EXK - Endeavour Silver: Another Year Of Successful Reserve Replacement

2023-07-04 00:14:08 ET

Summary

- Endeavour Silver has announced a financing package and construction decision for the Terronera project, and has managed to replace reserves despite inflationary pressures.

- Meanwhile, the company's shares are currently trading at a slight discount to its estimated net asset value of ~$610 million, an improvement from March levels.

- However, while EXK is trading at a more reasonable valuation and has done a satisfactory job maintaining reserves per share, I don't see enough margin of safety yet at US$3.00.

Just over three months ago, I wrote on Endeavour Silver ( EXK ), noting that while the story was improving with Terronera likely to be green-lighted, the stock wasn't offering any margin of safety above US$3.60 per share. Since then, the stock has suffered a ~20% drawdown and underperformed the Silver Miners Index ( SIL ). Fortunately, we have seen some good news since Q1, with Endeavour Silver ("Endeavour") announcing a financing package and construction decision and financing package at Terronera and being one of the few companies to report successful reserve replacement despite another year of significant inflationary pressures. And while we are likely to see further share dilution between now and Terronera's commissioning (late 2024), Endeavour has done a decent job of maintaining reserves per share, and especially relative to some peers like First Majestic ( AG ). Let's take a closer look at its FY2022 Reserve/Resource update below:

{kind=link}

All figures are in United States Dollars unless otherwise noted and most silver-equivalent figures are on a 75/1 basis.

2022 Reserves

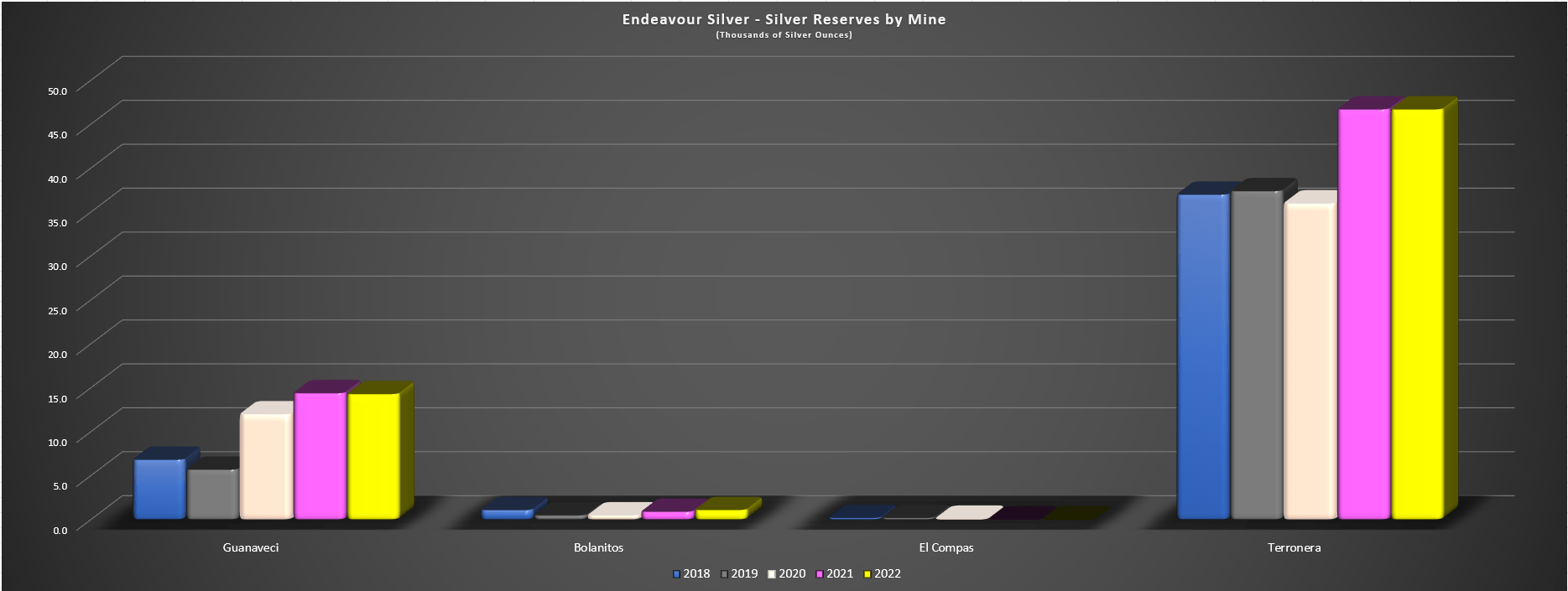

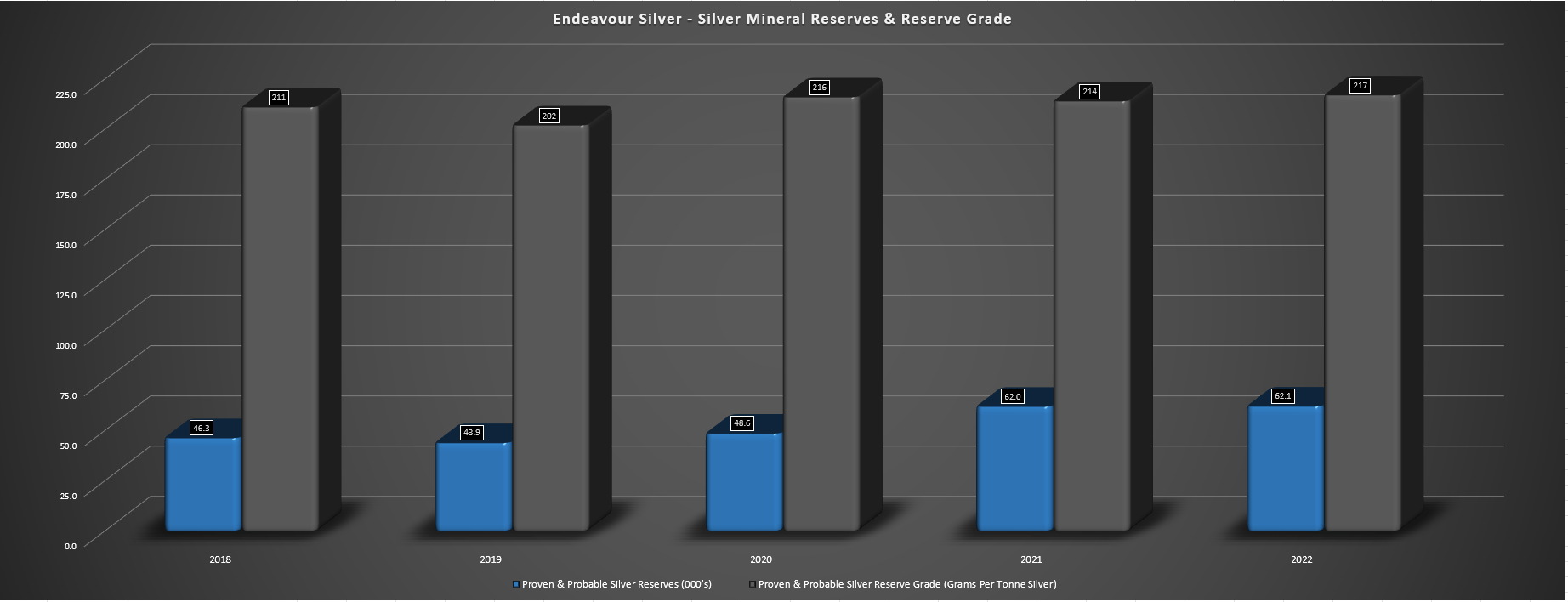

Endeavour Silver reported its FY2022 Reserve/Resource update earlier this year, highlighting its mineral reserve inventory, which is the economically mineable portion of a measured and or indicated mineral resource. The company's mineral reserves at year-end 2022 came in at ~8.9 million tonnes at 217 grams per tonne of silver and 2.14 grams per tonne of gold (~378 grams per tonne silver-equivalent), translating to ~62.1 million ounces of silver and ~612,500 ounces of gold, or ~108 million silver-equivalent ounces [SEOs]. This represented a slight increase from the year-ago period despite the impact of inflationary pressures on cut-off grades, with Guanacevi maintaining a similar reserve base of ~14.3 million ounces of silver and ~38,800 ounces of gold (+2% year-over-year on an SEO basis) while Bolanitos reported a 9% increase on an SEO basis, ending the year with ~1.1 million ounces of silver and ~39,700 ounces of gold.

Endeavour Silver - Silver Reserves by Mine (Company Filings, Author's Chart)

{kind=link}

Looking at the chart above, we can see that this steady growth in reserves at Guanacevi has been achieved despite a significant increase in mining depletion (higher production) which has made reserve replacement more challenging. However, this has been offset by the higher silver price assumption of $23.00/oz used in FY2022, up from $16.50 in FY2020, and while Guanacevi and Bolanitos grew reserves slightly last year, they're still staring down very short mine lives. In fact, assuming a throughput rate of ~400,000 tonnes per annum and the ~1.0 million tonnes of material in the reserve category, Guanacevi's reserve base is sitting at less than three years. And in Bolanitos' case, it isn't in any better shape, with the 520,000 tonne reserve base translating to less than two years of reserves assuming a similar throughput rate.

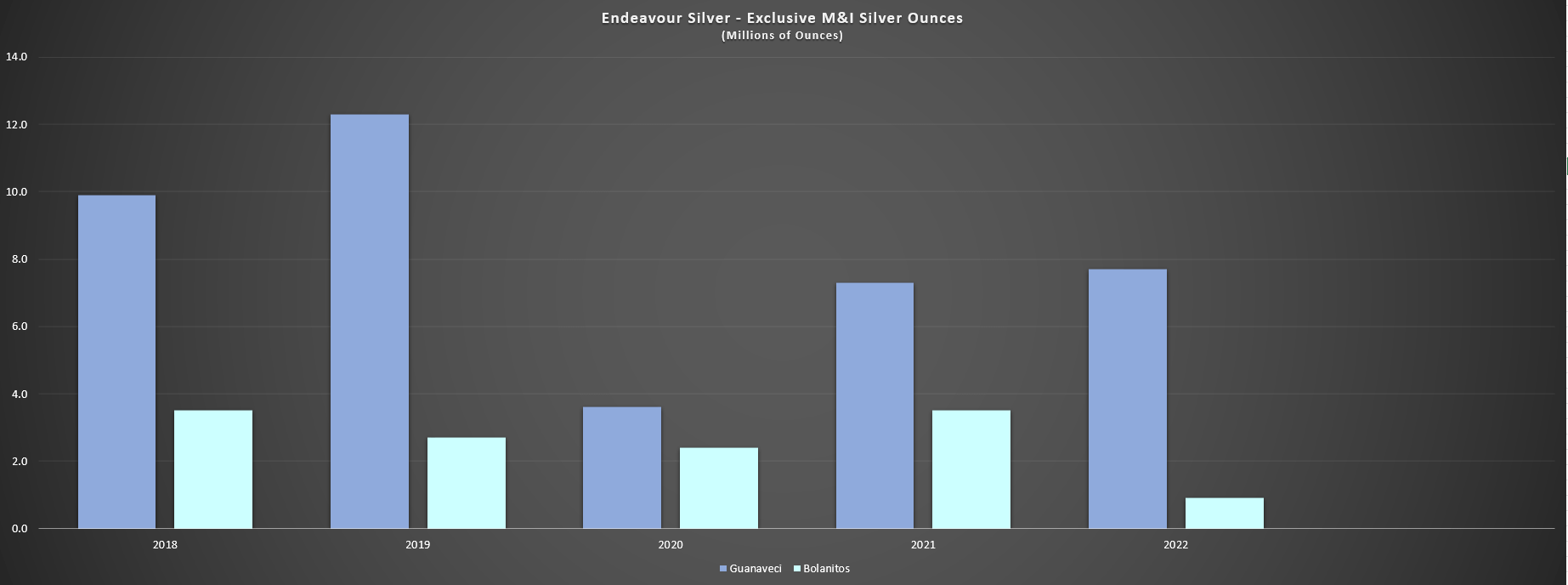

Endeavour Silver - Exclusive M&I Silver Ounces (Company Filings, Author's Chart)

{kind=link}

The silver lining is both assets have a decent amount of inventory in the measured & indicated category to back up their reserves. This means that while their mine lives based solely on reserves may be running low, there's reason to be optimistic about some mine life extension with another ~440,000 tonnes of material separate from reserves at Bolanitos and ~610,000 ounces at Guanacevi. The only issue is that the grades on these resources at Guanacevi are lower, and between continued inflationary pressures (power, steel, cyanide), and a stronger Mexican Peso which is affecting labor costs, we could see a further increase in cut-off grades year-over-year. Plus, with the company's reserve price used to calculate reserves sitting at spot prices ($23.00/oz) for its two operating assets, the company won't be able to lean on higher prices to help with resource conversion this year unless we see materially higher silver prices over the next six months.

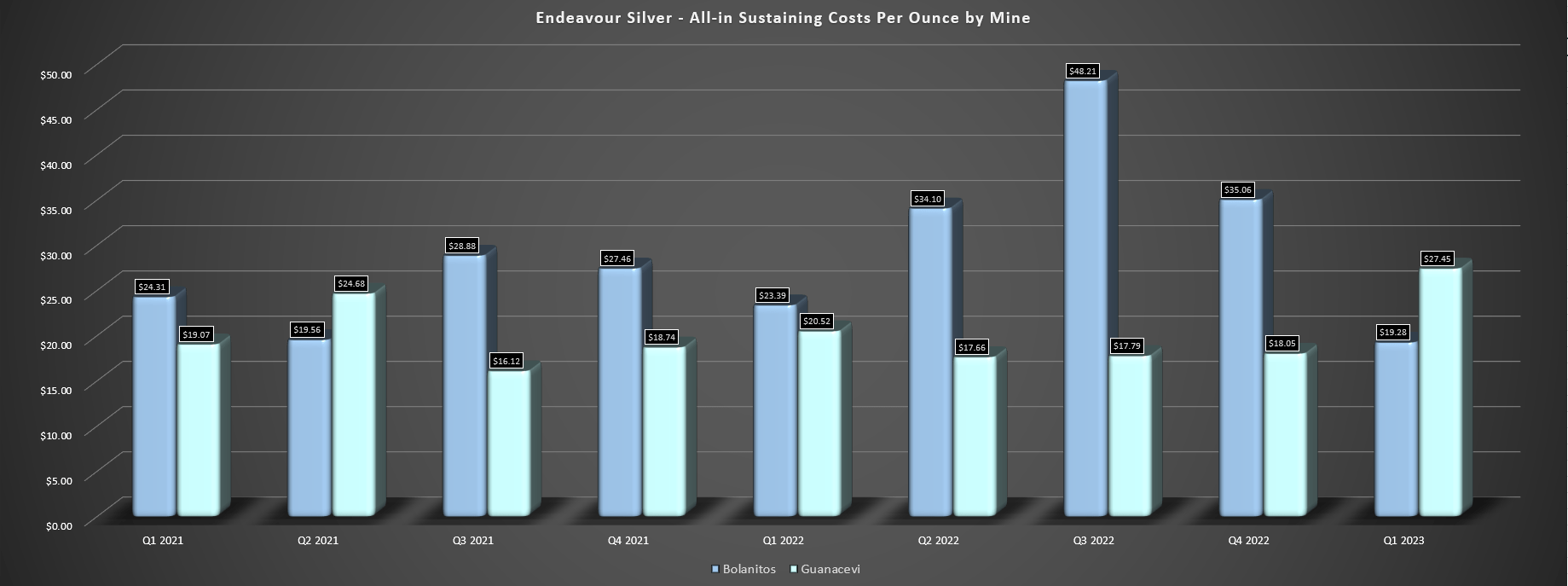

Normally, this would be a very negative development with sub 3-year mine lives based on reserves at two assets, and one reason to avoid a precious metals stock entirely. However, as the chart below shows, it wouldn't be the end of the world to see Bolanitos moved into care & maintenance when all-in sustaining costs [AISC] have consistently come in above $19.00/oz (trailing-two-year average AISC of ~$29.00/oz even before the impact of a stronger Mexican Peso felt in Q2 2023. Plus, the company has a phenomenal asset in Terronera (60% silver/40% gold reserve mix), which not only offers scale (~4.0 million ounces of silver) with a 10-year mine life at the proposed higher throughput rate, but also industry-leading margins, with AISC expected to come in below $4.00/oz even adjusting for inflationary pressures net of by-product credits.

Endeavour Silver - All-in Sustaining Costs Per Ounce By Mine (Company Filings, Author's Chart)

{kind=link}

As it stands, Terronera makes up ~75% of Endeavour Silver's silver reserve base, and it's one of the better undeveloped silver projects globally, with bottom-quartile mine-site projected all-in sustaining costs. Therefore, with this project now approved, financed and already in construction, the dwindling reserve base at its other two assets is less of an issue for the company. And it might make sense for Endeavour Silver to focus on its higher margin projects/mines (Guanacevi/Terronera) like Endeavour Mining ( OTCQX:EDVMF ) has in Africa, with its divest its weaker asset strategy helping the stock to re-rate vs. peers while others that have focused on a per ounce production figure vs. quality ounces have lagged, like Equinox Gold ( EQX ). Now that we've established that Terronera offsets the company's short reserve lives which would otherwise be a red flag for investment, let's look at Endeavour's reserve growth per share.

Endeavour Silver - Silver Mineral Reserves & Silver Reserve Grade (Company Filings, Author's Chart)

{kind=link}

Reserves Per Share

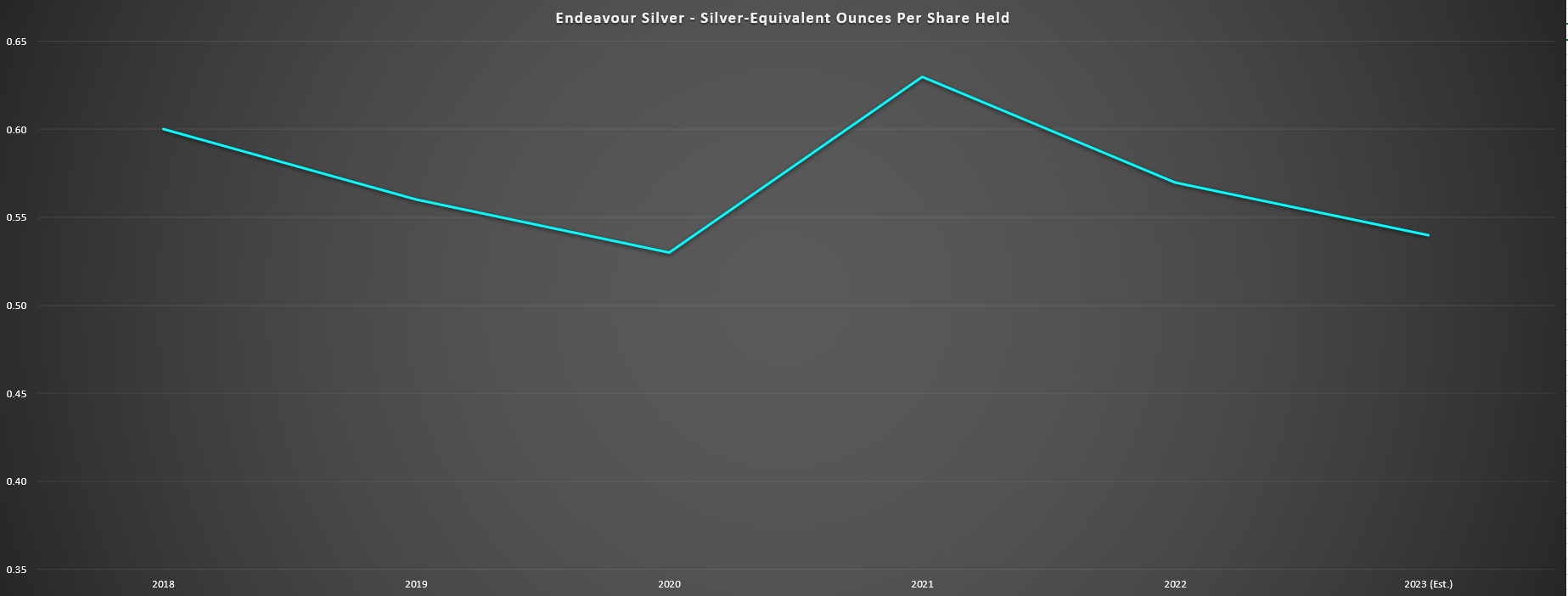

As discussed in past updates, reserve growth is important, but far more important is reserve growth per share . This is because reserve growth that comes at the expense of significant share dilution means that investors are getting exposure to fewer ounces of gold per share held and the result is one is actually seeing their exposure to precious metals diluted by owning a given producer. The result is that an investor is not getting their desired leverage to the silver and or gold price if reserves and or production per share are declining. Obviously, this isn't ideal, since it makes little sense to own a more volatile and riskier producer of a commodity (vs. the metal itself) if it is not offering the leverage that one should get for taking on this added risk.

Some examples of companies that have consistently failed to deliver reserve growth per share are Coeur Mining ( CDE ), Americas Gold and Silver ( USAS ), and McEwen Mining ( MUX ), which is why I continue to see these names as avoidable and uninvestable.

Endeavour Silver - Silver-Equivalent Ounces Per Share Held (Company Filings, Author's Chart & Forward Estimates)

{kind=link}

Fortunately, for Endeavour Silver, the company actually has one of the better reserve per share metrics over the past five years despite consistent share dilution, evidenced by its share count growing by ~45% to ~190 million shares last year vs. ~131 million shares at year-end 2018. However, unlike other precious metals producers that have grown their reserves per share without leaning on less conservative metals prices to calculate reserves like Agnico Eagle ( AEM ), Endeavour Silver has continued to raise its reserve price assumptions, with reserves at Bolanitos calculated at a $23.00/oz silver price and $1,725/oz gold price, well above the industry average. That said, the company has certainly done a better job than some of its peers, and while there's no guarantee that its pipeline projects will head into production, it's also built up its resource inventory with the acquisition of Pitarilla.

Overall, I wouldn't call Endeavour's slight decline in silver-equivalent reserves per share since 2018 anything to write home about, and with a $60 million At-The-Market equity program in place, I would not be shocked to see further reserve per share declines on deck between now and 2025. That said, there are far worse offenders regarding their ability to maintain and grow reserves per share elsewhere in the sector, with examples of serial diluters in the silver space being Americas Gold & Silver and Coeur Mining. So, while I am not overly optimistic on reserve growth in 2023, with continued inflationary pressures and a stronger Peso that could lead to even higher cut-off grades at Bolanitos and Guanacevi, the company has outperformed its peers from a reserve growth per share standpoint, even if this is due to the bar being set quite low.

Valuation

Based on ~197 million fully diluted shares and a share price of US$3.00, Endeavour Silver trades at a market cap of ~$590 million. This has left Endeavour Silver trading at a slight discount to its estimated net asset value of ~$610 million, a significant deviation relative to other names sector-wide that trade at large premiums to net asset value like Guanajuato ( OTCQX:GSVRF ), First Majestic Silver ( AG ), and Hecla Mining ( HL ). However, while this is certainly an improvement from when I warned against paying up the stock while it traded at over 1.30x P/NAV last year, I still don't see Endeavour Silver as offering any real margin of safety, given that it trades at ~8.5x three-year forward (FY2025) free cash flow estimates of ~$70 million. To put this in comparison, Pan American Silver ( PAAS ) trades at barely 0.75x P/NAV and just ~11x FY2024 free cash flow estimates with a far more diversified portfolio with significantly less exposure to Mexico (~20% of NAV).

This less attractive relative valuation doesn't mean that EXK can't rebound from current levels, but when buying precious metals names, I am looking for a significant discount to fair value to justify starting new positions. And even if we value Endeavour at 1.30x P/NAV, this would translate to a fair value closer to US$4.10, translating to just a 27% discount to fair value. Given that I am looking for a minimum 35% discount to fair value for small-cap names and especially those with all of their operations in Tier-2 jurisdictions, I would need a deeper pullback to get interested in EXK, with the ideal buy zone coming in at US$2.70 or lower. In summary, while EXK could enjoy an oversold bounce after its recent 30% correction, I think there are far more attractive bets elsewhere in the sector.

{kind=link}

As shown above, EXK currently trades at ~8.1x FY2024 cash flow per share estimates ($0.37) vs. a historical cash flow multiple of ~13.5, but using what I would argue to be a more conservative cash flow multiple of 9.0 given that it's a small-scale Tier-2 producer, I don't see enough margin of safety here from a P/CF standpoint either.

Summary

Endeavour Silver has one of the better records of maintaining its silver-equivalent ounce reserves per share over the past five years and certainly beats First Majestic Silver ( AG ) whose Jerritt Canyon acquisition led to significant share dilution with minimal to show for it from a reserve growth standpoint. Meanwhile, Endeavour's Terronera Project will transform the company once it heads into commercial production by Q2 2025. That said, I am looking for a material discount to fair value to justify starting new positions in small-cap cyclical names and although EXK has become more reasonably valued after its sharp correction, I still see far better bets elsewhere in the sector. So, while I would consider the stock from a swing-trading standpoint below US$2.70, I don't see a low-risk buying opportunity in the stock just yet.

For further details see:

Endeavour Silver: Another Year Of Successful Reserve Replacement