ENB - Enbridge: Is It Too Late To Buy This 8%-Yielding Dividend Aristocrat?

2023-12-11 07:38:44 ET

Summary

- Since initiating coverage on Enbridge, the stock has rallied about as much as the S&P 500.

- The midstream behemoth shared impressive financial results for the third quarter ended September 30.

- Enbridge’s industry leadership and robust financial position earn it a BBB+ credit rating from S&P with a stable outlook.

- Shares of Enbridge appear to still be priced at a 24% discount to fair value, which is a satisfying margin of safety.

- Assuming the current growth forecast is correct and the company reverts to the mean, Enbridge could top the total returns of the S&P 500 by a wide margin through 2033.

Dividend growth investing is as simple as picking high-quality businesses in industries with demand that can grow steadily over time. That's because great businesses plus growing industries often translate into dependable dividend growth.

The midstream giant Enbridge ( ENB ) is a business that I believe fits these two requirements. Having just upped its annualized dividend per share by 3.1% to 3.66 (0.915 per quarter) Canadian Dollars, the company extended its dividend growth streak to 29 consecutive years .

However, the stock has rallied 10% since my article in October . For context, that's about as much as the 11% that the S&P 500 ( SP500 ) has gained during that time in hopes that the Federal Reserve can pull off a soft landing.

This raises the following question that I pose in the headline of this article: Is Enbridge a buy after this rally and its recent dividend raise? To answer this question, I will highlight the company's third-quarter operating results, its balance sheet strength, and its valuation.

{kind=link}

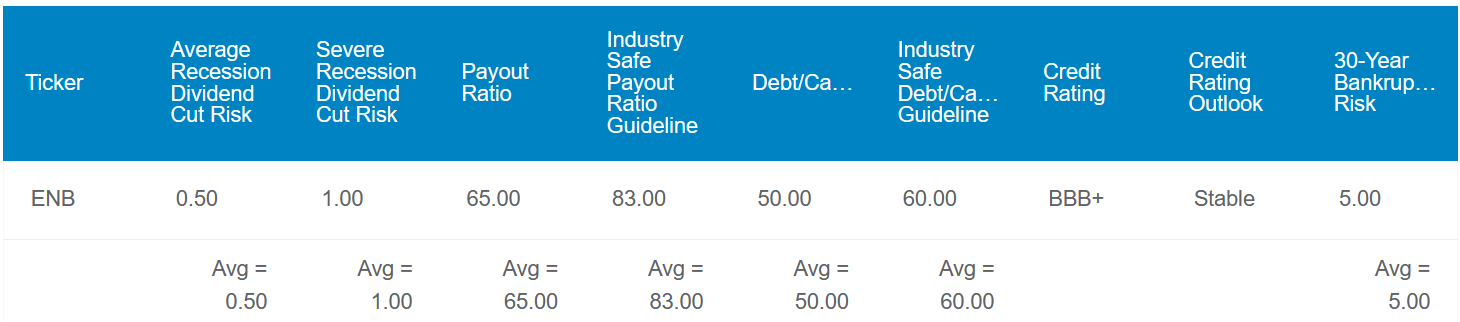

Enbridge's 7.7% dividend yield is substantially higher than the 4.2% yield of the 10-year U.S. treasury at this time. The spread of 350 basis points is 10 basis points more than when I last covered the company. Yet, Enbridge's dividend arguably remains as safe as ever. The company's 65% DCF payout ratio leaves it with a sizable buffer, versus the 83% DCF payout ratio that rating agencies consider sustainable for the midstream industry.

Enbridge's 50% debt-to-capital ratio is also below the 60% debt-to-capital ratio that credit rating agencies like to see for the industry. Thus, the company enjoys a BBB+ credit rating from S&P on a stable outlook. According to Dividend Kings, this implies the probability of Enbridge defaulting on debt in the next 30 years is 5%. Overall, that's also why Dividend Kings pegs the risk of the company slashing its dividend in the next average recession at just 0.5%.

{kind=link}

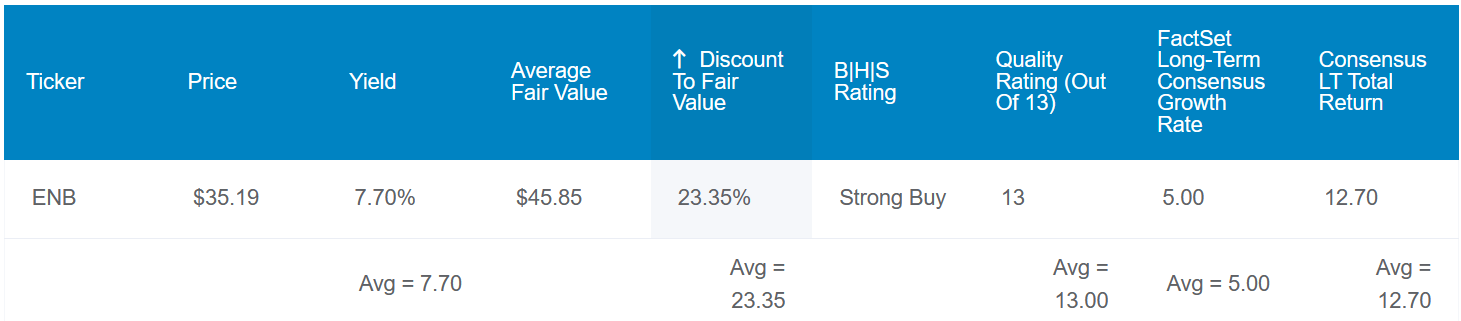

Enbridge's solid operating fundamentals and impressive balance sheet earn it a 13/13 ultra SWAN quality rating from Dividend Kings. Better yet, the stock also looks to still be cheap after its recent rally. Enbridge's current $35 share price (as of December 9, 2023) represents a 24% discount to its $46 fair value per historical valuation metrics like dividend yield.

If Enbridge meets growth expectations and returns to fair value, here are the total returns that could be in store for the coming 10 years:

- 7.7% yield + 5% FactSet Research annual growth consensus + 2.8% annual valuation multiple expansion = 15.5% annual total return potential or a 322% 10-year cumulative total return versus the 9% annual total return potential of the S&P 500 or a 137% 10-year cumulative total return

Delivering For Shareholders

{kind=link}

When Enbridge reported its third-quarter results last month, it unsurprisingly posted yet another quarter of respectable results.

Here are some of the more pertinent takeaways from CFO Pat Murray's opening remarks on the Q3 earnings call :

In liquids, our systems remain highly utilized, the mainline transported just under 3 million barrels per day, a record for third quarter volumes. In the Gulf Coast, Ingleside also posted record volumes, and we realized a full quarter of contributions from the increased economic interest in Gray Oak and Cactus II.

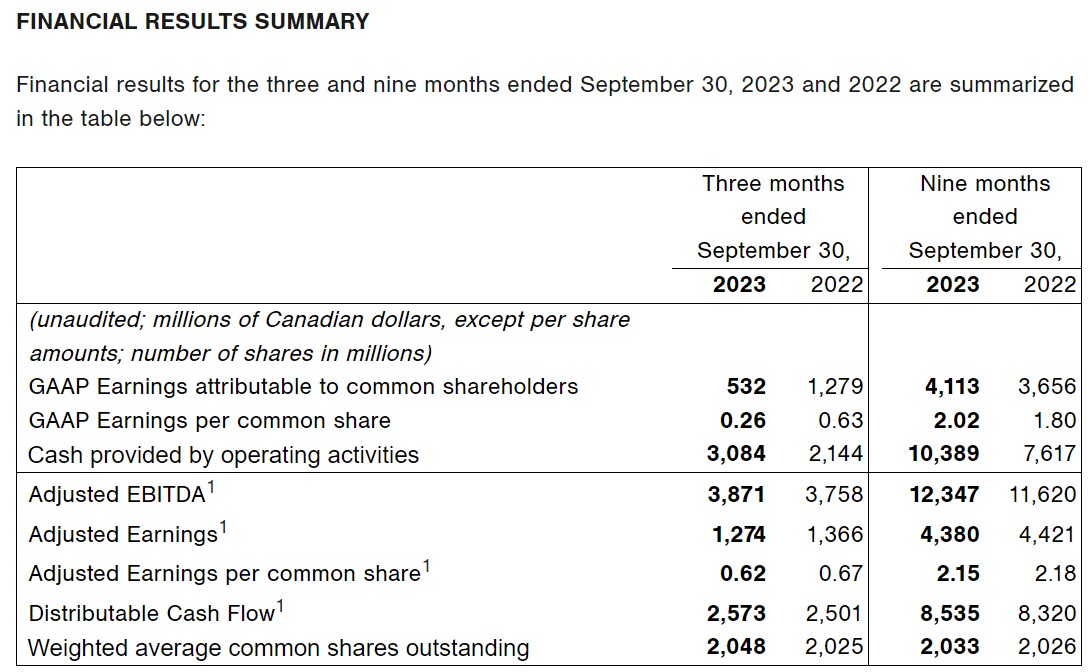

Thanks to these growth catalysts, Enbridge's adjusted EBITDA edged 3% higher over the year-ago period to 3.9 billion CAD during the third quarter. Inclusive of a higher share count, Enbridge's DCF per share grew by 1.7% year-over-year to 1.26 CAD for the quarter. The company's increased financing costs resulting from rising interest rates mostly explain how DCF per share growth lagged behind adjusted EBITDA growth in the quarter.

{kind=link}

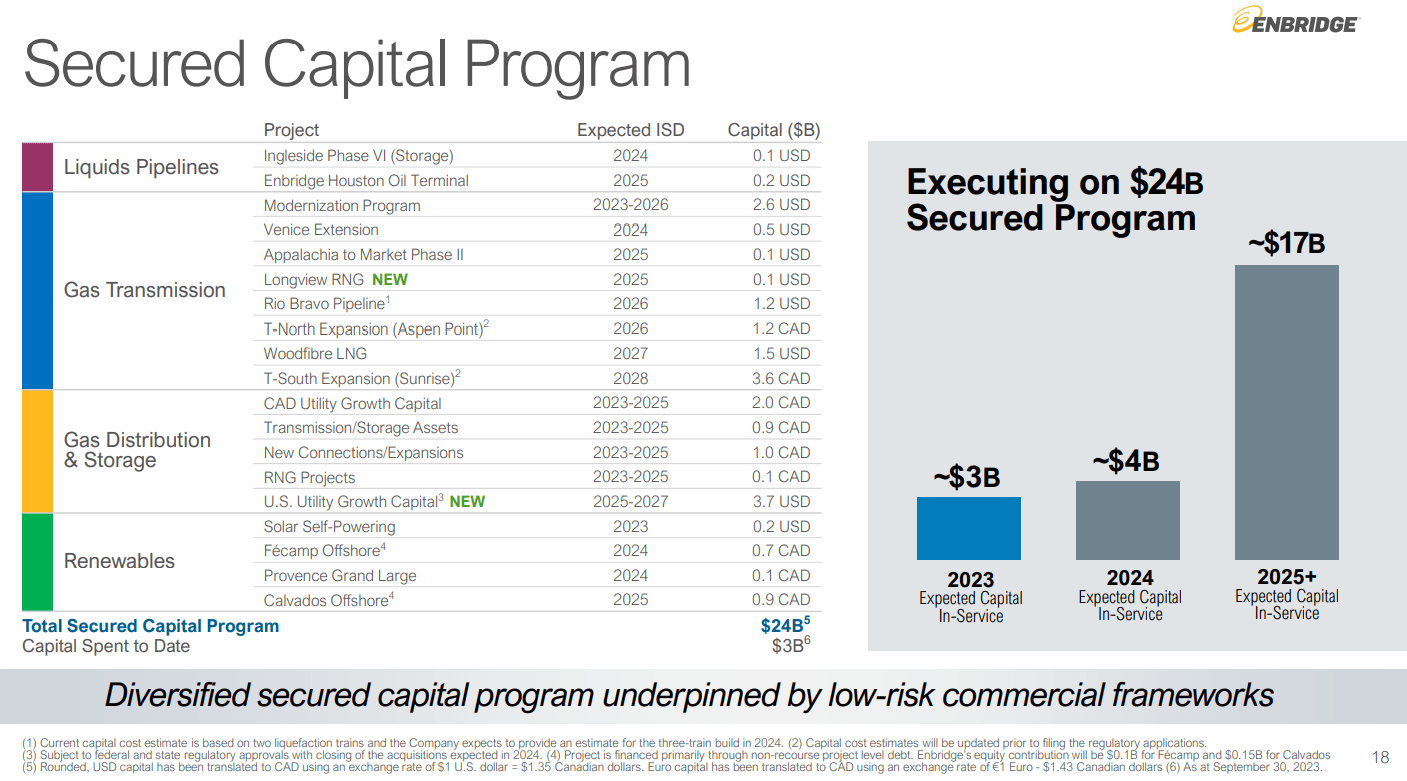

Enbridge's results moving forward should be just as strong. This is because, over the next few years, the company has 24 billion CAD in projects that are expected to come into service. Projects with expected in-service dates for next year include the Ingleside Phase 4 liquids storage terminal expansion, the Venice gas transmission extension, and the 497-megawatt Fécamp Offshore Wind Project off France's northwest coast.

Due to the upcoming completion of these projects and its strong existing business, Enbridge projects that its base business EBITDA will rise by 4% over the midpoint of its 2023 guidance. The company also thinks that its midpoint DCF per share will grow by about 3% in 2024 to 5.60 CAD over its midpoint 2023 guidance.

Finally, Enbridge is largely shielded from higher interest rates heading into 2024: The company estimates that only about 10% of its total interest expense is subject to floating rates. Enbridge's 4.5X debt to EBITDA ratio is also at the low end of its 4.5X to 5X range that it is targeting. Combining these factors with a customer base that is 95%+ investment-grade (details sourced from Enbridge's Q3 2023 Earnings Presentation ), it's not hard to understand why S&P rates Enbridge's debt BBB+ on a stable outlook.

Enbridge's Dividend Isn't Finished Growing

As remarkable as Enbridge has been at upping its dividend in the last three decades, there is reason to believe it is far from done doing so.

The company generated 4.20 CAD in DCF per share through the first nine months of 2023. Compared to the 2.66 CAD in dividends paid over that time, this works out to a 63.3% DCF payout ratio. This is well within the company's 60% to 70% targeted payout ratio, which is why I am reiterating my expectation of 3% to 5% future annual dividend growth.

Risks To Consider

Enbridge is a business that continental North America would have a tough time doing without, which makes it an appealing investment option. However, the company isn't for everyone.

As a Canadian company, taxable accounts are exposed to the 15% Canadian withholding tax. Fortunately, the easiest way to avoid this tax and not have to file for a tax credit to recover this withholding come tax time is to own the security in a tax-advantaged account like an IRA.

Natural disasters pose an operational risk to Enbridge. Floods, hurricanes, tornadoes, and fires could damage its infrastructure beyond insured amounts. That could hurt the company financially. Disruptions to operations from such events could also weigh on the company's results.

Another operating risk to Enbridge is the location of its pipelines and distribution systems near heavily populated areas. A safety incident could result in not only injury or loss of life to its workers and contractors, but to members of the public as well. This could lead to significant damage to the company's reputation and sizable legal liabilities.

Summary: A Compelling Pick For Income, Growth, And Value

Enbridge has had a nice runup in the last handful of weeks. However, for my money, I still like it here. The company's recent operating results affirm its quality in my mind, as do the variety of projects that it has in the works to drive growth.

Also, Enbridge's investment-grade balance sheet appears to remain strong. Furthermore, the company's market-crushing 7.7% dividend yield is well-covered. Finally, Enbridge's 24% discount to fair value provides investors with an adequate margin of safety in my opinion. While I don't rate the stock a strong buy as I did in October, I am comfortable still rating it as a buy.

For further details see:

Enbridge: Is It Too Late To Buy This 8%-Yielding Dividend Aristocrat?