ENB:CC - Enbridge: Acquiring 3 Utilities From Dominion For $14 Billion

2023-09-06 10:17:50 ET

Summary

- Enbridge has reached three deals with Dominion Energy to acquire three utility companies for a combined value of $14 billion.

- The acquisition will make Enbridge the largest gas utility company in North America, expanding its footprint into several states.

- The deal is expected to strengthen Enbridge's dividend growth profile and be accretive to distributable cash flow.

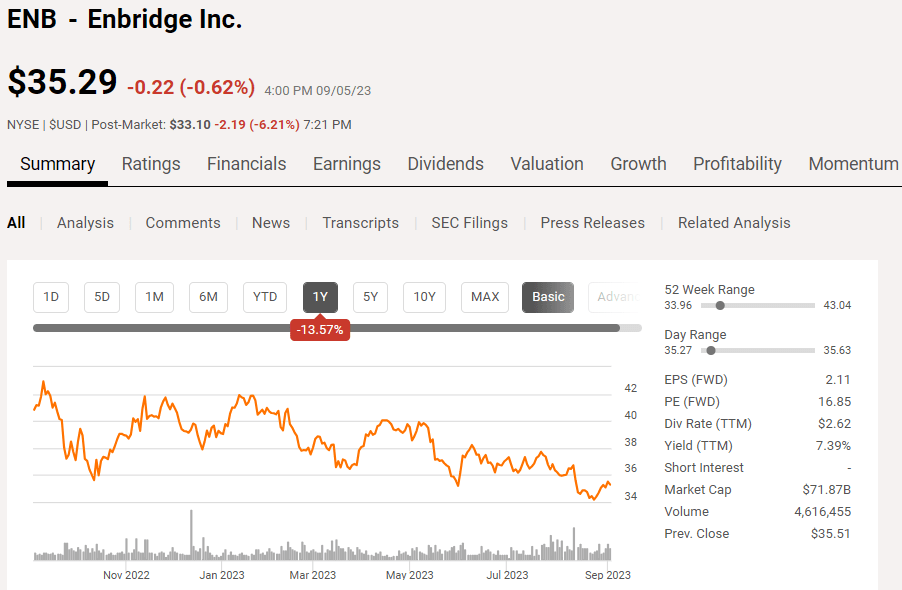

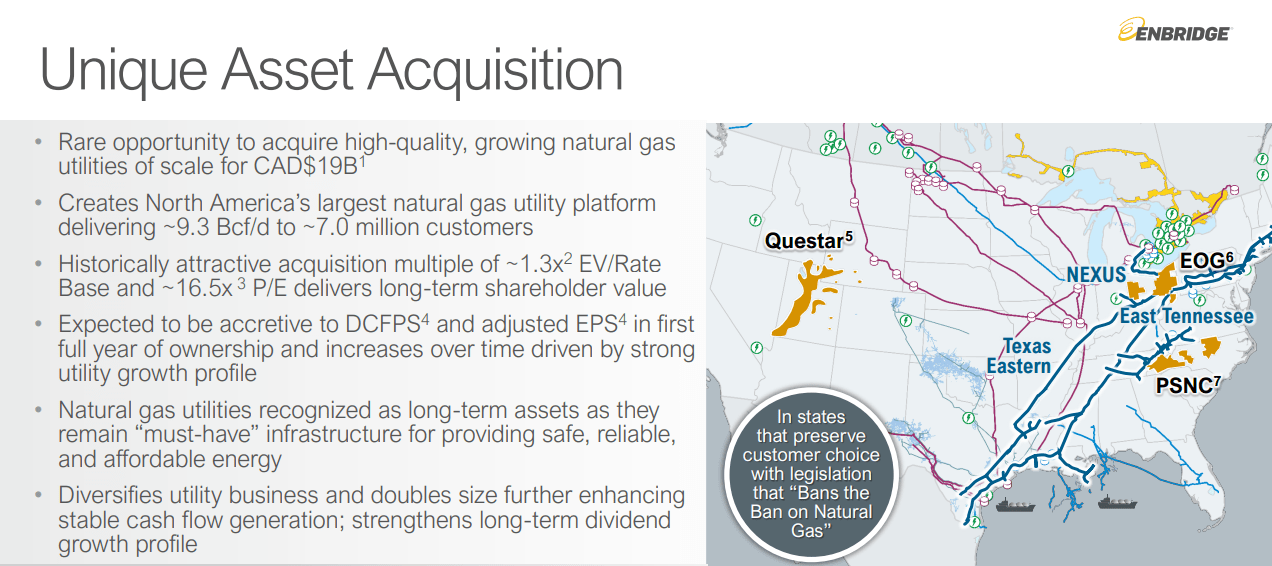

News just broke after hours that Enbridge ( ENB ), one of North America's largest energy infrastructure companies, has reached 3 deals with Dominion Energy ( D ) to acquire 3 utility companies from them. ENB will acquire East Ohio Gas Co, Questar Gas, and Public Service Company of North Carolina for a combined value of $14 billion. ENB will spend $9.4 billion in cash and assume $4.6 billion of debt from Dominion. ENB has indicated that they expect the deal to close sometime in 2024. In after-hours trading, shares of ENB have declined by -6.21%. I think this is a smart strategic move on ENB's part and I am planning on adding more shares to my position as this deal will make ENB the largest natural gas utility company across North America.

{kind=link}

Prior to this announcement, Enbridge had a long history in the gas utility business

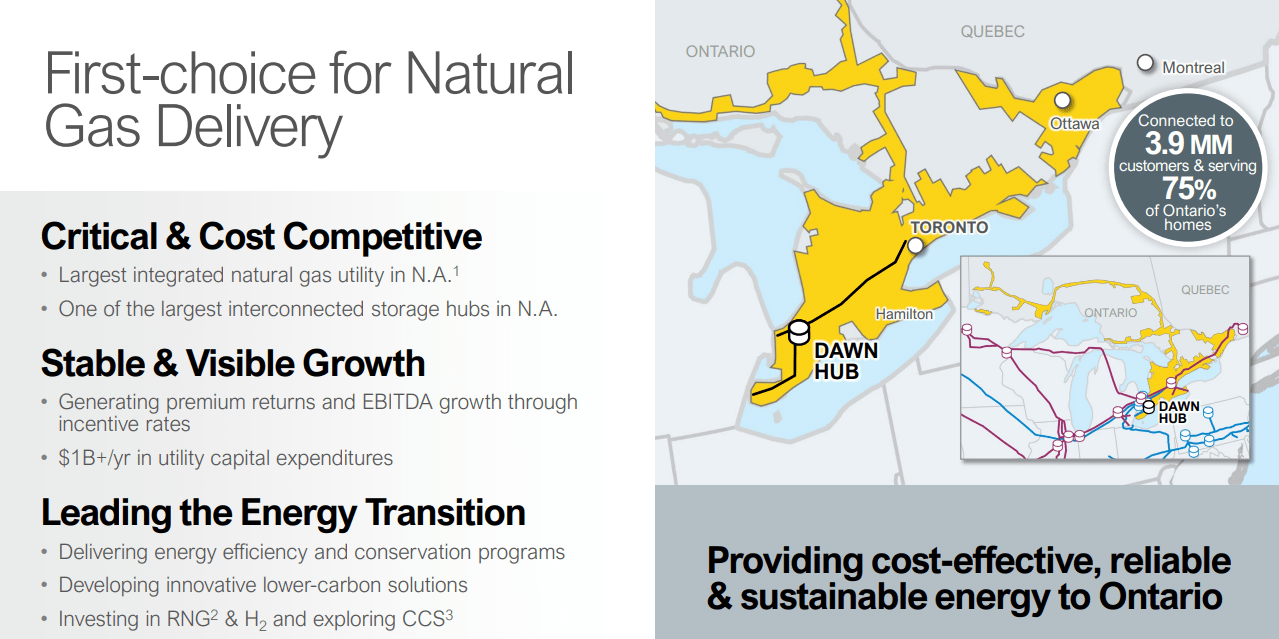

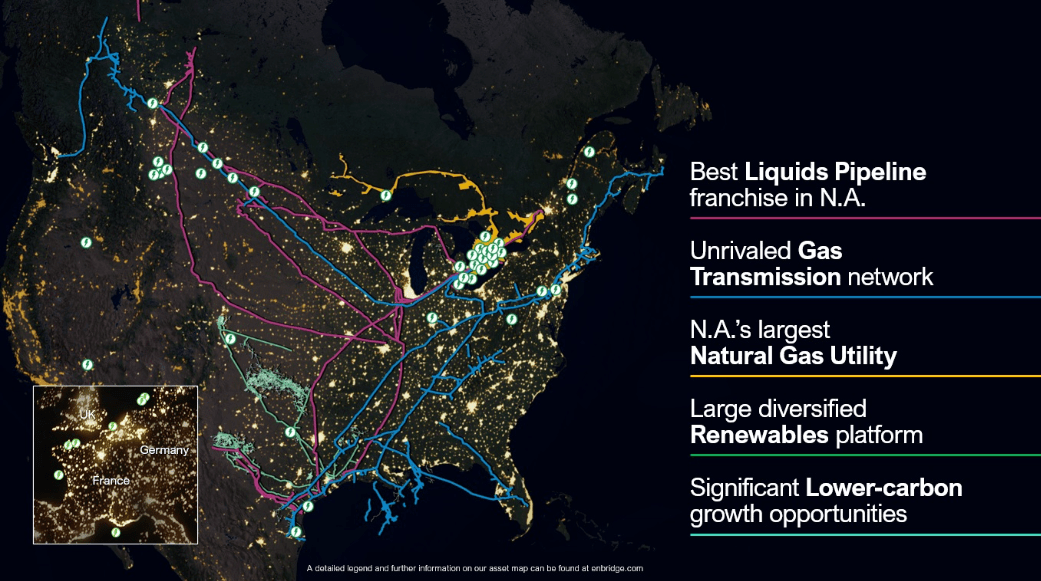

Prior to this announcement, ENB was the only major pipeline and midstream company that owned a regulated gas utility. ENB had operated North America's largest gas utility by volume and the 3 rd largest by customer count. Enbridge Gas Inc. has delivered energy for over 175 years, and within its infrastructure resides 52,505 miles of gas transportation and distribution mainlines and 41,631 miles of service lines. ENB provided 75% of Ontario's residents with their gas needs and provided service to 3.9 million customers, including both residential and commercial segments. ENB distributed over 5.9 Bcf/d of natural gas in 2022. On the storage side, ENB has 290.8 billion feet of working capacity.

This was one of the reasons why ENB was such an interesting investment. ENB was the only major pipeline company that was diversified throughout the utility industry and the renewable sector. In addition to owning and operating 73,796 miles of natural gas pipelines across North America, they also owned a utility company that provided service to the end users. ENB is a fully integrated company that can utilize its own pipes to move the natural gas needed to fuel its utility needs. This also diversified their asset mix and differentiated their earnings from their peers.

{kind=link}

The deal with Dominion Energy will make Enbridge the largest gas utility company in North America

Energy Transfer ( ET ) had continued its acquisition spree as they announced in the middle of August that they would be acquiring Crestwood Equity Partners, and ONEOK ( OKE ) had joined the purchasing wagon as they are looking to acquire Magellan Midstream Partners ( MMP ). In a previous article, I indicated that I felt more consolidation would occur across the energy infrastructure space, but I didn't think it would occur on the utility side.

I love this deal for ENB as it will transform them into the largest gas utility company in North America as it expands its utility entity into the United States. Once the deal closes, ENB will own The East Ohio Gas Company, Questar Gas Company and its related Wexpro companies, and Public Service Company of North Carolina. This will expand ENB's footprint into Ohio, North Carolina, Utah, Idaho, and Wyoming, which is a significant portion of the U.S. gas utility footprint. I like utility companies because of their low-risk regulated businesses that provide predictable cash flow.

These utility companies will double the scale of ENB's gas utility business to approximately 22% of Enbridge's total adjusted EBITDA. ENB will increase its footprint from delivering 5.9 Bcf/d of gas to 3.9 million people to servicing over 7 million customers by delivering 9.3 Bcf/d of gas. In total, ENB will add 56,000 miles of transmission, gathering, and distribution pipelines with over 60 BCF of storage and over 40 interconnections with 9 interstate natural gas pipelines.

{kind=link}

Natural Gas isn't going anywhere and gas utility companies will continue to be relevant

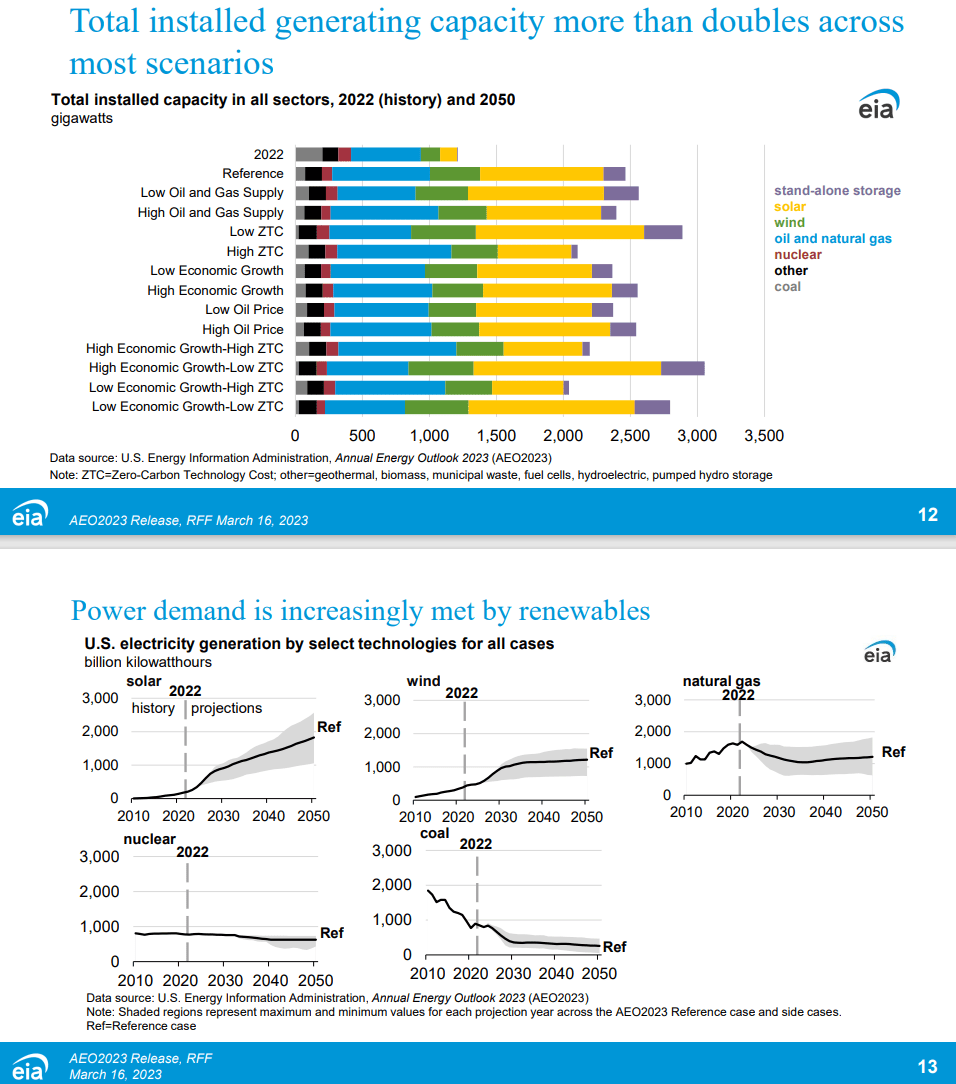

There has been a notion that solar and wind would eradicate the oil and gas industry as nations looked to transition to these renewable fuel sources. I am not against solar or wind power, and ENB has a large renewable portfolio to capitalize on the growing demand for these sources of energy. The EIA is predicting that the global energy demand will increase by 50% over the next three decades. As the demand for energy increases, the reality is that the void will need to be filled from all sources of energy, and unless there are drastic scientific breakthroughs, oil and gas will play a major role in providing sustainable energy for decades to come.

EIA

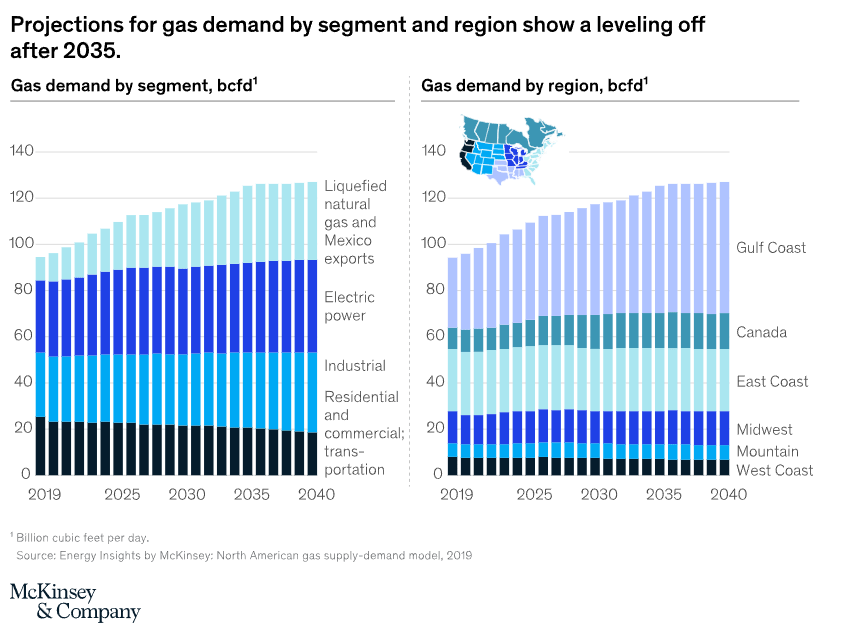

McKinsey & Company has projected that demand for natural gas in the United States will grow to 125 Bcf/d by 2035 and then plateau. Natural gas has been a tug of war regarding power generation as East and West Coast states have been passing legislation to move away from gas-fired power generation, while states in the Midwest, southern mid-Atlantic, and southern regions are continuing to rely on gas playing a major role in generation. In their base case, gas-fired power generation will displace coal capacity in the medium term and then nuclear over the long term.

{kind=link}

The Energy Information Agency ((EIA)) recently delivered its Annual Energy Outlook update and provided some critical information on the future of energy in the United States. The EIA has provided many different scenarios, and in most cases, oil and gas will expand from their 2022 levels through 2050 on a total installed generating capacity basis. The current trajectory is that wind and solar will see a large amount of growth, but even in the natural gas reference case for electricity generation, it will remain a major source of energy through 2050.

{kind=link}

This is why I like the deal for ENB, as they are becoming the largest gas utility in North America. I also feel that many individuals are not looking at the data being published by the EIA and are making assumptions based on feelings and emotions rather than facts. Natural gas will remain a critical energy source in the United States over the next 3 decades, according to the EIA, making this deal very interesting. Unlike companies such as Southern Company ( SO ), or Consolidated Edison ( ED ), ENB has a pipeline network that should create economies of scale for its utility companies, allowing ENB to benefit from owning and operating pipeline networks running near The East Ohio Gas Company, and Public Service Company of North Carolina.

{kind=link}

This deal strengthens the dividend which is music to my ears

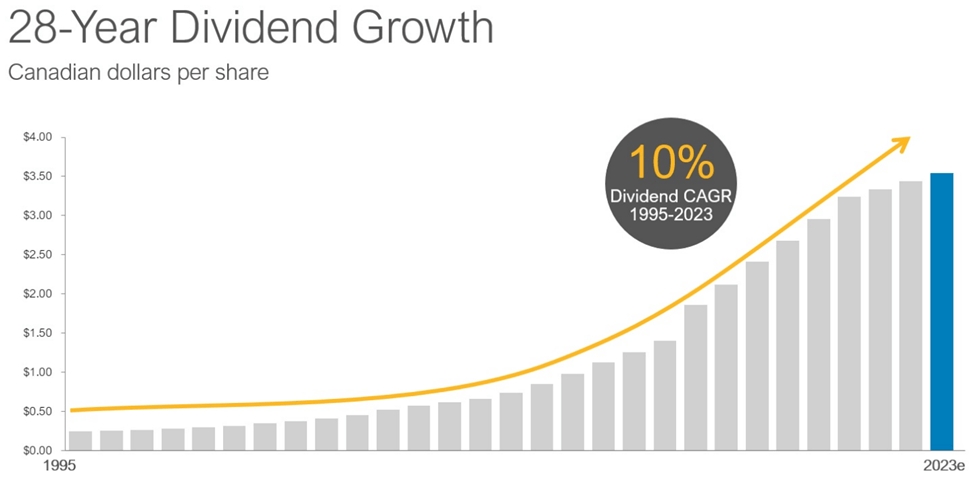

ENB expects that this acquisition will be accretive to distributable cash flow accretive to distributable cash flow in the first full year of ownership. They expect that this will increase over time as their growth backlog of projects comes online. ENB is maintaining its 2023 financial guidance in addition to its near and midterm outlook. ENB's funding plan for these utility companies will allow ENB to maintain leverage within its target range of 4.5x to 5.0x Debt-to-Adjusted EBITDA. ENB has indicated that this deal is expected to improve the long-term dividend growth profile as it further diversifies and de-risks its business operations.

In their most recent investor day presentation, ENB projected that its EBITDA could have a CAGR of 4-6% through 2025 while its distributable cash flow ((DCF)) grows at a 3% CAGR. Due to ENB's capital investments, they feel that its EBITDA and DCF can grow at around 5% annually, which could drive its forward dividend to grow at a 5% CAGR. ENB has provided annual dividend increases for the past 28 years at a 10% CAGR since 1995. The fact that management feels these utility assets can strengthen the dividend growth profile indicates that their previous projection of a 5% CAGR could be low after the deal closes and their new growth projects are brought online.

{kind=link}

Conclusion

Shares of ENB have fallen, and I am going to buy more in my Dividend Harvesting Portfolio series on Seeking Alpha ( can be read here ) and in my main dividend accounts. If, for some reason, the regulators reject the deal, I feel shares were undervalued at $35.29, and after the dip after hours, they are even more attractive to me. I like investing in companies that own physical assets and provide critical services. ENB's infrastructure is virtually impossible to replace, and this deal will make it the largest natural gas utility company in North America in addition to being one of the largest pipeline and renewable companies. I plan on adding to my position and reinvesting the dividends for years to come as the demand for energy will continue to increase, and ENB is a critical player from the production of renewables to the transportation of oil and gas and the distribution of power through its gas utility. After the dust settles, I feel ENB will be back over $40 sooner rather than later.

For further details see:

Enbridge: Acquiring 3 Utilities From Dominion For $14 Billion