EDVMF - Endeavour Mining: Beating Guidance In A Sea Of Misses

Summary

- Endeavour Mining is one of the better-performing gold miners year-to-date, up 3% for the year vs. a negative return for the Gold Miners Index.

- I attribute this Endeavour's outperformance to being one of the few companies to meet its production and cost guidance in a challenging year.

- Looking ahead, FY2023 will be another strong year for the company and we should see double-digit production growth looking out to FY2026 with two growth projects underway (Sabodala-Massawa Expansion/Lafigue).

- Given Endeavour's continued operational excellence and industry-leading margins, I would view pullbacks in the stock below US$19.20 as buying opportunities.

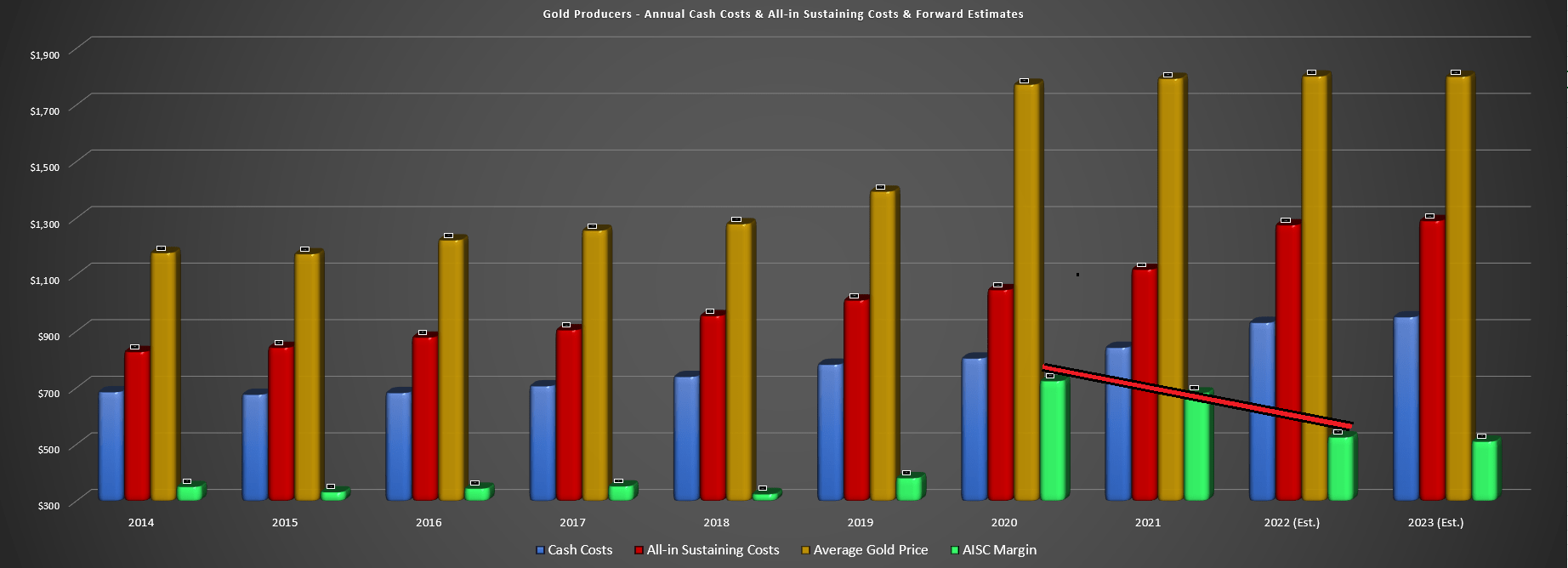

The Q4 and FY2022 results are finally underway for the Gold Miners Index ( GDX ), and to date, the results have left much to be desired. This is because we saw another year of margin compression with 90% of miners missing cost guidance, and many also coming in shy of production guidance despite relatively easy year-over-year comps (COVID-19 related absenteeism in 2021). Unfortunately, while the gold price appeared to be bailing producers out a little and helping to offset some of the significant cost creep, the gold price has pulled back sharply over the past two weeks, setting up what could be another year of margin compression or flat margins after two years of sharp declines.

Gold Producers - Cash Costs, AISC & AISC Margins + Forward Estimates (Company Filings, Author's Chart)

{kind=link}

While this certainly isn't ideal for the sector, this continues to be a stock-pickers market, and some producers have done a very solid job despite the challenging environment (labor tightness, supply chain headwinds, inflationary pressures). One name that stands out is Endeavour Mining ( EDVMF ), which delivered within cost guidance and beat output guidance in a sea of misses, producing ~1.4 million ounces of gold at industry-leading costs of ~$928/oz. Meanwhile, it over-delivered on shareholder returns, helped by opportunistic share repurchases at $21.46/share. Let's inspect its Q4/FY2022 preliminary results below:

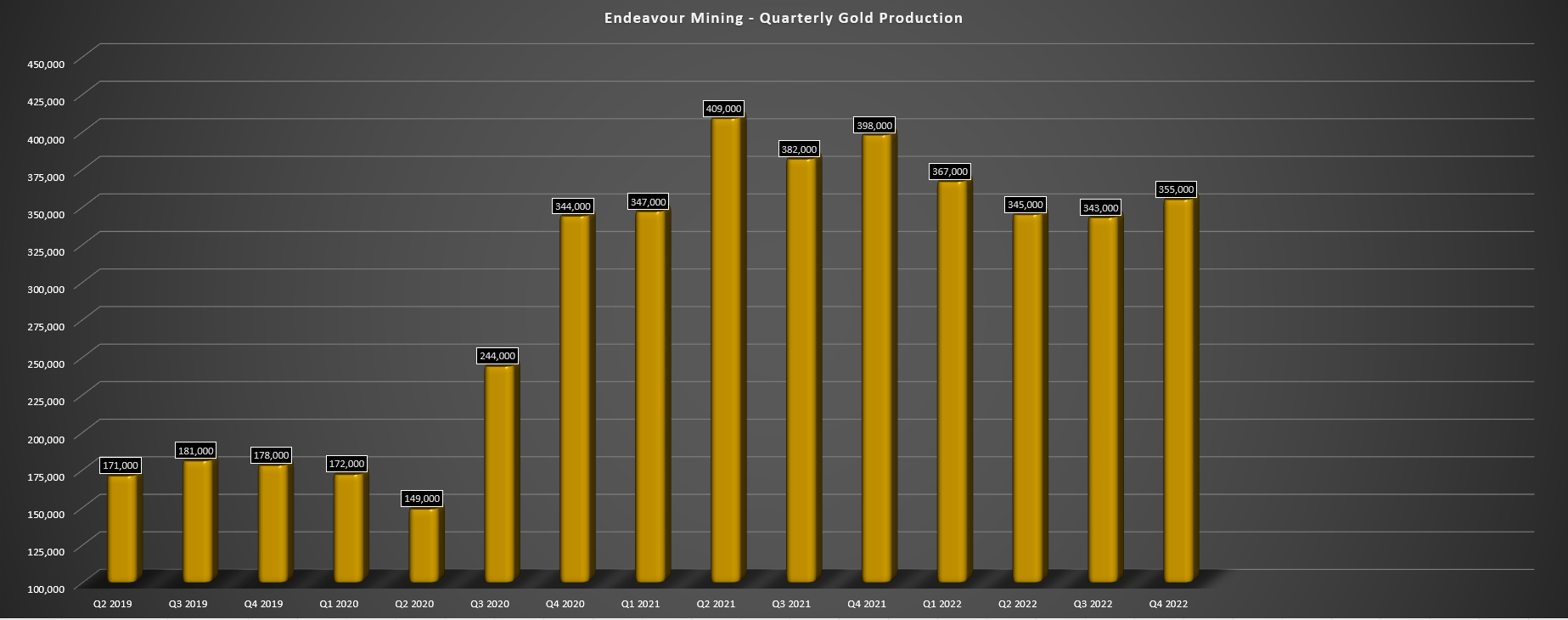

Q4 & FY2022 Production

Endeavour Mining released its preliminary Q4 results last month, reporting quarterly production of ~355,000 ounces of gold, an 11% decline from last year's levels if we don't adjust for portfolio divestments (Karma Mine). This strong finish to the year from its continuing operations helped the company to deliver at the top end of guidance (~1,315,000 to ~1,400,000 ounces) and this marked its 10th consecutive year of achieving or beating annual guidance, an impressive feat especially given the recent sector-wide headwinds. Key contributors to the solid 2022 performance included its Ity, Mana, and Hounde mines, offsetting misses at smaller assets (Boungou and Wahgnion).

Endeavour Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

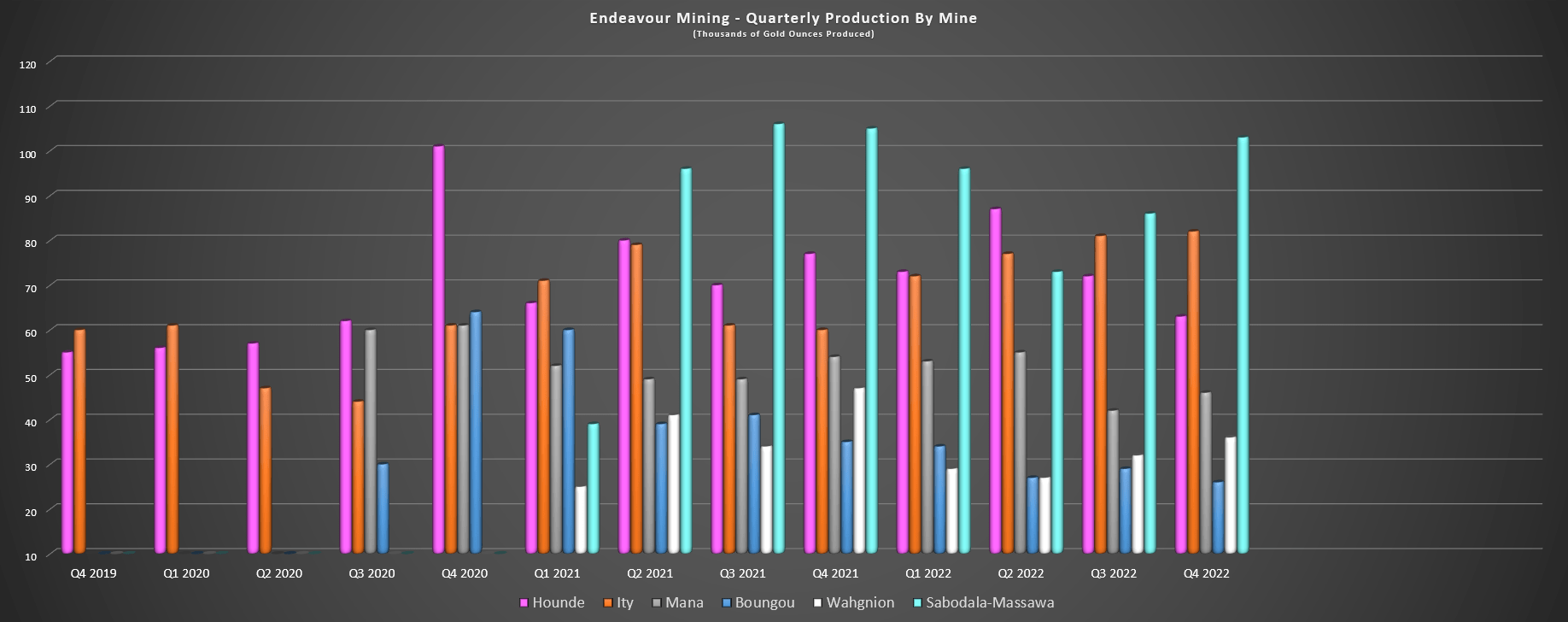

Beginning with the outperformers, Hounde had a fantastic year. This was despite a soft Q4, with quarterly and annual production of ~63,000 and ~295,000 ounces, respectively. Although the ~63,000 ounces in Q4 was down 18% year-over-year, Hounde's annual production trounced the FY2022 guidance mid-point of 268,000 ounces. The solid performance was driven by higher throughput (5.04 million tonnes processed), helped by optimization work and increased tonnes milled in Q4 (benefiting from softer ore at Kari West).

A slight decline in grades offset the increased throughput, with ongoing stripping at Kari Pump in Q4 (high-grade oxide feed) and mining in lower grade zones of Kari Pump, Vindaloo Main, and the Kari West pits in Q3. Given the beat vs. guidance, all-in-sustaining costs [AISC] came in at a very respectable $809/oz despite a year of severe inflationary pressures, with these costs over 37% below the FY2022 industry average (~$1,280/oz). Based on FY2023 guidance, Hounde has another strong year ahead, with production expected to come in at ~278,000 ounces at ~$890/oz despite an increase in sustaining capital (waste stripping and fleet rebuilds).

{kind=link}

Moving over to Endeavour's Ity Mine, this Tier-2 scale asset had a great 2022 as well, evidenced by FY2022 production of ~313,000 ounces at AISC of $812/oz, an improvement from the prior year despite lapping tough comps (~272,000 ounces at $836/oz). The strong performance was driven by higher throughput and feed grades, with ~6.35 million tonnes processed at 1.80 grams per tonne of gold and 85% recovery rates, up from ~6.25 million tonnes at 1.65 grams per tonne of gold and 80% recoveries in FY2021. The FY2022 production of ~313,000 ounces represented a 19% beat vs. its guidance mid-point, a massive beat, resulting in exceptional cost performance.

Endeavour attributed the better than planned production in FY2022 at Ity to grade outperformance, higher recoveries related to less transitional material from Daapleu, and improved plant performance because of the use of the surge bin. Based on FY2023 guidance of ~293,000 ounces at $878/oz, Endeavour can expect another very strong year from Ity, helping to keep its consolidated all-in-sustaining costs below $1,000/oz. Notably, these high margins at Ity (FY2023 expectations) are despite an 87% increase in sustaining capital year-over-year ($25 million vs. $13.4 million).

Looking at the underperformers, these were Endeavour's two smallest assets, Boungou and Wahgnion. At Boungou, production came in at just ~116,000 ounces (guidance mid-point: 135,000 ounces), with reduced mining activity due to supply chain headwinds that affected availability of high-grade ore. The lower sales volumes in FY2022 drove costs much higher ($1,064/oz vs. $801/oz) when combined with higher fuel, security, and consumables costs. At Wahgnion, FY2022 production came in at just ~124,000 ounces at $1,525/oz AISC due to lower grades and a higher strip ratio. Fortunately, 2023 will be a better year with higher production at lower costs (albeit back-end weighted), with expectations of 150,000 to 165,000 ounces of output.

Endeavour Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

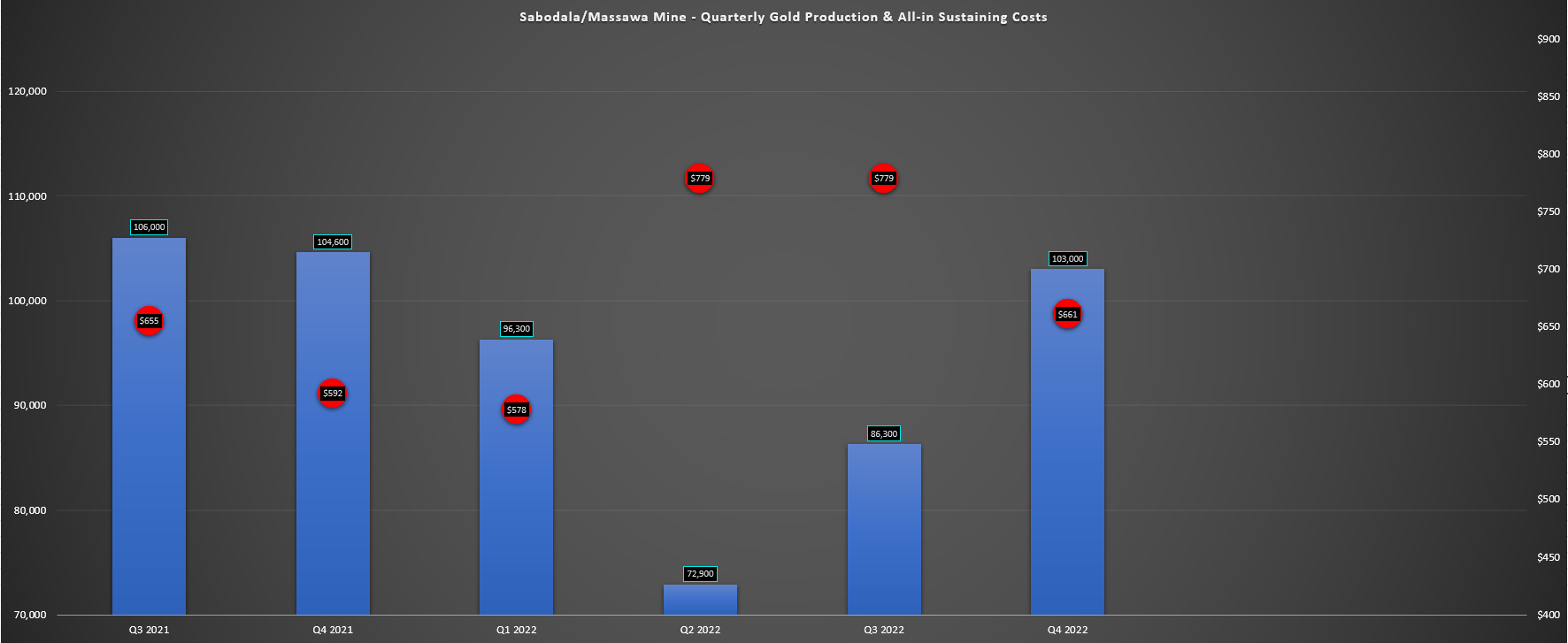

Finally, at Endeavour's largest mine, Sabodala-Massawa, the operation had a solid year but came up just short of meeting its FY2022 guidance. However, although it reported a near miss, the mine still had a phenomenal year relative to other assets sector-wide, with annual production of ~358,000 ounces at all-in-sustaining costs of $691/oz. These costs were 46% below the industry average and although FY2023 will be a softer year based on guidance (~328,000 ounces at $785/oz), this will still be one of the lowest cost mines globally. The lower gold production was related to lower grades without the benefit of the high-grade Sofia pit, and the 2022 miss was because of delayed access to high-grade ore.

Sabodala-Massawa - Production & AISC (Company Filings, Author's Chart)

{kind=link}

Endeavour noted in its prepared remarks that its Sabodala-Massawa BIOX Expansion remains on budget and on schedule, with plans for the project to be in H1 2024. Meanwhile, its Lafigue Project also remains on track and 53% of Sabodala-Massawa capital and 30% of Lafigue capital is committed to date with pricing in line with the company's expectations. In the case of Lafigue, this will add ~200,000 ounces per annum at sub $900/oz AISC. Meanwhile, the Sabodala-Massawa Expansion will add incremental gold production of ~194,000 ounces at sub $550/oz all-in-sustaining cost, with both projects helping Endeavour to maintain its industry-leading margins.

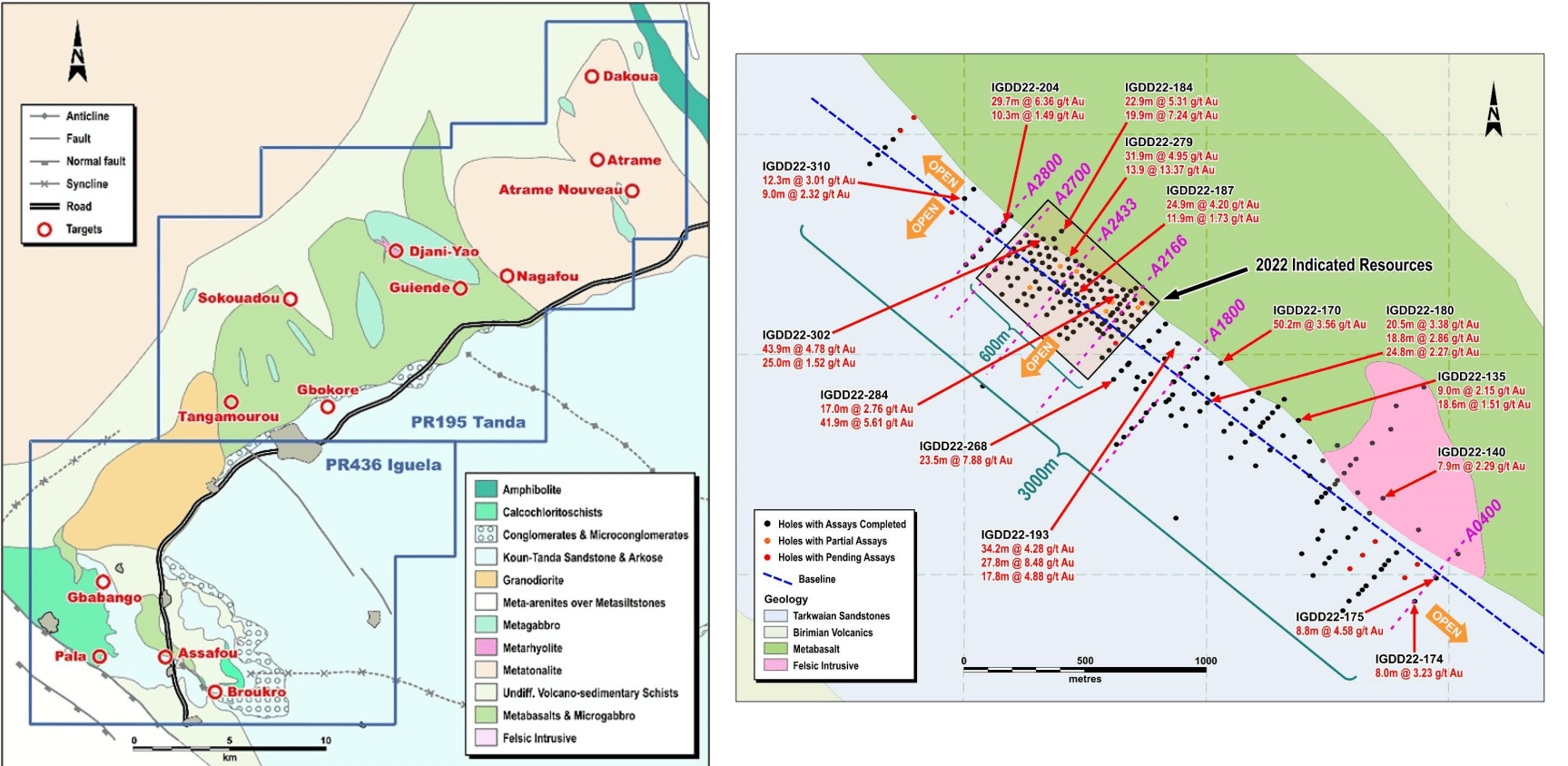

Finally, it's worth noting that Endeavour has made a new greenfields discovery in Cote d'Ivoire (Tanda-Iguela Property) that appears quite significant. The company has outlined an indicated resource of ~14.9 million tonnes at 2.35 grams per tonne of gold (1.1 million ounces) with an additional 32.9 million tonnes at 1.80 grams per tonne of gold (1.9 million ounces). This combines for a total resource of ~3.0 million ounces of gold and the indicated resource base has been delineated over less than 20% of the mineralized system identified to date. Notably, these indicated ounces were delineated at an impressive cost of just $10/oz, which is phenomenal if they can be pulled out of the ground for ~$1,400/oz (projected AISC plus growth capex to build a stand-alone project)

Tanda-Iguela Property, Targets, and Assafou Resource (Company Presentation)

{kind=link}

Endeavour noted in its recent presentation that preliminary metallurgy is favorable with the potential for ~95% recovery rates and a significant portion recoverable by gravity, and there are currently 10 other targets identified on the property to the north, northeast, and directly northwest. The company has budgeted 50,000 meters of drilling this year to test additional targets, and if successful, the company could unearth a 5.0+ million-ounce projected (M&I plus inferred) which could be its next major development project closer to the end of this decade. Given that Assafou appears amenable to open-pit mining and benefits from infrastructure, this could be another sub $1,000/oz AISC operation to add to its portfolio.

Endeavour has estimated mining costs to range from $2.10 to $3.12/tonne for oxides, transitional, and fresh rock, with a very reasonable 5.9/1 strip ratio for a deposit with these grades.

To summarize, from both an operational and exploration standpoint, Endeavour had an exceptional year and this year is expected to be just as exciting with another year of aggressive exploration budget ($22 million greenfield, $70 million total). So, regardless of where the gold price goes this year, Endeavour should have a great year, especially if it can deliver into guidance yet again and enjoy AISC margins of ~$900/oz in FY2023 ($1,850/oz gold price [-] $930/oz AISC).

Costs & Margins

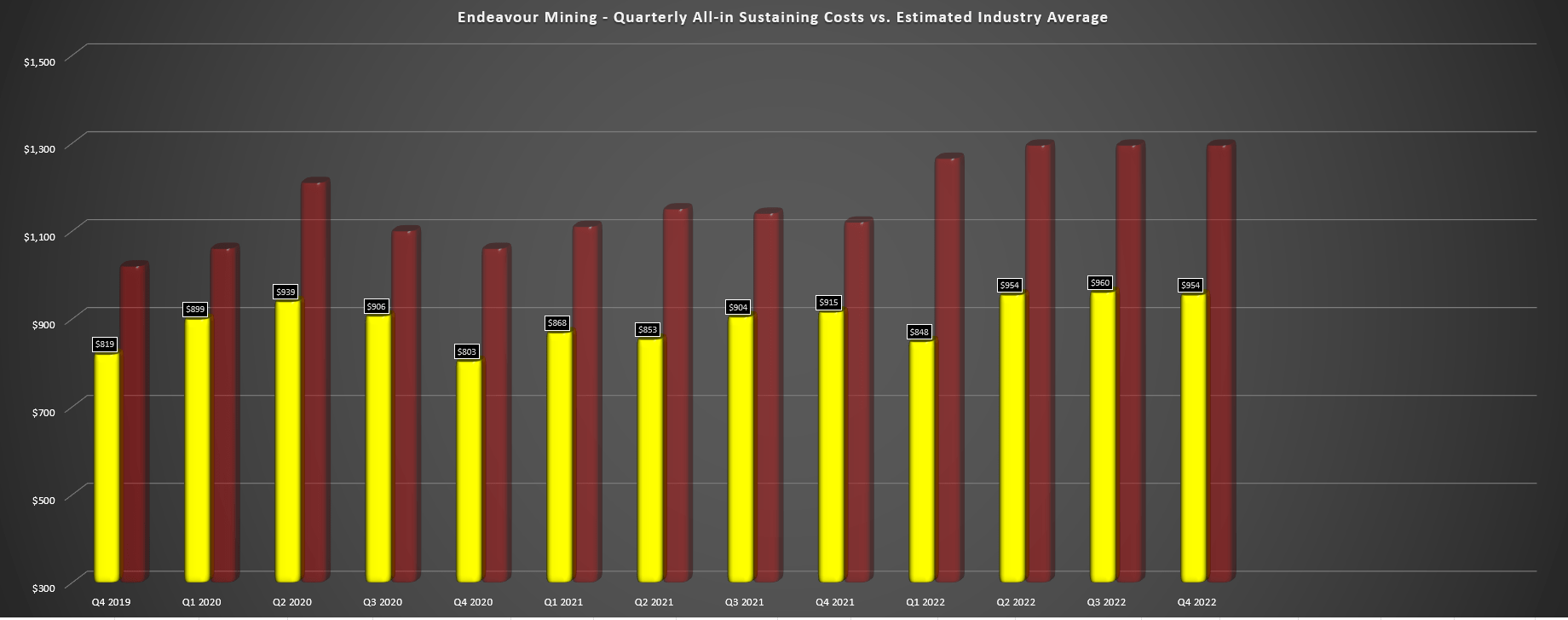

Moving over to costs and margins, Endeavour reported preliminary AISC of $954/oz in Q4 2022, a 5% increase from $915/oz in the year-ago period. The increase in costs was driven by inflationary pressures (fuel, explosives, grinding media) combined with higher security costs. Fortunately, Endeavour benefited from in-country fuel pricing which helped it to avoid spikes in energy prices with the in-country fuel pricing resulting in pricing being adjusted periodically. Meanwhile, Endeavour benefited from having a considerable portion of its costs in Euros (65%), with the Euro declining significantly vs. the US Dollar ( UUP ) last year.

Endeavour Mining - Quarterly AISC vs. Industry Average (Company Filings, Author's Chart)

{kind=link}

Looking at the chart above, we can see that while Endeavour's AISC increased year-over-year, it remains well below the industry average (red bars), and should only increase 5% year-over-year using the mid-point of guidance ($968/oz). Given the company's track record of meeting cost guidance even in a period of difficult circumstances, I would not be surprised to see FY2023 AISC come in below $960/oz, which would be approximately 26% below the estimated FY2023 industry average of ~$1,290/oz for full universe of gold producers (40,000+ ounce gold producers and above).

This would represent industry-leading margins, and should help the company to command a premium multiple vs. other less diversified and higher-cost African producers.

Finally, from a margin standpoint, Endeavour may see a cost increase of 3-5% year-over-year in FY2023 with higher costs at all assets except Wahgnion (mostly because of easy year-over-year comps at this mine), but its average realized gold price is likely to increase as well. This is because its FY2022 average realized gold price came in at just $1,792/oz ($1,807/oz when including benefit of hedges), and I would not be surprised to see its average realized gold price come in above $1,840/oz this year (Endeavour has hedged 30,000 ounces per quarter at $1,828/oz through forward sales contracts or just under 10% of total production). So, even if Endeavour's AISC increases by $40/oz, this should be offset by a slightly higher average realized gold price, resulting in flat to higher AISC margins.

Valuation & Technical Picture

Based on ~248 million fully diluted shares and a share price of US$21.90, Endeavour trades at a market cap of ~$5.43 billion and an enterprise value of US$5.30 billion. This compares favorably to an estimated net asset value of ~$6.54 billion, with Endeavour trading at roughly 0.83x P/NAV despite being one of the lowest-cost producers sector-wide, only behind Orla Mining ( ORLA ), Lundin Gold ( LUGDF ) and Centerra ( CGAU ). However, what these three producers lack is diversification (two are single-asset producers currently), and Endeavour also has superior capital returns, with the potential for 5% plus returns to shareholders in 2023 depending on how aggressive the company is with share repurchases.

Using what I believe to be a fair multiple of 1.05x P/NAV to account for Endeavour's impressive development pipeline and reserve replacement offset by its less favorable jurisdiction profile (West Africa), I see a fair value for Endeavour of ~$6.88 billion [US$27.75]. This translates to a 27% upside from current levels (30% on a total return basis), making Endeavour one of the more attractively valued million-ounce producers, especially given Endeavour's consistent ability to make greenfields discoveries at a relatively low cost to augment an already strong pipeline (Lafigue, Tanda-Iguela). So, I would argue that this price target is multiple is conservative, making Endeavour one of the better buy-the-dip candidates sector-wide.

So, is the stock a Buy?

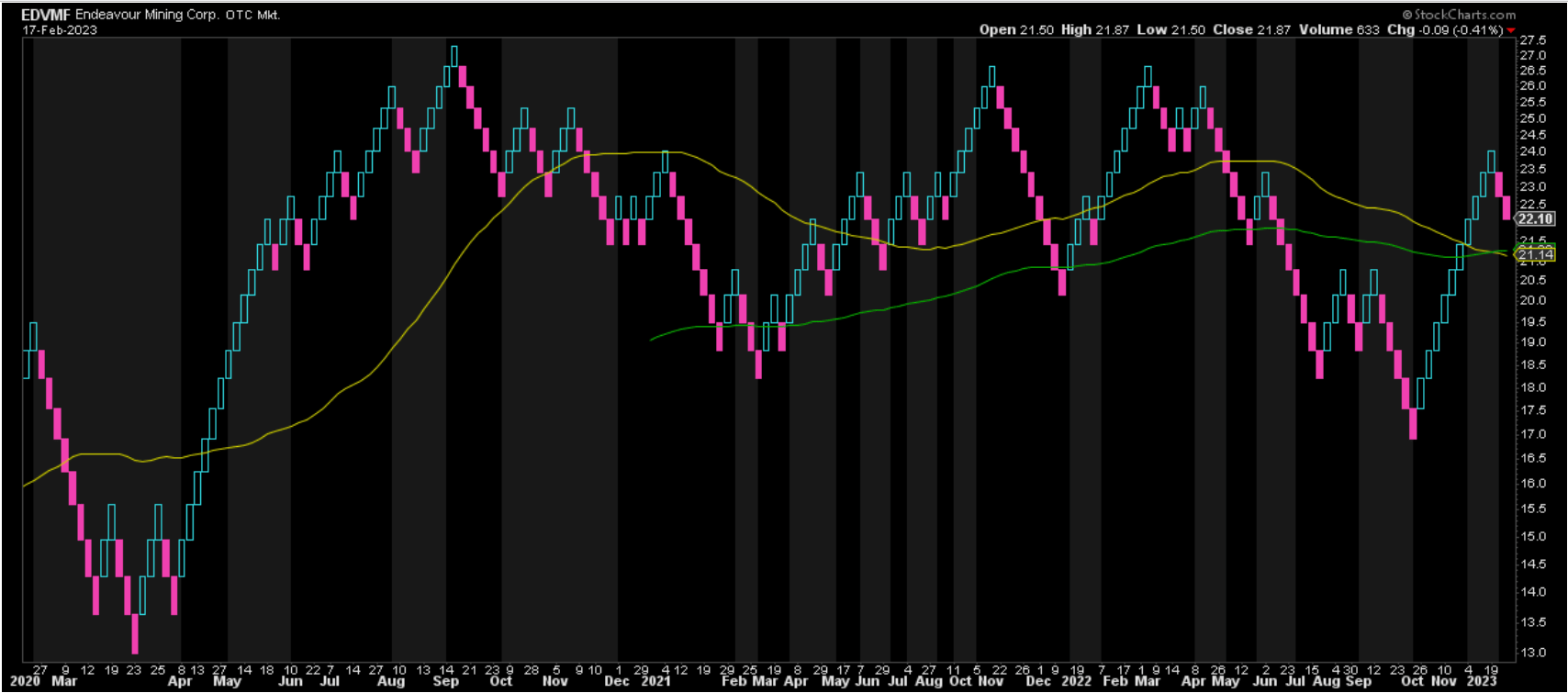

While Endeavour remains reasonably valued, I prefer buying cyclical names when they are out of favor and trading closer to support levels. In Endeavour's case, the stock is still near the mid-point of its support/resistance range even after its recent pullback, with strong support at US$17.85 and strong resistance at US$24.45. This doesn't mean that the stock can't go higher, but its current reward/risk ratio of 0.63 to 1.0 is below my preferred reward/risk ratio of 5.0 to 1.0 or better, meaning that EDVMF would need to decline below US$19.00 to become attractive from a technical standpoint. So, while I am long the stock from lower prices, I am not adding just yet.

EDVMF Daily Chart (TC2000.com)

{kind=link}

Summary

Endeavour Mining had another exceptional year and continues to do what many producers aren't willing to - focus on the most profitable ounces within the portfolio, not simply the absolute ounce figure for production. This strategy allowed it to remain at the bottom of the pack from a cost standpoint among its peer group, and with two high-margin growth projects in development, Endeavour should keep its throne as an extremely low-cost producer. Given Endeavour's diversified portfolio, superior shareholder returns, and attractive margin profile, I continue to see it as a top-10 producer. So, if I were looking for ways to add gold exposure, I see this as an attractive name to buy on dips.

For further details see:

Endeavour Mining: Beating Guidance In A Sea Of Misses