rather than advocating an outright sell on the stock.

Exhibit 6. Price objectives to $52, currently above the market price, certainly a balancing factor in the ENTA investment debate.

Data: Updata

In summary, there's plenty to like about ENTA's clinical pipeline and the trajectory it is working towards in providing solutions to complex disease segments. However, the macro-economic picture cannot be denied at this stage, especially the impact of rising treasury yields on the valuation of risk assets. Moreover, this appears to be reflected in market positioning, with investors searching for shorter-duration stocks that fit the value factor bill.

Still, there's evidence to suggest Enanta Pharmaceuticals, Inc. could hold its current market price[s], and even mean revert to its longer term averages. With this culmination of factors in mind, we rate Enanta Pharmaceuticals, Inc. a hold for now, and look forward to providing further coverage.

For further details see:

Enanta: Deep Losses In FY 2022 Look To Be Justified Given Macro Landscape