DAVA - Endava: Quick Revisitation Of The Superior Financials And Opportunity

2023-08-01 09:50:51 ET

Summary

- Endava's operational metrics remain strong, with increasing revenue from clients, global revenue diversity, and growing average spend per client.

- The company's finances reflect its operational success, with consistent growth, stable margins, and a strong balance sheet.

- Despite a decline in share price, Endava's valuation is lower than its peers, suggesting potential for a quick upward move in valuation.

Summary

One of my largest personal holdings is IT Outsourcing Consultant Endava (DAVA). I have discussed their operations and the excellent opportunity they present in multiple prior articles (which are also summarized here ). Now, I will again provide an update on the company to determine any risk factors that may be causing the lagging share price as other IT companies rise in 2023. To summarize, I continue to believe Endava has consistent and superior growth prospects, valuable profitability, and a lower-than-normal valuation, all of which suggest that temporary risk and pessimism are unlikely to last.

Operational Metrics Remain Strong

Endava is a well-run business. As the key to the investment, organic growth is incredibly important. This has been the case for the past 10 years and is reflected by the following operational indicators:

-

Top 10 clients are becoming a smaller percentage of total revenue every quarter.

-

The number of clients generating over one million pounds in revenues is increasing at over 20% per year.

-

Average spend per both top ten and all clients is increasing, at 19% and 7% per year, respectively.

-

Global revenues are increasing in diversity, with less reliance on the UK and Europe, and more support from North America and the RoW.

Endava is doing well to grow organically through increased pricing power, and inorganically through various customer acquisition strategies. However, one issue that has arisen, and may be a major red flag for investors, is the fact that the total number of clients has fallen year-over-year in Q3 from 717 to 685 after many years of positive growth. While the other data points suggest that only weaker and smaller clients have pulled back on spending on consulting and outsourcing revenues, investors pessimistically believe that growth will fall soon. Thankfully, it seems that Endava has pulled many internal levers to continue driving excellent financial growth despite the sector headwinds present in 2023.

Finances Reflect Operational Success

Endava has been able to grow consistently over the past five years despite major global headwinds developing. Importantly, despite the firm basing the majority of their staff in nearshore countries of Eastern Europe, no loss of productivity has resulted due to the Russian Invasion of Ukraine. Major competitors such as EPAM ( EPAM ) had to work hard to relocate staff, and did well under the pressure, but this is reflected financially. As an example, EPAM's peak revenue growth in 2021-22 rivaled Endava's, upwards of 50-60% per quarter, EPAM's three recent quarters have seen a significant divergence in growth.

Whether due to geopolitics, weak client segments, or the ~6x smaller size of DAVA, EPAM has underperformed over the past three years by 20% in terms of revenue growth on average, despite soaring together. While Endava has also outperformed another peer, Globant ( GLOB ), over the last two quarters, there is clearly a unique issue present at EPAM, which is the risk associated with its former Soviet Bloc operations, as opposed to Globant's mainly Latin American operations.

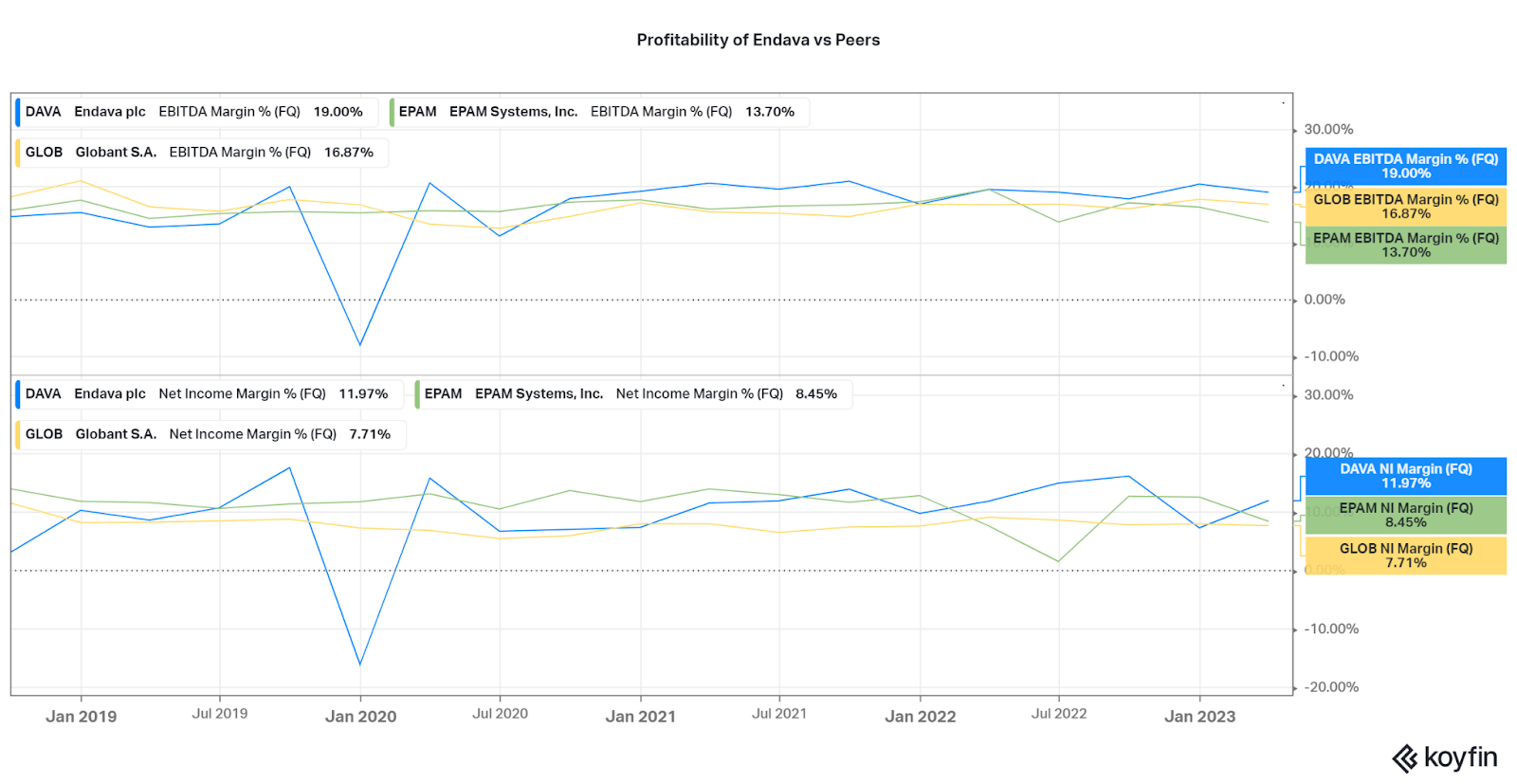

Koyfin

Beyond successful revenue growth, Endava has done well to stabilize competitive margins despite their smaller footprint than peers. With the prior quarter seeing both EBITDA and Net Income margins higher than both EPAM and Globant, a pattern that has repeated multiple times the past few years, Endava is both the top choice in terms of growth and profitability. This will allow the company to manage the weak market environment by investing profits where needed, primarily into bolt-on acquisitions, but also into capex and debt reduction.

Just look at the company's balance sheet: less than 2% dilution per year, net cash of ~115 million pounds, and no quarters with negative free cash flows since 2017. This operational success on the small scale will no doubt continue as economies of scale, favorable credit rating, and prestige allow for higher profits, lower interest burden, and continued organic growth.

{kind=link}

Valuation Tailwind

Due to these financial facts, many investors are no doubt concerned with the declining share price over the past two years. The poor run is based on the swift rise and fall of valuation in the post-pandemic era, but now fails to highlight the underlying fundamentals. While the rest of the tech market sees a boom from AI sentiment, this subsector of tech consulting companies have only fallen. This is despite the fact that these companies consult on the use and management of AI applications.

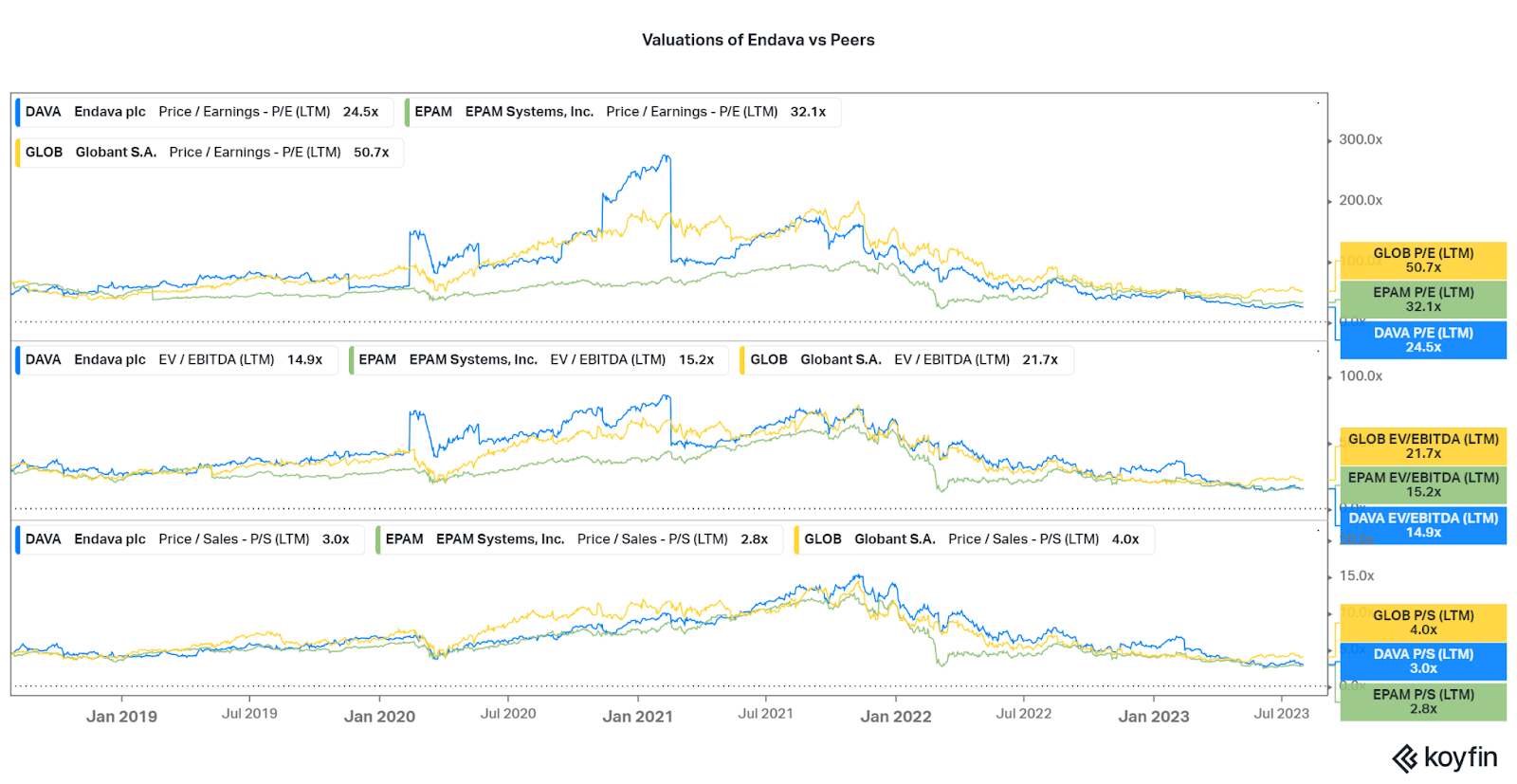

Endava now trades at a discount to both EPAM and Globant on a P/E and EV/EBITDA basis, and this is historically reversed. Combined with the fundamentals it is clear that Endava can see a quick move in valuation upwards, but the sector needs a favorable catalyst to start the upward climb.

{kind=link}

Conclusion

It seems to be that Endava is being held back by larger underperforming peers. Some may blame Endava's exposure to the payments industry, but overall banking and credit risk metrics have remained low, especially with the latest slew of earnings. While the recession factor is always on the forefront, we have to consider Endava fairly insulated from downside risk as they are consultants and managers of essential software infrastructure.

While some smaller, more consulting-based clients may disappear in the next few quarters, most major clients will continue spending and providing plenty of revenues. While momentum is low and affects algorithmic and technical buying, I welcome this weakness. And with high revenue growth and low valuation, Endava will soon have all three boxes checked, and a strong bull cycle will begin.

Interactive Brokers

With all these factors in place, I will continue to hold Endava as one of the top holdings in my personal portfolio. I continue to add on a regular basis, and will do so for the coming quarters. While I will be watching the fundamentals, especially client data, I do not foresee major issues arising operationally. I am also keeping realistic expectations by assessing the historical valuation of Endava and the peer group. In particular, EPAM has averaged a 45x P/E, 24x EV/EBITDA, and 4.5x P/S since 2012.

This suggests there is plenty of upside available for Endava, close to 50% in fact, but I do not expect the company to trade at levels seen in 2020 or 2021. And, it is possible to see multiple years in a row of a suppressed valuation, but don't forget the company is growing over 15% per year organically. This will keep the valuation risk as just one small part of the equation, and suggest great times ahead for investors.

Thanks for reading this update. Please feel free to read my prior articles for more depth, or I can happily answer inquiries in the comments.

For further details see:

Endava: Quick Revisitation Of The Superior Financials And Opportunity