EDVMF - Endeavour Mining: Portfolio Optimization Maintains Industry-Leading Margins

2023-08-15 04:58:59 ET

Summary

- Endeavour reported solid Q2 results even if the headline results may have looked weak, with industry-leading AISC, solid margins, and a strong H2 on deck.

- Meanwhile, the portfolio has been optimized further with less exposure to Burkina Faso and low-cost assets, and Tanda-Iguela looks like it could be a potential game-changer for the company.

- In this update, I'll look at where Endeavour Mining's low-risk buy zone lies and why Tanda-Iguela could be a future pillar of major growth for Endeavour.

It's been a mediocre Q2 Earnings Season with the Gold Miners Index ( GDX ) down over 5% since it began last month, and suffering a drawdown of 10% at last week's lows. These mixed results can be attributed to one-time headwinds for some mines (extreme weather, power outages, strike actions) but also to rising costs, even if inflationary pressures have eased from the double-digit inflation experienced last year. Unfortunately, this has resulted in a limited benefit for the sector despite record gold prices from a margin standpoint, and some names like Coeur Mining ( CDE ) benefited less given that a portion of their gold output goes to a stream (Palmarejo) or hedges. Fortunately, Endeavour Mining ( EDVMF ) (EDV:CA) posted solid results and has an even better H2 on deck while being positioned to remain one of the lowest-cost miners sector-wide. Let's take a closer look below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

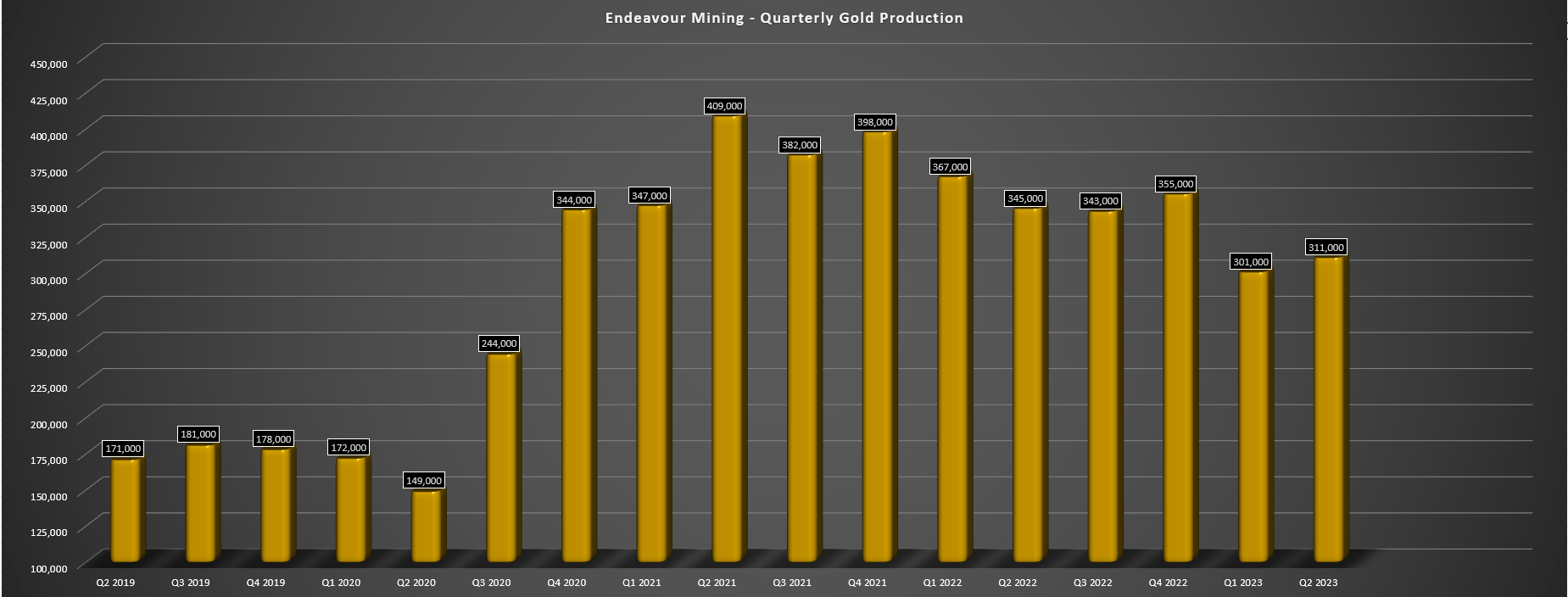

Endeavour Mining released its Q2 results earlier this month, reporting quarterly production of ~311,000 ounces of gold (all operations) or ~267,600 ounces of gold (continuing operations), a 10% decline from the year-ago period. The sharp decline in gold production was largely expected due to being up against tough year-over-year comps and a back-end weighted production profile this year with higher grades at Kari Pump & Vindaloo Main and increased stope production at Wona UG in H2, as well as what was forecasted to be a better H2 from its recently divested assets (Boungou and Wahgnion). So, while this decline in production might appear alarming, the production levels do not reflect the overall potential of this portfolio, which looks to have 1.50+ million ounce per annum potential long-term even post divestment.

Endeavour Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

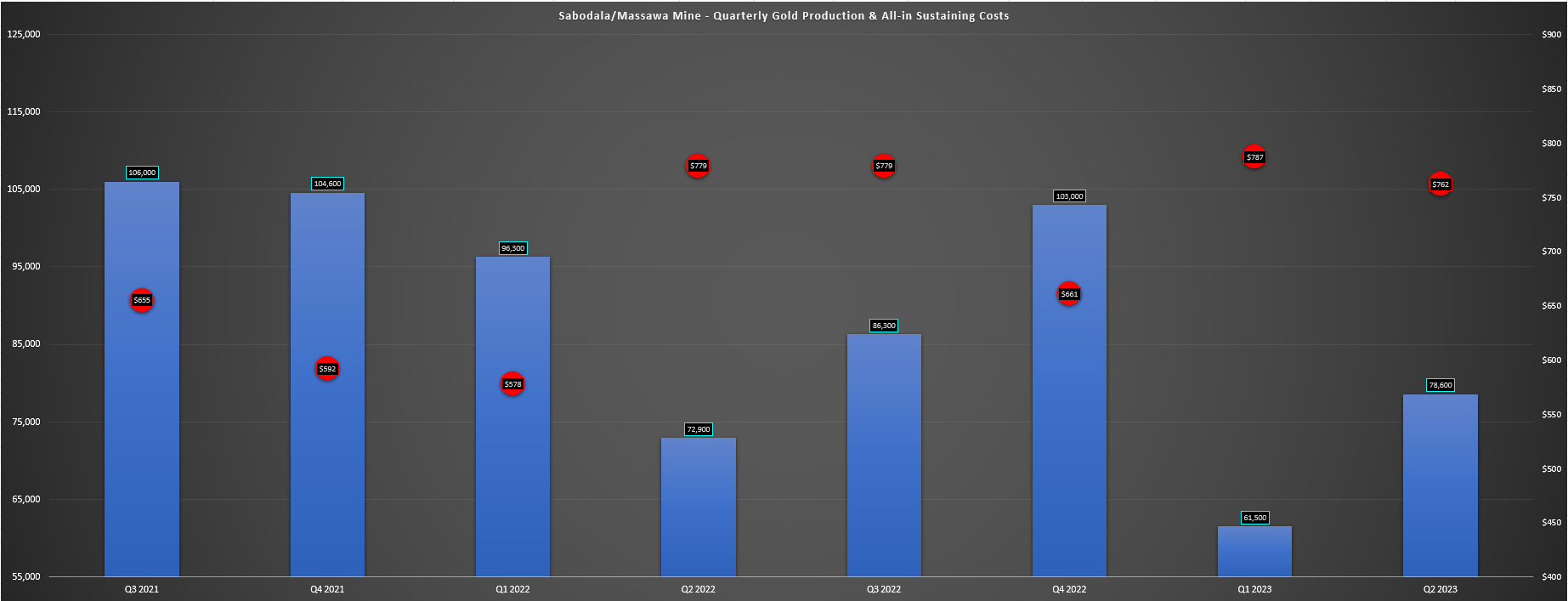

Digging into the operations a little closer, the company's Sabodala-Massawa Mine produced ~78,600 ounces of gold (Q2 2022: ~72,900 ounces), an 8% increase from the year-ago period. The higher output was driven by increased throughput (~1.2 million tonnes) and slightly better recoveries on a year-over-year basis, partially offset by lower grades (2.17 grams per tonne vs. 2.38 grams per tonne). As noted by the company, the grade decline was related to lower contributions from high-grade ore sources (Sofia North, Bambaraya, and Sabodala pits), and all-in sustaining costs of $762/oz remained at industry-leading levels, benefiting from lower sustaining capital partially offset by higher maintenance, fuel, and labor costs.

However, with ~140,100 ounces produced year-to-date and guidance for ~327,000 ounces or better at the midpoint, investors can look forward to a robust H2 out of this asset from an output standpoint. Meanwhile, Endeavour noted it has committed ~$219 million of a planned ~$290 million in growth capital for the ongoing Expansion Project, with pricing in line with expectations and project completion expected in June 2024. Also of note is that the company is looking at building a 37MW PV solar facility 3 kilometers from the site, which will allow Endeavour to benefit from $0.015/kWh power costs, down from $0.18/kWh from the heavy fuel oil generated cost of power currently. This could allow for a 20% plus reduction in power costs per annum at a modest cost of $55 million, with a Q1 2025 planned start date.

Sabodala-Massawa - Production & AISC - Company Filings, Author's Chart

{kind=link}

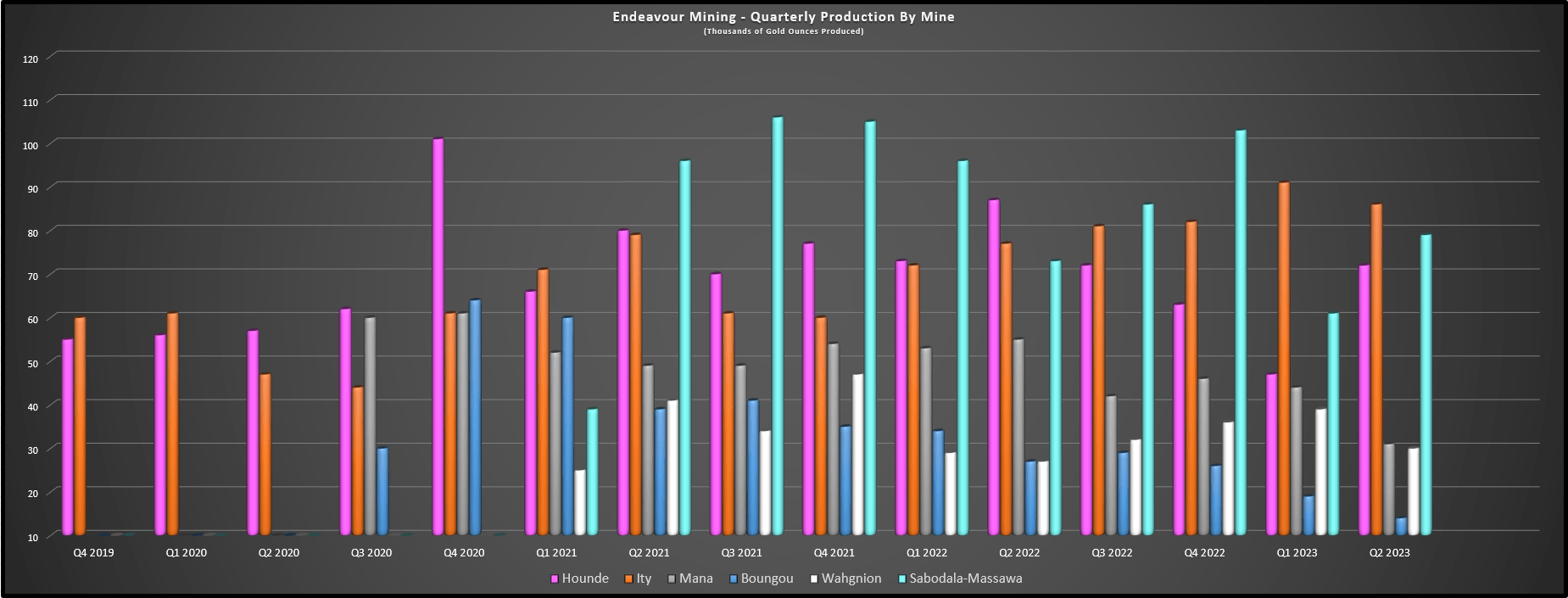

Moving over to one of Endeavour's other large mines, Ity, the asset produced ~85,900 ounces of gold in the period, a 12% improvement year-over-year, with it also reporting industry-leading all-in sustaining costs of $797/oz (Q2 2022: $895/oz). Ity's higher output was driven by another quarter of impressive throughput levels (~1.81 million tonnes processed at 1.61 grams per tonne of gold) and improved recoveries, offsetting the lower grades in the period. As noted by Endeavour, increased throughput in H1 benefited from the use of the surge bin while recoveries benefited from less semi-refractory feed in the ore blend. As for costs, they benefited from lower sustaining capital year-over-year, helping the mine to report costs over 40% below the industry average in Q2 (~$797/oz vs. ~$1,350/oz).

Endeavour - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

Finally, at the company's Mana Mine, production fell off sharply vs. the year-ago period, coming in at just ~31,100 ounces at all-in sustaining costs of $1,481/oz. This was certainly a disappointing result relative to Q2 2022 output of ~54,800 ounces at $905/oz, but the performance was softer for two reasons. For starters, the asset was up against very difficult comparisons with a feed grade just shy of 2.90 grams per tonne gold in Q2 2022. Second, the asset had abnormally low sustaining capital in the period, translating to a much lower AISC figure in the year-ago period. So, while underground tonnes mined were up in Q2 2023, there was less stope production from Siou UG and primarily low-grade development ore from Wona Underground. In addition, the mine saw a much higher strip ratio for open-pit tonnes in the period, and combined with inflationary pressures (fuel, consumables), costs rose materially.

{kind=link}

Unfortunately, the slower ramp-up for the new mining contractor at Wona UG means the Mana Mine is unlikely to meet its FY2023 guidance of 190,000 to 210,000 ounces at $950/oz to $1,050/oz all-in sustaining costs, which is not surprising with year-to-date production at ~75,000 ounces at $1,277/oz. Fortunately, we will see better performance in H2 as stope production ramps up from Wona UG, and mined grades are expected to improve at Siou UG as well. To summarize, while the tough H1 at Mana with a new mining contractor (that's also new to Africa) was unfortunate, I would expect much better results going forward from Mana, with more normalized production levels (~50,000 ounces per quarter) set to translate to a dramatic reduction in unit costs.

As it stands, Endeavour's continuing operations are tracking well behind updated FY2023 guidance midpoint of 1,095,000 ounces (~511,000 ounces year-to-date), but as noted earlier, the company expects a back-end weighted H2. This is expected at all of its sites with the exception of Ity, which is tracking ahead of guidance, setting Endeavour up for a solid Q3 and Q4 performance across nearly all of its mines. Meanwhile, from a cost standpoint, FY2023 AISC is expected to come in over 25% below the industry average at sub $950/oz, solidifying Endeavour's position as one of the sector's lowest-cost producers with scale next to Evolution Mining ( CAHPF ).

Finally, on M&A, news was released in late June that Endeavour Mining was looking at Kinross ( KGC ) as a possible acquisition target, but that talks did not advance past the initial stage due to differences in valuation. When questioned on the Q2 Conference Call, Endeavour's CEO Sebastien de Montessus reaffirmed their plan to remain disciplined and that it does not need M&A given its strong pipeline. I believe this is the right move and that only opportunistic M&A for quality assets makes sense, especially when the company is uncovering high-grade near-surface ore at a cost of less than $30/oz in regions where it's already present. And while Kinross would be a nice fit and provide improved diversification with two large-scale low-cost assets in Tasiast (Mauritania) and Paracatu (Brazil) and a strong development asset in Great Bear (Canada), it's encouraging to see the company being strict on the price it's willing to pay.

"On M&A, I think it's important is to continue to remain extremely disciplined. And while it's sometimes unfortunate to see leaks, it does have the advantage of, I guess, showing to the market that we are doing our homework, I mean, to evaluate assets that may fit our criteria. But we are able to also very easily walk away if we are too far away on price expectations. And I think it's the advantage of not being under pressure to do any acquisition given the strong organic growth pipeline. So we'll continue around those lines. There is no need, I mean, for M&A, and therefore, we'll continue to be extremely disciplined when looking at stuff."

- Q2 Conference Call, Endeavour President & CEO, Sebastien de Montessus

Costs & Margins

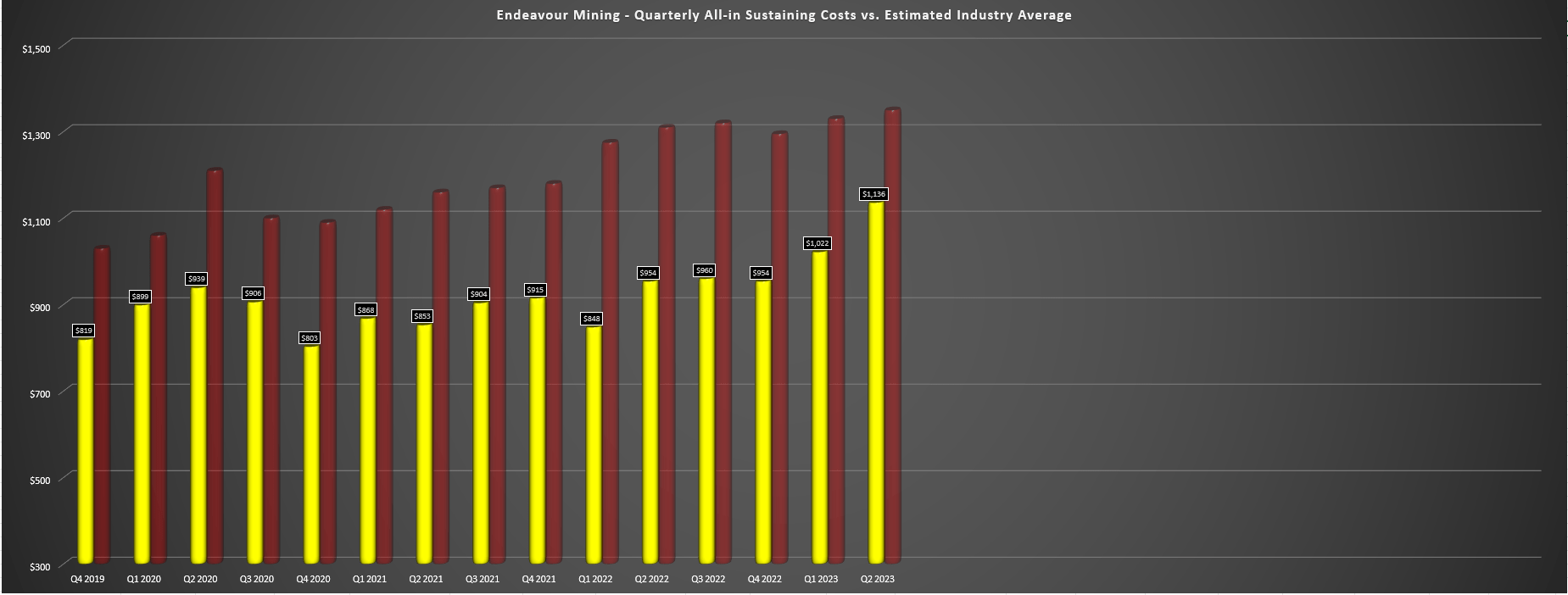

Moving over to costs and margins, Endeavour reported all-in sustaining costs of $1,136/oz in Q2 (all operations), or $1,000/oz based on solely continuing operations. While this was an increase from Q2 2022 levels, the $1,136/oz costs are not reflective of the current portfolio with the divestment of smaller high-cost assets that dragged up costs in the period (Boungou: $2,147/oz, Wahgnion: $1,817/oz). In addition, costs were elevated in H1 2023 due to lower production levels at its core assets, but we should see a meaningful improvement in costs during H2 with the benefit of higher production and sales. Plus, despite the increase in costs in Q2, costs still remained well below the industry average (red shaded bars).

Endeavour Mining - Quarterly AISC & Estimated Industry Average (Company Filings, Author's Chart)

{kind=link}

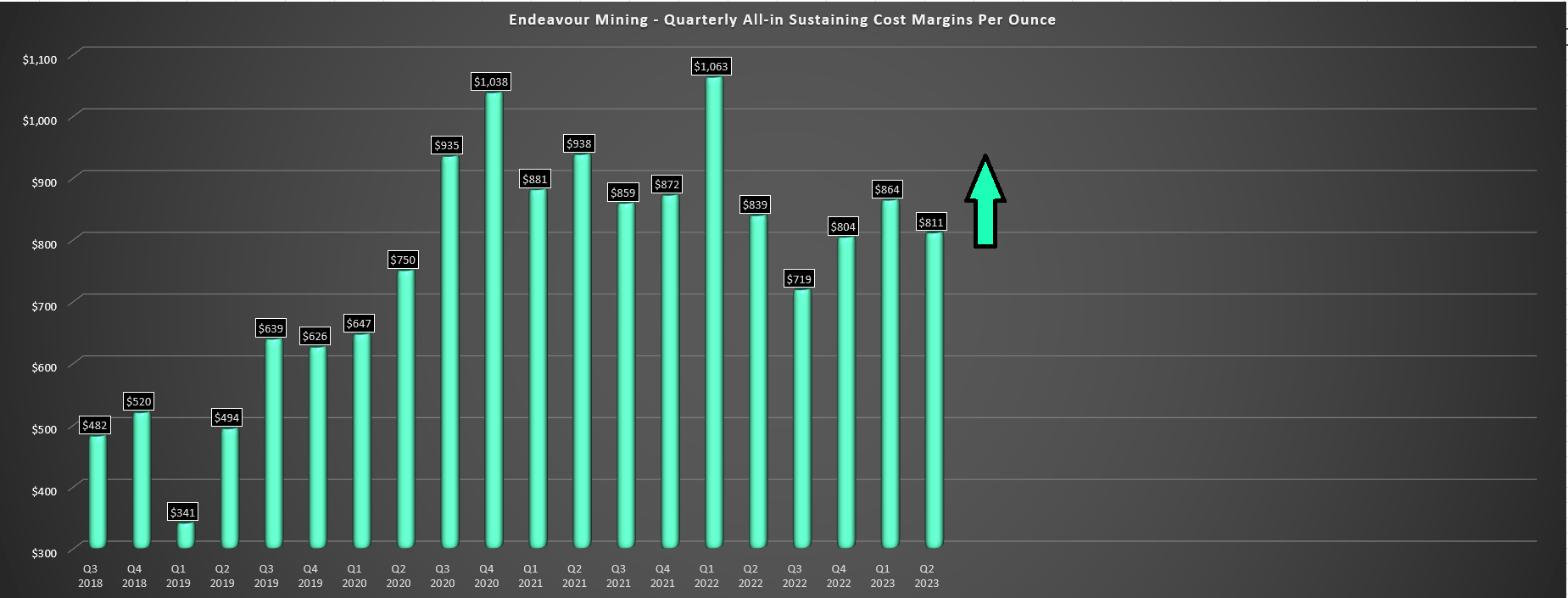

Looking at Endeavour's AISC margins, the company reported an average realized gold price of $1,947/oz in the period (Q2 2022: $1,879/oz), resulting in minimal margin compression despite ($811/oz vs. $839/oz) the higher costs from its non-core assets that were sold in the period. And on a continuing basis, AISC margins came in at industry-leading levels of $947/oz, and are set to improve even further in H2 if the gold price continues to cooperate. Plus, between the addition of a low-cost asset in Lafigue (sub $900/oz), improved unit costs at Mana, increased production from one of its highest-margin assets (Sabodala-Massawa), and room to further improve costs with a grid connection at Sabodala-Massawa plus a solar facility, Endeavour certainly has a path to maintain its sub-$950/oz AISC and its spot as one of the highest-margin producers sector-wide.

Endeavour Mining - AISC Margins - Company Filings, Author's Chart

{kind=link}

Given the solid cost performance across the board despite higher costs from Mana and the benefit of a higher gold price, Endeavour reported revenue of $524.1 million in Q2 and operating cash flow of ~$160 million. This helped the company to finish the quarter with less than $200 million in net debt (~$840 million in cash) despite elevated growth capital spend of ~$104 million in the period, and the company remains on budget and schedule at its key growth projects, with completion in late Q2 and Q3 2024 for Sabodala-Massawa and Lafigue, respectively. And assuming both remain on schedule, we should see Endeavour grow its production profile to 1.22+ million ounces in 2024 and 1.35+ million ounces in 2025, offsetting nearly all of the lost ounces from its recently divested assets.

Recent Developments

As for recent developments, the major news in the quarter was that Endeavour divested its two non-core assets in Burkina Faso (Boungou and Wahgnion), which will lead to lower production this year and next year. The company sold these assets for upwards of $300 million to Lilium Mining in upfront and deferred cash and royalties. The company noted that this is a positive from a security standpoint in Burkina Faso as both mines are close to each other, allowing it to direct its security efforts into a single area of the country. However, the major news in Q2 was the continued exploration success at Tanda-Iguela in eastern Cote d'Ivoire that has prompted to increase its already aggressive exploration budget. In fact, drilling at Tanda-Iguela came in at ~95,000 meters in H1, beating out Hope Bay where Agnico Eagle ( AEM ) is also drilling aggressively (~89,000 meters drilled in H1), and drilling at Tanda-Iguela is expected to total 180,000 meters this year.

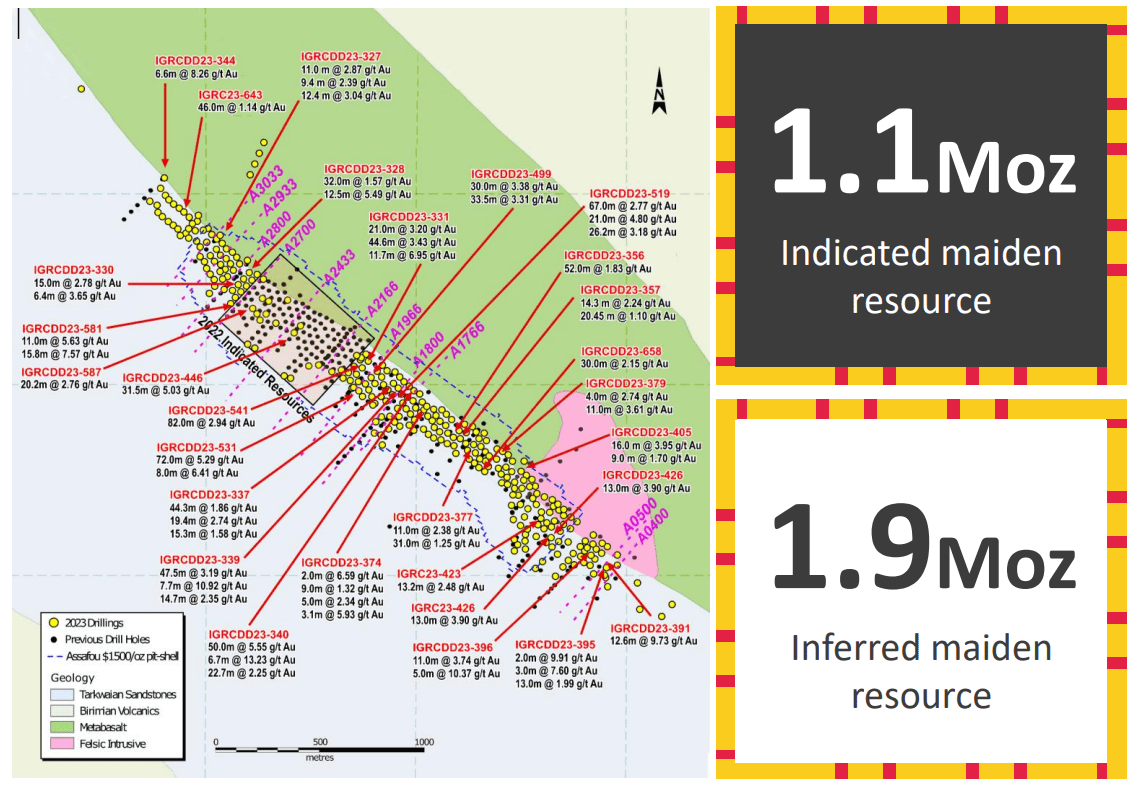

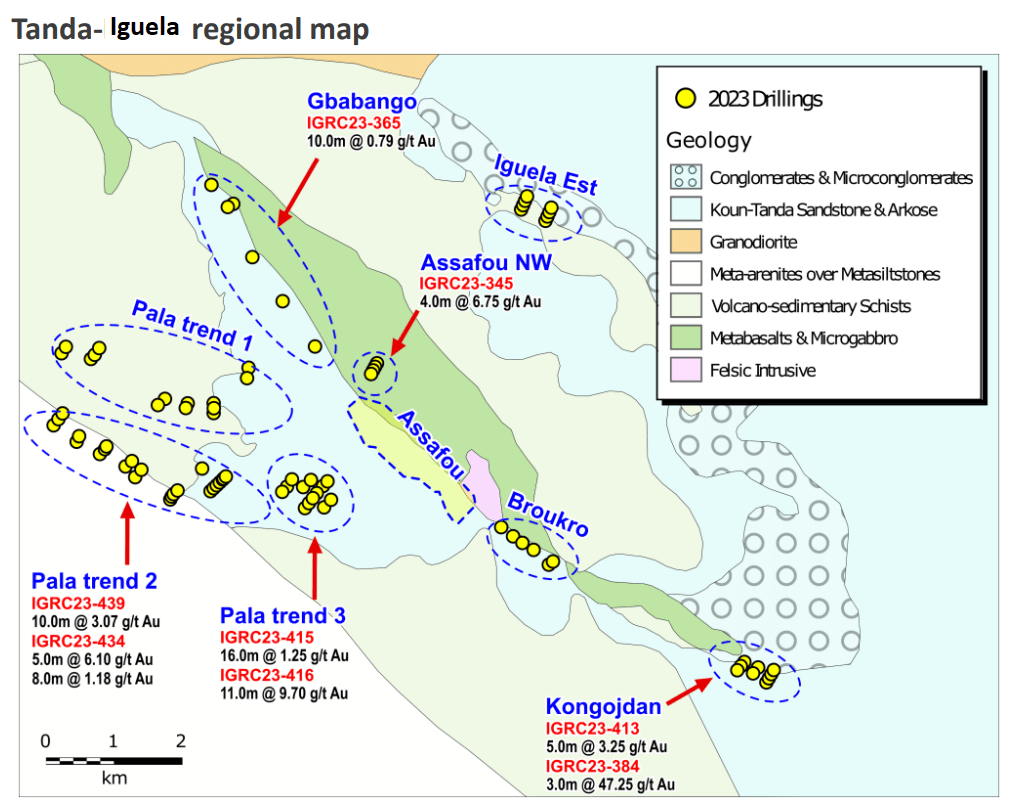

For those unfamiliar, this asset started with 395 square kilometers of land (Tanda permit and northern portion of the Tanda-Iguela Property), which was added to Endeavour's portfolio in late 2015 following the La Mancha transaction. Endeavour added to this asset when it was awarded the Iguela permit (298 square kilometers) in 2017, located south of the Tanda permit. The addition of this second major parcel of land was certainly a smart move by the company given that in just 15 months of drilling, the company released a maiden resource last year of ~3.0 million ounces at 2.0+ grams per tonne of gold, made up of ~14.9 million tonnes at 2.33 grams per tonne of gold (indicated category) and ~1.9 million ounces at ~1.80 grams per tonne of gold (inferred category). Notably, the mineralized system at the Assafou deposit covers just 20% of the 3-kilometer-long mineralized system and is conveniently located near grid power, benefits from 95%+ recovery rates, with average processing recoveries of ~92% for the three material types (oxide, transitional, and fresh ore).

Tanda-Iguela Drill Highlights & Indicated Resource Footprint (Company Website)

{kind=link}

As drilling above highlights, the indicated portion of this resource which is higher-grade makes up a small subset of the overall resource base, and not only has drilling at Assafou yielded multiple thick high-grade intercepts like 30.9 at 3.90 grams per tonne of gold, 68.7 meters at 2.22 grams per tonne of gold, 27.4 meters at 5.21 grams per tonne of gold, and 18.0 meters at 13.82 grams per tonne of gold, but there are multiple targets within a close proximity to Assafou that could act as satellite pits. And early drilling at Pala Trend 2 and 3 located 4 kilometers southwest have yielded promising intercepts as well (11.0 meters at 9.7 grams per tonne of gold and 10.03 meters at 3.07 grams per tonne of gold). Meanwhile, at the Kongojdan target to the southeast, we've also seen high grades with an impressive intercept of 3.0 at 47.25 grams per tonne of gold. And as discussed in the Q2 2023 Conference Call:

"Mineralization is already identified over 600 meters along the Northwest strike, and it remains open along strike and at depth. At the Kongojdan target, the structural contact between the Tarkwaian basin rocks and the Birimian basement had been well defined through geophysics. This has confirmed that the prospective structure hosting a Assafou continues over 20 kilometers, extending 4 kilometers to the southeast to the Kongojdan target and 5 kilometers northwest of Assafou towards the Gbabango target."

- Endeavour Mining, Q2 2023 Conference Call

{kind=link}

This is very exciting, with geophysics suggesting that mineralization could continue well past Assafou with the potential for a much larger mineralized system than what's been outlined to date. And what it's certainly premature to discuss economics, I have presented a table below which looks at conceptual production profiles assuming a 92.5% recovery rate and production scenarios from 6.0 to 7.0 million tonnes per annum at varying feed grades, with these throughput rates being justifiable in my view if Endeavour could ultimately prove up a 100.0+ million tonne resource or 70.0+ million tonne reserve base within a 10-kilometer radius of a central mill. As we can see, a 7.0 million tonne per annum throughput rate at grades of 2.3 grams per tonne of gold (bullish case) could support a 450,000+ ounce production profile in the early years with elevated grades, while even lower throughput scenarios at more conservative grades (6.0 million tonnes per annum at 2.0 grams per tonne of gold) would translate to an impressive operation with similar scale to its top-3 assets, Ity, Hounde, and Sabodala-Massawa.

Tanda-Iguela - Conceptual Production Profiles At Different Throughput & Grades - Company Filings, Author's Chart & Estimates

{kind=link}

As noted by Endeavour, we should see an updated resource at Tanda-Iguela by year-end and if this follows a similar course to Lafigue, we could see this asset in production well before the end of the decade. To be clear, I do not expect to see a 100.0+ million tonne resource outlined in the upcoming resource which would be a doubling of the previous resource, but I would not be surprised to see a resource of this size delineated by year-end 2025. And if achieved, this could be Endeavour's next mine with an ultra-low discovery cost, supporting the view that Endeavour does not need M&A to grow its production profile, it just needs its massive portfolio of highly prospective ground, its talent exploration team led by Jono Lawrence (former Exploration Manager at Randgold), and its strong balance sheet, which supports ramping up exploration aggressively when it hooks a potential monster like it has at Tanda-Iguela.

Summary

Endeavour Mining's Q2 results have appeared mediocre on the surface, but the portfolio looks better than ever, it's been optimized to enjoy even higher margins post-2023, and its growth projects are progressing well and on schedule, supported by Endeavour's nearly $1.0 billion in available liquidity. Meanwhile, its exploration success continues to look promising, with underground potential confirmed at Hounde, and a very impressive new discovery being outlined at Tanda-Iguela. Given the company's industry-leading margin profile, attractive valuation (~5.0x FY2024 cash flow per share estimates), and consistent leading returns to shareholders (~$120 million in share repurchases over the past 18 months), I would view any pullbacks below US$20.50 as buying opportunities.

For further details see:

Endeavour Mining: Portfolio Optimization Maintains Industry-Leading Margins