ENB:CC - Enbridge: Jagged Little Debt Pill (Rating Downgrade)

2023-03-07 16:46:26 ET

Summary

- Enbridge Inc. is probably the best in its class.

- Debt is becoming a problem for the class, though, and dividend investors should keep an eye on rising interest rates.

- We rate Enbridge stock a hold at current levels, but might test the water at a lower price.

Introduction

Everything is on the energy side of the stock supermarket sale these days. You could almost throw a dart at a list of energy stocks and come away with a winner. Hold your horses, and take your finger off that "unfollow" button...I said, "almost." The downdraft in producers I sort of get in the face of oil and gas price declines. The same for the OFS companies. But, the fact the toll-taking midstream sector is down 20-30% suggests that factors other than the business fundamentals are in play. In this article we will look at one factor in particular that may be sending investors scurrying for cover. It's a new era and debt is a four-letter word.

Enbridge Inc. ( ENB ) is a solid dividend payer with a strong track record of paying a fairly stable high yielding dividend-through good times and not-so-good times. Probably no higher compliment can be paid to the company. Except for one little thing. They have been balancing the books (dividends, growth capex, interest payments) with debt. The TTM payout ratio is 269% for 2022.

{kind=link}

Readers should also review my past articles on the company for color and depth. The most recent of which was in September of 2021 , so a reasonable amount of time has elapsed, and it's time for another look. In that outing, I gave Enbridge Inc. a buy rating, but it was a different era. Low interest rates meant debt was just a detail on the balance sheet. When a maturity came up, it was rolled into a new one, often at a better interest rate than before. "The time's they are a changing," as we will posit.

Enbridge is a dividend play, pure and simple. Investors looking for growth should probably continue their search. Enbridge stock is already selling for 13X EBITDA, and I don't see that multiple expanding a lot in the current environment. What they offer is above-average, long-term, low-risk income - for now . The debt monster could come calling in years ahead. I regard ENB as Best In Class, in no small part for their Class-C Corp structure which avoids the IRS K-1 morass. ( Feel free to take this up with your tax advisor if you wish more information on K-1s. ) This not necessarily a reason to buy the stock at this level, as we will discuss in the rest of this article. Best In Class, does not mean, "First Class."

Why is Enbridge a dividend play?

The company is in the business of moving different classes of hydrocarbons from one place to another through pipes buried underground-mostly. They also have end point storage along the Texas Gulf Coast and Suezmax/VLCC wharfage in Corpus Christie. (Much of this was discussed in the September, '21 article linked above.)

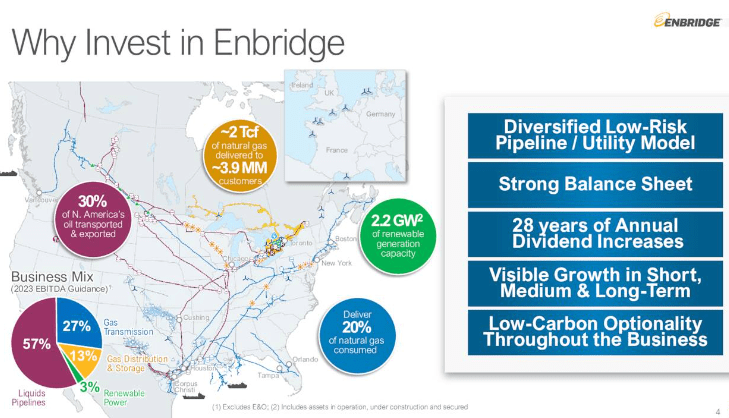

You can get an idea of their various footprints from the slide below. Recently the company has made a low-carbon foray into windfarms in Europe to leverage high electricity prices, and in the U.S. made a $3bn acquisition of an onshore windfarm developer - Tri Global Energy . We won't elaborate much on the low-carbon stuff, as it's an obvious play on the Inflation Reduction Act - IRA , hog-cutting , that's been pretty well discussed by myself and a couple of thousand other authors. Bottom line, it's a Federal Pork-barrel cash grab, and they would be poor stewards of capital if they didn't haul some in.

{kind=link}

The Enbridge "tolling" business model is fairly standard in the industry. Units go into the system, usually under long-term contracts, and a fee is paid for transit. Conceptually it insulates them somewhat from fluctuations in commodity prices, but as a practical matter, they feed at the same trough as producers. When the market turns sour, they catch the flu, too, albeit with a delay of sorts as their volumes decline. ENB is currently beset with the oil and gas price "flu" which creates the opportunity we now have to scoop up shares at a discount to recent pricing. But, should we?

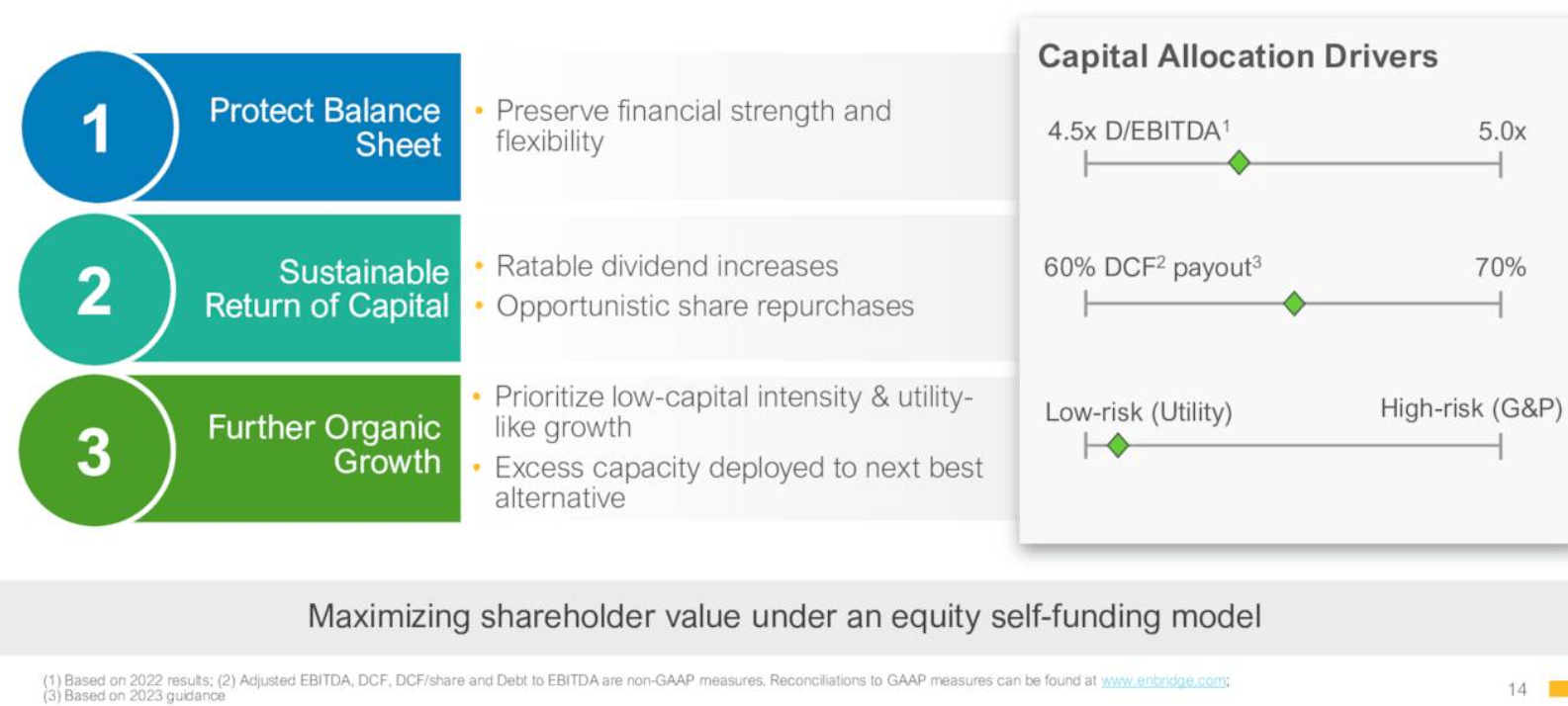

Three other things keep the stock price from ever reaching escape velocity. The first is debt. They are in a capex-intensive business and carry an inordinate amount of it - currently some $53 bn USD, a figure at which they've been chipping away recently as interest rates have risen. It was $56 bn a year ago, so that's $3 bn to the good. You might explain away carrying this amount of debt in the interest rate era that wound up in late 2021. It's already starting to show up on the balance sheet as ENB paid about $250 mm more interest YoY from 2021-2022. It should be noted, as they do in the slide below that ENB doesn't consider this debt excessive, and it is well managed with cash flow on their balance sheet....so far. The debt here is worrisome in a rising interest rate environment... to me, anyway.

{kind=link}

Now, this debt concern is certainly not to cast any doubt on their liquidity, about $10 bn at present. I am speaking to dividend investors here, and the company is currently paying out ~$3.5 bn in interest on a TTM basis. Much more of this type of action and the math might not work on the dividends. The company has very little cash, so capex and dividends are funded with cash flow...and debt.

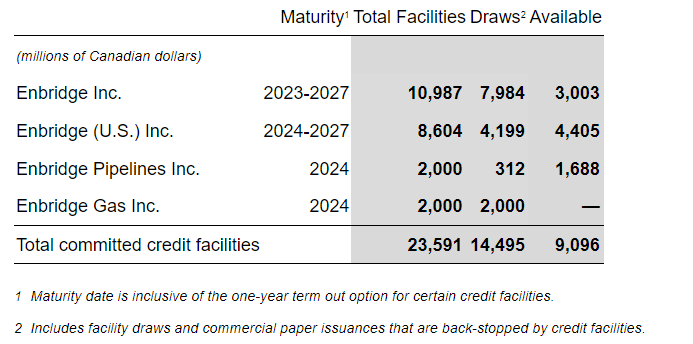

You can see below what their near-term debt picture looks like. 2027 is a long way off, and who knows what interest rates will be then.

{kind=link}

2022 was a year of substantial debt rescheduling for ENB. They have $1.9 bn due in May, '23, $5.5 bn in July of '24, and another $12.7 bn due between 2024 and 2027.

With TTM cash flow running in the range of ~$8.3 bn, normalized capex of ~$4.5 bn, $3.5 bn of interest charges, and a dividend obligation of ~$5.1 bn, you can see we are deeply into "new math." ( Math that is way too complicated for old mud engineers. ) My 50-year-old Rockwell Tr-9 calculator tells me that ENB is going to have to dip into that pool of liquidity to make ends meet. In that scenario, interest charges are going higher, leading to concerns in the next few years about the ability to fund the dividend at the current level. Ok, I am done with this rant. Moving on.

The next thing that hobbles Enbridge Inc.'s stock from going higher is never-ending legal exposure. Everybody hates pipelines these days, from environmental groups, to FERC - the federal regulator for pipelines - to the indigenous tribes that seem to have ancestral hunting grounds and water supplies along every pipeline route from Canada to the U.S. Gulf Coast. ( I am exaggerating a hair here. But not much.) On the plus side, the tribal objections can be often overcome with a liberal dose - $10's of millions - of monetary largesse. As Mary Poppins said, "A spoonful of sugar..." I digress.

The environmental and regulatory bodies are a different scenario, though, as they are driven, not by money, but by idealogues with a green vision of the future. A vision in which pipelines will play no role because hydrocarbons will be phased out, so there will be no reason to have pipelines. ENB's travails at replacing Line-5 in Michigan are as good a case in point as you will ever find. A Bloomberg article notes:

Michigan has been in court for years with Calgary-based Enbridge in an effort to shut down Line 5, fearing a disaster in the Straits of Mackinac, the ecologically sensitive region where the pipeline crosses the Great Lakes.

The legal saga, however, has been dominated almost from the start by arcane procedural questions about jurisdiction and precedent, with Tuesday's decision likely to deepen that morass even more.

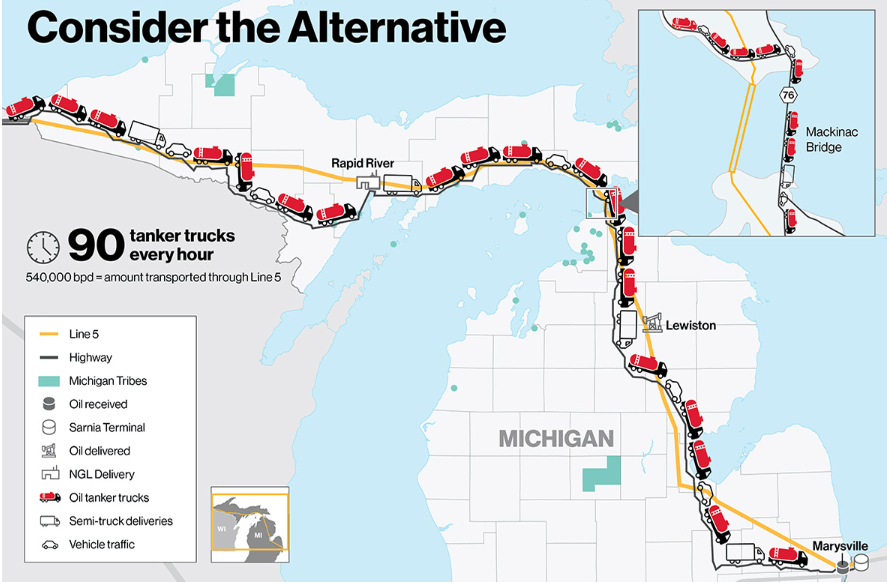

It's a fight made even more absurd by the fact Line-5 is the primary source of supply for about half a million BOPD of propane and NGLs - 65% and 55%, respectively - upon which thousands of Michiganders rely for winter heating. Enbridge estimates that 2,100 tanker trucks daily would be needed to replace it.

{kind=link}

It is a fairly safe bet that many of the people engaged in fighting ENB on Line-5, or in cheering on those who are, would be adversely affected were it to really shut down.

Finally, there is the political/NIMBY-Not In My Backyard, problem with pipelines. Curiously, no one wants to live near one. Particularly in the crowded Northeast, where pipelines can run close to urban centers. News of an impending pipeline permit stirs up a lot of emotion in the affected places. That can create an overhang in the mind of fund managers that an investment in ENB will have enviro-activists storming their annual meetings, and gluing themselves to portraits of board members. Here, as with the environmental lobby and regulators, there's just not much you can do to ameliorate the objections!

Q4 2022 and 2023 guidance

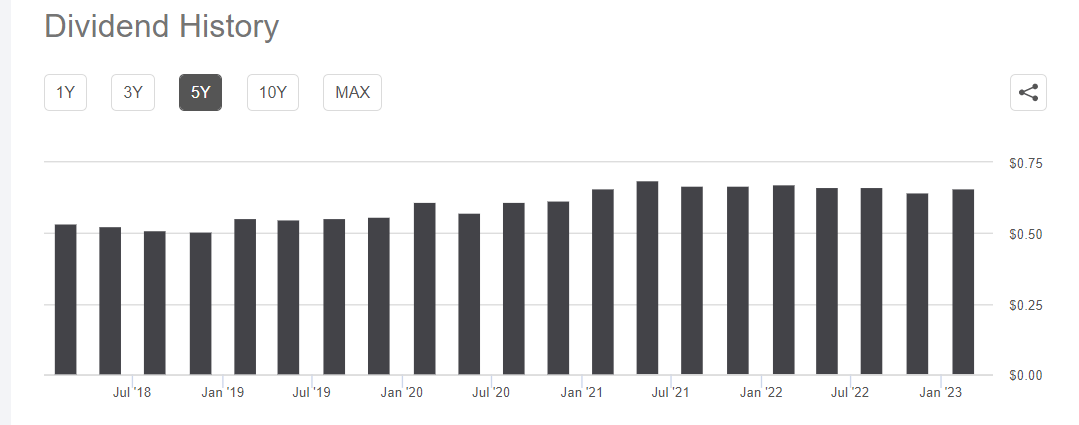

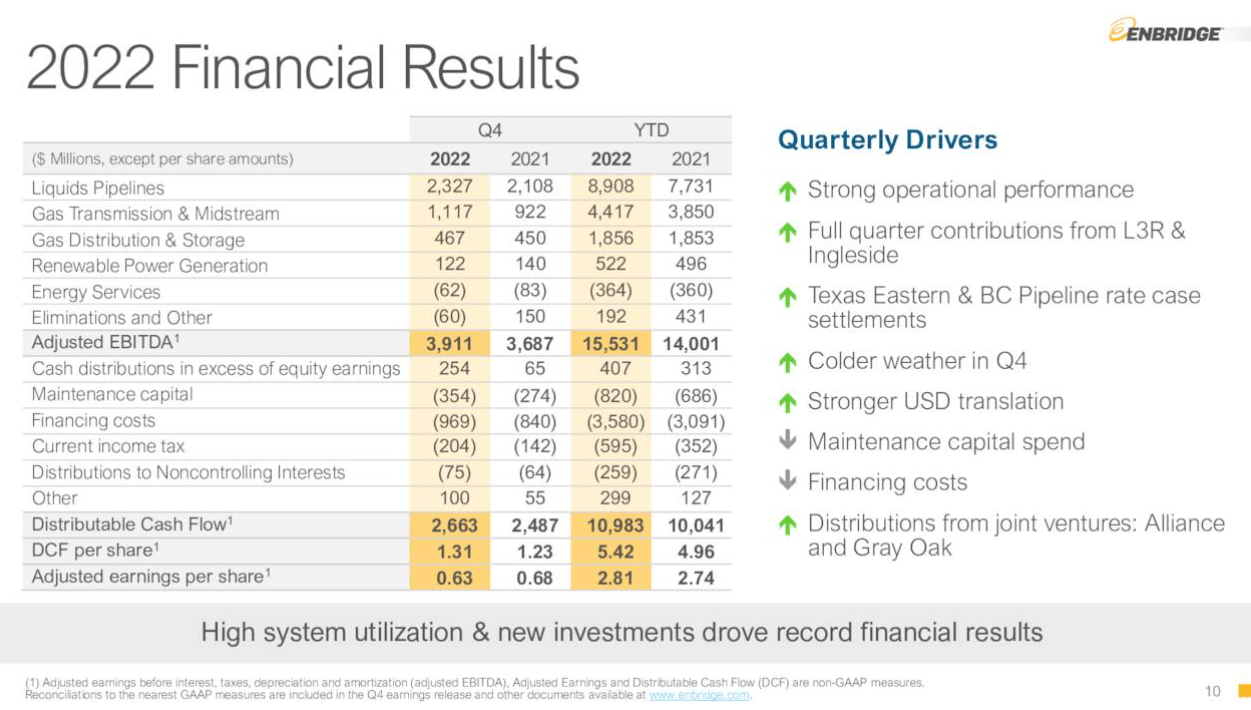

ENB missed on the top and bottom lines for Q4 2022 , thanks to the selloff in commodities, but still turned QoQ and YoY improvements in result as can be seen below. Of particular interest to investors was the ~9% increase in discounted cash flow ("DCF") for the year, from the results of 2021. That translated to a roughly 10% increase in the payouts, which, it should be noted, beat the worst of the inflation rate.

{kind=link}

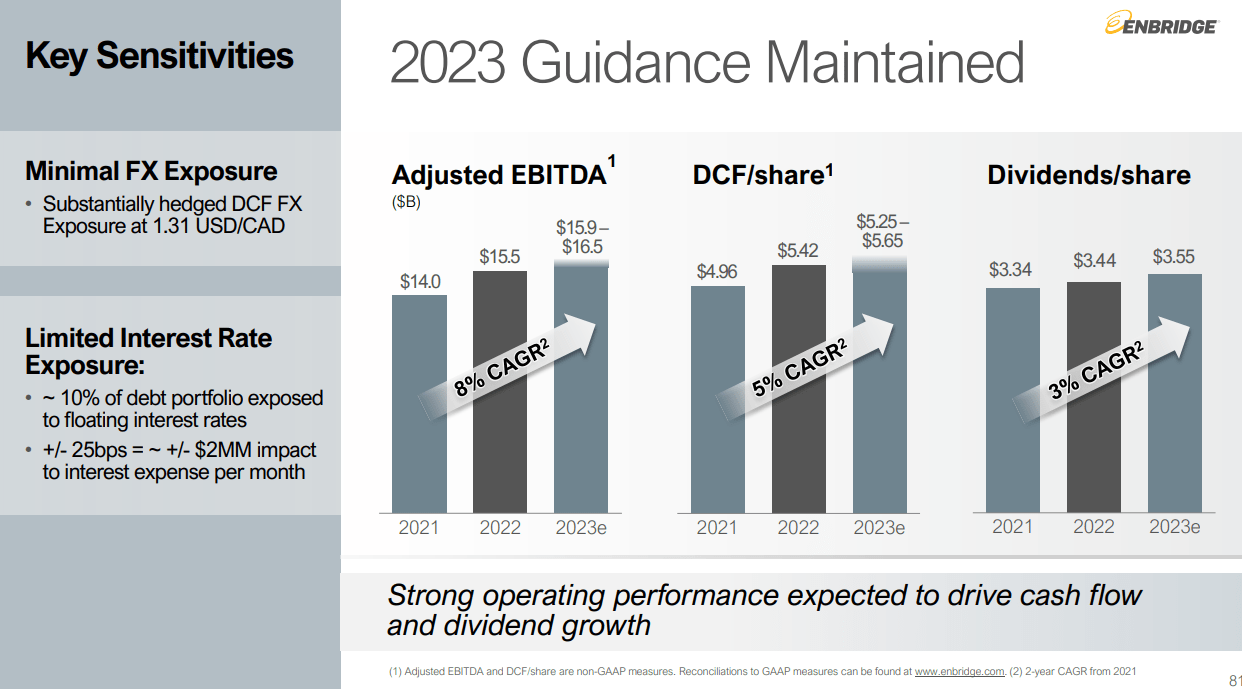

The company is guiding for approximately 8% CAGR growth in EBITDA, leading to further increases in DCF and dividends for 2023.

{kind=link}

Your takeaway

If you take anything away from this article, I think it should be that Enbridge Inc. has billions of dollars worth of assets in place that can and have delivered growth in revenues and EBITDA on a quarterly and annual basis. Speaking to dividend investors, of which I am one, I can't think of a high-yielding sector with less risk than pipelines over the short term. They may have their ups and downs, but they provide an essential service to millions of people on a daily basis, and I am betting they are here for the long haul. But is Enbridge Inc. the one to buy? Best in class or not, there are other options in this space.

I waxed on a good bit about the debt, and with some justification in my view. That said, I am in no way suggesting Enbridge Inc. is in any sort of crisis. There are many levers to pull when these maturities come due. I am just saying interest costs are rising and may rise faster than cash flow. In that scenario, the dividend could come under the axe.

ENB is on sale in relation to its recent high, but not cheap in comparison to its main competitors. It is trading at 13X EV/EBITDA, right in line with its 10-year historical average. For reference competitors Energy Transfer LP ( ET ) and Enterprise Products Partners L.P. ( EPD ) are yielding slightly higher-9.3% and 7.5%, respectively, and with lower EV/EBITDA multiples-both about 7.5X.

Should we buy ENB for yield? In my view, it comes down to the corporate structure disparity. I dislike dealing with K-1s so much I will pay a higher multiple to avoid them. But not nearly double. At the current multiple, I think there are better options, and they are not necessarily ET or EPD. I am not going to make a direct comparison with them until I have a chance to write them up. A company is more than just its Enterprise Value multiple.

No, what I am thinking of is an exchange-traded fund, or ETF, that will focus on the sector. For example, Global X MLP ETF ( MLPA ) yields 7.21% and carries none of the various risks we've discussed for ENB in this article, outside of the entire sector crashing - this has happened, and pulling the ETF down with it. We discussed MLPA in an article a while back, and you should give it a read if this sector interests you.

Bottom line, I am long MLPA, and would not consider buying Enbridge Inc. at its current EV/EBITDA multiple. If the dividend yield were to get substantially back above 8%, then it might go on the list. But not until then. Remember, risk-free Treasury rates are near 5% now.

For further details see:

Enbridge: Jagged Little Debt Pill (Rating Downgrade)