DAVA - Endava: The AI Company You Wouldn't Expect

2023-07-28 10:15:31 ET

Summary

- I believe artificial intelligence is experiencing a speculative bubble, similar to the dot-com bubble, leading to inflated prices for AI-related companies.

- Endava, an IT consulting company focused on digital transformation, presents an interesting investment opportunity in the AI field.

- Endava's differentiated strategy, strong financial performance, and potential for growth in the digital transformation market make it an attractive investment option.

Over the past few months, it is indisputable that artificial intelligence has been the main topic of discussion, both because of its impact in everyday life and because of the hype it has brought to the financial markets. Currently investing in a company actively involved in artificial intelligence has become complicated, as the vast majority of them have already experienced a sharp increase in price since the introduction of Chat GPT.

Wanting to make a comparison with a historical period similar to the current one, the analogies with the dot-com bubble seem obvious:

- Hype toward companies concerning the new fad of the moment.

- Price multiples reflecting more than rosy growth prospects.

- Belief that everything will be disrupted with new technologies.

These three are all traits of a speculative bubble, in any case, I would like to clarify my position on the matter to avoid misunderstanding. Just as in 2000 with the advent of the Internet, I believe that artificial intelligence will change the world in the coming years, but that does not justify the hype that companies involved in this market are experiencing. Basing one's valuations purely on the growth prospects of a particular market is extremely risky, as one risks buying an excellent company at a price that is too high. It is worth remembering that even the best company in the world can turn out to be a bad investment if bought at an unreasonable price.

Probably, Microsoft's (MSFT) long-time shareholders who bought it in 2000 know this very well since they saw their first profits after almost 17 years. Of course, holding on to their position to this day would still have made it a bargain, but I doubt everyone has been so patient.

So, what to do? We know that artificial intelligence is the trend of the future, but the most interesting and dominant companies in the field are already too expensive in my opinion. The train to buy companies like Meta (META), Nvidia (NVDA) and Microsoft has already passed, but by digging deep you can still find interesting opportunities and in this article I will show you my investment thesis on one of them. Except for the first, all quotes belong to CEO John Cotterell during the Q3 2023 conference call.

Business model description

Generally, when we talk about artificial intelligence our mind wanders to companies that produce humanoid robots or innovative technologies that can automate processes such as driving or storage. Making this association is not wrong since indeed AI is present in these areas, however, reasoning in this way runs the risk of only observing the tip of the iceberg. AI is also used heavily by many other companies in less interesting areas that are often put on the back burner.

Creating an innovative solution for bad debt recovery does not generate the same hype as a chatbot capable of interacting with humans, but both in their own way utilize AI. We can argue that the latter is a more important innovation overall, but that does not detract from the fact that the former also deserves attention. In other words, I think it is still possible to invest in companies involved in AI without necessarily paying too much for them, but we should not look to those companies that to date have already achieved triple-digit returns and are the talk of the town. Based on this reasoning, I think Endava (DAVA) represents an interesting option; probably, few people know about it.

Endava operates in the field of IT consulting and is based in London. Its main goal is to improve the efficiency and business organization of companies that need it, which makes the services it offers quite broad. In general, we can consider Endava as one of the leading UK companies focused on the inevitable digital transition of companies with outdated and traditional activities.

As a result of the rapid social changes the world has been forced to adapt over the last several years, businesses have had to swiftly evolve to ensure they could continue to operate, while meeting a very different set of customer expectations. In this new reality, an organisation’s ability to operate primarily in a digital landscape may dictate its ability to both survive and succeed. We believe, moving forward, true digital transformation and the establishment of a flexible business model will become mission critical for businesses.

Endava offers consulting in multiple areas, and its services are tailored to the client's needs, which is why it is complex to understand all the circumstances by which it generates revenue. To give you a clearer idea about this, I think it is useful to describe two real circumstances that Endava has had to deal with in recent months.

- A digital marketing agency in New York was struggling to capitalize on the large amount of data it was collecting and needed a solution to allocate advertising budgets among different marketing channels based on real-time channel performance. In short, real-time dashboards that could capture the latest trends and performance were needed, and Endava was able to provide them. In this way, the long delays associated with traditional approaches were avoided.

- An international insurer needed to improve its bad debt recovery process by making better use of the data at its disposal. As a result, Endava created a data platform solution that could more accurately and comprehensibly interpret the available information.

{kind=link}

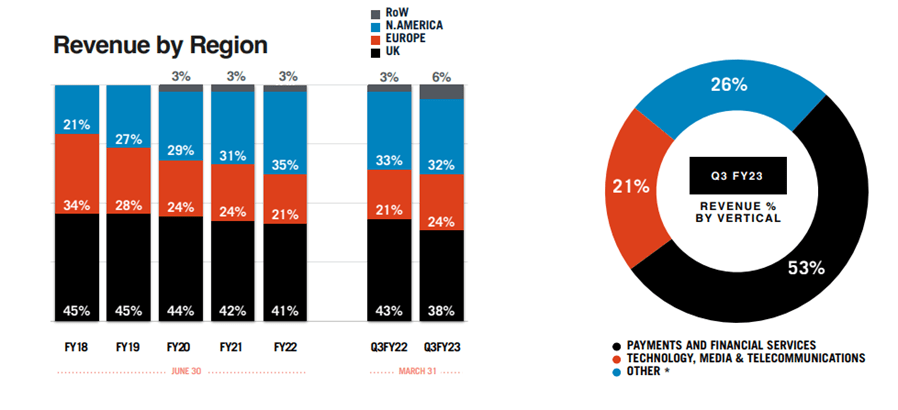

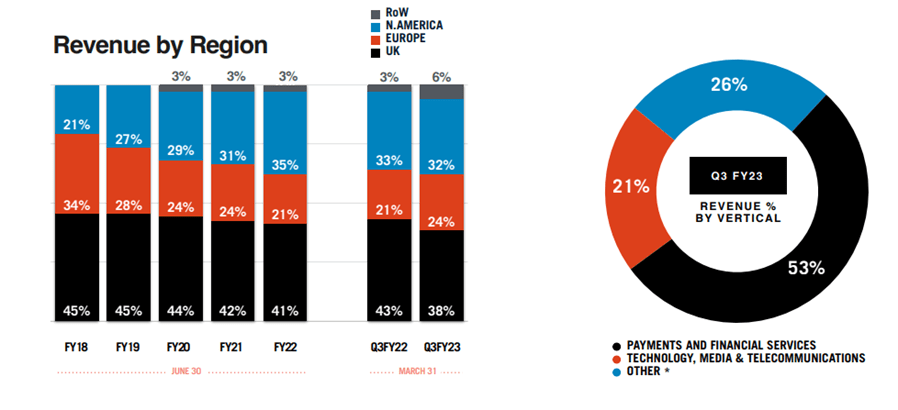

In short, there is no single sector to which Endava offers its services, but multiple, although currently payments and financial solutions are responsible for 53 percent of revenues. On the other hand, the geographic origin of revenues is a different matter. CEO John Cotterell has repeatedly expressed his desire to make Endava more international and especially more exposed to the U.S. market. In fact, from 2018 to the present, the minor exposure to the United Kingdom and the increasing exposure to the United States is evident.

Either way, the rest of the world should not be neglected, as the company is currently focused on expanding mainly in Australia.

We see demand as being excellent in Australia. So we've seen good organic growth over the last 12 months and that is continuing to come through. Now part of the attraction of the Australian market is that the maturity of genuine digital suppliers is actually lower than we see in Europe and in North America. And so putting ourselves together with some of the emerging digital players in that market is creating a lot of interest, a lot of sales opportunities. And so we are anticipating outsized growth out of our APAC and Australian-based business.

Expansion in Australia is taking place mainly through strategic acquisitions, and the recent acquisitions of Mudbath and DEK are evidence of this. The former is an Australian technology company that specializes in strategy, design and engineering services; the latter is an Australian company that develops software and hardware solutions for various applications, including real-time solutions, telecommunications and data communications. In short, both are exposed to the growing Australian market and can best integrate into Endava's ecosystem. Also worth mentioning is the acquisition of Lexicon in October 2022, also a tech company exposed to the Australian market.

Differentiation strategy

So far we have seen how Endava generates its revenues and where they come from geographically; now we will see who its customers are and what strategies it employs.

{kind=link}

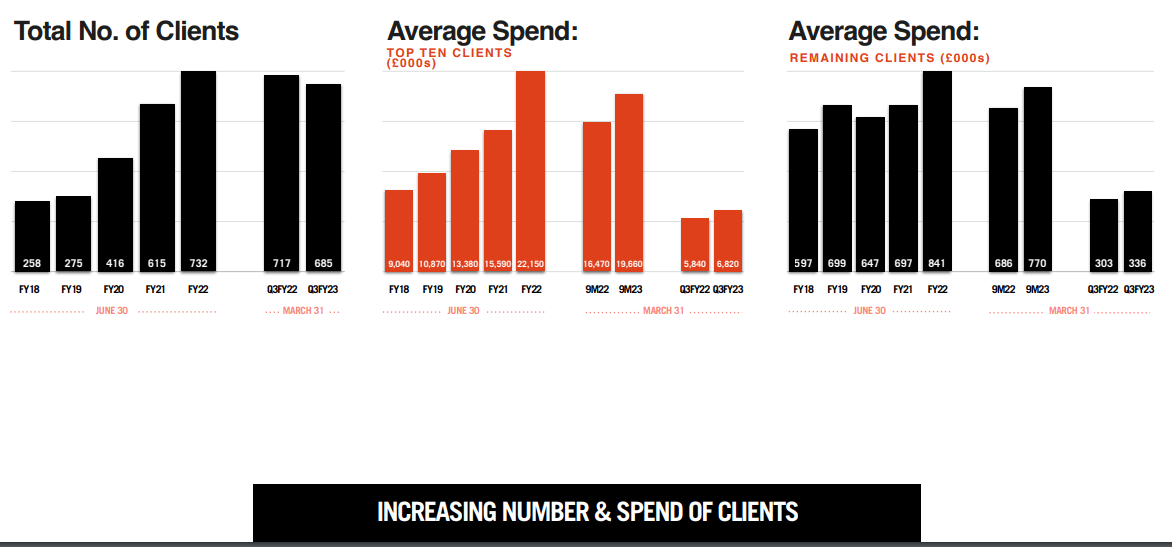

As you can see from this image, it is quite curious to note that Endava's customers are very few and what is more, also decreasing: in Q3 2022 there were 717 while in Q3 2023 only 685.

At first glance these may seem like negative figures, but they are actually in line with the company's strategy of focusing more on its best customers and gradually reducing the less important ones. In fact, looking at the average customer spending, there was a 10.90% improvement over last year's quarter. In other words, customers are fewer, but good.

We actually want to focus our efforts on the larger clients. Now if you look at the numbers for our larger clients, we've been particularly strong in the larger ones. So the greater than 5 million, those increased to 31 compared to 23 last year.

And we have published a band. But if you look at the 2 million to 5 million client band, that moved up to 56 compared to 35 last year. So it's all about us putting the energy into the larger clients that have the opportunity to scale. Obviously, we're still bringing in a good number of new, smaller clients. But they get outweighed or have done over the last two or three quarters by the trimming of the very small ones.

{kind=link}

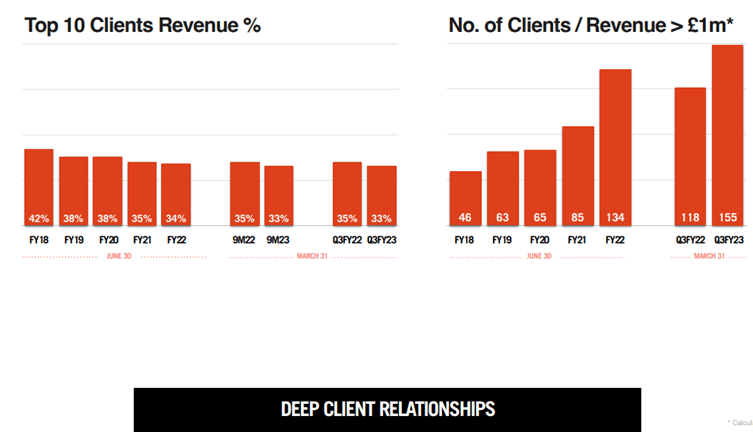

Thus, it is clear that Endava is trying to grab only the best customers and those that allow it to scale the business by increasing margins accordingly. In my opinion, this is comparable to a differentiation strategy, as the company seems open to offering its services only to certain customers. Of course, minor customers will not be completely excluded, in part because the company still needs this type of revenue. To date, such customers are often taken over at the time Endava acquires another company and then it proceeds to select only the best ones.

As a company that capitalizes at only $3 billion, the strategy of avoiding small customers appears to run against the goal of global expansion, yet the results to date prove the company is right in my view.

Endava Q3 2023

Revenues have grown at a CAGR of 31.70%, and the company has had no difficulty growing again this year. Moreover, the most important figure in my opinion of all, is that on average over the last 5 fiscal years 88.60% of revenues have come from customers who purchased Endava services during the previous fiscal year. This is a clear sign of customer satisfaction and loyalty. As we will see later, customer satisfaction also positively impacts profit margins.

How artificial intelligence will affect the future of Endava

Before talking about how AI will affect the future of Endava, I would like to emphasize my perspective on this topic. In my view, to understand the future impact of AI, we must first take a step back.

Artificial intelligence is not a discovery of the last few months, as the first studies date back to 1956 . Companies such as Alphabet (GOOG) (GOOGL) and Meta have been investing billions in AI for decades in order to optimize their services; therefore, I honestly do not understand all this sudden media hype. Artificial intelligence has been a part of our lives for a long time now, and as useful as ChatGPT may be, in the end it has not turned the world upside down as hoped. Personally, I do not believe that in the coming years AI will disrupt the way we live, just as it will not disrupt in the short run the profits of the companies that are involved in this technological revolution. Certainly, in the long run there will be significant changes, but it is perhaps best to limit the enthusiasm since predicting the future is not one of the strengths of human beings.

That said, making short-term estimates about how AI will affect Endava's revenues is pure speculation for me; instead, I find it reasonable to consider how the company is positioned from a long-term perspective toward this important growth driver.

As explained earlier, Endava's mission is to facilitate the digital transformation of companies, make them more efficient and more organized. As time goes on, I expect that more and more companies plan to implement new AI-based systems within their operations, and they may need Endava's help. Based on this important growth driver, the company expects many new high-value projects in the coming years. But the positive effects of AI do not stop at a growing demand for its services.

Endava is currently evaluating models from Open AI, Google and open source within the context of three industry verticals healthcare, financial services and insurance. The analysis evaluates the strengths and capabilities of each model in relation to industry specific client implementations.

The knowledge we gain from this exercise is foundational in delivering effective applications of AI for our clients because the nuanced understanding we are gaining of how the different models behave in different industry scenarios will allow us to apply the right technology to each client scenario.

In other words, the ability to use new cutting-edge models will enable Endava's engineers to speed up the process of creating ad hoc services, as well as avoid lengthy phases of experimentation and wasted time.

We believe these latest technological developments will be an important source of additional work opportunities for Endava. Clients will spend less on legacy work, leaving larger budgets for complex transformation work that will continue to need delivery by experienced, high performing cross-functional teams who will deliver results faster using generative AI tools. Additionally, this new technology will improve productivity across the board, allowing for higher spend.

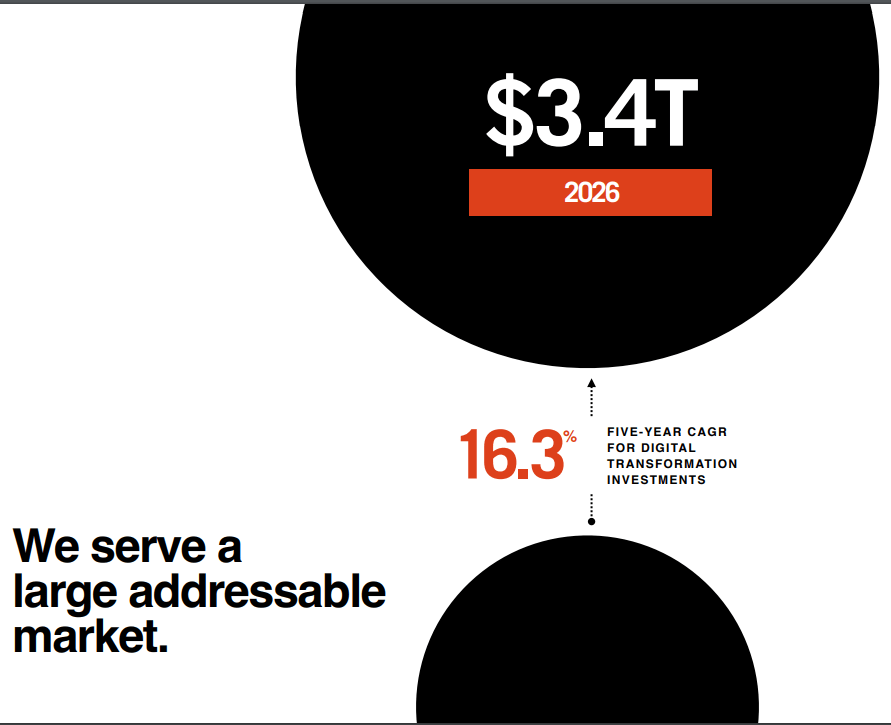

Overall, I believe that the technological revolution based on artificial intelligence will facilitate the work done by Endava and result in new customers interested in implementing the latest technologies. Indeed, the first benefits are already evident, and the company has repeatedly stated that it is now able to solve problems through AI that would have been considered insurmountable years ago. For example, Endava recently worked with a Central European bank that needed AI to modernize the retail banking experience by making it more engaging. This is an example of how modern AI has improved a traditional industry such as banking; similar situations will be increasingly commonplace in my view. More and more companies will be forced to enter the world of AI to keep up with the competition; after all, their survival is at stake. As of today, it is impossible to precisely quantify in revenues the benefits of artificial intelligence for Endava, however, we can draw some considerations by analyzing the growth and size of the addressable market.

{kind=link}

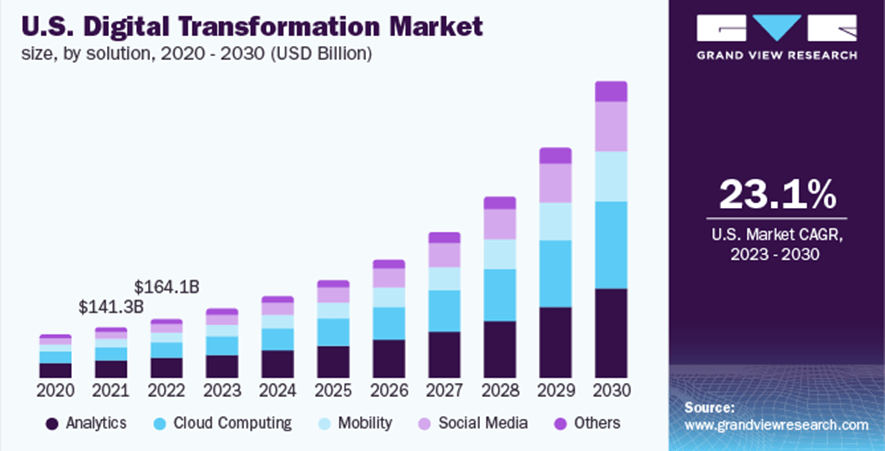

In 2026, digital transformation investments are estimated at $3.40 trillion, which would imply a 5-year CAGR of 16.30% from current levels. In other words, Endava's addressable market is huge, and the company could continue its rapid growth in the coming years.

{kind=link}

Looking at other sources, however, and specifically considering the digital transformation market , the result does not change much: strong growth is still expected through 2030.

Overall, from a long-term perspective Endava has on its side a fast-growing market driven by new digitalization needs from historically traditional businesses. The current hype toward artificial intelligence is anticipating a process that appears inevitable, namely the complete digitization of most businesses. Given the potential of the underlying trend, I would not be surprised if Endava continues double-digit growth through 2030.

Financial Data

When it comes to investing in small-cap companies involved in AI we often come across some that are very interesting based on their mission but not very concrete in terms of profitability. In other words, lots of good hopes and prospects but still heavily loss-making and therefore too speculative.

In the case of Endava this problem does not arise since the company has already been profitable for several years and is already at a more advanced stage of its business cycle. Obviously, being a less speculative investment than companies with more innovative business models the return on investment could be lower eventually, but at the same time so will the risk. This is one of the reasons I chose to analyze Endava and not any other company: it conforms to my investment criteria. Having said that, let us now turn to an analysis of the results achieved over the past ten years.

{kind=link}

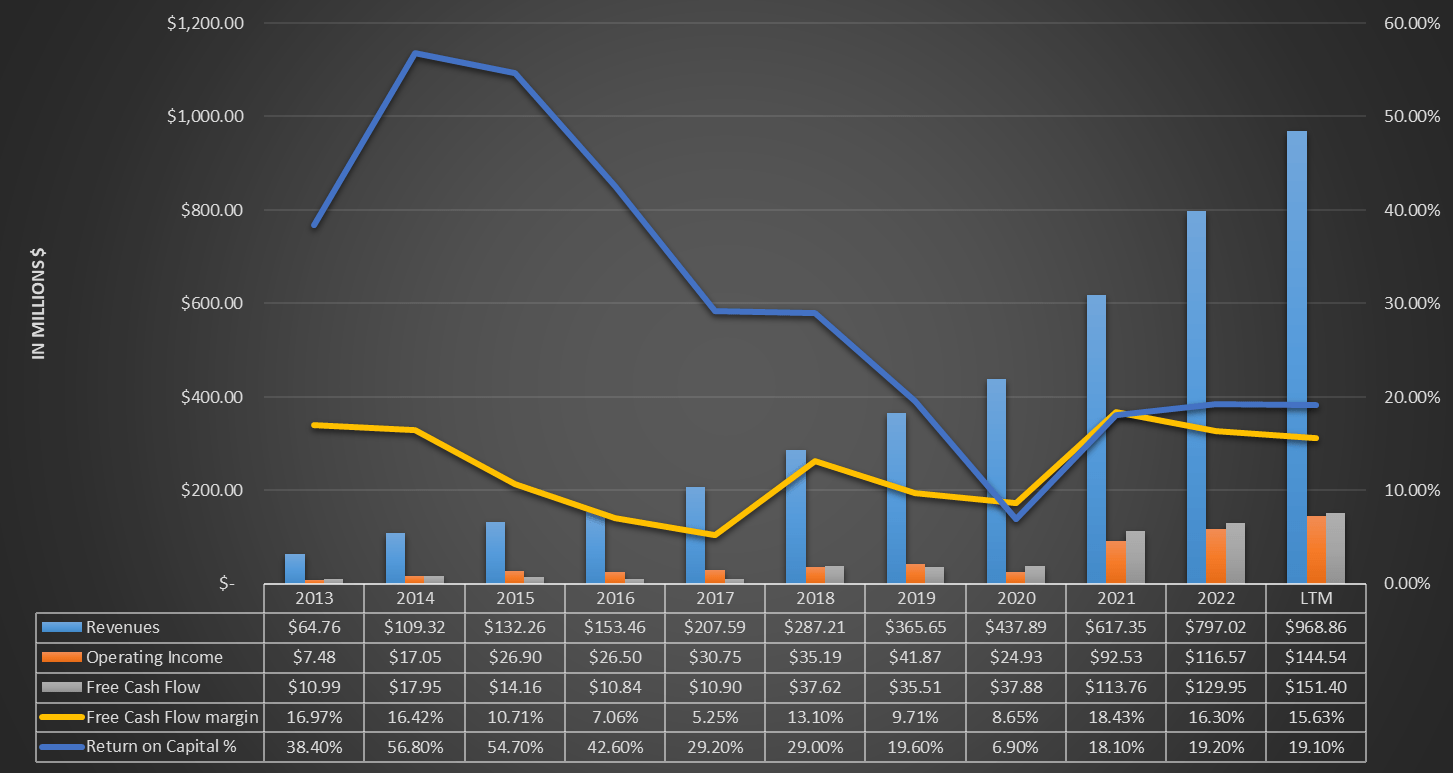

As we can see from this graph, it is clear that this company is in an optimal condition driven by revenues growing year after year with a return on capital approaching 20 percent. Free cash flow also has experienced excellent growth over the long term and now accounts for about 15% of revenues. The only sore point is that in LTM stock-based compensation amounts to $43 million, just over ¼ of free cash flow. For the rest, it is difficult to find a downside related to Endava's recent history; after all, in addition to growth, profitability is one of its strengths.

{kind=link}

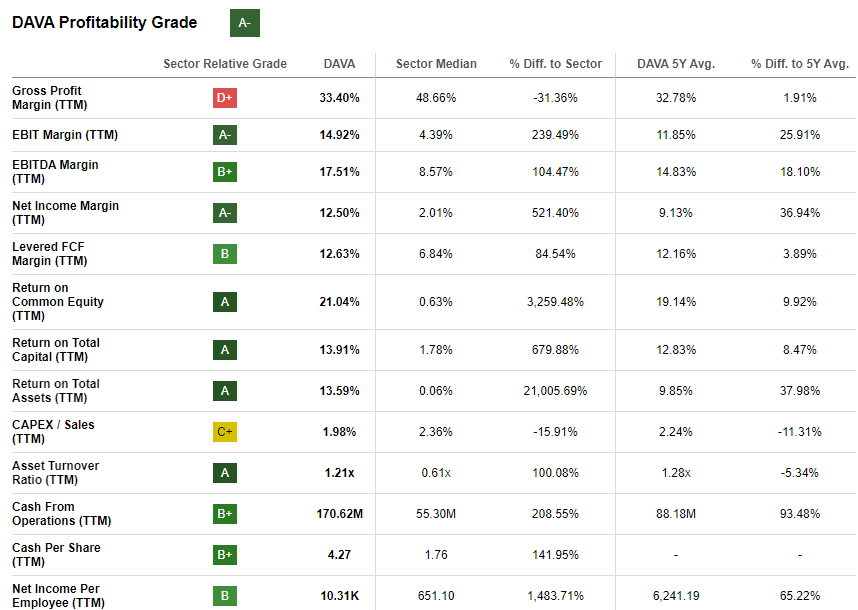

The quant rating of A- on Seeking Alpha denotes a certain margin advantage over its reference sector. In my opinion, it is due to the differentiation strategy previously discussed.

Finally, regarding the financial situation, there is very little to say since Endava has more cash than debt. Its net debt stands at ($166 million), which is another point in its favor.

Overall, based on the last ten years, Endava has managed to have significant and steady revenue growth, fairly good margins, and excellent return on capital. All this, while maintaining almost always negative net debt. Certainly, past performance is no guarantee of the future, but it does matter when evaluating a company.

Valuation

To understand what the fair value of Endava amounts to, I will use a free cash flow model. This model will consist of both objective inputs and subjective inputs. So, it is clear that the resulting fair value will be influenced by my view toward this company that may turn out to be wrong.

As objective inputs in this model we have shares outstanding and net debt, both obtained from Seeking Alpha. All values will be converted to dollars.

As subjective data we have the future growth rate and the required return.

- In the first case I will consider a 10-year CAGR of 13% and a perpetual growth rate of 2.50%. This seems to me to be a reasonable growth rate based on both the growth expectations of the digital transformation market and the growth achieved in the past. As we noted in the previous paragraphs, for the former a CAGR of 23.10% is expected, for the latter the CAGR was 31.70% between 2018-2022.

- As for the required rate of return, I opted for 12% per year. Investing in Endava carries a rather high risk; it is a company that capitalizes at only $3 billion and competes against giants such as Accenture (ACN). For this reason I have included a higher required return than the historical return obtained by the S&P500. This is a subjective figure and not calculated through the classic CAPM formula.

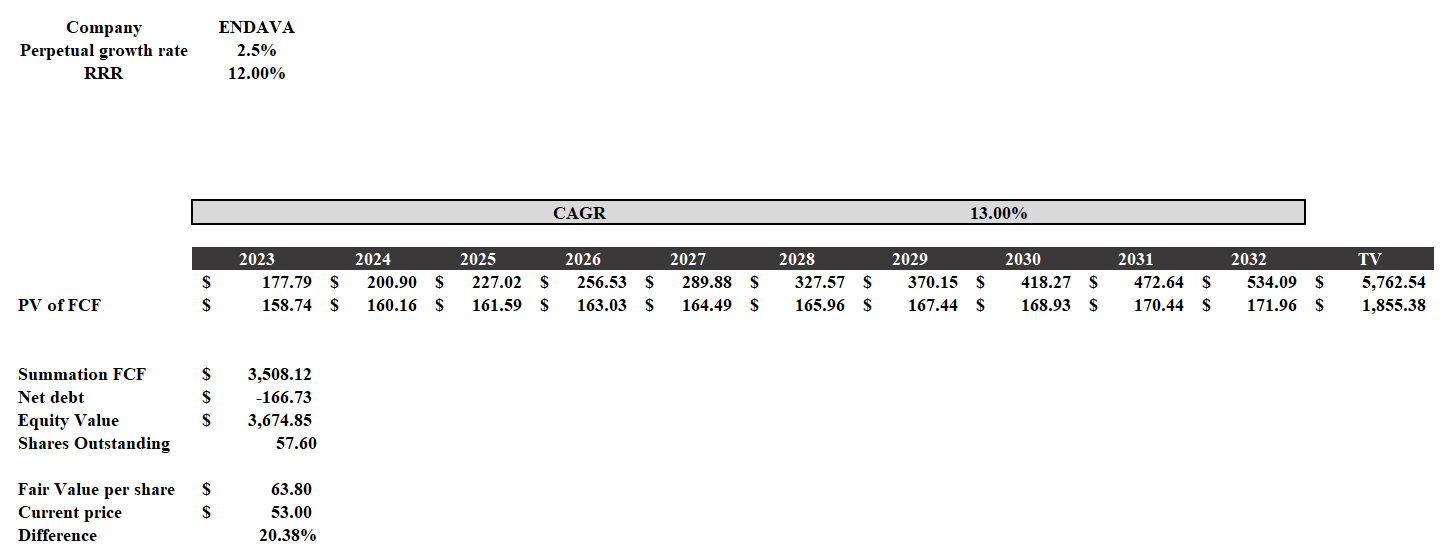

{kind=link}

The result is that the fair value of Endava calculated through these assumptions comes out to be $63.80 per share, which means that the stock is undervalued by about 20 percent. In short, it seems that at the current price there is a basis for a first purchase. Anyway, I realize that not everyone would have entered the same inputs as I did, so I attach for completeness a table with various fair values based on different inputs.

Fair values based on different inputs

For those who expect a CAGR of 5 percent, Endava is in no way a good investment at the current price; however, for those who are optimistic and expect a CAGR of 20 percent, there is a good chance that it could prove to be a good investment even requiring 15 percent per year.

Overall, I rate Endava as cheap, but certainly not the bargain of a lifetime. It might also make sense to wait for a further decline; after all, in June 2023 it had reached $44 per share. At that price it was definitely more than interesting.

Risks

So far I have mostly covered the positive aspects of Endava such as its financial strength, the growth it has achieved in the past, and the potentially high growth it can achieve in the future. Indeed, there are good premises, but Endava is certainly not risk-free. Assessing the downsides as well is the basis of any successful investment, which is why in this section I will discuss the four main risks I have identified.

The first risk concerns poor sectoral diversification of revenues.

{kind=link}

As we can see, 53 percent of revenues come from the payments and financial services sector, which makes this company very exposed to the performance of the financial sector. The latter is known to be very cyclical, which means that in the event of a recession, Endava is likely to experience a major revenue meltdown. What is more, it must not be overlooked that at the beginning of the year the failure of Silicon Valley Bank led to the collapse of other banks subsequently. All this currently makes the banking sector rather fragile. If this crisis continues, Endava's potential clients concerning this sector may decrease. After all, when there is distrust toward banks, they tend to hold back as much liquidity as possible in order to avert liquidity problems related to a possible bank run. In this scenario, I doubt that their first thought is to improve the efficiency of their models.

The second risk concerns competition. Although Endava has good margins and a very good return on capital, it does not have such a high competitive advantage in my view. Deloitte Consulting, IBM (IBM) Consulting, and Accenture are three giants that this company has to contend with. Certainly Endava's clients have proven to be loyal over time, but it is worth remembering that there is a lot of competition in this industry.

The third risk concerns dilution. As discussed earlier, stock-based compensation is often present in this company's financials, which dilutes the ownership of existing shareholders. In 2018 there were 53.03 million shares outstanding; today there are 57.60 million. This is not a serious dilution but it is worth mentioning.

The fourth risk concerns future growth expectations. If Endava has grown a lot in recent years, it is because the pandemic has forced many companies to modernize in order to continue operating. This has led to a sharp increase in demand for the services offered by Endava resulting in higher growth rates. Today, however, Covid-19 is no longer an issue and this growth driver is no longer present. Regarding this aspect, the CEO talked about it quite openly in the last conference call :

So yes, there was definitely a bubble in demand. If you remember, we were delivering 50%, 60% year-on-year growth through that period, which is much higher than our sort of normal expected growth rates. And so that was stretching the business really hard as we were growing at those sorts of rates. So the ability to optimize to make reorganization when you're actually being stretched by growing at 50% was something that we deferred and chose not to do.

Conclusion

There has been nothing but talk about AI in recent months, but this hype is leading the major companies involved in this topic to reach extremely high prices. In my opinion there is a speculative bubble going on, and right now it is worth focusing on companies that are less well known but will nonetheless ride the AI trend. I consider Endava to be one of them.

This company has been showing strong results for years, both in terms of growth and profitability. With the new technologies at its disposal it may be able to solve problems that previously took much longer or seemed insurmountable. Management is already working to make the most of them and will operate in a rapidly expanding addressable market.

Overall, my view for the future of this company is positive and at the current price an initial purchase seems like a reasonable move.

Editor’s Note : This article was submitted as part of Seeking Alpha’s Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Endava: The AI Company You Wouldn't Expect