DAVA - Endava: Finally Trading At A Compelling Price

2023-03-21 06:02:14 ET

Summary

- Endava has dropped over 60% after hitting its all-time high in 2021.

- The company continues to be a huge beneficiary of the increasing adoption of digital transformation.

- Despite facing a tough macro backdrop, its latest earnings still demonstrated strong top-line growth.

- Current valuation is discounted when compared to peers.

- I rate the company as a buy.

Investment Thesis

Endava ( DAVA ) has performed well since going public in 2018, as it benefited from the pandemic that boosted the adoption of technologies. However, the company has pulled back over 60% from its all-time high in 2021 as the market sentiment turned south due to rising rates and inflation. I believe the drop should be temporary and offers a great buying opportunity for investors. Despite the volatility surrounding the economy, digital transformation remains a priority for companies, which should continue to drive demand. The latest earnings also showed little slowdown as top-line growth is still very upbeat. The company’s valuation now looks attractive as multiples are below peers and its own historical averages, which should offer meaningful upside potential.

The Digital Transformation Tailwind

Endava is a London-based digital consulting company founded in 2000 by John Cotterell. The company provides digital transformation services through fast-growing technologies such as Cloud, e-commerce, and digital payments. It works hand in hand with customers from generating ideas to prototyping and to actual production. It has a strong presence in Europe and the UK with 62% of revenue generated from the region. Current customers include notable names such as Bain, BBC, and Rakuten ( OTCPK:RKUNY ). The company has been gaining strong traction as the adoption of digital transformation continues to increase, especially after the pandemic which made companies realize how critical technologies are. It is also benefiting from companies outsourcing transformation work to third parties due to the complexity and cost of labor.

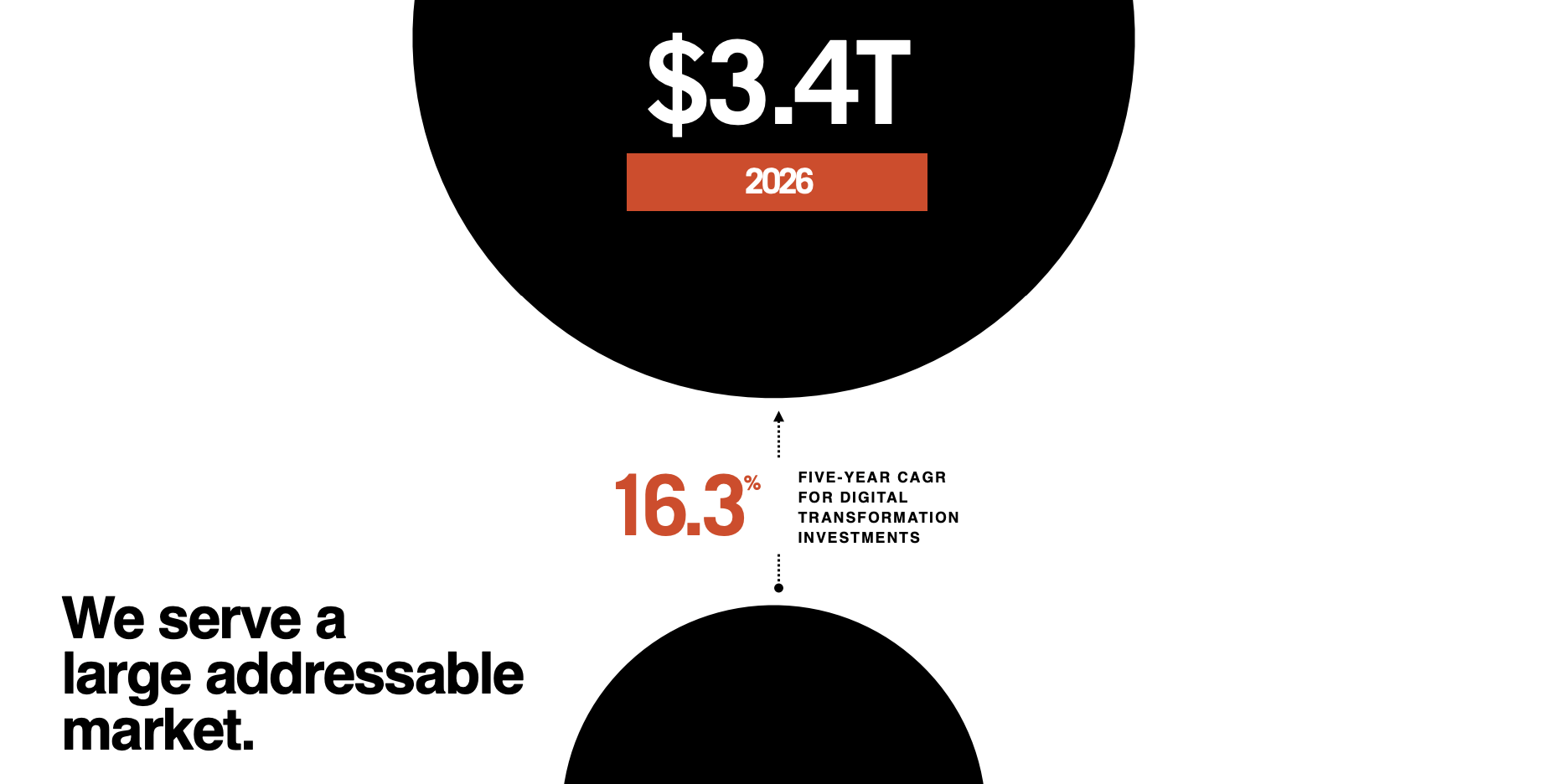

While we have made meaningful progress in the past decade, I believe digital transformation is still only in its early innings. For example, the recent emergence of ChatGPT has shown the world how impactful generative AI could become in the future. According to Precedence Research , the TAM (total addressable market) of AI is forecasted to grow from $119.8 billion in 2022 to $1.59 trillion in 2030, representing an insane CAGR (compounded annual growth rate) of 38.1%. Most companies have no choice but to adopt the latest technologies, or else they will be at a significant disadvantage against competitors. Thanks to increasing adoption, the TAM of digital transformation is forecasted to grow at a CAGR of 26.7% from $880.3 billion in 2023 to $4.6 trillion in 2030, according to Grand View Research . Endava themselves also estimates the investment in digital transformation will grow at a CAGR of 16.3% to $3.4 trillion in 2026. The increasing pace of technological change should continue to be a strong growth driver for the company.

{kind=link}

Financials

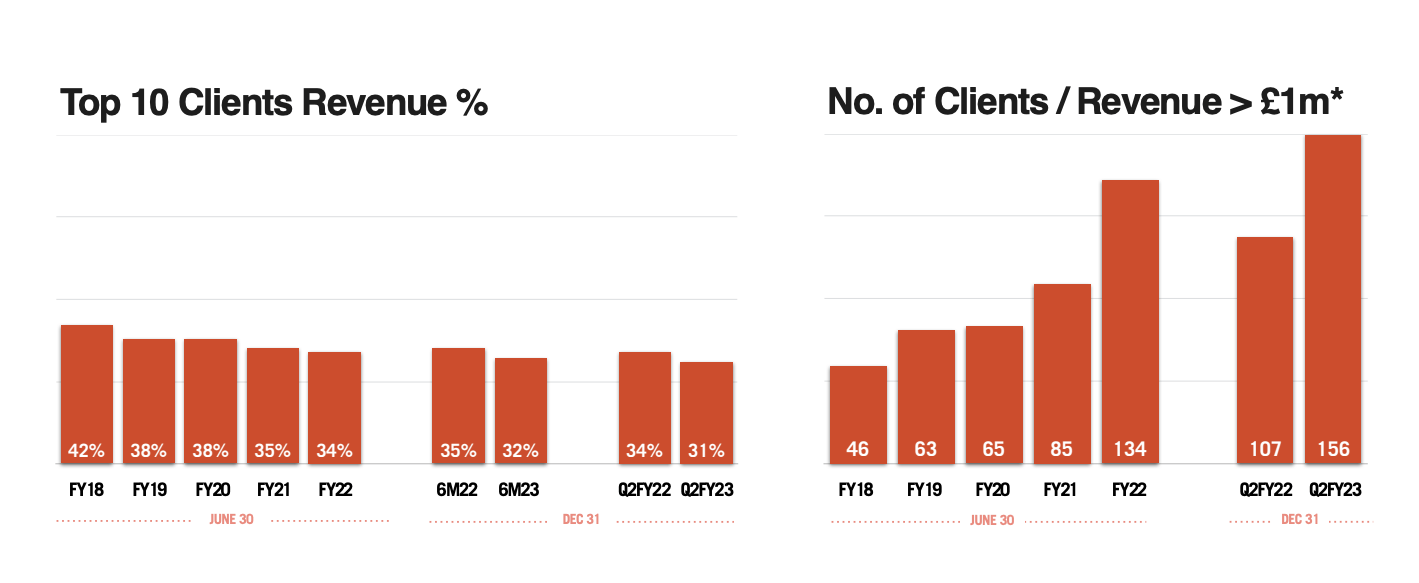

Endava announced its second-quarter earnings last month and it continued to show impressive top-line growth as demand remained strong. The company reported revenue of £205.2 million, up 30.2% YoY (year over year) compared to £157.7 million (the company reports in Pounds as it is based in the UK). On a dollar basis, revenue growth was 23.4%, as the pound weakened significantly against the dollar during the year. The growth is driven by the increase in high-paying clients and spending. The number of clients with over £1 million in revenue increased 45.8% from 107 to 156. The average spend for the top ten customers grew 20.4% from £5.4 million to £6.5 million. While the average spend for the remaining customer grew 15.8% from £298 thousand to £345 thousand.

John Cotterell, CEO, Q2 results

Even with the global economic uncertainty, digital transformation remains a priority for our clients and they value the transformation services we are delivering. Demand from new and existing clients continued to drive revenue growth in the quarter, leading to a revenue increase of 23.4% in constant currency for Q2 FY2023.”

As the increase in costs of sales moderated, the gross profit margin expanded 230 basis points from 33% to 35.3%. Gross profit also increased by 39.4% YoY from £52.1 million to £72.5 million. SG&A (selling, general and administrative) expenses as a percentage of revenue also dipped 210 basis points from 20.3% to 18.2%, as the company benefited from better operating leverage. This resulted in the operating income increasing 69% from £19.4 million to £32.8 million. The diluted EPS was £0.26 compared to £0.27. This is not comparable due to financial expenses unrelated to operations. The company’s balance sheet remains extremely healthy with £185.3 million in cash and only £67.3 million in debt.

{kind=link}

Valuation

After the 60% drop in share price, Endava’s valuation is finally looking compelling. The company is currently trading at a PE ratio of 32x, which is pretty discounted compared to both peers and its own historical average. For instance, other notable digital consulting companies such as EPAM Systems ( EPAM ) and Globant ( GLOB ) are trading at a PE ratio of 39.5x and 42.7x, as shown in the chart below. This represents a meaningful premium of 23.4% and 33.4% respectively. It is also worth noting that Endava’s revenue growth in the latest quarter was the highest among the group at 30.2% compared to EPAM System’s 11.2% and Globant’s 29.2%.

On a historical basis, the valuation appears to be even cheaper. Its current PE ratio is near its historical low and represents a 63.6% discount compared to its 5-year average of 88x. However, it is worth noting that the sample size for historical averages is limited as the company has only been public for 5 years, therefore it may not be the most accurate reference.

Investor Takeaway

I believe Endava should perform well in the long run thanks to the ongoing adoption of digital transformation. As new technologies such as generative AI emerge, the pace of change will only accelerate even faster. Investment in digital transformation should remain a priority for companies as it improves efficiency and strengthens competitive advantages. This should provide strong resilience for demand even if the economy further weakens over the course of the year. The company's current valuation is discounted and should offer solid upside potential. Therefore I rate DAVA stock as a buy.

For further details see:

Endava: Finally Trading At A Compelling Price