WWE - Endeavor Group Holdings And World Wrestling Entertainment: The Market Is Fighting Back

2023-04-03 16:30:38 ET

Summary

- Shares of both Endeavor Group Holdings and World Wrestling Entertainment took a hit after news broke that the two firms would merge UFC and WWE into a separate entity.

- Conceptually, this deal makes a lot of sense and will create a major player in the entertainment space.

- But the price does not make sense and results in investors in Endeavor Group Holdings giving too much away for what it's receiving.

April 3, 2023, proved to be a rather interesting day for fans of both UFC and WWE. After news broke that Endeavor Group Holdings ( EDR ), the parent of UFC, would be merging with World Wrestling Entertainment ( WWE ) in a massive, multi-billion-dollar, transaction, shares of both companies took a tumble. Although stock in Endeavor Group Holdings already was a bit pricey, the implied purchase price assigned to WWE is astronomical. Frankly, both companies deserved to experience this pullback in response to the development. After all, the transaction overvalues WWE and the all-stock composition of the deal effectively dilutes the value of UFC.

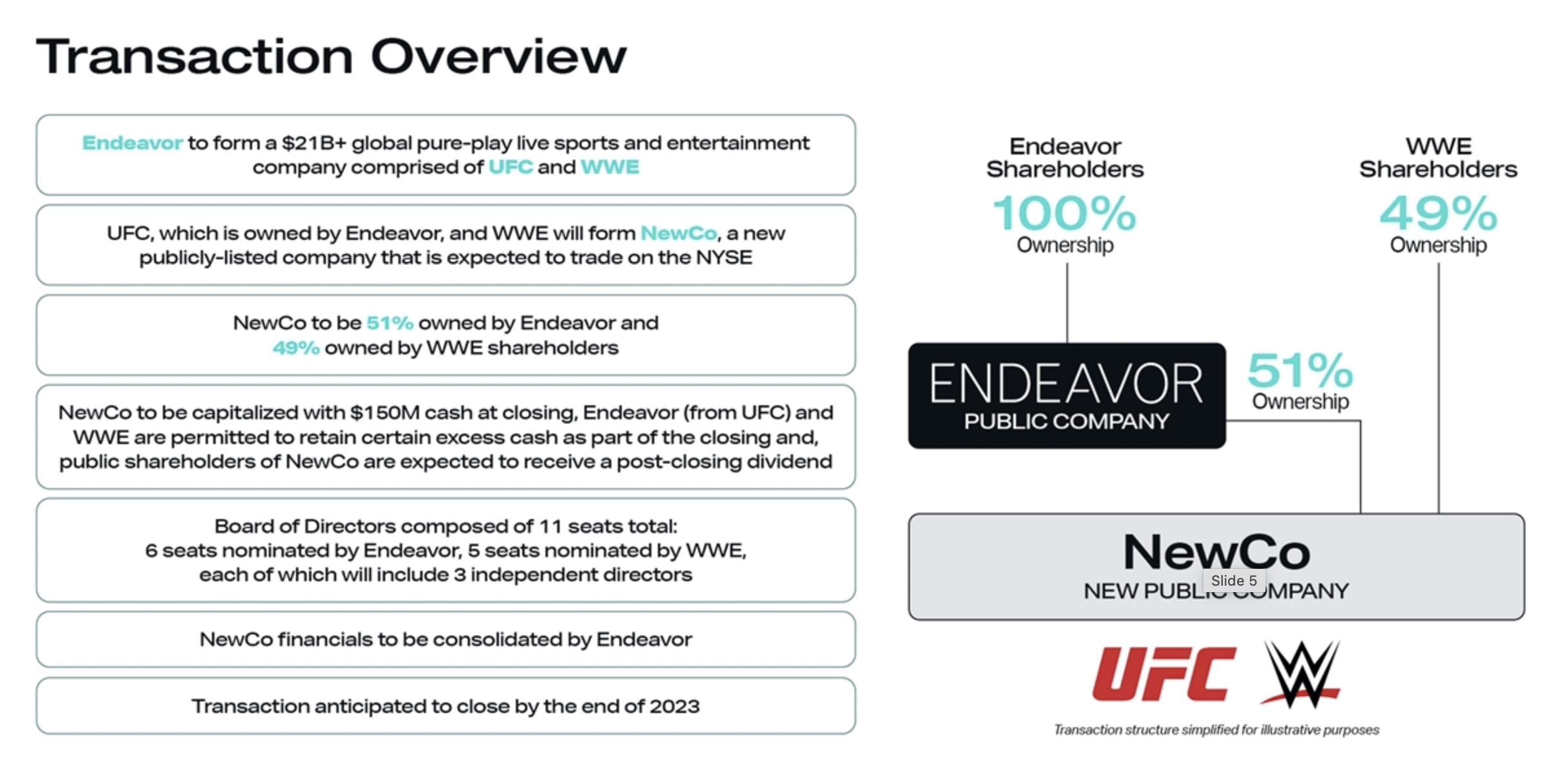

A look at the deal

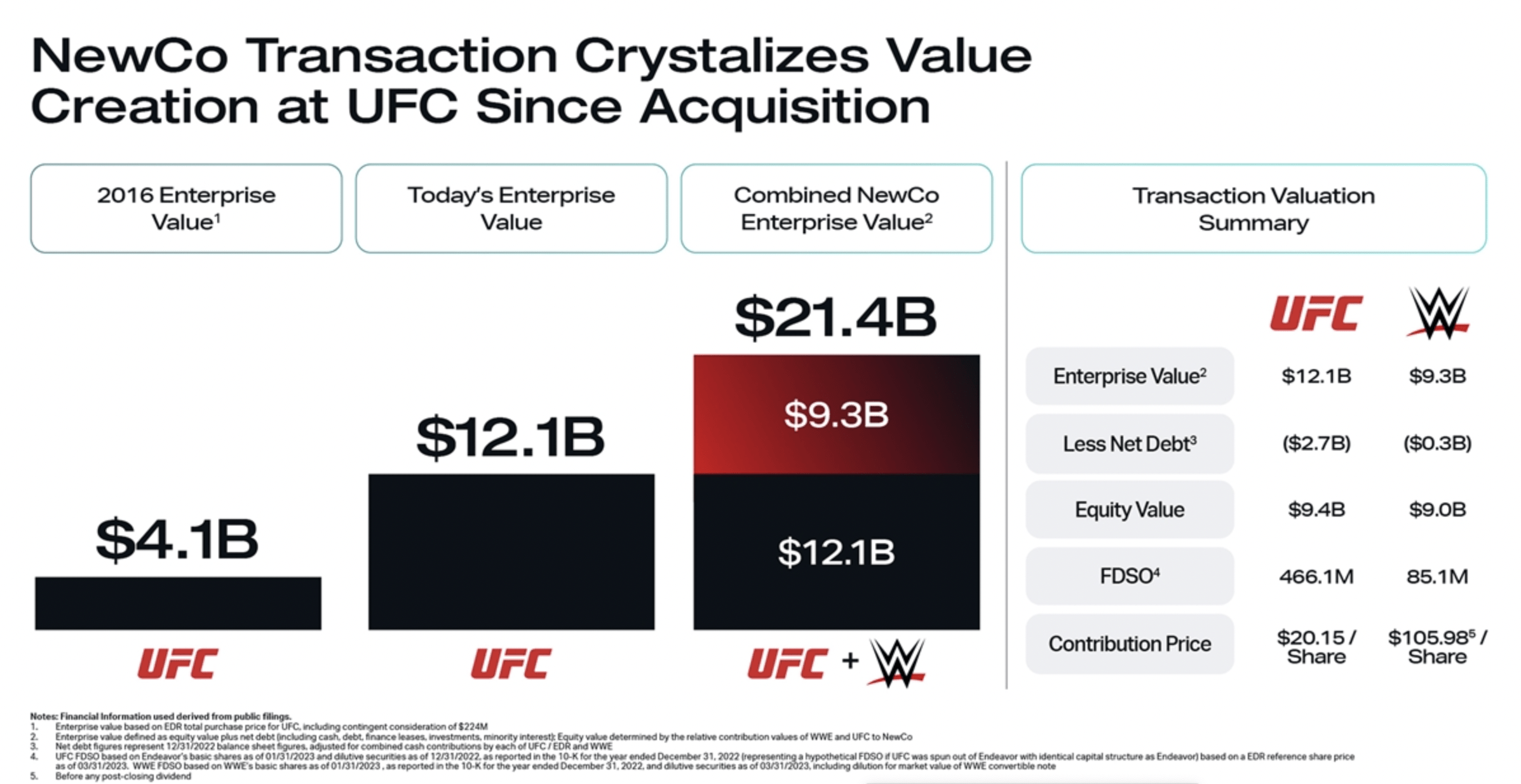

I don't know about you, but when I hear of an all-stock transaction, I often expect a fairly straightforward deal that doesn't have much in the way of complication. But not every all-stock transaction is so simple. In truth, the deal between Endeavor Group Holdings and WWE is a bit irregular in structure. The headline is that the implied price being paid for WWE works out to $105.98 per share. Investors looking at that headline may then be perplexed by the fact that shares of the company dropped 5% in response to the news, falling to approximately $86.76 as of this writing. But this is not really with the price being paid for WWE is. Instead, it's the effective value that Endeavor Group Holdings is assigning it for the purpose of determining what percent of the combined enterprise that shareholders of WWE will receive.

{kind=link}

The way the transaction works is that Endeavor Group Holdings will contribute its ownership in UFC to a separate, publicly-traded entity. That entity also will effectively absorb WWE, with shareholders of Endeavor Group Holdings receiving a 51% stake in the enterprise and shareholders of WWE receiving the remaining 49%. The implied buyout price of WWE could have theoretically been anything. If, for instance, the price assigned had been $200 per share, then investors in WWE would have gotten 64.4% of the combined business instead. The amount transacted is not the actual value relayed. And the market clearly understands and dislikes that. In essence, to make the deal more appealing to WWE shareholders and management, Endeavor Group Holdings decided to try assigning a much higher price on the transaction than what the market was willing to value the firm at.

{kind=link}

At the prices listed by management, the total enterprise value of the combined entity comes out to roughly $21.4 billion. $9.3 billion of this implied price comes from WWE, with the remaining $12.1 billion being the implied valuation for UFC. The equity value implied by these deals is approximately $18.4 billion, with $9.4 billion involving UFC and the remaining $9 billion assigned to WWE. Management has high hopes for the transaction. For instance, they expect the company to achieve between $50 million and $100 million in annual run rate synergies, much of which will come from operating cost cuts. It's worth noting that, upon completion of the deal, shareholders will receive a one-time cash distribution. Unfortunately, we don't know how large that will be. Based on my estimate for current cash balances, and factoring in the $150 million in cash and cash equivalents that the combined company plans to have on its books, I estimate total proceeds at around $328.7 million for the distribution. If the market had honored the implied merger price, this would translate to a roughly 1.8% distribution.

A combination makes sense

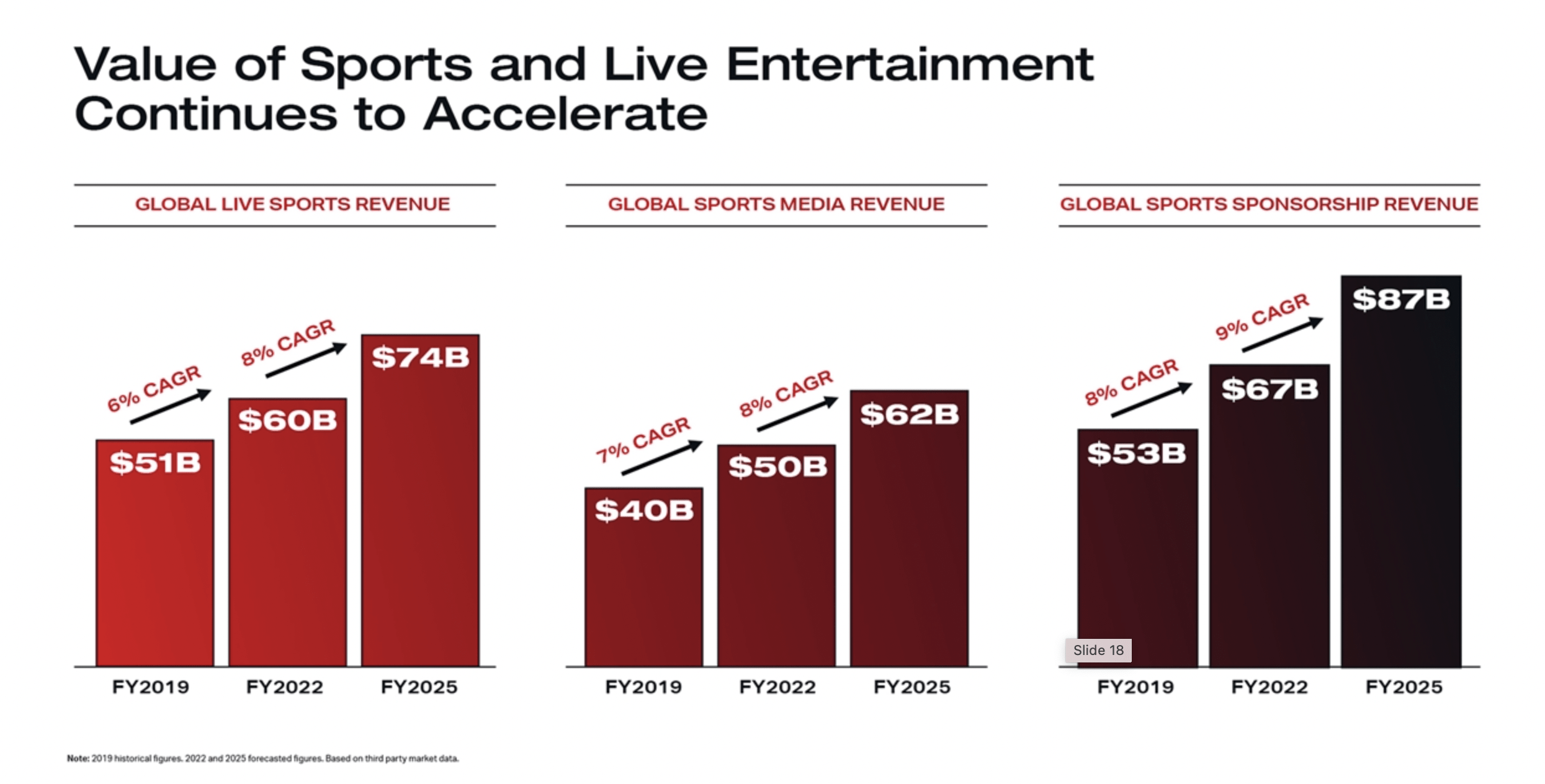

Conceptually, a combination of these two companies makes a great deal of sense. For starters, they operate in some rather large markets. In 2022, for instance, the global live sports market was estimated to be worth $60 billion. That was up from $51 billion in 2019. Through 2025, that market should grow at about 8% per annum, hitting $74 billion a year. But there are other markets to compare this to. The global sports media market is worth about $50 billion and is expected to hit $62 billion by 2025. Even more impressive is the global sports sponsorship market. By 2025, it should grow to $87 billion. That implies about a 9% per annum growth rate compared to the $67 billion that it was worth in 2022.

{kind=link}

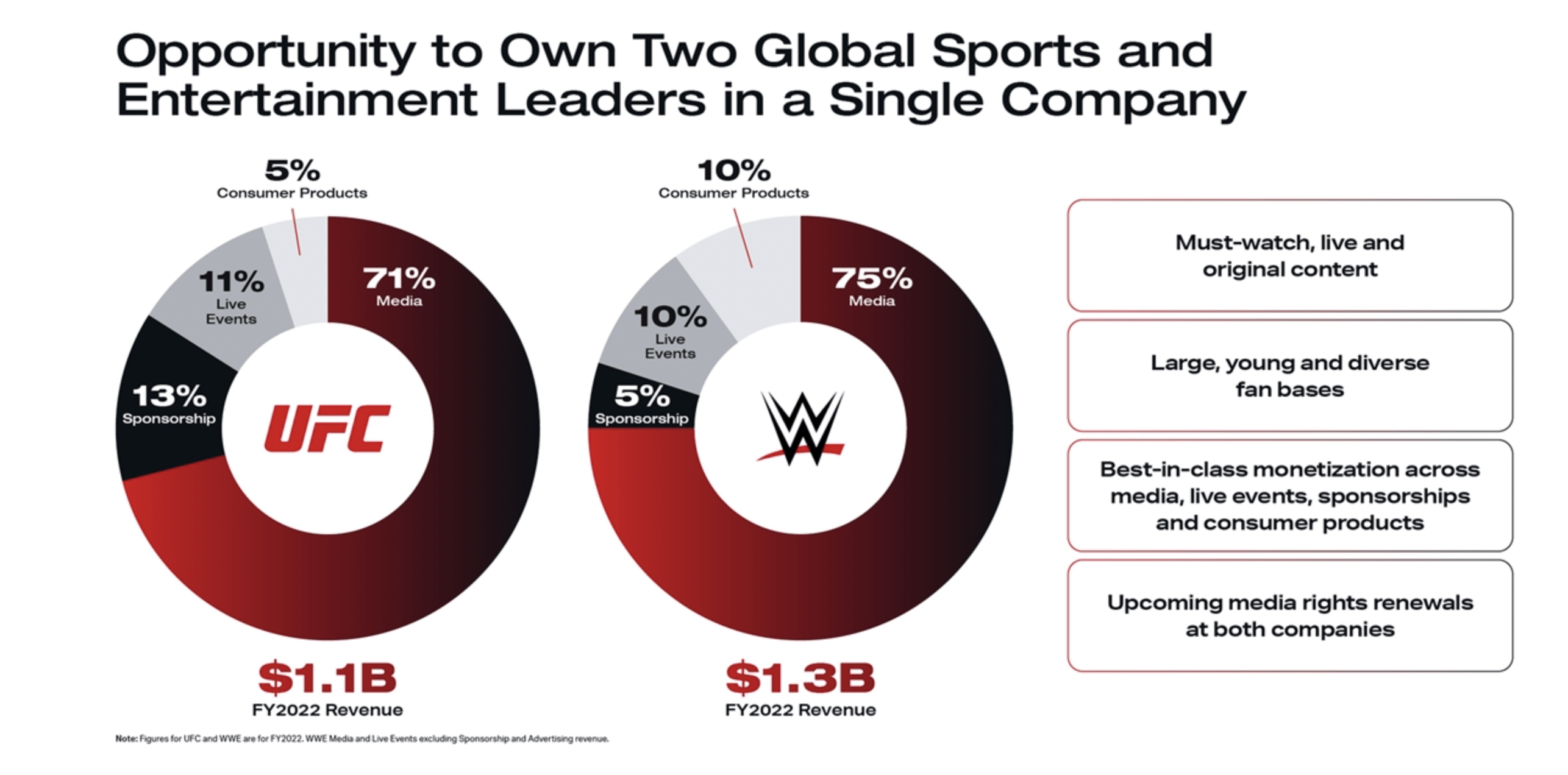

All combined, the company will already have a sizable market presence with revenue of $2.4 billion per year. One area for improvement for the entity might be the potential to grow its sponsorship revenue. Using data from last year, 13% of sales from UFC involved sponsorship activities. That number was only 5% for WWE. Although this is a small piece of the overall pie, sponsorship revenue does tend to have rather lofty margins. In addition to this, current shareholders of UFC might benefit from potential growth in the consumer products category. 10% of sales associated with WWE come from these activities compared to only 5% for UFC. And unlike sponsorship activities, we do know that the segment profit margin for consumer products under WWE is a robust 40.4%.

{kind=link}

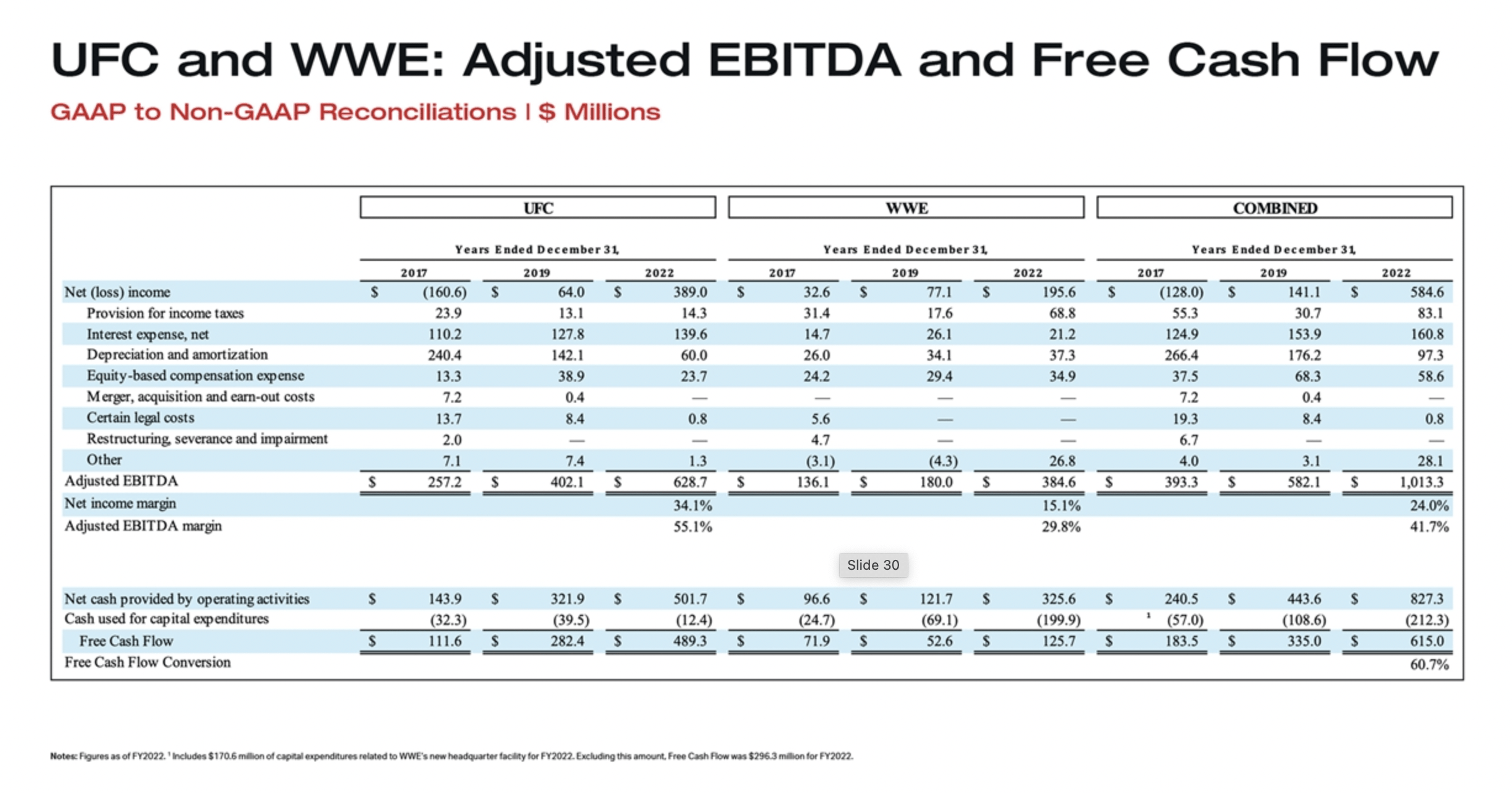

On the bottom line, investors can anticipate net income of about $584.6 million. This is where the picture becomes more or less lopsided. Due in part to the higher net leverage that Endeavor Group Holdings brings to the table, the company was also compelled to bring in a higher share of overall profits. Despite shareholders getting 51% of the enterprise, UFC accounts for 66.5% of overall profits. The number for EBITDA isn't much different at 62%, while for operating cash flow it is 60.6%.

Why this deal is a tough sell

Both the market and I believe that this is not the best deal for shareholders on either side of the transaction. Fundamentally, both companies have done well over the past few years. For instance, UFC has gone from a net loss of $160.6 million in 2017 to a net profit of $389 million last year. WWE has gone from a profit of $32.6 million to a profit of $195.6 million over the same window of time. Other profitability metrics also have been positive. EBITDA for UFC has managed to rise from $257.2 million to $628.7 million at a time when WWE saw its EBITDA grow from $136.1 million to $384.6 million. And operating cash flow has gone from $143.9 million to $501.7 million, while for the latter enterprise, it grew from $96.6 million to $325.6 million.

{kind=link}

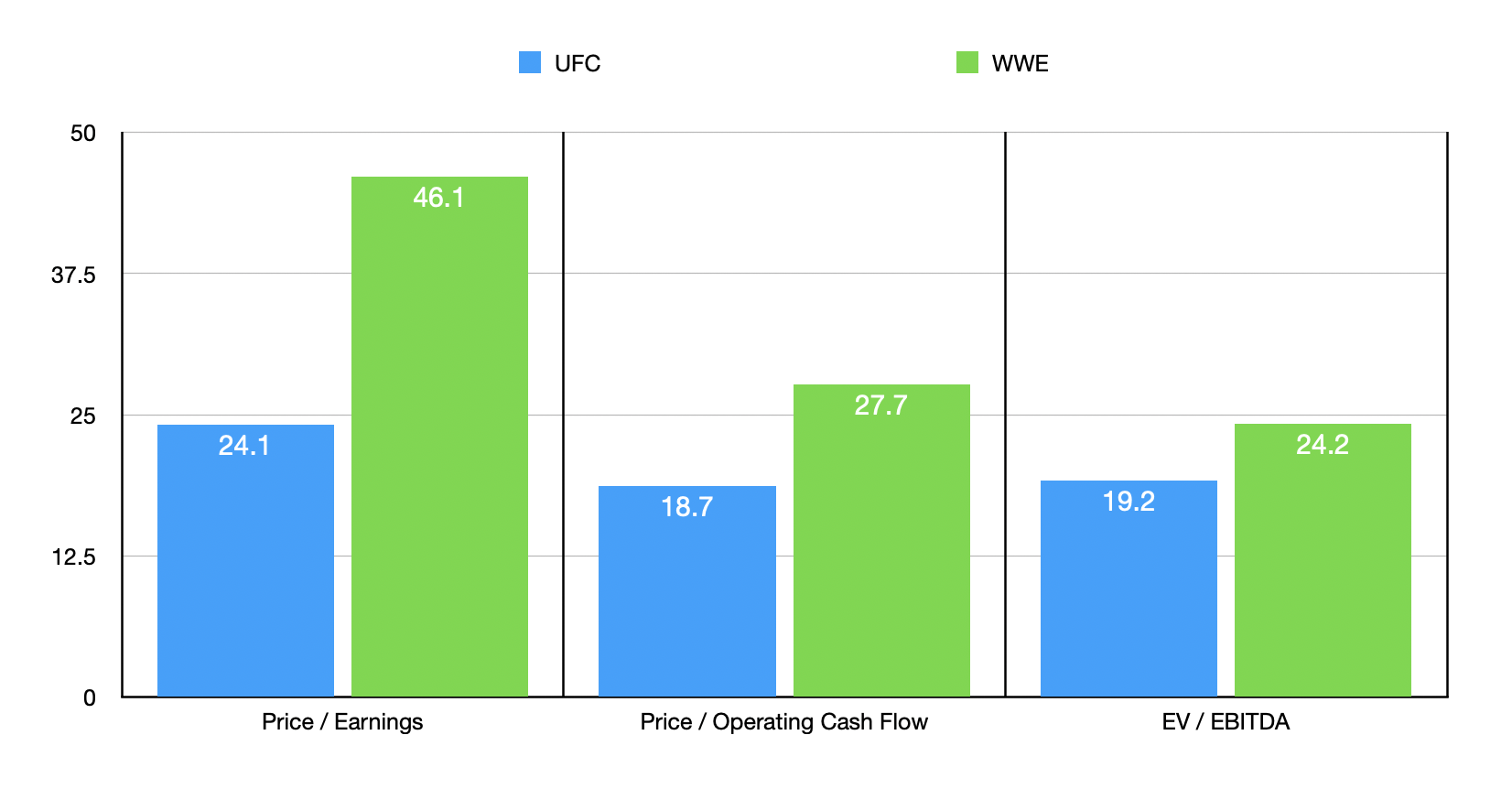

What we have are two companies that are growing at a reasonable rate and that operate in large and growing markets. The problem lies not in these issues, but in the fact that Endeavor Group Holdings is sacrificing too much. Using the 2022 figures, I calculated that UFC is being valued at a price-to-earnings multiple of 24.1, while the implied value for WWE is 46.1. That's a premium of 91.3% if comparing one firm to the other. And he praised the operating cash flow basis, these multiples are 18.7 and 27.7, respectively, for a premium of 48.1%. And when it comes to the EV to EBITDA approach, the multiples are 19.2 and 24.2. That translates to a premium on an enterprise value basis of 26%. It's true that the bottom line improvement seen since 2019 by WWE has been more impressive than what UFC has experienced, but on the other hand, margins associated with UFC are significantly larger. The net profit margin for the company, for instance, is over 35%. For WWE, meanwhile, it was around 15%. So although investors might be getting an enterprise that's growing its bottom line more rapidly, they're paying up quite a hefty amount for that growth and are still getting an asset that's less profitable on a margin basis.

{kind=link}

Takeaway

The way I see it, a transaction between these two entertainment companies makes a lot of sense conceptually. But how the deal was arranged, and the terms ultimately agreed to perform a disservice for investors in Endeavor Group Holdings. Shares of both companies have pulled back in response to the transaction, with investors in Endeavor Group Holdings likely recognizing that they're overpaying for the business and investors in WWE pushing the stock down because the all-stock composition of the transaction means that its shares should now move more or less in line with shares of Endeavor Group Holdings from here on out.

For further details see:

Endeavor Group Holdings And World Wrestling Entertainment: The Market Is Fighting Back