EINC - Enbridge: A Nice Way To Earn A 6.20% Yield

- Enbridge is one of the largest midstream companies in North America and a long-time favorite of income-focused investors.

- The company enjoys remarkably stable cash flows over time regardless of the macroeconomic environment, which helps to support the dividend.

- The company boasts some significant growth projects that should allow it to grow its cash flow at a 5% to 7% rate over the 2022 to 2024 period.

- The company boasts a 6.20% dividend yield that it appears more than able to sustain.

- The debt load is a bit higher than I really want to see in a midstream company, but it is not unreasonable.

Enbridge, Inc. ( ENB ) is the largest midstream company in Canada and one of the largest in North America, as the company has operations stretching across much of Canada and the United States. This has proven to be a very volatile sector over the past few years as the outbreak of the pandemic collapsed the market prices of many of these companies, but they have since recovered along with energy prices. Enbridge, for its part, is up 10.44% over the past year, which is admittedly not particularly impressive but this is still better than the losses that numerous other companies have delivered.

The company's cash flows have been much more stable than its stock price, which is a defining characteristic of Enbridge's business model. Enbridge offers much more than just stability and a very attractive 6.20% dividend yield, however. The company also has some substantial growth prospects that should allow it to grow both its cash flows and dividend yield in the coming years. This is exactly the kind of scenario that should appeal to any income-focused investor. Therefore, let us have a look at Enbridge and see if the company could be right for your portfolio.

About Enbridge

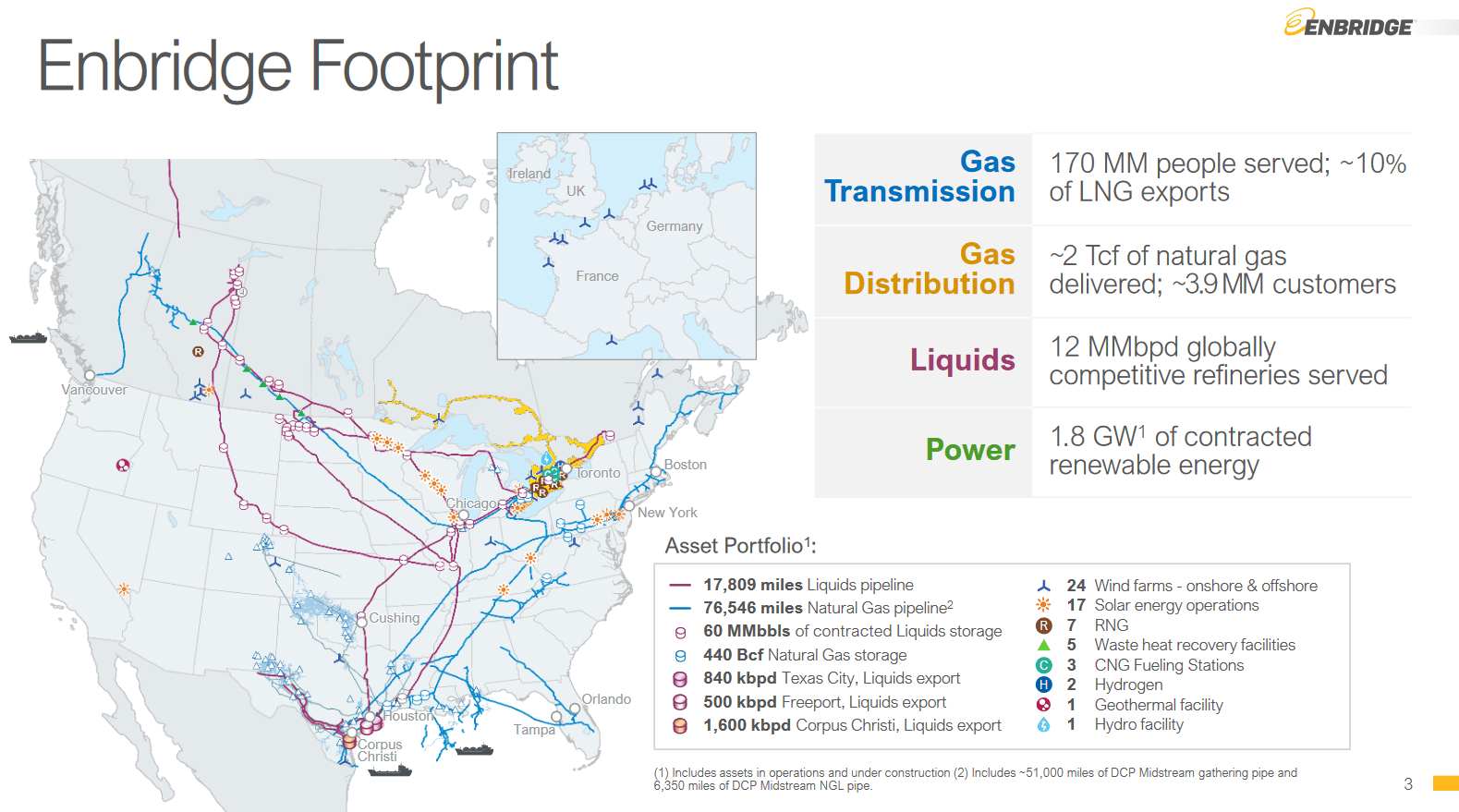

As stated in the introduction, Enbridge is the largest midstream company in Canada and one of the largest in North America, having a network of pipelines and other infrastructure that stretches across much of Canada and the United States. In total, Enbridge boasts 17,809 miles of liquid and 76,546 miles of natural gas pipelines coupled with sixty million barrels of liquid and 440 billion cubic feet of natural gas storage:

{kind=link}

One of the things that we notice here is that Enbridge's infrastructure encompasses most of the major basins in which hydrocarbon resources are produced. This is nice because each of these basins has very different fundamentals. For example, the Bakken Shale is primarily targeted by upstream companies that are looking to produce crude oil while the Marcellus is primarily a production center for natural gas and natural gas liquids. The Canadian Waterfloods, meanwhile, is a very active producer of both of these compounds. This is nice because it provides Enbridge with some product diversity, which is important because the fundamentals for crude oil and natural gas are different.

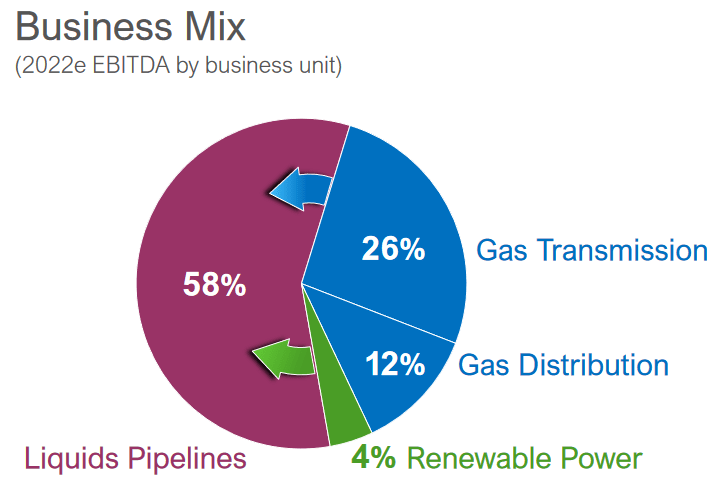

Most importantly, natural gas has much stronger fundamentals than crude oil, which we will see later in this article. As Enbridge handles both products, the company is able to benefit from the characteristics of each of them. With that said though, Enbridge's cash flows are mostly weighted towards liquids, which may be somewhat surprising considering that its natural gas infrastructure is much more extensive:

{kind=link}

As we can see, despite liquids accounting for more of the company's cash flow than natural gas, the two products together make up nearly all of its income. It is unlikely to be a surprise to anyone reading this that the market prices of both crude oil and natural gas have risen substantially over the past eighteen months. As of the time of writing, West Texas Intermediate crude oil is up 48.15% while natural gas at Henry Hub is up 106.44% over the past twelve months. Unfortunately, Enbridge does not really benefit from this because of the business model that it uses.

In short, Enbridge enters into long-term (typically five to ten years in length) contracts under which a customer utilizes Enbridge's infrastructure to transport its hydrocarbon resources. In return, the customer compensates Enbridge based on the volume of products that the company handles, not on their value. This business model provides Enbridge with a great deal of insulation against changes in resource prices. This protects the company against steep price declines like what we saw in 2020 but it also, unfortunately, prevents the company from being able to truly benefit from a high-price environment like what we have today. As fully 98% of the company's cash flow comes from these contracts, Enbridge enjoys remarkably stable cash flows regardless of the broader macro-economic conditions. We can see this by looking at the company's operating cash flows over the past few years:

{kind=link}

(all figures in millions of U.S. dollars)

The overall stability that we see with respect to the company's cash flow is quite nice because of the support that it provides to the dividend. After all, it is much easier for the company to pay out very large percentages of its cash flow if it knows that it will have a similar amount coming in the next quarter. Enbridge aims to pay approximately 60% of its distributable cash flow out to the investors so we can see how important it is for the company to have stable cash flows if it is to maintain the high dividend yield that we have come to appreciate over the years. Naturally, though, the contracts that Enbridge has with its customers do not mean very much if the customer lacks the financial capacity to honor them through difficult economic conditions. This might be important given that there are a growing number of analysts predicting that we will soon be in a recession if we are not already.

It therefore might be comforting to learn that fully 95% of Enbridge's contracts are with investment-grade customers. The reason that this is nice is that an investment-grade customer is highly unlikely to default on one of its contracts with Enbridge. After all, these companies typically have strong enough balance sheets to weather any tough economic conditions. An investment-grade company will also have a vested interest in protecting its reputation as a good partner to do business with and that reputation could be severely jeopardized if the customer reneges on its contract with Enbridge. Thus, it is reasonable to assume that Enbridge's customers will almost certainly do everything in their power to ensure that they honor their contracts with the company. Thus, we can assume that Enbridge's cash flows are likely to be quite secure.

In the introduction, I stated that Enbridge boasts some significant growth opportunities. This is something that is very nice to see since as investors we are interested in much more than simply stability. We want to see growth as well. As we might guess based on the company's business model, the only realistic way for it to see growth is by increasing the volume of hydrocarbon products that it transports. However, the company's infrastructure only has a finite quantity of resources that it can transport so logically the company needs to construct new infrastructure so that it can transport a higher volume of resources. Enbridge currently has C$10 billion (US$7.76 billion) worth of new infrastructure currently under construction that will come online over the 2022 to 2024 period that will serve the purpose of boosting the firm's volumes:

Enbridge Investor Presentation

The nicest thing about these projects is that Enbridge has already secured contracts from its customers for the use of this new infrastructure. This is nice because we can be certain that Enbridge is not spending a great deal of money to construct pipelines and other projects that nobody wants to use. In addition, Enbridge knows in advance just how profitable its projects will be so it knows that it will earn a high enough return to justify the investment. The company states that on average its projects will pay for themselves in three to eight years, which is reasonable for a midstream infrastructure project.

This is in line with what Kinder Morgan ( KMI ) and The Williams Companies ( WMB ) typically achieve from their growth projects and substantially better than what Equitrans Midstream ( ETRN ) achieves on its projects. Overall, the company's current growth projects will allow it to grow its distributable cash flow at a 5% to 7% compound annual growth rate over the 2022 to 2024 period. As Enbridge aims to pay out 60% of its distributable cash flow as a dividend to investors, we can assume that the company will grow its dividend at a similar rate. This is something that any income-focused investor should be able to appreciate.

Fundamentals Of Hydrocarbon Resources

As we have already seen, Enbridge makes its money primarily by transporting natural gas and liquid hydrocarbons, with its cash flows directly correlating to the volume of resources that it handles. Fortunately, the fundamentals of both crude oil and natural gas are quite positive and point towards rising volumes going forward, although natural gas is positioned much more strongly. This could pose a problem for Enbridge since its business is heavily geared toward crude oil and other liquids but its natural gas business is certainly nothing to sneeze at. According to the International Energy Agency, the global demand for natural gas will increase by 29% while the global demand for crude oil will only increase by a much more moderate 7% over the next twenty years:

Pembina Pipeline/Data from IEA 2021 World Energy Outlook

Perhaps surprisingly, the demand for natural gas is being driven primarily by climate change concerns. As everyone reading this is certainly well aware, these concerns have led governments all over the world to impose a variety of incentives and mandates that are intended to reduce the carbon emissions of their respective nations. One of the most common strategies to accomplish this is to encourage utilities to convert their old coal-fired power plants into renewable ones. However, renewables are not reliable enough to support a modern electric grid on their own. After all, wind power does not work when the air is still and solar power does not work at night.

Thus, utilities have frequently begun supplementing renewable power plants with natural gas turbines to ensure that the grid remains operational at all times. This is because natural gas burns much cleaner than any other fossil fuel and is reliable enough to ensure that we continue to enjoy the performance that is expected of a modern grid. It is for this reason that natural gas is often referred to as a "transitional fuel" as it provides a way to both reduce carbon emissions and ensure that the electrical grid can continue to reliably provide businesses and consumers with electricity until renewables are capable enough to do it on their own.

The case for crude oil demand growth may be a bit harder to understand, particularly since politicians and other government officials have been pushing very hard to reduce the consumption of crude oil within their borders. This is true in the world's developed markets but it is a very different story in the various developing nations around the world. These nations are expected to see tremendous economic growth over the twenty-year projection period, which will have the effect of lifting the citizens of these nations out of poverty and putting them securely into the middle class.

These newly middle-class people will naturally want to enjoy a lifestyle that is much closer to what their counterparts in the developed nations enjoy than what they have now. This will require growing consumption of energy, including energy derived from crude oil. As the populations of these nations are considerably larger than the populations of the world's developed nations, the growing crude oil consumption in these parts of the world will more than offset the stagnant-to-declining crude oil demand in the wealthy Western nations.

The United States and Canada are among the only areas of the world that can increase production sufficiently to satisfy this growing demand. The reason for this is the incredible mineral wealth of areas like the Bakken Shale and the Permian Basin. This is one of the reasons why it is nice to see that Enbridge has operations in every major basin since we are not sure exactly where this production growth might occur.

Enbridge will still benefit from any production growth in its footprint even though it does not produce any resources itself. This is because somebody will have to take the resources away from the oil and natural gas fields and to the market where they can be sold, which is the exact business that Enbridge is in. This should thus result in growing volumes of transported resources for Enbridge as the trend plays out. As Enbridge makes its money based on volumes, we should therefore see the company continue to produce steady cash flow growth well beyond the 2022 to 2024 projection period that we discussed in this article.

Financial Considerations

It is always important to analyze the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. As few companies have the ability to pay off their debt with cash, this is typically accomplished by issuing new debt and using the money to pay off the existing debt. This could result in the company's interest costs increasing following the rollover, depending on overall market conditions. In addition to this problem, a company must make regular payments on its debt if it is to remain solvent. Thus, a decline in cash flows can push a company into financial distress if it has too much debt. Although midstream companies like Enbridge tend to have remarkably stable cash flows, this is still a risk that we should not ignore.

The usual way that we analyze a midstream company's ability to carry its debt is by looking at the leverage ratio, which is also known as the debt-to-EBITDA ratio. This ratio essentially tells us how long it would take the company to completely pay off its debt if it were to devote its entire pre-tax cash flow to that task. In its first quarter 2022 earnings results , the company stated that it will have its leverage ratio down to 4.7x by the end of the year. This is admittedly a bit high, although it is below the 5.0x that analysts typically consider to be reasonable. One of the trends that we have seen over the past few years is midstream companies attempting to get this ratio down to less than 4.0x in order to improve the margin of safety. Enbridge's target range is 4.5x to 5.0x, which is higher than that of most of its peers given this shift in the industry. This could be concerning as it may be a sign that the company is using too much leverage with respect to its operations.

Dividend Analysis

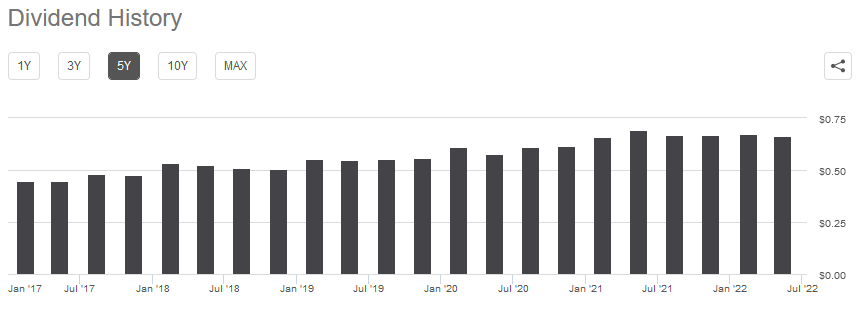

One of the biggest reasons that investors purchase stock of Enbridge is because of the historically high dividend yield that the company has boasted. Indeed, as of the time of writing, the company yields 6.20%, which is substantially higher than the 1.52% yield of the S&P 500 index ( SPY ). Enbridge also has a long history of steadily growing its dividend over time, although the exact amount varies depending on the exchange rate between the U.S. and Canadian dollars:

{kind=link}

The company's steadily growing dividend is very appealing during inflationary times, such as what we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that we receive. Anyone that has been to a gasoline station or grocery store recently can attest to this. The fact that the company increases the amount that it pays us helps to offset this effect and improves our ability to maintain our lifestyles. As is always the case though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want it to suddenly be forced to reverse course and cut the dividend since this would both reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge the ability of a midstream company like Enbridge to afford its dividend is by looking at a metric known as the distributable cash flow. This is a non-GAAP figure that theoretically tells us the amount of cash that was generated by the company's ordinary operations as is available to be distributed to the common stockholders. In the first quarter of 2022, Enbridge reported a distributable cash flow of C$3.072 billion, which works out to C$1.52 per common share. However, the company only pays a quarterly dividend of C$0.86 per common share. This gives the company a dividend coverage ratio of 1.76x, which is very reasonable. Analysts generally consider anything above 1.20x to be sustainable but I am more conservative and prefer to see this ratio above 1.30x to add a margin of safety to the investment. As we can clearly see, Enbridge more than meets these requirements. Overall, the dividend looks to be very safe and investors should not have to worry too much about a potential cut.

Conclusion

In conclusion, Enbridge has been one of the favorites among dividend investors for a very long time. There are good reasons for this as the company boasts stable cash flows that are positioned to grow over time and provide its investors with a very attractive 6.20% dividend yield. The long-term fundamentals are quite good here as the era of fossil fuels will not be coming to an end anytime soon and Enbridge is positioned to profit as demand grows over the coming years.

The only potential concern here is that the company's debt load is a bit higher than we really want to see, but it is not altogether unreasonable. Overall, the company is quite worth considering for any investor that is seeking income.

For further details see:

Enbridge: A Nice Way To Earn A 6.20% Yield