ENB:CC - Enbridge: On The Verge Of A Major Bottom (Rating Upgrade)

2023-12-13 13:00:23 ET

Summary

- Enbridge Inc. stock has markedly underperformed its leading energy infrastructure peers despite a planned acquisition to become North America's largest gas utility platform.

- Concerns remain over Enbridge's debt exposure and its near-term impact on earnings available for distribution.

- However, Enbridge's high-quality earnings should support improved buying sentiments as the Fed reaches the end of its rate hike regime.

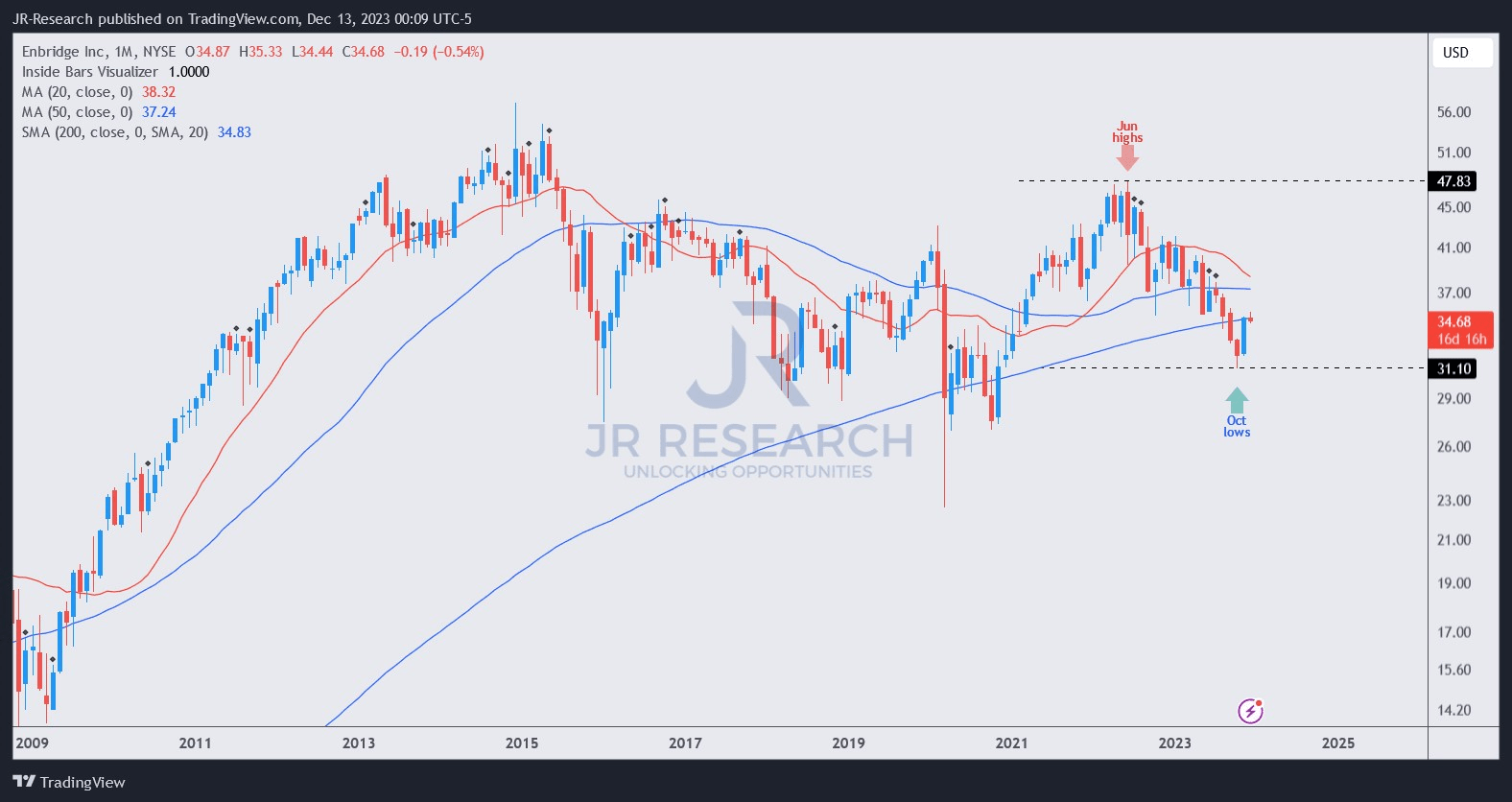

- I assessed that moment has likely arrived in October as ENB likely bottomed out, as dip-buyers returned with conviction.

- I argue why investors should return and benefit from its bottom and snap up its relatively attractive 7.7% forward dividend yield.

Enbridge Inc. (ENB) investors are likely in a bind as ENB continues to underperform its leading energy infrastructure peers, even as it looks to close the gas utilities acquisition from Dominion Energy ( D ) in 2024. Management explained that it had already pre-funded C$8.3B of the C$12.8B cash consideration for the acquisition. In addition, the company has committed to staying within the adjusted EBITDA leverage ratio of between 4.5x and 5x, helping to mitigate investors' concerns about its increased debt load.

The planned acquisitions are expected to lift Enbridge into "North America's largest gas utility platform." However, the updated 2024 guidance provided by management doesn't include the modeling from these planned acquisitions. As a result, investors could remain in a state of flux over the execution risks emanating from the purchases as Enbridge looks to capitalize on the synergies to bolster its increased scale and improve its utility-like earnings profile for its investors.

{kind=link}

As a result, ENB holders must wonder whether its relative underperformance against its peers could soon end, as it posted a total return of -7% over the past year. ENB significantly underperformed Energy Transfer ( ET ) stock in this comp set, as ET posted a 1Y total return of nearly 25%.

Enbridge's premium "D+" valuation likely didn't help, suggesting investors could be pricing in a much slower earnings growth phase while accounting for higher debt risks from its recent acquisition. Management attempted to assure investors that the company had sufficiently hedged its interest rate exposure as it updated its 2024 outlook in late November. Accordingly, Enbridge underscored that its updated guidance "accounts for higher interest rates on planned new fixed-rate financings and outstanding floating-rate debt." As a result, the company expects to "limit interest rate variability exposure to less than 10% of the debt portfolio by the start of 2024."

Keen observers should recall that management's recent update suggests a 2024 adjusted EBITDA range of between $16.6B and $17.2B for a midpoint metric of $16.9B. The company also telegraphed a DCF per share outlook of $5.6 at the midpoint of its guidance range for FY24.

Wall Street estimates are pretty much in line, suggesting analysts expect Enbridge to be on track in meeting its outlook, which could provide more confidence to investors. However, concerns will likely remain over the company's debt exposure, affecting its earnings available for distribution. Accordingly, Enbridge highlighted " higher financing costs resulting from higher interest rates" at its Q3 release. Given that these assets aren't expected to be accretive to DCF per share until 2025 (pending close), near-term interest exposure risks could still dominate investors' concerns as ENB isn't priced at a discount relative to its peers.

{kind=link}

Notwithstanding my near-term caution over the visibility of Enbridge's earnings, I gleaned that buyers returned with conviction since ENB bottomed out in October 2023. With the 10Y ( US10Y ) falling below 4.2% this week, it could have attracted income investors to return to the fray, as the company remains in a solid position to improve its distribution over time.

With ENB still valued at a forward dividend yield of nearly 7.7%, it seems relatively attractive as the Fed potentially reaches the end of its rate hike regime. A potentially more aggressive rate cut cadence could bolster ENB's relative appeal to alternative income-generating assets. However, it might not be necessary, given the high quality of Enbridge's earnings (rated "A-" for profitability).

As a result, I view the improved buying sentiments at ENB's $31 support level as constructive, helping it to bottom out at the pivotal 200-month moving average or MA (purple line). As long as ENB could hang on to its long-term MA and grind higher from here, I'm confident we could have seen its long-term bottom.

Rating: Upgraded to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn't? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Enbridge: On The Verge Of A Major Bottom (Rating Upgrade)