EXK - Endeavour Silver: Further Weakness Should Present A Buying Opportunity

2024-01-12 17:34:44 ET

Summary

- Endeavour Silver's FY2023 production came in slightly below its guidance mid-point, doing little to help what's been a brutal bear market in the stock.

- Unfortunately, the company's outlook for 2024 implies lower production and similar costs, with another year of razor-thin margins on deck.

- On a positive note, we appear to be seeing some signs of capitulation as some investors throw in the towel judging by relentless selling pressure.

- In this update we'll dig into the Q4/FY2023 results, the FY2024 outlook, and whether the stock is nearing a low-risk buy zone yet.

Just over two months ago, I warned on Endeavour Silver Corp. ( EXK ), noting that while the stock had already suffered a 30% correction from its July highs, there wasn't any margin of safety in the stock just yet, suggesting patience was the best course of action. This was because the company had benefited from above-average mined grades over the past year at Guanacevi which led to better margins, but was now working against a stronger Mexican Peso (operating costs/Terronera development costs), and this translated to a risk of higher than planned share dilution. Since then, EXK has seen continued underperformance with a ~20% drawdown, and its recent 2023 production results didn't help with gold/silver production coming in slightly below the mid-point for the year.

On a positive note, we appear to be seeing some signs of capitulation as some investors throw in the towel, and the company is now one year closer to production at Terronera. That said, the 2024 outlook leaves a lot to be desired with lower production implied by the midpoint and costs well above the industry average yet again. In addition, the company isn't getting any help from the Peso to start the year, with the MXN/USD continuing to hover near multi-year highs. In this update we'll dig into the Q4/FY2023 results, the FY2024 outlook, and whether the stock is nearing a low-risk buy zone yet.

Q4 Production & Sales

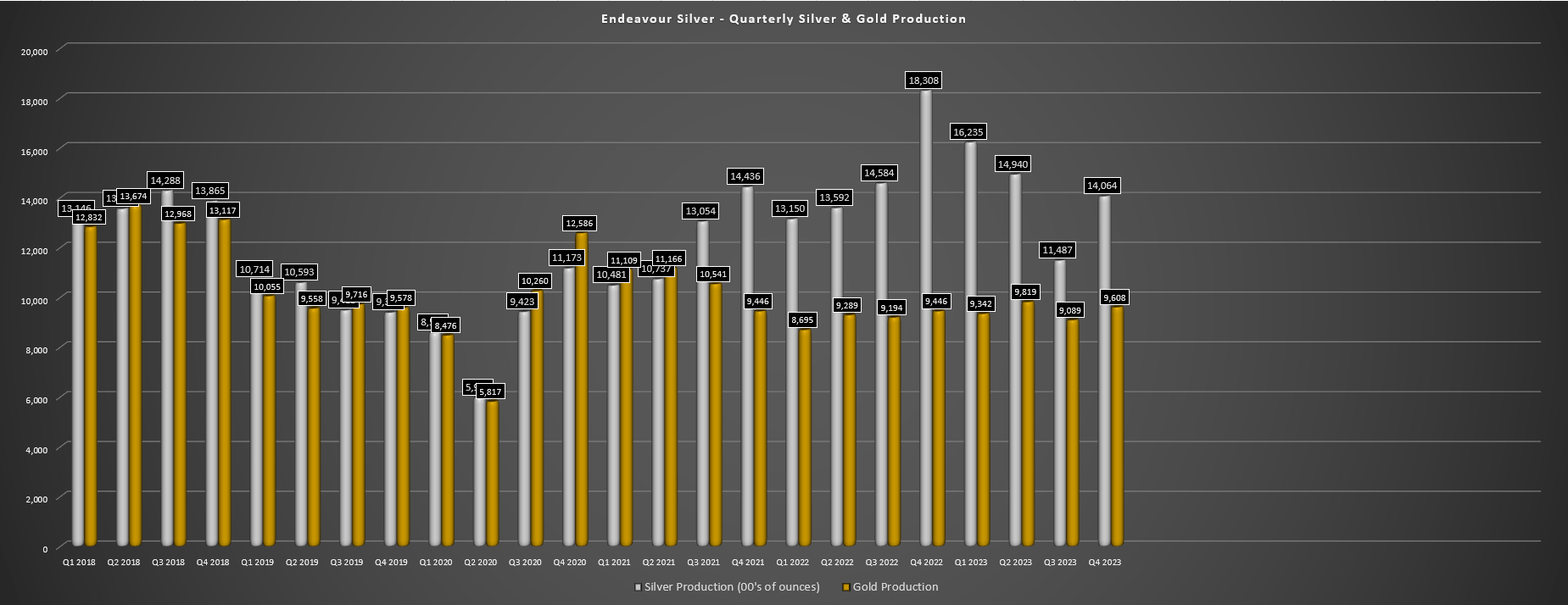

Endeavour Silver released its Q4 production results earlier this month, reporting quarterly production of ~1.41 million ounces of silver and ~9,600 ounces of gold, a significant decline year-over-year vs. production of ~1.83 million ounces of silver in the year-ago period. Unfortunately, this mediocre finish to 2023 resulted in both silver and gold production coming in below their respective guidance midpoints of 6.0 million ounces and 38,000 ounces, with production of ~5.67 million ounces of silver and ~37,900 ounces of gold in FY2023. Worse, this was a significant decline vs. FY2022 levels, with lower grades and recoveries (87.7% vs. 91.5%) more than offsetting the higher throughput in the period.

Endeavour Silver Quarterly Metals Production - Company Filings, Author's Chart

{kind=link}

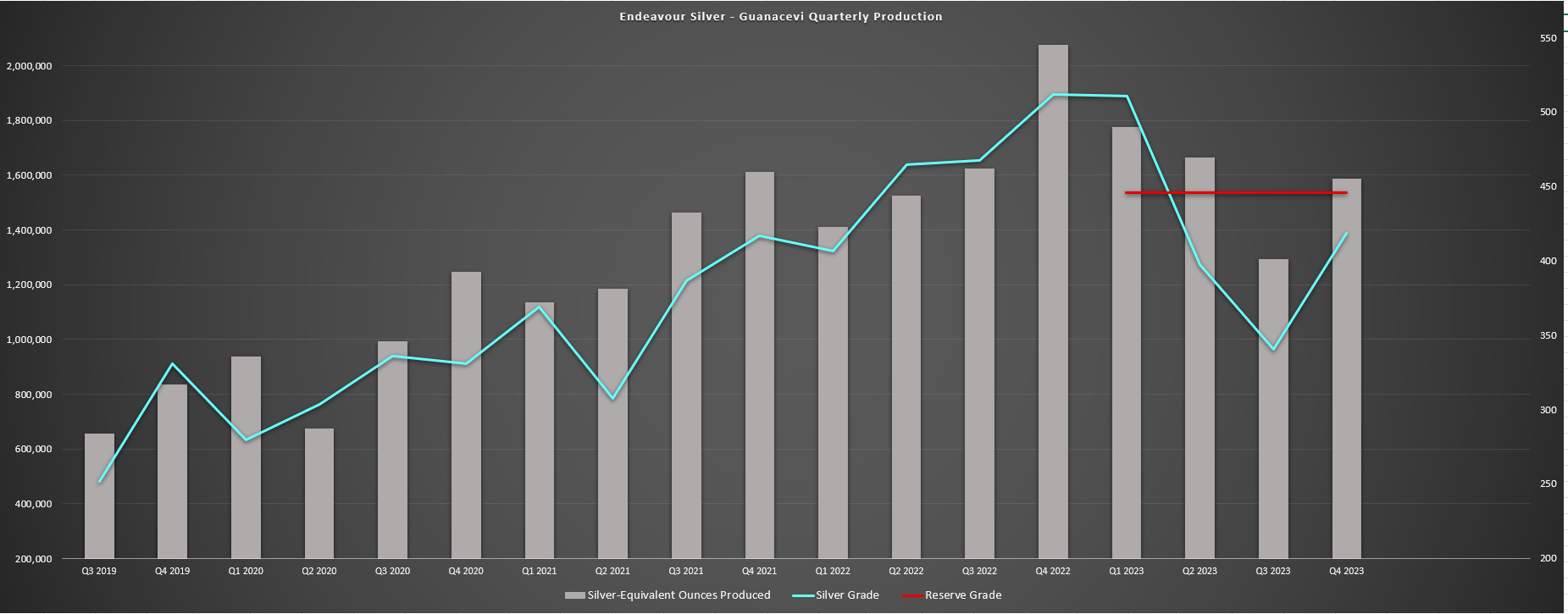

Digging into the operations a little closer, the company's larger Guanacevi Mine produced ~1.27 million ounces of silver and ~3,700 ounces of gold in Q4, a ~25% decline from the year-ago period. In fairness, the company was lapping some tough comps with an average head grade of 512 grams per tonne of silver in Q4 2022, meaning that a dip in production was to be expected given that H2-2022 grades were running over 9% above the average reserve grade at Guanacevi, averaging ~490 grams per tonne. And while annual production did decline over 4% to ~5.1 million ounces of silver, Endeavour reaffirmed the improved performance following a tough Q2/Q3, with grades and throughput above plan in the quarter, and throughput expected to average 1,200 tonnes per day this year (a 1% increase from 2023 levels).

Guanacevi Mine Quarterly Production & Average Reserve Grade - Company Filings, Author's Chart

{kind=link}

As for the company's Bolanitos Mine, there wasn't much to write home about, with this continuing to be a relatively small and high-cost asset, with annual production of ~570,000 ounces of silver at ~$30.00/oz all-in sustaining costs [AISC]. This figure was down from FY2022 production of ~620,000 ounces because of lower silver grades and recoveries, with a slight offset from higher gold production in the period. Unfortunately, AISC has remained miles above the company's average realized silver price despite the benefit of higher by-product credits with increased gold sales and a higher gold price, and the outlook for 2024 isn't much better, with little hope for Endeavour to generate mine site free cash flow here unless silver spends most of 2024 above $30.00/oz.

Endeavour Silver Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

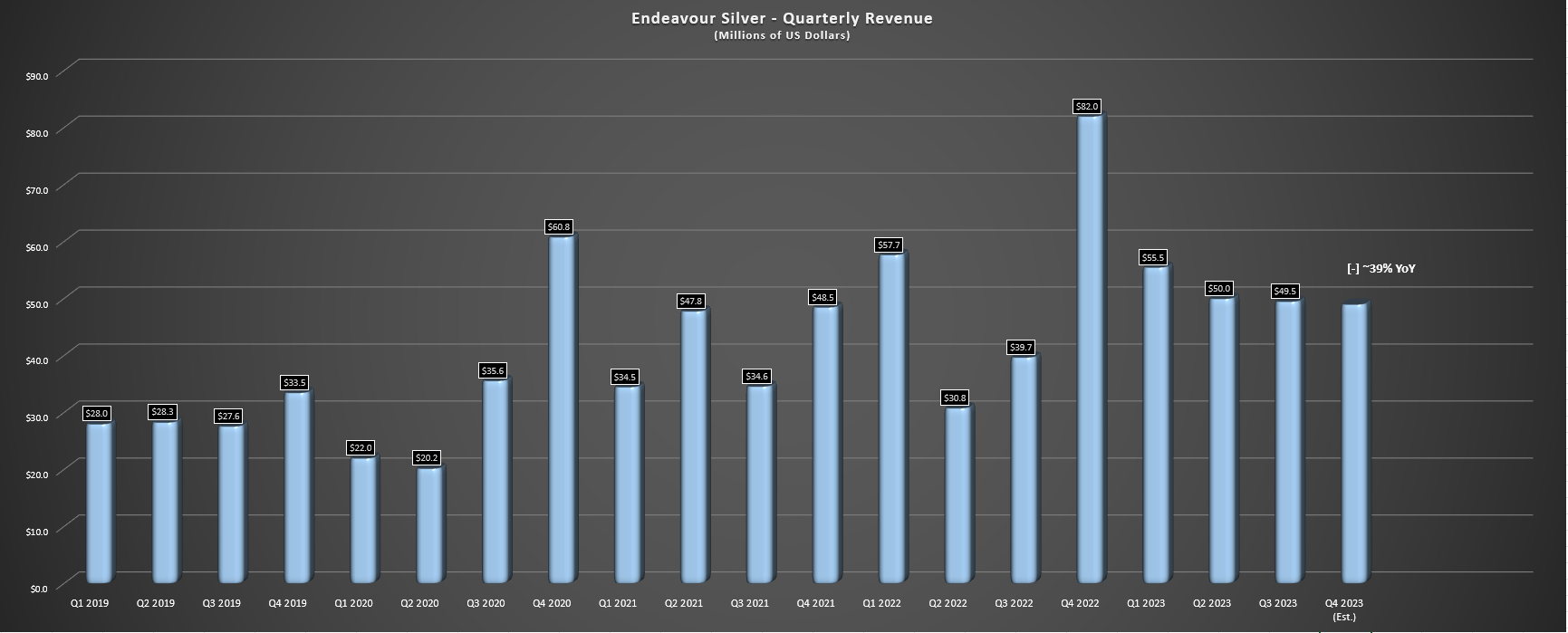

Finally, looking at sales, Endeavour noted it sold ~1.33 million ounces of silver and ~9,400 ounces of gold in the quarter, holding inventory of ~500,000 ounces of silver. This should translate to a significant decline in revenue compared to $82.0 million in Q4 2022, with revenue likely to come in closer to ~$49.0 million depending on its average sales price for both metals. On a positive note, the company has easier comparisons on deck in Q1 as it laps revenue of $57.7 million, and this will be the last quarter of tough comparisons for Guanacevi as Endeavour laps a ~1.8 million SEO quarter in Q1 2024 (Q1 2023 Guanacevi production: ~1.78 million SEOs), setting up a better Q2-Q4 2024 period from a sales standpoint assuming metals prices can cooperate.

FY2024 Outlook & Recent Developments

Moving over to the 2024 outlook, Endeavour has guided for production of 5.55 million ounces of silver and 36,000 ounces of gold at the mid-point, implying moderate declines in output on a year-over-year basis. This is related to lower mined grades at Guanacevi, which was to be expected after a period of extremely elevated grades, while lower gold grades will partially offset higher silver grades at Bolanitos. However, the cost outlook is far worse than 2023 ($19.00/oz to $20.00/oz AISC guidance after gold by-product credits), with Endeavour guiding for FY2024 AISC of $22.50/oz at the mid-point, suggesting another year of razor-thin margins despite lower sustaining capital in the period. The company stated the following:

"The influence of a stronger local currency, coupled with inflationary pressures on essential inputs like labor, explosives, energy, and steel prices, continue to impact the bottom line. While we pursue opportunities to mitigate cost pressures in all areas, maintaining and enhancing safety at our operations will always be our focus."

- Endeavour Silver CEO, Dan Dickson

Not surprisingly, the Mexican Peso continues to take a toll on costs with a double-digit gain vs. the US Dollar ( UUP ) last year, and several companies continue to discuss inflationary pressures as a headwind even if the rate of change has moderated from 2022 levels. This is not as much of an issue for companies like K92 Mining Inc. ( KNTNF ) that will benefit from lower operating costs per tonne as they triple throughput at their Kainantu Mine with all-in sustaining costs below $900/oz (three-year average). However, for Endeavour Silver, its operations are extremely sensitive to metals prices due to its high costs, meaning that investors can expect more ugly financial results until the silver price improves and while we await the company's new higher-margin mine starting commercial production by May of next year.

{kind=link}

Finally, while investors can breathe a sigh of relief that most of the share dilution is in the rear-view mirror, the company recently announced an At-The-Market Offering of up to $60 million, on top of ~7 million shares (3%+ share dilution) that were sold subsequent to the end of Q3 at multi-year lows (US$2.44). Hence, while Endeavour Silver's production was down year-over-year, production per share took a more significant beating with EXK's fully diluted share count rising over 12% year-over-year, resulting in a 15% decline in production per share. While some investors might argue that this decline in per share metrics will be solved post-2024 with Terronera online, we could see up to 230 million fully diluted shares by the time Terronera is in commercial production (~60% share dilution since 2019), meaning that any production growth achieved from Terronera has essentially been offset by share dilution to bring this asset into production, resulting in little benefit for shareholders that have stayed the course in the period.

Endeavour Silver Annual Share Count - Company Filings

{kind=link}

Let's take a look at the valuation below and see whether EXK is offering enough of a margin of safety at current levels:

Valuation

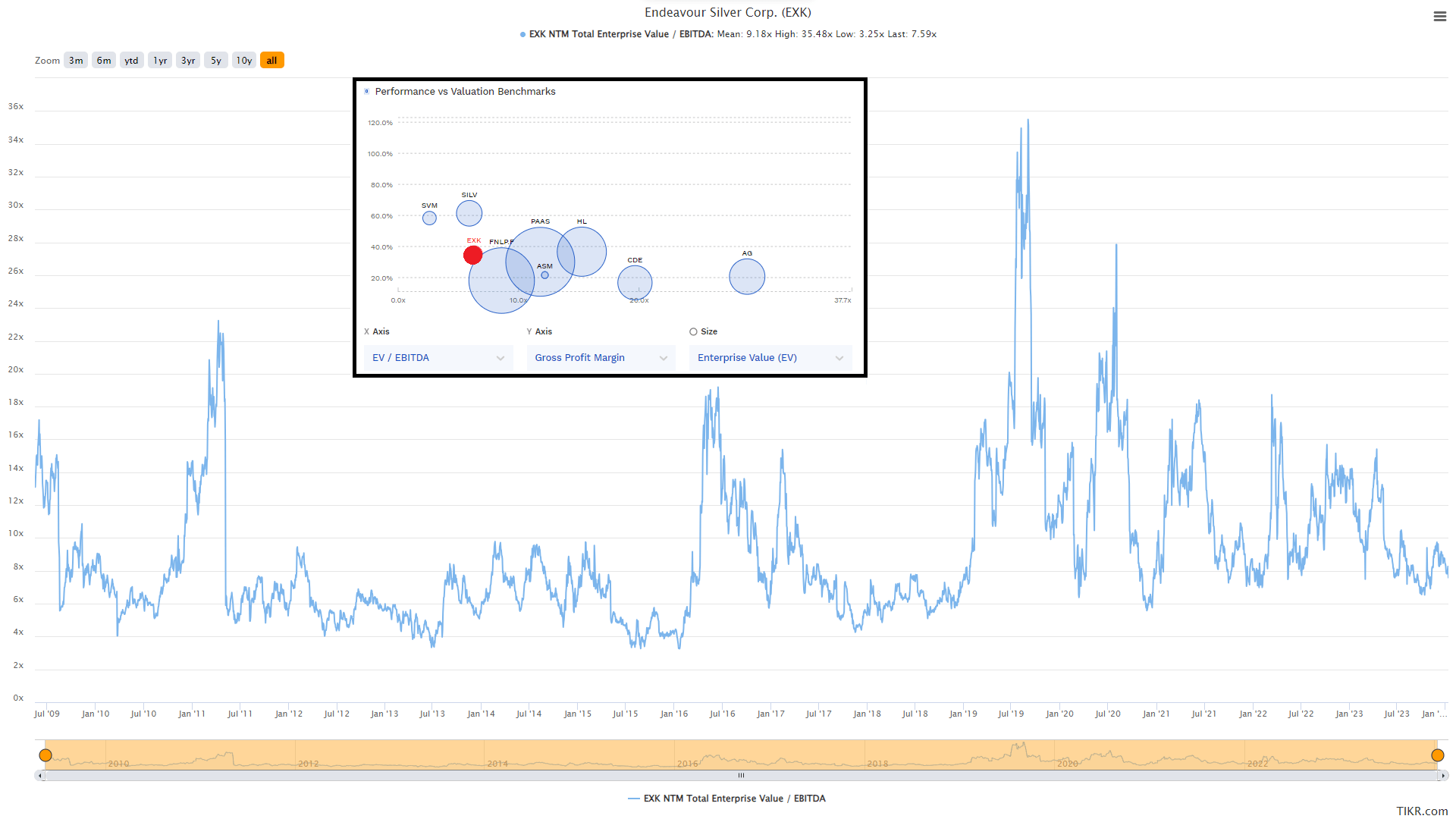

Based on ~220 million fully diluted shares and a share price of US$1.84, Endeavour trades at a market cap of ~$405 million, which leaves it trading at a steep discount to its estimated net asset value of ~$540 million. However, while this is one of the largest discounts to net asset value in years (0.75x P/NAV), some of this can be attributed to the declining investment attractiveness for Mexico, above-average share dilution, and multiple compression we've seen sector-wide because of persistent negative sentiment. Hence, while EXK is undoubtedly getting cheap, it is one name that is cheap for a reason and could continue to underperform with razor-thin AISC margins and further risk of share dilution until Terronera moves into commercial production by May 2025.

Endeavour Silver Valuation/Margins vs. Peers & Historical EV/EBITDA Multiple - FinBox, TIKR

{kind=link}

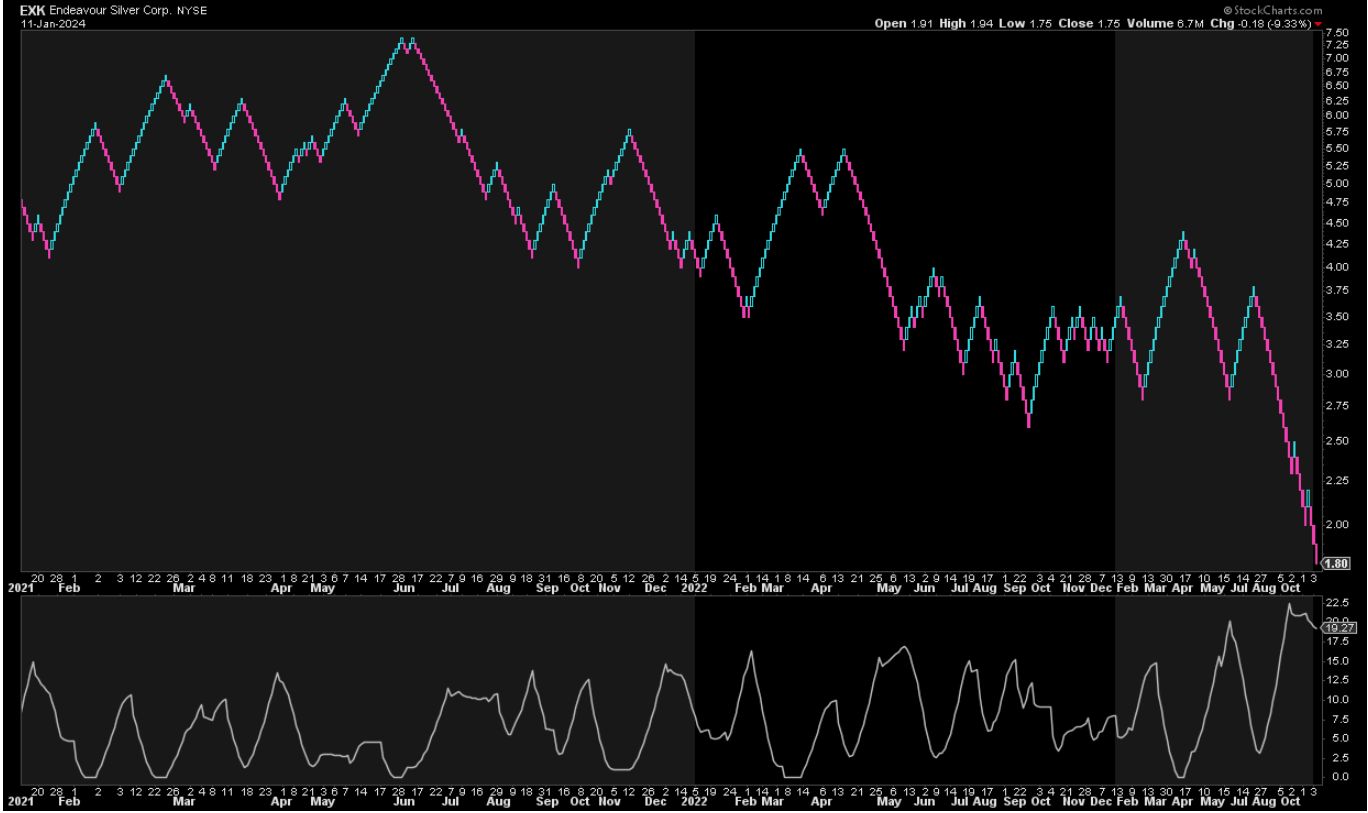

That said, there is reason to believe that the selling in EXK is close to being exhausted after a brutal 75% correction over the past two years. Meanwhile, sentiment is the worst I've seen it in this stock in several years, and that's despite the fact that Endeavour is on the event of a transformation that will lead to a material improvement in margins in H2-2025 (commercial production at Terronera). Hence, if I were a patient investor interested in a more speculative bet, Endeavour is getting interesting at current levels, with its low-risk buy zone coming in at US$1.67 or lower. This low-risk buy zone is based on an estimated fair value of US$2.75, and a required 40% discount to fair value to justify starting new positions in small-cap producers.

EXK 3-Year Chart - StockCharts.com

{kind=link}

So, why I am still on the sidelines?

While Endeavour Silver may be attractively valued relative to other Mexican producers like First Majestic Silver Corp. ( AG ) and on an absolute basis, I prefer to invest from a relative value standpoint and find the most attractively valued names across all sectors to build my portfolio. And if we look out across the precious metals sector, I continue to see far better values in the gold space, like Argonaut Gold Inc. ( ARNGF ) trading for less than 0.40x P/NAV with its largest assets in Tier-1 ranked jurisdictions (Ontario, Nevada). This not only makes Argonaut a more desirable takeover target (already in commercial production in a better jurisdiction with a lower multiple), but suggests it could outperform given that Argonaut will be generating free cash flow this year and not further diluting shareholders and the same can't be said for EXK. Hence, although I may consider EXK from a swing-trading standpoint below US$1.67, I remain focused elsewhere.

Summary

Endeavour Silver had a mediocre year at best in 2023, though the margin pressure was out of its control with a sharp rise in the Mexican Peso and silver struggling to spend any meaningful time above the $25.00/oz level. The good news is that the company only has one more quarter of difficult comps on deck (Q1 2024 vs. Q1 2023), is benefiting from a strong gold price, and has guided more conservatively on costs for 2024. In addition, the company is less than 18 months from a transformation as it brings a high-margin silver asset online with a simultaneous lift to production. So, with Terronera closer to the finish line and sentiment the worst it's been in years, I would view any further weakness below US$1.67 as a buying opportunity from a swing-trading standpoint.

For further details see:

Endeavour Silver: Further Weakness Should Present A Buying Opportunity