EDVMF - Endeavour Mining: A High-Margin Producer At A Very Reasonable Price

2023-11-22 12:17:06 ET

Summary

- Endeavour had another solid quarter in Q3 with flat production (continuing operations) and industry-leading costs despite a softer quarter at Mana.

- The bigger story though is continued exploration success at Tanda-Iguela, which looks like it's shaping up to be a 400,000-ounce per annum mine by 2030 (if approved).

- In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies.

We're nearing the end of the Q3 Earnings Season for the Gold Miners Index (GDX) and one of the most recent companies to report its results is Endeavour Mining (EDVMF). Overall, the company had another solid quarter, true to form, with industry-leading all-in sustaining cost [AISC] margins, continued progress on its growth projects which remain on budget/schedule, and ended the quarter with a relatively strong balance sheet unlike other peers such as IAMGOLD (IAG), Kinross (KGC), and Evolution (CAHPF) that have levered up heavily to deliver current/future growth. In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies.

Sabodala-Massawa Site & Construction Progress - Company Website

{kind=link}

All figures are in United States Dollars.

Q3 Production & Sales

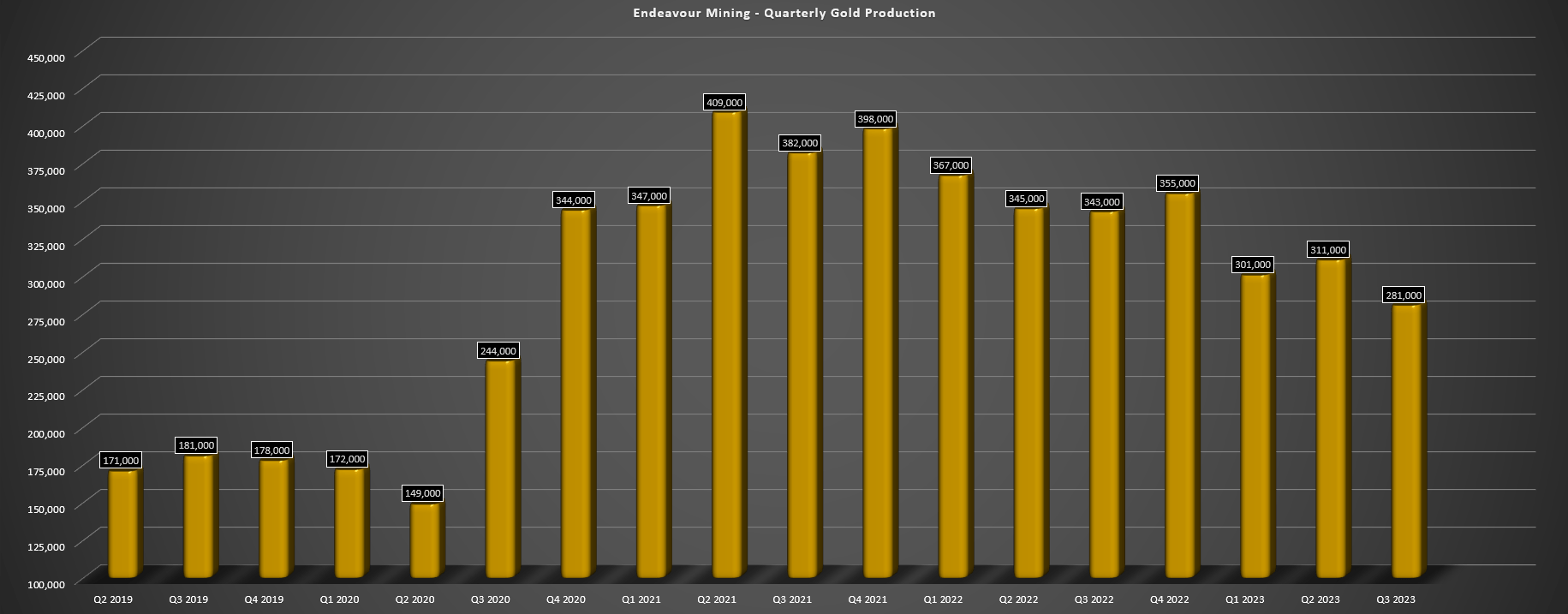

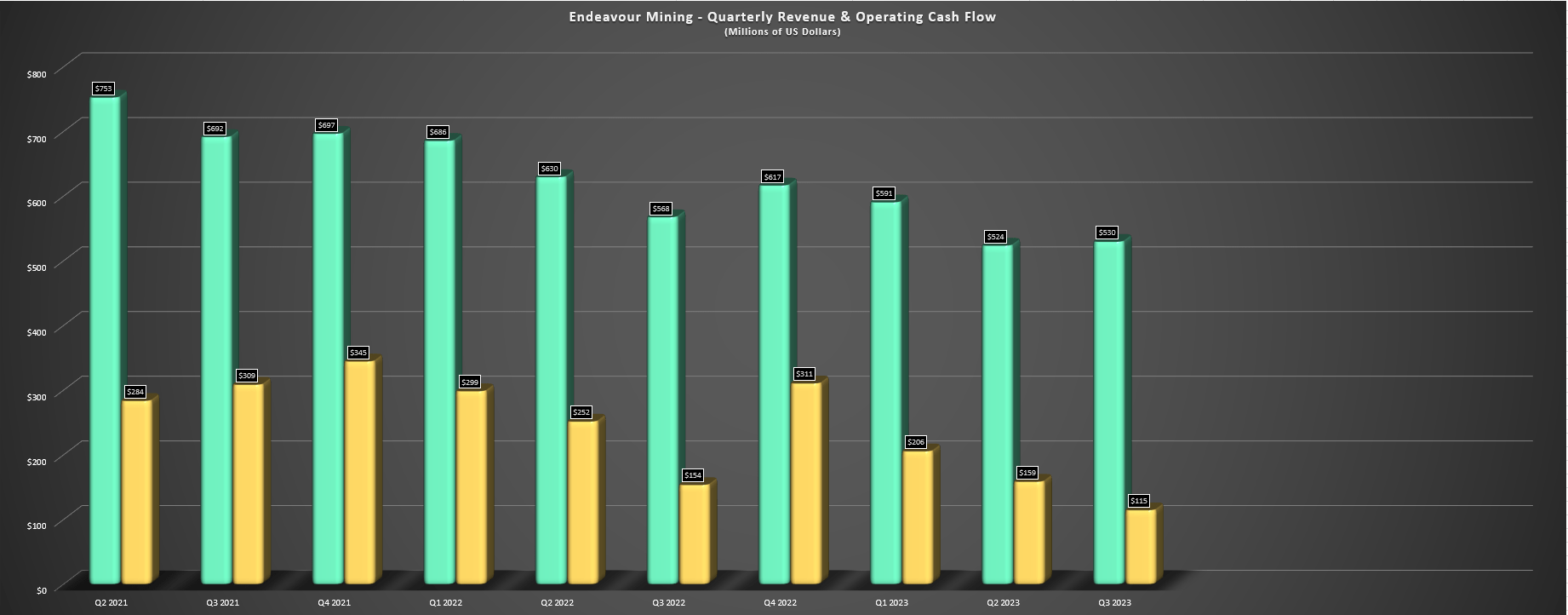

Endeavour Mining released its Q3 results earlier this month, reporting quarterly production of ~281,000 ounces of gold, which was flat from the year-ago period (continuing basis) or down ~18% on a non-continuing basis given that it was operating two additional mines in Q3 2022 (Wahgnion, Boungou). These two mines contributed ~61,000 ounces of gold production in Q3 which distorts the production results in the below chart, but it was a solid quarter on a continuing basis with a monster quarter from Hounde (higher throughput and benefit of positive grade reconciliation) offsetting lower production at Sabodala-Massawa, Mana, and Ity. Meanwhile, revenue was also affected by the lower gold sales (two fewer mines producing), with Q3 revenue of ~$530 million, down from $568 million in the year-ago period despite a higher average realized gold price ($1,903/oz vs. $1,679/oz).

Endeavour Mining Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

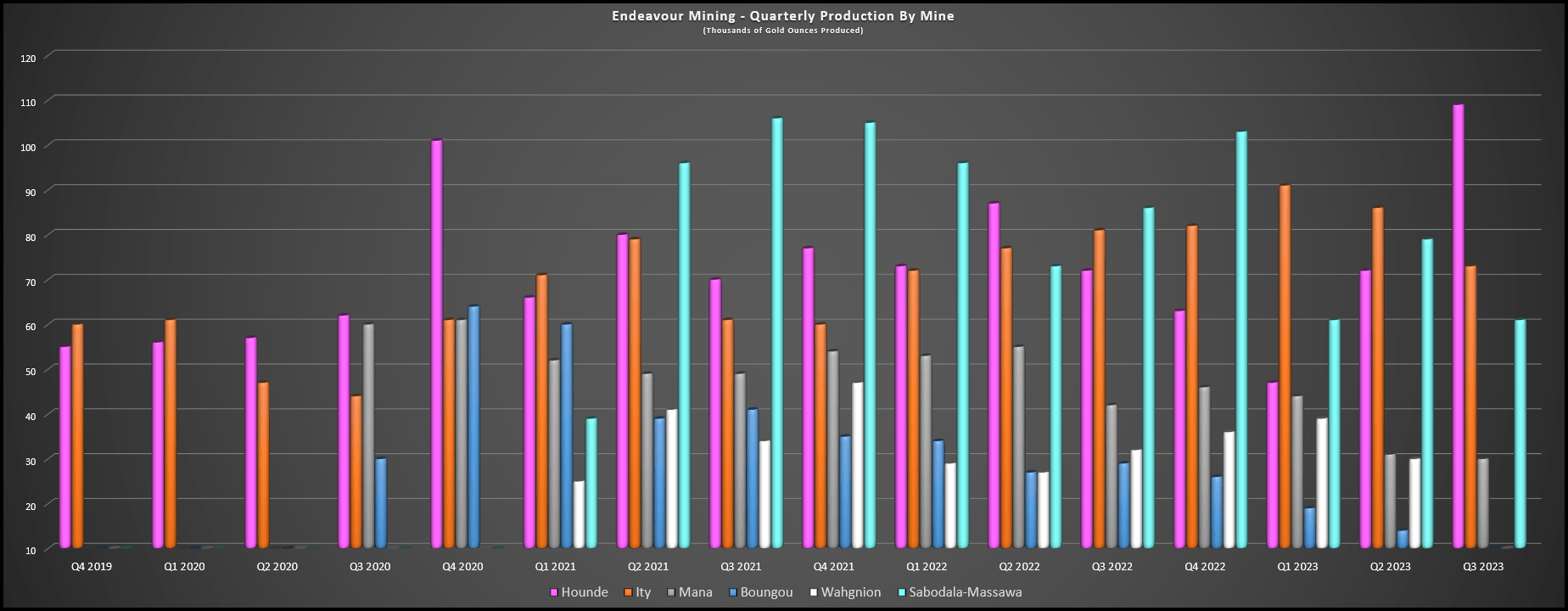

Digging into the results a little closer, Hounde was the stand-out mine in Q3, producing ~109,000 ounces of gold (+51% year-over-year) with ~1.4 million tonnes processed at an average grade of 2.68 grams per tonne of gold (Q3 2022: ~1.23 million tonnes at 1.83 grams per tonne of gold). The company noted that the mine benefited from mining the Kari Pump Pit and a high-grade pocket within the pit, but that we will see a dip in production in Q4 (to be expected after lapping some tough comparisons sequentially), with more feed coming from the lower-grade Kari West and Vindaloo pits. Still, the mine is on track to deliver at the high end of guidance and potentially above the top end based on ~228,000 ounces produced to date and a guidance range of 270,000 to 285,000 ounces, and margins have remained at industry-leading levels despite higher fuel and consumables costs and higher sustaining capital with year-to-date AISC of $959/oz (albeit up from the first nine months of 2022).

{kind=link}

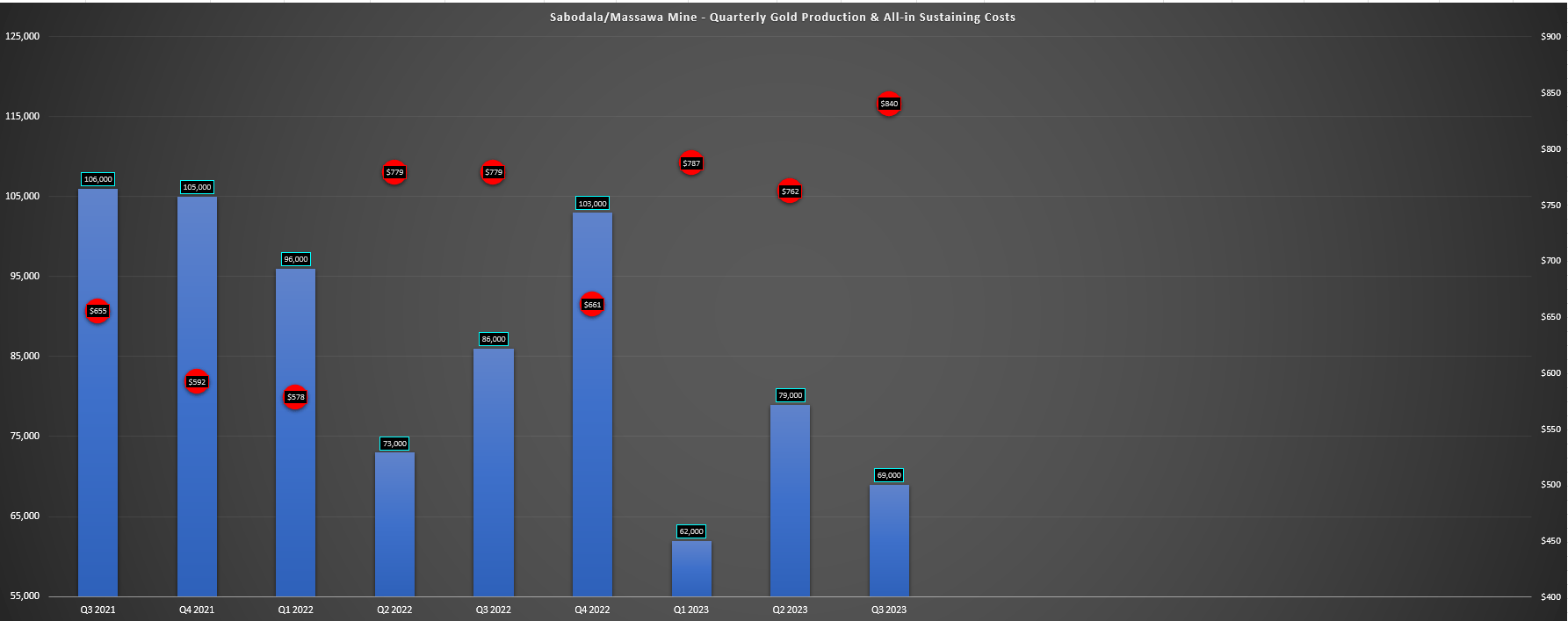

Moving over to Sabodala-Massawa, production was down year-over-year to ~69,000 ounces (Q3 2022: ~86,000 ounces) with all-in sustaining costs increasing to $840/oz vs. $779/oz. The lower production was related to a decline in grades (2.06 grams per tonne of gold vs. 2.84 grams per tonne of gold), and year-to-date production was significantly lower with less high-grade feed from the Sofia North, Bambaraya, and the Sabodala pits. The result is that the mine is tracking to the lower end of its guidance of 315,000 to 340,000 ounces. On a positive note, Q4 is expected to be much stronger from higher grade ore coming from the Sabodala and Massawa North Zone pits and recoveries should benefit from a higher blend of oxide ore from Niakafiri East and Sofia North at the mill. Plus, the expansion project continues to progress well (84% of $290 million total capital costs committed, $114 million spent year-to-date and ~$167 million incurred), and construction is beginning on a 37MW PV solar plant to reduce fuel and power costs (Q1 2025 commissioning).

Sabodala-Massawa Production & Costs - Company Filings, Author's Chart

{kind=link}

As for the mine's AISC ($795/oz year-to-date vs. $703/oz in year-ago period), it was higher due to lower sales and higher fuel/consumables costs like Endeavour's other assets, but still miles below the industry average of ~$1,350/oz. However, while AISC is expected to come in above $770/oz this year, production will increase materially starting in late 2024 once the new 1.2 million tonne per annum BIOX plant is in production, with production expected to be 400,000+ ounces at sub $800/oz costs in its first four years on a combined project basis. This would make this one of the more profitable gold mines globally from a production/scale standpoint, rivaling other impressive assets like Greenstone and Cote Gold at ~400,000 ounces with sub $850/oz AISC in their first few years (but which are shared assets vs. 90% ownership for Endeavour). Lastly, Endeavour noted that sustaining would be lower at Sabodala-Massawa (and company-wide), with the acceleration of the Niakafiri East and Sofia North extension pits into the mine plan which has allowed the company to push out stripping at the Massawa pits into 2024.

Endeavour Mining - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

As for Ity and Mana, the two assets combined for production of ~103,000 ounces vs. ~123,000 ounces in Q3 2022 with lower grades at both sides. At Ity (~73,000 ounces produced), lower grades were partially offset by higher throughput (use of surge bin) and higher recoveries (addition of pre-leach tank and less fresh semi-refractory ore from the Daapleu pit). Meanwhile, at Mana (~30,000 ounces produced), gold production was down due to lower grades (1.66 grams per tonne of gold vs. 1.90 grams per tonne of gold) and lower recovery rates. Regarding grades, the Maoula pit which is nearing the end of its life contributed lower grades and we've seen a slower than planned ramp-up underground at Wona with the new underground mining contractor. This has resulted in a meaningful negative revision in cost and much higher costs year-over-year when combined with inflationary pressures and a higher strip ratio ($1,408/oz vs. $993/oz).

Overall, the production and cost results at Mana might have been disappointing from a headline standpoint, but we will see higher production in Q4 with improved development rates (2,685 meters in Q3 at Siou and Wona combined vs. 2,217 meters in Q2), allowing for an increased proportion of stope ore and a higher overall grade with the open-pit tonnes continuing to drop at Maoula as it approaches the end of its mine life. This higher denominator (increased production) should allow for a meaningful improvement in costs. And as for sales performance, Endeavour reported quarterly revenue of ~$530 million and operating cash flow of $115 million ($121 million before working capital changes), which was down year-over-year from $568 million and $154 million, respectively, but largely due to operating four mines instead of two in the period.

Endeavour Mining - Quarterly Revenue & Cash Flow - Company Filings, Author's Chart

{kind=link}

Costs & Margins

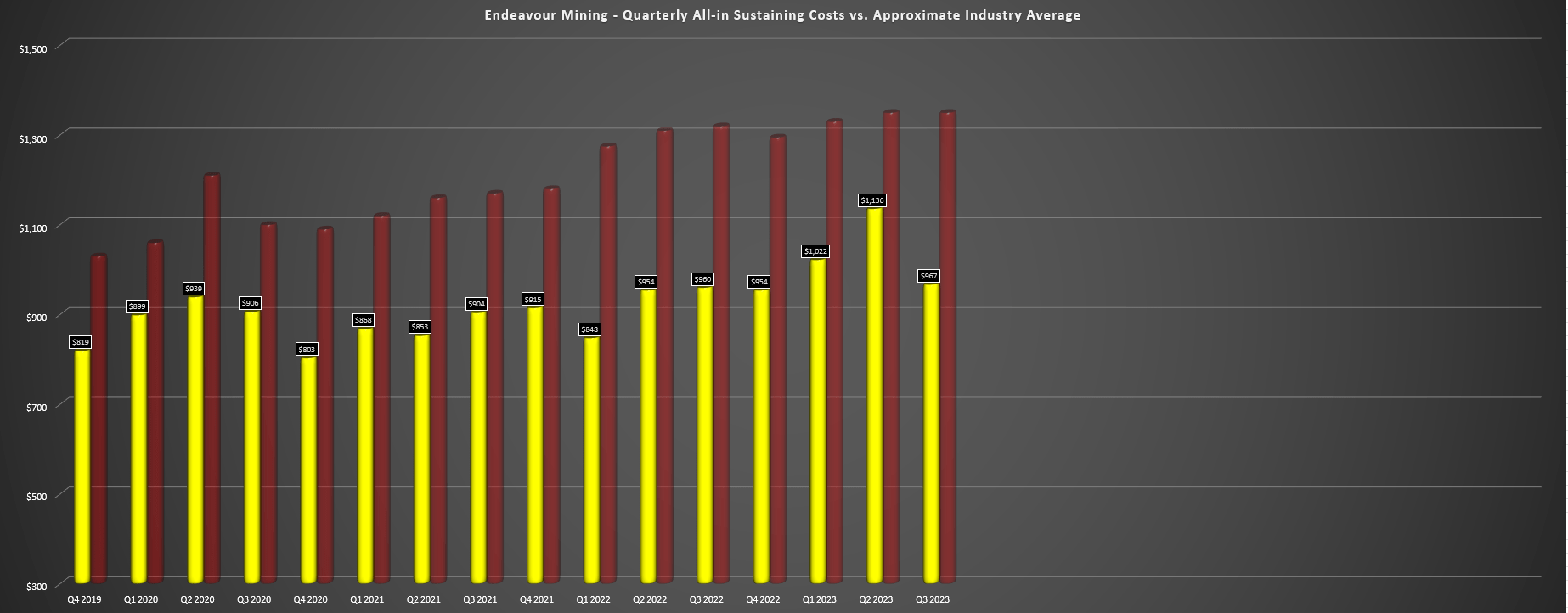

Moving over to costs and margins, Endeavour Mining had another solid quarter, reporting all-in sustaining costs of $967/oz which were nearly 30% below the estimated industry average (~$1,350/oz). And while costs were up year-over-year (Q3 2022: $967/oz on non-adjusted basis or $856/oz vs. continuing operations), it's worth noting that Endeavour's top-3 mines average AISC of ~$830/oz, with Mana dragging up the average due to its lower production in the period. It's also worth noting that we will see a greater proportion of production from its lowest-cost mine (Sabodala-Massawa) in H2 2024 with the expansion on track for completion in Q2-2024 (BIOX reactors, neutralization tanks and BIOX CCD thickener tankage and pipe racks erected, plus first populations of BIOX material on site and growing in plant). In addition, the Lafigue Project (scheduled for Q3-2024 first gold pour) will also add meaningful high-margin production, and is expected to produce ~203,000 ounces at sub $925/oz costs even factoring in inflationary pressures. Hence, Endeavour has a clear path to holding its position as one of the lowest-cost miners, with the potential for ~1.3 million ounces at ~$950/oz costs in 2025.

Other BIOX plants commissioned over the past two decades include Fosterville in Australia, Kokpatas in Uzbekistan, and Runruno in the Philippines.

Endeavour Mining - Quarterly AISC - Company Filings, Author's Chart Endeavour Mining Quarterly AISC Margins - Company Filings, Author's Chart

{kind=link}

{kind=link}

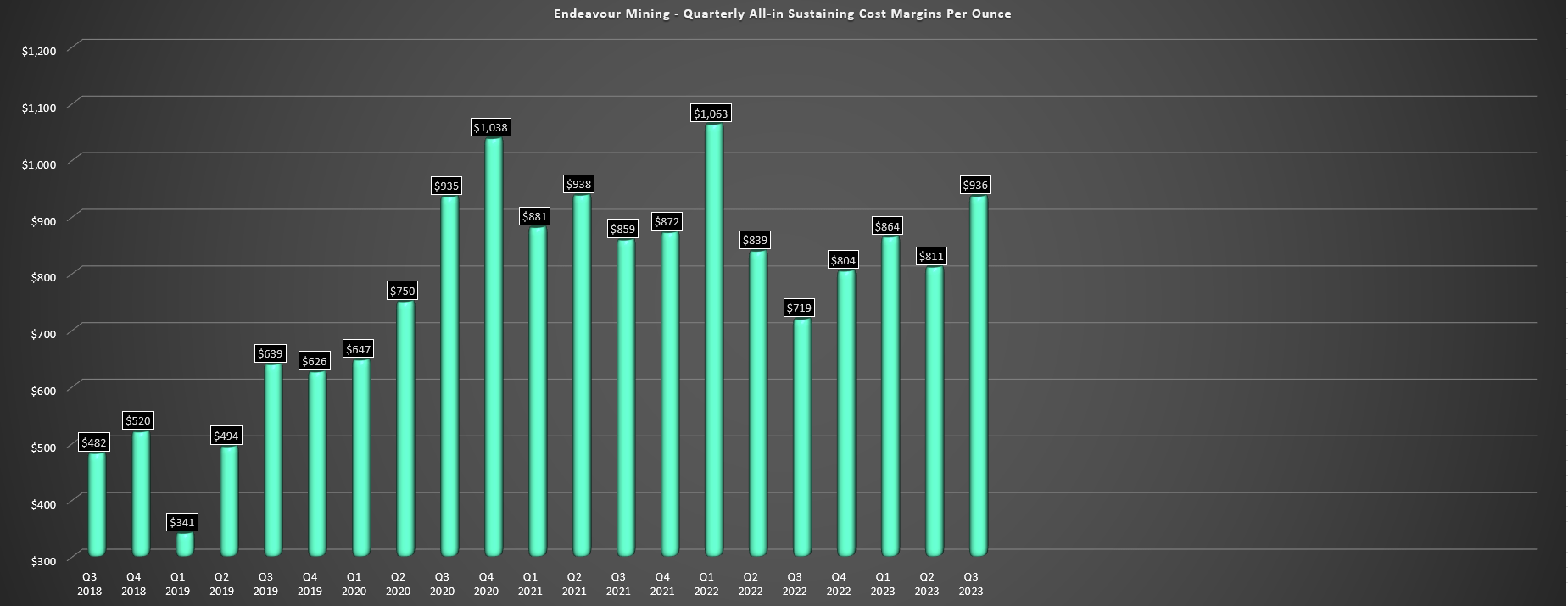

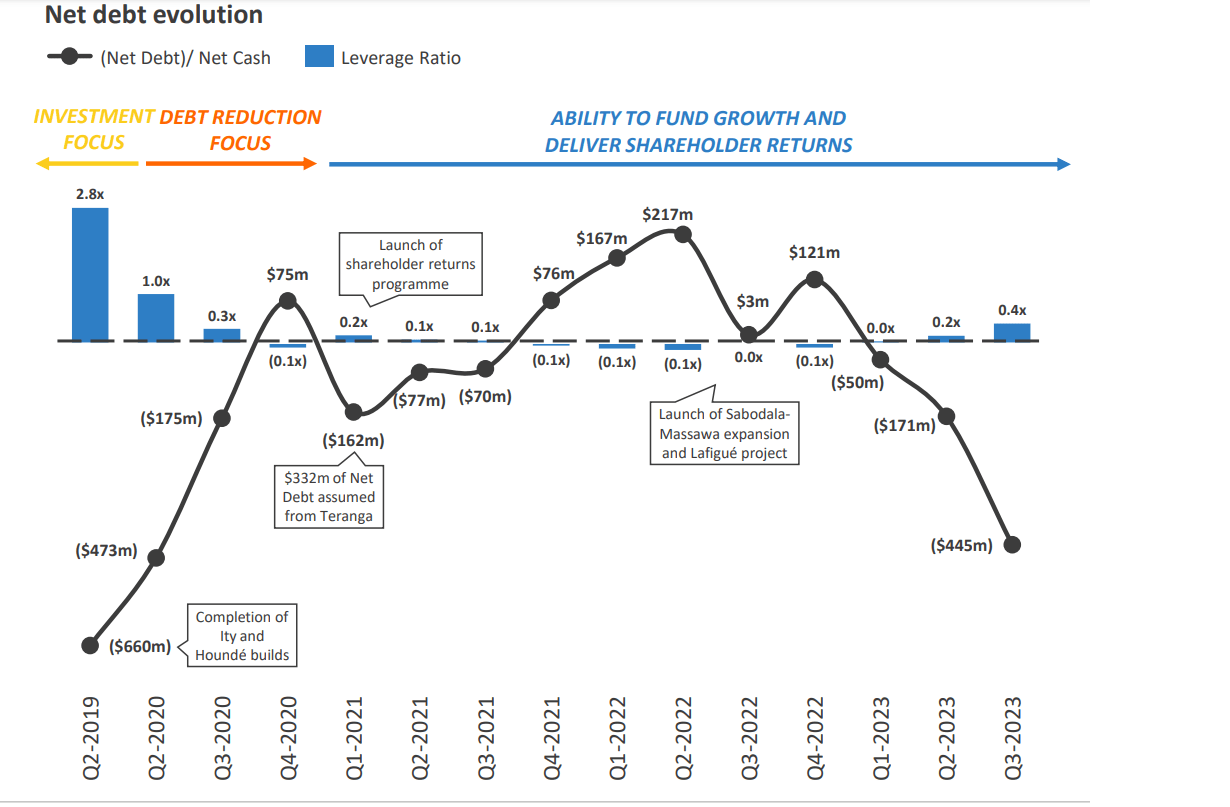

Looking at its results from a margin standpoint, Endeavour's AISC margins came in at $936/oz in Q3 2023 (+30% year-over-year) helped by shedding its lower-cost assets and the benefit of a higher average realized gold price, offset by delivering into gold forward contracts at $1,828/oz which it has put in place to reduce risk during its period of elevated capex. Plus, these margins should improve further on a sequential basis (Q4 vs. Q3) with higher production and a higher average realized gold price, with the gold price averaging $1,940/oz quarter-to-date. Finally, while free cash flow was negative in Q3 at [-] $76 million, this was largely due to the sharp increase in growth capex ($116 million), with the result being that net debt increased to $445 million. However, the below chart highlights that while the company's net debt has increased materially, this is during a period of industry-leading shareholder returns and its leverage ratio is much lower than it was during its past phase of growth (Ity & Hounde) given its larger production profile.

{kind=link}

Recent Developments

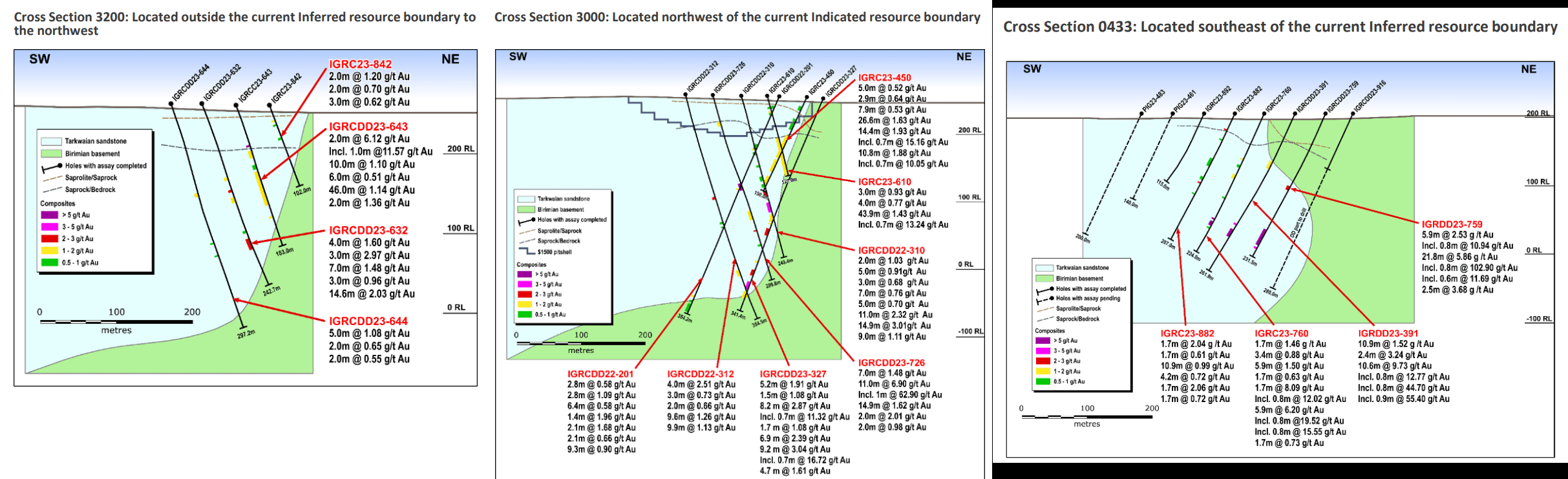

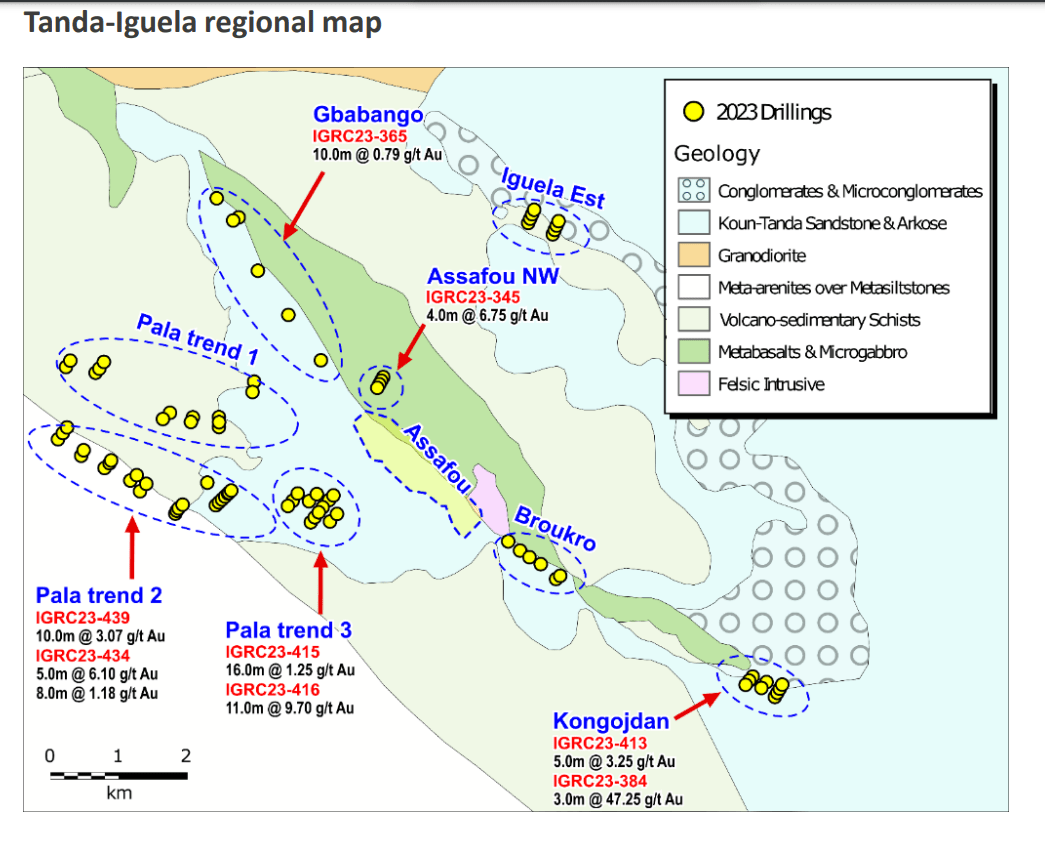

As for recent developments, Endeavour noted that its growth projects remaining on budget and schedule (Q2-2024 and Q3-2024 for Sabodala-Massawa Expansion and Lafigue, respectively), which will result in relaxed growth capital spend this time next year and the ability to consider increasing shareholder returns. However, the real story continues to be Tanda-Iguela, which is turning into a monster with its strike length increased by ~50% to 3.3 kilometers and with ~180,000 meters expected to be drilled this year ahead of an updated resource at year-end (131,000 meters year-to-date). For those unfamiliar, the ~3.0 million ounce mid-grade resource was based on just ~55,000 meters along a 2.2 kilometer mineralized trend, suggesting that we should see a meaningful increase in indicated ounces (previously: 14.9 million tonnes at 2.33 grams per tonne of gold), and a significant increase in the overall resource.

{kind=link}

Although Assafou continues to exceed management's expectations, there are multiple targets nearby (high-grade intercepts on nearby Pala Trend 2 and 3 targets include 10.3 meters at 3.07 grams per tonne of gold and 11 meters at 9.7 grams per tonne of gold, and 3.0 meters at 47.25 grams per tonne of gold at Kondojdan) that could act as satellite opportunities. Hence, it's no surprise that Endeavour continues to suggest that this asset has "Tier-1 potential" which by its definition of Sabodala-Massawa would suggest that it seems Tanda-Iguela as an asset with 400,000 ounce per annum production potential. Given the favorable metallurgy to date (~95% recoveries with over 55% recoverable by gravity) and size of this asset which could benefit from economies of scale, the long-term picture for Endeavour's margins is also quite bullish with this having the potential to produce at sub $850/oz AISC later this decade.

Tanda-Iguela Regional Targets & Drill Highlights - Company Website

{kind=link}

So, with what ultimately looks to be ~5.0 million ounce resource potential for this project, Endeavour certainly isn't under pressure to do M&A in my view, even if there are several attractive opportunities when it's able to delineate ounces for ~$10/oz (median price paid in Tier-1 jurisdictions past four years for M&I ounces is ~$130/oz). Plus, from a growth standpoint (and assuming Hounde can maintain a ~250,000-ounce production profile which looks possible with Mambo, the underground potential at Vindaloo and possible Golden Hill integration), Endeavour could ultimately grow into a 1.5+ million ounce producer organically (in line with its previous potential before it sold Wahgnion and Boungou) but with higher-quality assets on balance and the potential for two Tier-1 (400,000+ ounce per annum) mines. Hence, while the production/cost performance is commendable, the exploration success at Tanda-Iguela could be a game-changer with a major step-change in growth by the end of this decade.

Summary

Endeavour Mining had another solid quarter in Q3, has strong liquidity of ~$870 million with another $97 million expected from its recent divestments (delayed payment) and there looks to be upside in its dividend and more aggressive share buybacks post-2024 as growth projects move across the finish line. Meanwhile, the company continues to be one of the lowest-cost producers with strong organic growth yet trades at a very reasonable valuation of just ~4.8x FY2024 P/CF. To summarize, with an attractive history of discipline when it comes to M&A (a rarity in this sector), high margins and a trend of growing returns to shareholders once its major growth projects are complete, I would view any pullbacks below US$19.45 as buying opportunities.

For further details see:

Endeavour Mining: A High-Margin Producer At A Very Reasonable Price