EXK - Endeavour Silver: A Softer Q3 But Finally Some Peso Relief

2023-10-12 05:27:19 ET

Summary

- Endeavour Silver's Q3 production declined by 21% for silver and 1% for gold compared to the previous year.

- And while the company got some relief from a stronger USD/MXN recently, the offset has been a sharp decline in precious metals' prices.

- In this update, we'll dig into the disappointing Q3 report and whether EXK is finally entering a buy zone after what's been a waterfall ~40% decline since July.

Just over six months ago, I wrote on Endeavour Silver (EXK), noting that while it was one of the few names to beat its FY2022 guidance and Terronera being green-lighted was a positive catalyst, there was limited upside in the stock from a share price of US$3.50. This is because it was trading near ~1.20x P/NAV, a difficult multiple to justify given that it's one of the more sensitive miners sector-wide given its razor-thin margins and the USD/MXN had just broken critical support. Since then, the Mexican Peso's strength has continued and the silver price has struggled to hold on to any of its gains, which has sent the stock ~35% lower from a drawdown standpoint. Not only has this represented underperformance vs. the Silver Miners Index (SIL), but it's also meant that any future equity sales under its $60.0 million ATM (if needed) will be less impactful and hurt more from a dilution standpoint, with EXK sitting near multi-year lows. Let's dig into the Q3 results and any recent developments below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Production & Sales

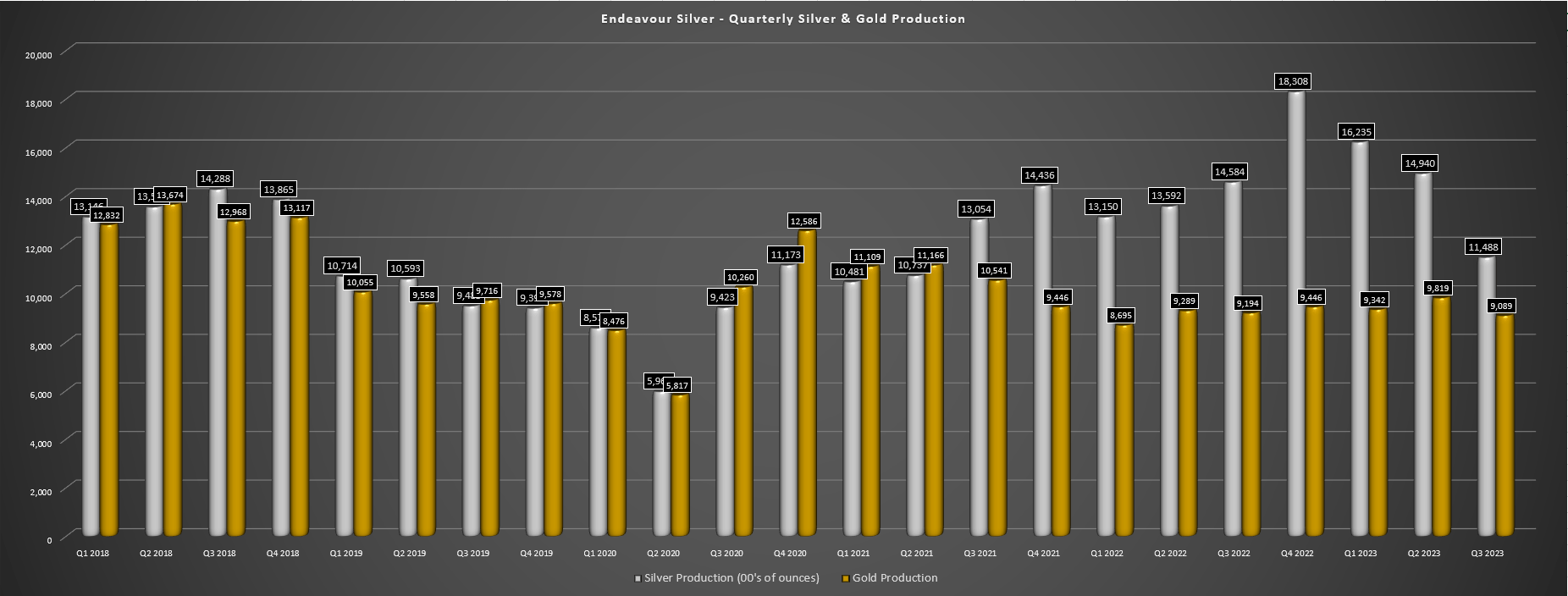

Endeavour Silver released its preliminary Q3 results this week, reporting quarterly production of ~1.15 million ounces of silver and ~9,100 ounces of gold, a 21% and 1% decline from the year-ago period, respectively. Fortunately, the softer Q3 follows a strong H1, so the company is still positioned to deliver into its guidance of 8.6 to 9.5 million silver-equivalent ounces [SEOs] with ~6.53 million SEOs produced year-to-date, and while Guanacevi had a tough quarter, the company has confirmed that it's back on track with a better Q4 on deck. That said, Q3 certainly wasn't the best quarter to see a dip in production, with the Mexican Peso spending most of Q3 at a 5+ year high vs. the United States Dollar ( UUP ), and silver mostly range-bound outside of brief rallies that were immediately sold into near $24.00/oz. The result? A weak Q3 financial report on deck despite easy comparisons year-over-year.

Endeavour Silver - Quarterly Silver/Gold Production - Company Filings, Author's Chart

{kind=link}

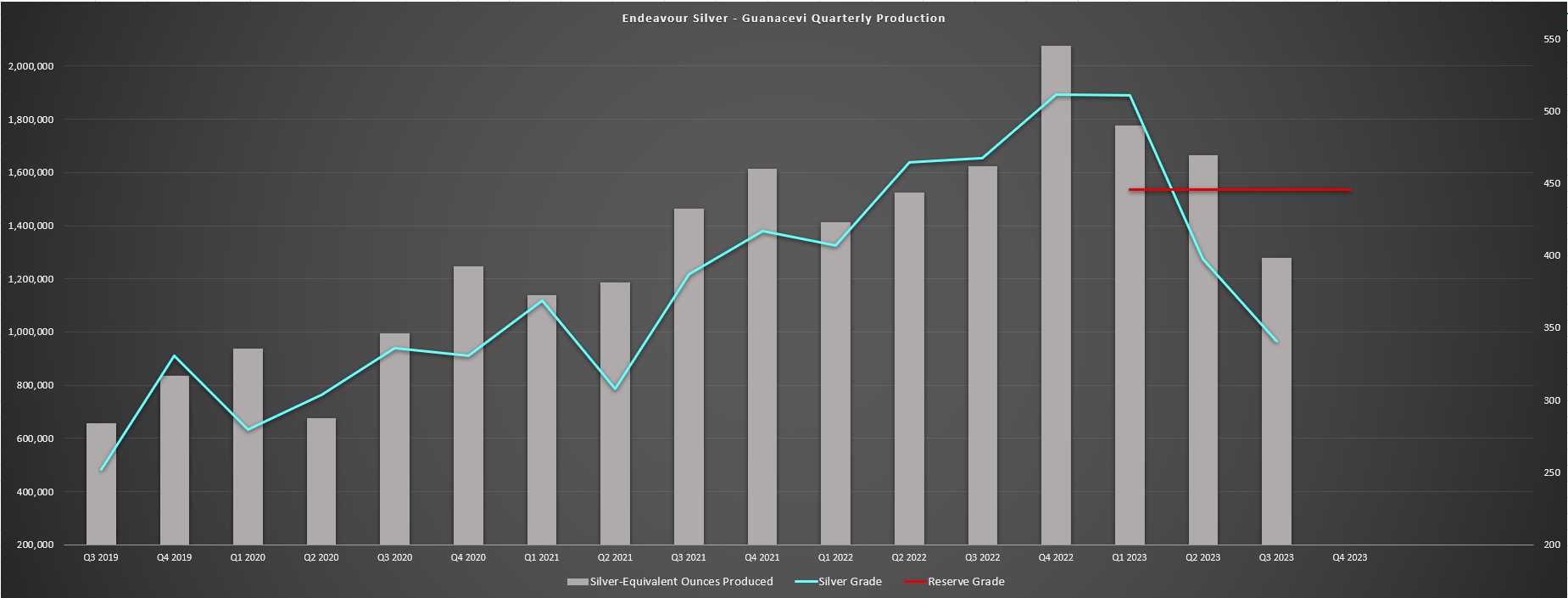

Digging into the results a little closer, we can see that silver production fell for its third consecutive quarter and was down 21% year-over-year to ~1.15 million ounces of silver, while gold production was also down despite a better quarter at Bolanitos for gold grades. As I warned in past updates, the temporary peak silver production in Q4 2022 looked unsustainable given that Guanacevi was benefiting from grades well above its reserve grade (red line below) and some normalization was more than overdue vs. the 500+ gram per tonne grades in Q4 2022/Q1 2023. Unfortunately, this has come to fruition in the past two quarters and while the most recent quarter's softness was related to mine sequencing changes related to access and ventilation, the days of 500+ gram per tonne silver grades look to be numbered.

Guanacevi - Quarterly SEO Production, Silver Grade & Reserve Grade - Company Filings, Author's Chart

{kind=link}

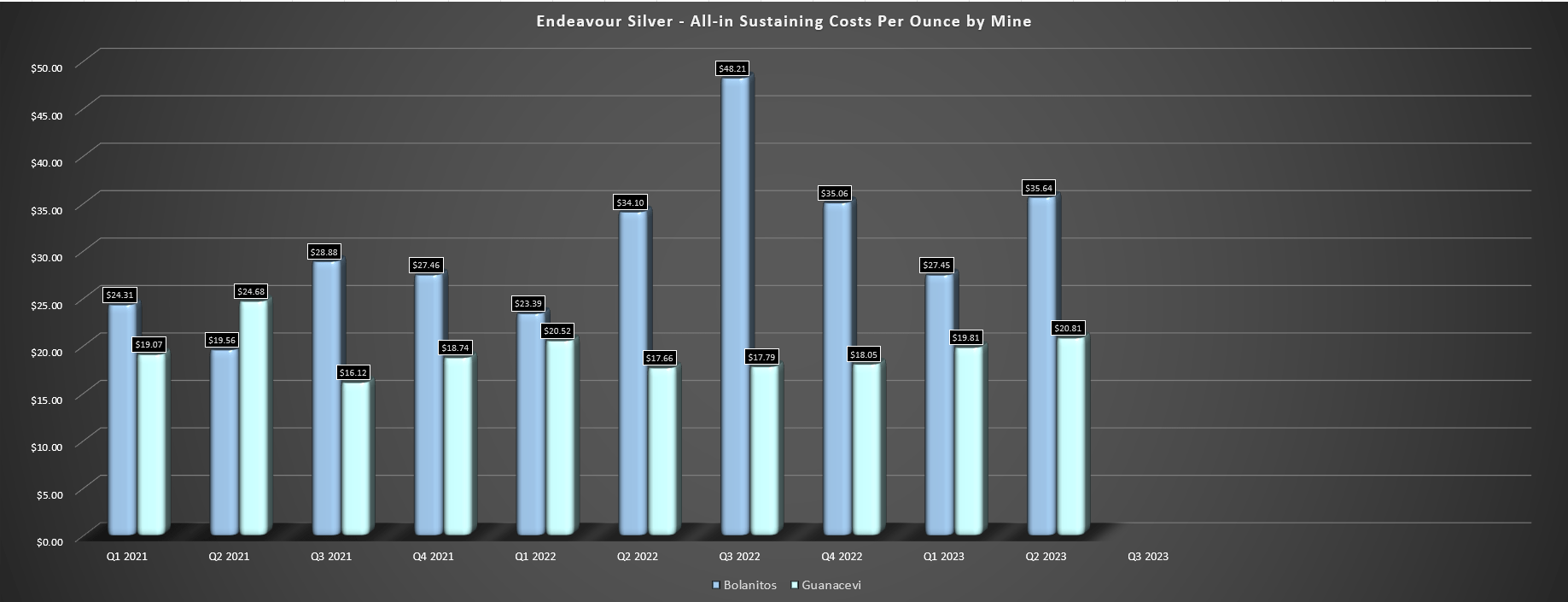

On a positive note, Endeavour shared it expects grades to tick up in Q4 2023 at Guanacevi and that planned maintenance at the plant complete, and that grades will increase in Q4. However, they're increasing from a much lower base in Q3 and without the benefit of 500+ gram per tonne silver grades, it will be more difficult for this operation to keep costs down at the same levels that they were in H2 2022 (sub $18.00/oz AISC). This is especially true when the US Dollar remains ~13% weaker relative to the Peso on a trailing-three-month basis at ~$17.20 compared to a USD/MXN ratio of ~$19.70 in Q4 2022, with this spread being despite the benefit of a relief rally recently in the USD/MXN. And with illegal blockades at other mines like San Jose related to wages and a strike at Penasquito which ended with an 8% pay increase, I would expect pressure on mining wages in Mexico going forward with other mines also looking for increased wages or profit-sharing. Hence, I would think the normal is $19.50/oz plus AISC at Guanacevi.

Guanacevi & Bolanitos Quarterly AISC - Company Filings, Author's Chart

{kind=link}

As for the company's smaller Bolanitos Mine, it was a mediocre quarter, with ~110,900 tonnes processed, a ~5% increase from the year-ago period. However, while gold production was up due to higher grades and throughput (1.89 vs. 1.83 grams per tonne of gold) silver production was sharply lower due to lower grades in the period, sliding ~15% to ~107,500 ounces. This could put further pressure on all-in sustaining costs with lower SEOs in the period, and this mine's costs are already among the highest levels sector-wide, averaging ~$36.60/oz over the past four quarters even with only half of this period affected by the breakout in the significant strength in the Peso. Hence, the combination of a weaker silver price and higher costs has certainly dampened the outlook from a cash flow standpoint in H2, suggesting a higher probability that the company may need to draw on its ATM at some point to ensure it can fully fund Terronera.

{kind=link}

Recent Developments

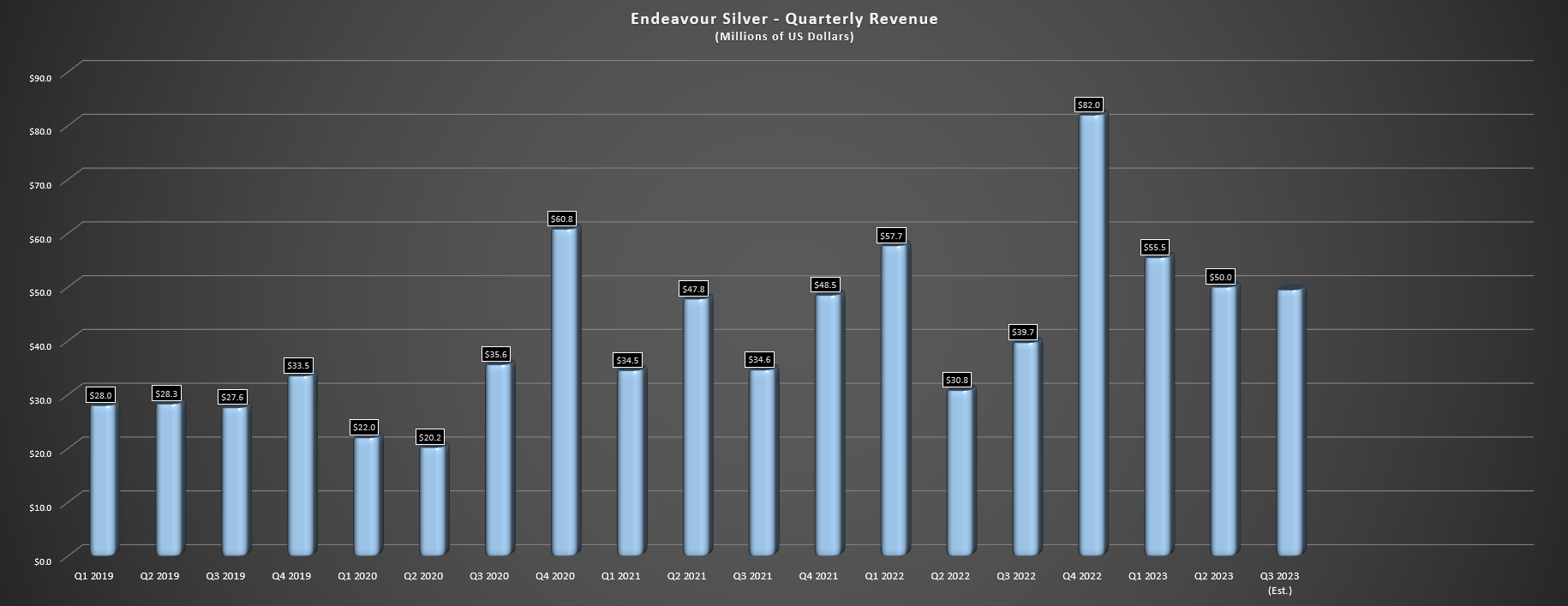

While the recent plunge in silver prices certainly doesn't help for Endeavour Silver hoping to unload some of its inventory from lower sales in the period relative to production, the company has at least got some help from the Peso recently, which has seen a moderate pullback vs. the US Dollar. This could provide some relief in Q4 to partially offset the lower silver price, and with sentiment for the Peso sitting at ~70% bulls on its long-term moving average according to Daily Sentiment Index data, there could be room for a further retracement over the coming months. That said, and as noted below, Endeavour is in an unfavorable position as it's been mining above reserve grades at Guanacevi and may struggle to replicate these grades (~490 grams per tonne trailing-twelve-month average as of Q1 2023) going forward. So, even if the company gets help short term from a softening Peso, it's going to need some help from the silver price if it hopes to generate any meaningful free cash flow at Guanacevi.

Endeavour Silver - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Moving over to its development project, there is fortunately a light at the end of the tunnel from a margin standpoint, with Endeavour Silver set to transform from a high-cost producer with razor-thin margins to one of the higher-margin producers sector-wide, especially if it takes the high-cost Bolanitos Mine offline. However, while this is a positive development, it's unclear whether the company will be able to bring Terronera into production without further share dilution, and while the gains from a production standpoint will be significant, they'll be much less meaningful considering the 60%+ share dilution since 2016.

{kind=link}

As I've noted in past updates, I am looking for miners that have are growing per share metrics and ideally have high margins to weather any cyclical downturns in metals prices, and have the balance sheet to support buybacks opportunistically vs. equity in the weak times like we've seen from other silver names like Coeur (CDE), First Majestic (AG), and Avino (ASM). And while EXK is not the serial diluter that Coeur Mining, the consistent dilution will unfortunately offset much of the benefits of Terronera. Plus, while Terronera is a game-changer, given that it's a very impressive asset relative to Guanacevi and Bolanitos and one of the higher-margin silver assets sector-wide (sub $5.00/oz AISC with by-product credits), we're still 18 months from commercial production, so it's possible investors might have to wait a little longer before the market prices in an overdue re-rating (assuming Terronera can deliver on its expectations).

{kind=link}

Valuation

Based on ~196 million fully diluted shares and a share price of US$2.45, Endeavour Silver is finally trading at a more attractive valuation, sitting at a market cap of just ~$480 million, leaving it trading at a rare discount to an estimated net asset value of ~$570 million. This is very reasonable for a silver producer, but it's worth noting that Mexico's investment attractiveness is on the decline following multiple developments (Penasquito strike, illegal blockades at multiple operations, La Colorada armed robbery, mining reforms). Hence, I don't think investors can expect EXK to sustainably trade above 1.50x P/NAV as it has in the past, and while its current valuation of ~0.85x P/NAV may be attractive relative to its historical multiples and richly valued peers like First Majestic, it's not all that cheap relative to what else is out there in the market.

{kind=link}

In fact, there are some Tier-1 jurisdiction precious metals producers trading at less than 0.70x P/NAV and developers like Marathon Gold (MGDPF) trading at less than 0.30x P/NAV using higher discount rates. So, although EXK is cheap and the stock could easily bottom out here, I continue to see more attractive bets elsewhere. That said, given that there is finally a path to more respectable margins and production growth with Terronera over 30% complete, I see the stock as a Speculative Buy below US$2.13.

Summary

Endeavour Silver had a tough Q3 operationally because of lower than expected grades and combined with a stronger Peso, I would expect a relatively weak Q3 from a financial standpoint. Worse, the company is getting no help from the silver price, which doesn't help its near-term cash flow outlook, and while it has sufficient liquidity to build Terronera following the closing of its debt facility, it's hard to entirely rule out share dilution between now and commercial production. On a positive, the stock is finally within sight of production at Terronera with solid progress to date, and while there was no way to justify going near the stock above US$4.00 over the past year, the stock has become much more reasonably valued at US$2.45. Hence, if I were looking for silver exposure and didn't mind a 95%+ NAV weighting to Mexico, I would strongly consider EXK from a swing-trading standpoint below US$2.13.

For further details see:

Endeavour Silver: A Softer Q3 But Finally Some Peso Relief