TRP - Enbridge: Strong Income From Inflation Protected Pipelines

- Enbridge is currently hitting on both cylinders: Demand and volumes are strong for both its Canadian oil sands pipelines and its U.S. nat gas pipelines (acquired from Spectra in 2017).

- Demand for Canadian oil sands product is very strong because demand for heavy oil to refine into diesel is very strong.

- Demand for U.S. nat gas/LNG is strong because Russian supply to the EU is constrained by Putin and a summer heat wave is boosting demand from electric power gen plants.

- The potential for Western Canadian LNG offers significant future upside for Enbridge while cancellation of Keystone-XL is an opportunity for ENB to gain market share.

- Meantime, ENB offers excellent, safe, and moderately growing dividend income. The current yield is 6.1%.

As most energy investors know, Enbridge ( ENB ) operates the Mainline oil pipeline transportation system that not only carries ~70% of all Canadian oil exports, but that is delivers oil which is highly integrated into U.S. refineries complexes (notably the 50-50 Cenovus ( CVE )/ Phillips 66 ( PSX ) WRB Joint Venture ). ENB also owns and operates substantial large-scale natural gas interstate pipeline assets in the United States that deliver ~20% of all the nat gas consumed in the U.S. However, many investors are unaware or under-appreciate Enbridge's natural gas utility business, which is why I wrote a Seeking Alpha article specifically covering that segment (see Enbridge: The Seasonally Prosperous Union Gas Utility ). All that said, the outlook for new large-scale interstate O&G pipelines going forward is certainly not as good as it was in the past. That being the case, today I want to discuss the growth opportunities that Enbridge does have while pointing out that its current 6.1% yield is very attractive. And safe.

Investment Thesis

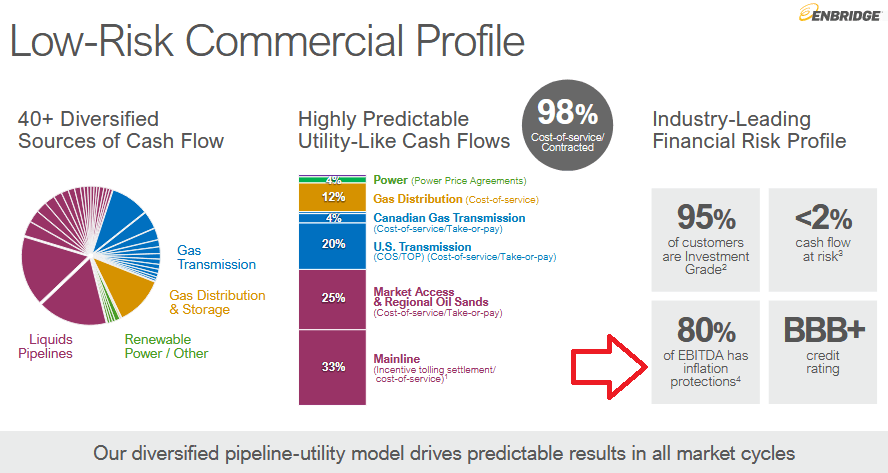

Enbridge is the largest O&G infrastructure company in North America, and it has a very solid and low-risk commercial profile that has utility-like cash flow predictability as well as built-in inflation protection covering 80% of EBITDA:

{kind=link}

Enbridge 2022 Investment Day

Source: May 2022 Investment Day Presentation

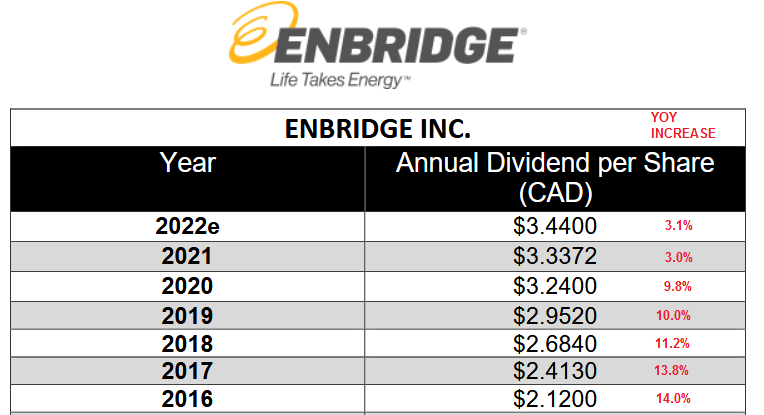

Following its acquisition of Spectra in 2017, ENB met its dividend growth commitments to shareholders and that was a very positive catalyst for a few years. However, since those commitments, ENB's dividend growth story has slowed dramatically along with the prospect of new large-scale pipeline projects due to all the court and environmental battles that have added significant delays and additional costs for ENB big pipeline projects (like Line 3 and Line 5):

{kind=link}

Enbridge

[NOTE: Red annotations added by the author.]

As can be seen from the graphic above, dividend growth was very strong from 2016-2020, but has averaged only 3% since. That being the case, investors are likely asking a simple question: What will power dividend growth going forward? That's what I will discuss today.

Growth Moving Forward

While ENB has several organic growth projects to strengthen its base business, the truth of the matter is that ENB is now so big (market cap of $89 billion while the midpoint of FY22 adjusted EBITDA guidance is C$15.3 billion) that such small organic growth projects, in aggregate, simply are not enough to move the needle. Likewise, the Union Gas and Renewable Power segments, while performing just fine, are also not big enough to move the needle.

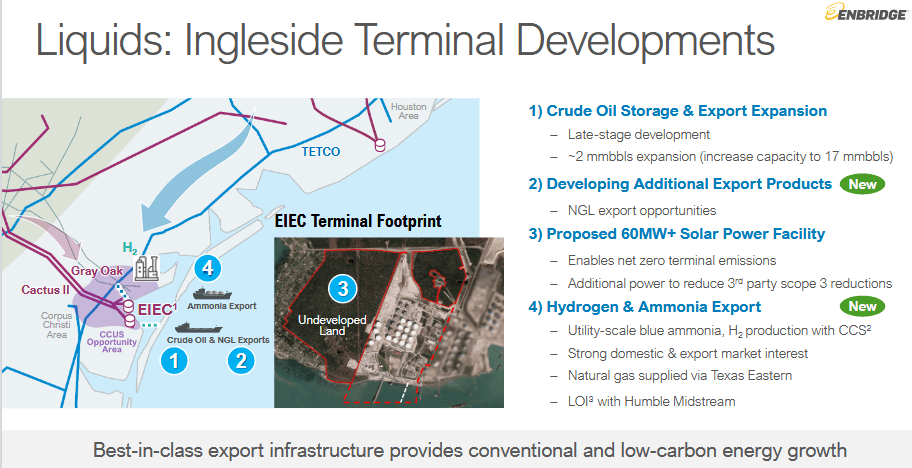

One avenue for growth is obviously M&A. Enbridge flexed its muscles last year by closing the $3 billion purchase of the Ingleside Export Terminal in Texas. The acquisition, which includes a 20% interest in the 670,000 bpd Cactus Pipeline as well as excellent crude oil export potential, also opens up new avenues for growth in the export of NGLs and possibly hydrogen and ammonia as well:

{kind=link}

Q1 Presentation

In the midterm, Enbridge is in an excellent position to benefit from the cancellation of the Keystone-XL pipeline, which would have been a competitive threat to the company. Last year, TC Energy ( TRP ) - the -XL pipeline operator - finally called it quits and cancelled the -XL pipeline for once and for all. That puts Enbridge in an ideal position to build new organic pipeline expansions to serve the needs of producers who were heretofore depending on -XL for additional capacity and production growth.

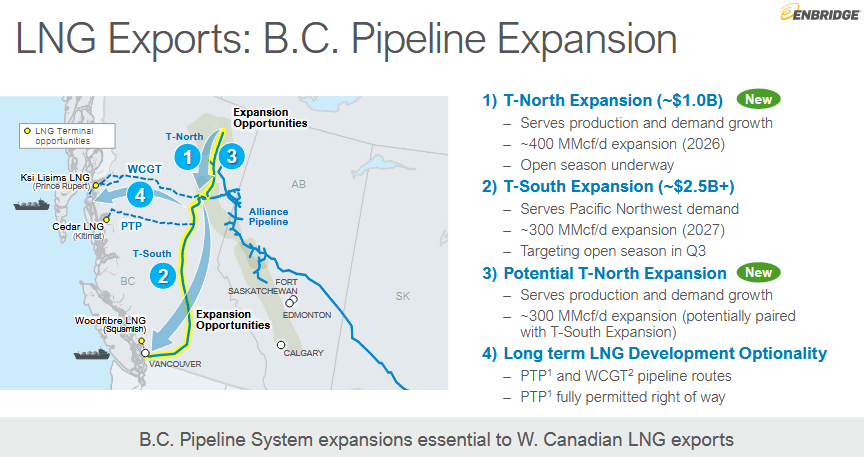

Longer term, Enbridge has excellent potential to benefit if the Canadian energy sector ever gets off its collective duff and opens up LNG export terminals on its Western Coast to take full advantage of its massive Deep Basin natural gas assets:

{kind=link}

Q1 Presentation

The much closer proximity to Asia as compared to U.S. Gulf Coast LNG terminals makes Western Canadian LNG export terminals such a no-brainer, I'm still amazed they are not already in operation today. Time will tell when (if?) these long-dreamed of Canadian LNG terminals actually come online. If they do, ENB is well positioned to benefit.

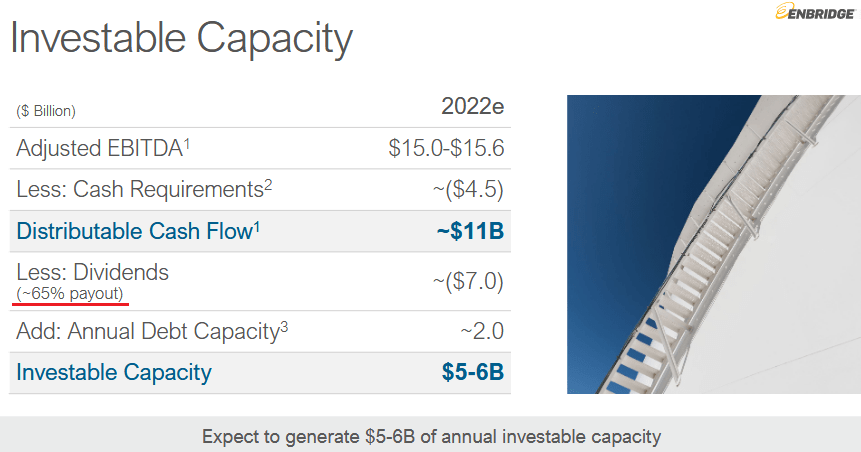

However, the biggest hope for dividend growth in the short term is actually very simple: Enbridge management simply needs to change their somewhat arbitrary target of returning only 65% of DCF to shareholders:

{kind=link}

Enbridge: 2022 Investor Day Presentation

I say that because at times it appears that Enbridge management is pushing on a string to over-invest capital in large-scale pipeline development projects when that strategy frequently leads to regulatory conflict and big delays and costs over-runs that have in the past been a big waste of shareholder capital. In other words, perhaps ENB management simply needs to be more pragmatic and acknowledge the fact that the growth and invested capital rates of pipeline growth projects in the past simply no longer make sense.

That being the case, if ENB changed its DCF payout ratio to say a more reasonable 75%, that would be a huge windfall for shareholders: DCF for dividends would jump from the $7 billion (shown above) to $8.25 billion. With 2.03 billion shares outstanding at the end of Q1, the extra $1.25 billion would open up the potential for an additional C$0.62/share of dividend income for shareholders. That's obviously a very significant increase, considering the quarterly dividend declared today (Tuesday, July 26) was C$0.86/share.

Risks

Other than the long-term risks associated with EVs, global warming, and the potential for much reduced oil demand in the coming years, ENB's dividend - at least in the short and midterm, looks very secure (i.e., see the payout ratio as a percentage of DCF shown above).

A possible shut-down of the Dakota Access Pipeline ("DAPL") would negatively affect ENB's Mainline volumes. Meantime, investors should recognize that Canadian oil sands are some of the least environmentally friendly sources of oil production on the planet. On the other hand, ENB has excellent exposure to the cheapest and cleanest fossil fuel: natural gas.

Meantime, another way ENB could increase dividends would be to reduce growth cap-ex targets in order to pay down its considerable debt load. Despite its excellent cost-of-service and utility type businesses, ENB's credit rating is only BBB+. That's largely because the company has a whopping $56.4 billion of long-term debt . Note that interest expense in Q1 was a relatively large C$733 million, or - annualized, close to C$3 billion a year. That's huge and, in my humble opinion, ENB's debt load should be reduced sooner rather than later in my opinion. That would not only reduce interest expense, but lead to higher DCF and, eventually, higher dividends for investors.

Summary And Conclusion

Enbridge is performing very well at the moment, given strong demand for both the oil and natural gas it transports through its large-scale pipelines. Though dividend growth has slowed significantly of late, I still view Enbridge's 6.1% dividend yield as very attractive. That's because, despite all the hoopla about rising interest rates, the U.S. 10-year Treasury still yields only 2.79% . Speaking of inflation, note that most of ENB pipelines are covered by inflation adjusted rate increases.

Longer term, ENB has several potential growth avenues that could lift its recent dividend growth profile. However, the biggest potential for dividend growth would come simply from a pragmatic decision by ENB management to raise the DCF payout ratio to better reflect potential growth prospects until they actually materialize. But don't hold your breath. Meantime, I rate ENB a HOLD and relatively attractive for investors seeking safe and secure O&G pipeline based income.

I'll end with a 10-year price chart of ENB stock and note that - like so many energy stocks - the stock price is not far from where it was 10-years ago. That being the case, the primary investment thesis for ENB is dividend income, not total returns.

For further details see:

Enbridge: Strong Income From Inflation Protected Pipelines