ENB - Enbridge: A Core Holding For Any Dividend Investor

Summary

- Enbridge Inc. is one of the largest midstream companies in North America, owning an extensive infrastructure network that spans the continent.

- The company enjoys remarkably stable cash flows regardless of conditions in the broader economy.

- Enbridge boasts significant forward growth opportunities and is working to get into the rapidly growing liquefied natural gas space.

- The company's debt is a bit higher than I really like, but it is not horrible.

- The Enbridge 6.55% yield is easily sustainable.

Enbridge Inc. ( ENB ) is a Canadian midstream company that owns and operates one of the largest pipeline networks in North America. This is generally a good business to be in, despite the widespread belief that fossil fuels are becoming obsolete. That incorrect belief has caused the shares of many companies in the traditional energy industry to be severely undervalued, and Enbridge is certainly no exception to this. The company’s impressive 6.55% current yield is a testament to that.

In addition to this, the company enjoys remarkably stable cash flows throughout any economic environment. This is something that could prove especially valuable in today’s uncertain economic environment. Enbridge also boasts fairly strong forward growth prospects that should allow it to deliver a rising stream of income to its investors over the coming years. Enbridge stock has long been a core holding of many energy investors, which is a title that the company continues to deserve.

About Enbridge

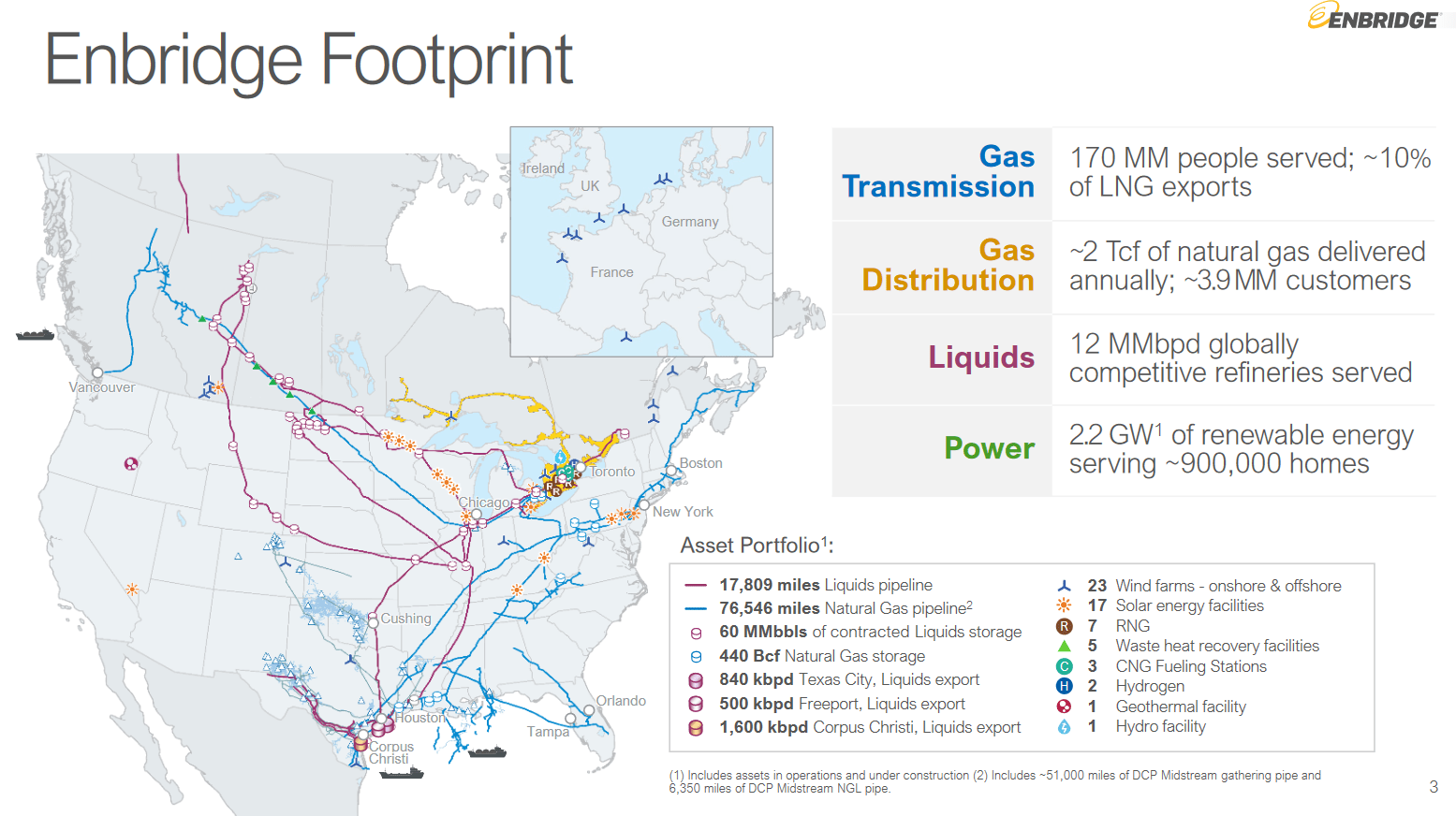

As stated in the introduction, Enbridge is a large Canadian midstream company that owns and operates one of the largest pipeline and midstream infrastructure networks in the United States and Canada. In total, the company owns 17,809 miles of liquid pipelines, 76,546 miles of natural gas pipelines, 60 million barrels of liquid storage, 440 billion cubic feet of natural gas storage, and many other assets:

{kind=link}

One thing that we immediately notice from the map above is that Enbridge has operations in just about every major basin in which hydrocarbons are produced in both the United States and Canada. This is something that is fairly nice to see because each of these basins has somewhat different fundamentals and geology. For example, the Marcellus Basin in Appalachia is usually targeted by energy producers that are seeking to produce natural gas.

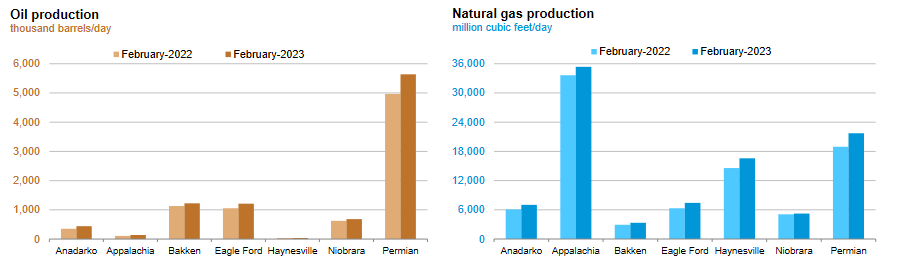

On the other hand, the Permian Basin is generally considered a source of crude oil, although it also has a significant amount of natural gas and natural gas liquids. We have also seen production in the Permian Basin increase much more than the production of an area like the Niobrara during certain periods. For example, the former region has seen much greater production growth over the past year:

{kind=link}

The fact that Enbridge has operations in all of these different areas grants it plenty of diversification benefits as it has exposure to the advantages of each of these different regions.

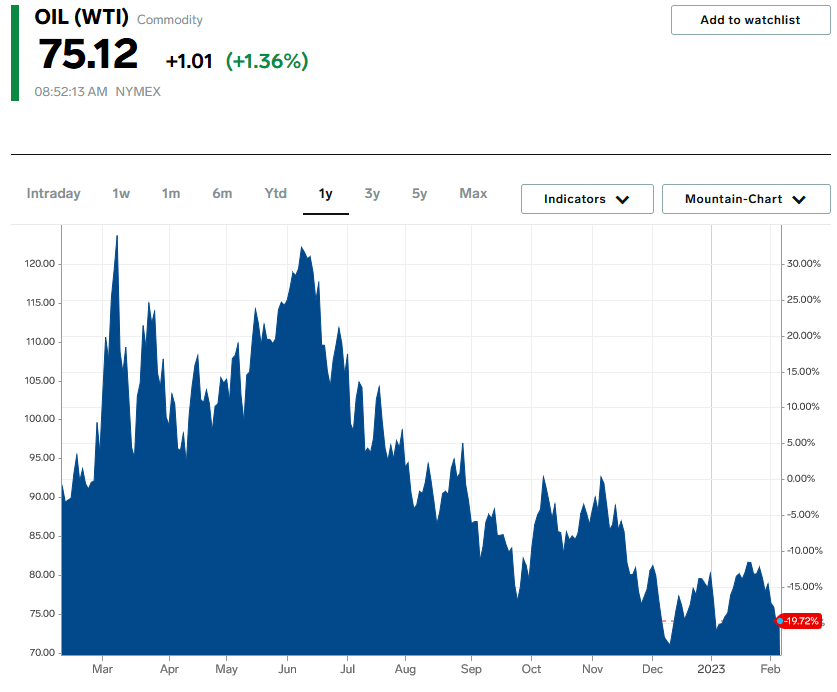

As mentioned in the introduction, Enbridge has remarkably stable cash flows regardless of energy prices or broader economic conditions. This is rather nice considering the volatility that we have seen in crude oil prices over the past year. As we can see here, the price of West Texas Intermediate crude oil peaked at $123.70 per barrel back in March 2022 but has fallen back since then and currently sits at $75.12 per barrel:

{kind=link}

While this has had an effect on Enbridge’s stock price, it has had no significant impact on the company’s cash flows. In the third quarter of 2022, Enbridge reported an adjusted EBITDA of CAD$3.758 billion compared to CAD$3.269 billion in the equivalent quarter of 2021. That represents a 15% year-over-year increase. The company’s year-to-date financial performance has shown a similar growth rate as it reported an adjusted EBITDA of CAD$11.620 billion in the first three quarters of 2022 compared to CAD$10.314 billion in the same period of 2021. That is roughly a 13% increase year-over-year. That is overall much more stability than we saw in crude oil prices over the same period.

The biggest reason for the company’s stability is the business model that it utilizes. In short, Enbridge enters into long-term (usually five to ten years in length) contracts with its customers. Under these contracts, the customer transports crude oil, natural gas, and other hydrocarbon products using Enbridge’s expansive pipeline and storage network. In exchange, the customer compensates Enbridge based on the volume of resources transported, not on their value. This overall provides Enbridge with a great deal of insulation against changes in crude oil and natural gas prices. As fully 98% of Enbridge’s cash flow comes from these contracts, we can quickly see that the company should be relatively unaffected by any changes in energy prices that occur.

At this point, there may be some readers that point out that the production of resources tends to decline when energy prices are low. We saw this happen back in 2020 following the price crash that accompanied the COVID-19 pandemic and the lockdowns that severely reduced the demand for crude oil. This could be expected to have a negative impact on Enbridge’s cash flow as fewer resources would need to be transported through the company’s infrastructure due to the lower production volumes.

However, Enbridge has a way to protect itself against events such as this. In short, the company’s contracts include what are known as minimum volume commitments. These contractual clauses require that the customer send a certain volume of resources through the company’s infrastructure or be paid for anyway. These clauses, therefore, place an effective floor on the company’s cash flows through which they cannot decline past. That is something that we can appreciate as income investors since it provides the company with a baseline level of cash flow to use to cover the dividend.

Of course, the contracts through which Enbridge derives its revenue are only as good as the counterparties. After all, if a counterparty goes out of business, then the company’s revenue from that contract will terminate. Although the high energy price environment that has dominated for the past year or two has greatly increased the financial strength of most upstream producers and thus made this scenario less likely than it was a few years ago, it is still possible for an irresponsible company to find itself in financial distress today.

Fortunately, Enbridge seems to be relatively protected against that risk as 95% of its cash flow comes from counterparties that boast an investment-grade credit rating. This is nice to see since any energy company that has an investment-grade rating has the sufficient financial strength to honor its commitments even through a worst-case scenario. In addition, most of these companies have a vested interest in maintaining their reputation as reliable business partners so they will probably do everything in their power to make the payments that are required of them under the contracts with Enbridge.

Overall, we can clearly see that Enbridge is very well equipped to weather anything and deliver income to us as investors reliably. This is exactly the reason why this company is a core holding in any energy income portfolio.

Growth Opportunities

Naturally, as investors, we want to see more than just stability. We like to see growth from the companies that we are invested in. Enbridge has a long history of delivering this growth as the company has consistently grown its adjusted EBITDA (a proxy for pre-tax cash flow) since 2008:

Enbridge

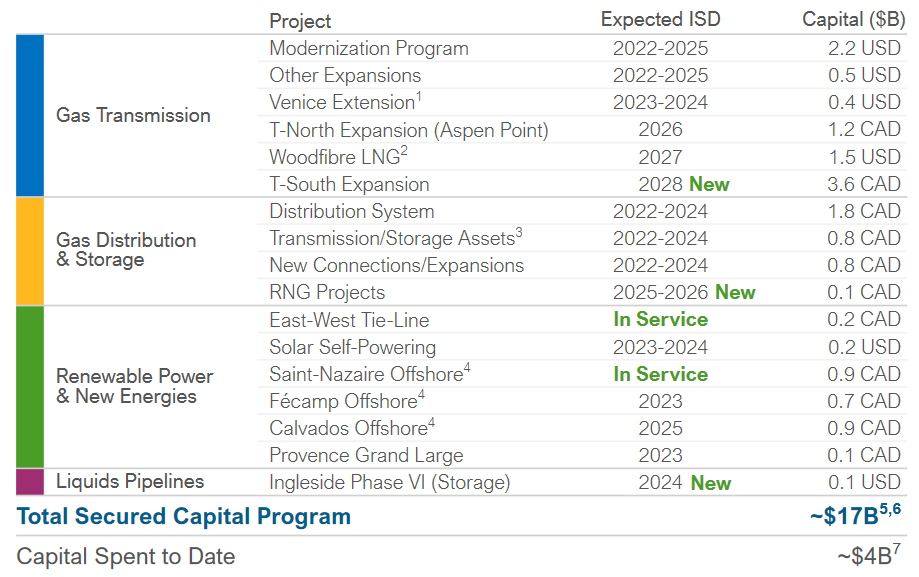

This time period included the Great Recession that followed the financial crisis in 2007 and 2008, as well as three energy bear markets (2009, 2015, and 2020), and the pandemic-related lockdowns. The company’s adjusted EBITDA never once declined despite all of these negative events, which only reinforces its financial stability. There is also a great deal of growth here that Enbridge is likely to continue going forward. The primary way that the company is doing this is by constructing new infrastructure. In fact, the company currently has CAD$17 billion worth of new projects under construction that are expected to come online between now and 2026:

{kind=link}

The reason why this is necessary for growth is that pipelines, storage facilities, and other midstream infrastructure only has a limited number of resources that it can handle. Therefore, as the company’s cash flows are directly correlated with the volume of resources that it handles, it needs to increase its capacity in order to grow cash flows. That is accomplished by constructing new infrastructure.

The nice thing about all of these projects is that Enbridge has already secured contracts with its customers for their use. This is nice because it ensures that the company is not spending a great deal of money to construct new infrastructure that nobody wants to use. In addition, Enbridge knows in advance how profitable each project will be before it actually starts spending money on construction. This ensures that the company will receive an acceptable return on its invested capital. Unfortunately, Enbridge has not provided estimated return figures for all of these projects and the ones that it has provided are somewhat disappointing. Here they are:

Enbridge

With the exception of the DRA Expansion, these multiples are worse than we want to see. Kinder Morgan ( KMI ) frequently manages to achieve a 4x multiple on its growth projects. The Williams Companies ( WMB ) has a 6x multiple on the natural gas pipeline projects that it is working on. As we can see, Enbridge has a few projects that have less attractive multiples than this and this is concerning. While the Gulf Coast LNG Laterals and Ingleside Acquisition will still generate growth for the company, its returns will not be as high as we would really like to see given what the company’s peers are consistently achieving. This means that its growth will not be as strong as it could have been had it managed to get these projects done for cheaper.

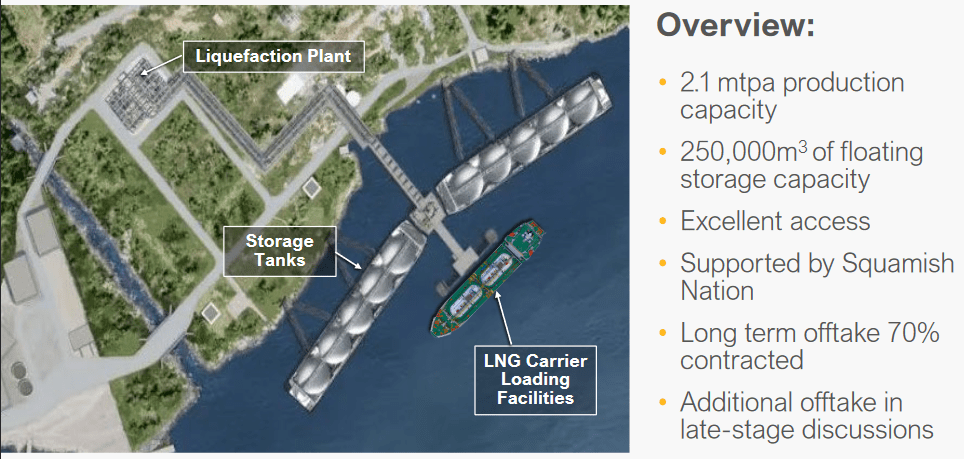

One of Enbridge’s major projects is the Woodfibre LNG Project. This appears to be a similar move to the one that Pembina Pipeline ( PBA ) made a few years ago to enter into the production of liquefied natural gas, which is one of the most rapidly growing segments of the energy industry. As envisioned, the Woodfibre LNG Project consists of a liquefaction plant that is capable of producing approximately 2.1 million tonnes of liquefied natural gas annually, along with 250,000 cubic meters of floating product storage, and a facility for loading the liquefied natural gas onto ocean-going tankers:

{kind=link}

The facility will be located on the coast of British Columbia, Canada just north of Vancouver. This is a site that makes a great deal of sense considering that it provides very easy access to the Asian markets. All one would need to do is sail a tanker across the Pacific Ocean to get there, after all. As I discussed in a recent blog post , the Asian demand for liquefied natural gas is expected to increase by 40% over the 2021 to 2030 period as the region attempts to address its pervasive smog and air quality problems.

This is on top of the liquefied natural gas demand growth that we are seeing in Europe as that continent attempts to wean itself off of Russian-supplied natural gas. Thus, this clearly could be a good business for Enbridge to get into, especially considering that it already has the pipelines in place to carry natural gas to the liquefaction plant.

The Woodfibre LNG Project is certainly not a near-term growth project for Enbridge, however. It takes a very long time to construct a liquefaction plant, which is something that Europe has been discovering as it is taking the continent longer than politicians originally hoped to replace the Russian natural gas supplies with American imports. As such, the Woodfibre LNG Project is not expected to start operating until 2027 and we should not expect it to have an impact on Enbridge’s financial performance until that time. In addition, Enbridge only owns 30% of the project so it will not benefit from all the cash flows that it produces. However, it will certainly result in a boost to the company’s income when it starts operating and it is something that long-term investors can look forward to.

Financial Considerations

It is always important to look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is normally accomplished by issuing new debt and using the proceeds to repay the existing debt. That can cause a company’s interest expenses to increase following the rollover depending on conditions in the market.

In addition, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a firm’s cash flow to decline could push it into financial distress if it has too much debt. Although midstream companies like Enbridge typically have remarkably stable cash flows, it is still possible for them to get into financial problems so this is a risk that we should not ignore.

The usual method that we use to measure a midstream company’s ability to carry its debt is to look at its leverage ratio. The leverage ratio, which is also known as the debt-to-adjusted EBITDA ratio, essentially tells us how many years it would take the company to completely repay all of its debt if it were to devote all of its pre-tax free cash flow to that task. As of September 30, 2022, Enbridge has a leverage ratio of 4.9x based on its trailing twelve months adjusted EBITDA. That is disappointing, as many of the best-financed midstream companies have gotten this ratio down under 4.0x in the two years following the outbreak of the pandemic.

Enbridge thus remains one of the most heavily-leveraged companies in the industry. With that said, Wall Street analysts generally consider anything under 5.0x to be an acceptable level of debt so Enbridge does meet their requirements. For my part though, I would like to see the company take steps to address this and get it well under the company’s year-end goal of 4.70x.

Dividend Analysis

One of the biggest reasons why investors purchase midstream companies like Enbridge is because of the high dividend yields that they typically possess. Indeed, all throughout this article, I have been highlighting the company’s positive qualities as an income investment so this is indeed my biggest goal with this company as well. Fortunately, Enbridge shines in that respect as the company boasts a 6.55% yield at the current price and has a long history of increasing its dividend on an annual basis:

Enbridge

The fact that the company increases its dividend annually is something that should prove especially valuable during inflationary times, such as the one that we are living through today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. As such, it is likely to feel as though we are getting poorer and poorer with the passage of time. The fact that the company sends us more money each year helps to offset this effect and maintains the purchasing power of the dividend.

As is always the case though, it is vital that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want it to be forced to reverse course and cut the dividend as that would both reduce our income and almost certainly cause the company’s stock price to decline.

The usual way that we analyze a midstream company’s ability to maintain its dividend is by looking at its distributable cash flow. The distributable cash flow is a non-GAAP measure that theoretically tells us the amount of cash that was generated by a company's ordinary operations and is available to be distributed to the common shareholders. In the third quarter of 2022, Enbridge reported a distributable cash flow of CAD$2.501 billion.

That works out to CAD$1.24 per common share, which was sufficient to cover the declared distribution of CAD$0.8875 per share 1.40 times over. That is a reasonable ratio that is well within the 1.20x maximum that Wall Street analysts generally consider to be sustainable. I am more conservative than these analysts and like to see a 1.30x ratio in order to add a margin of safety to the dividend. Enbridge clearly meets even this more stringent requirement so we can conclude that the dividend is likely to be quite safe. That should be comforting for income investors.

Conclusion

In conclusion, Enbridge Inc. has long been a core holding for dividend investors for a very good reason. Enbridge Inc. boasts incredibly stable cash flows regardless of economic conditions along with a historically high dividend yield. When we combine this with the company’s respectable forward growth prospects, it is likely to continue to possess these qualities going forward. Overall, Enbridge Inc. looks to be a good way for any investor to get a 6.55% yield today.

For further details see:

Enbridge: A Core Holding For Any Dividend Investor