EXK - Endeavour Silver: Inflationary Pressures Continue To Pressure Margins

2023-05-15 03:24:32 ET

Summary

- Endeavour Silver released its Q1 2023 results last week, reporting quarterly production of ~1.62 million ounces of silver and ~9,300 ounces of gold, a 23% and 7% increase year-over-year, respectively.

- Fortunately, all-in-sustaining costs declined 4% in Q1 to $20.16/oz, but they are tracking above guidance despite what should be catch-up in sustaining capital due to lower spending in Q1.

- The good news is that Terronera construction has finally begun with a $120 million senior secured debt facility, and while capex is higher, it is relatively modest at ~$230 million.

- That said, I still don't see nearly enough margin of safety in EXK, so I continue to favor other opportunities elsewhere in the market.

We're more than halfway through the Q1 Earnings Season for the precious metals sector and one of the most recent companies to report its results was Endeavour Silver ( EXK ) (EDR:CA). While the company's production results were solid and are tracking in line with FY2023 guidance (8.6 - 9.5 million silver-equivalent ounces), costs remain elevated, with razor-thin margins in Q1 despite the recovery in metals prices. And while Terronera will provide a significant reduction in the company's operating costs once in commercial production (2025), we're still two years and it's hard to be optimistic about Bolanitos long-term. Let's dig into the Q1 results below:

Q1 Production & Sales

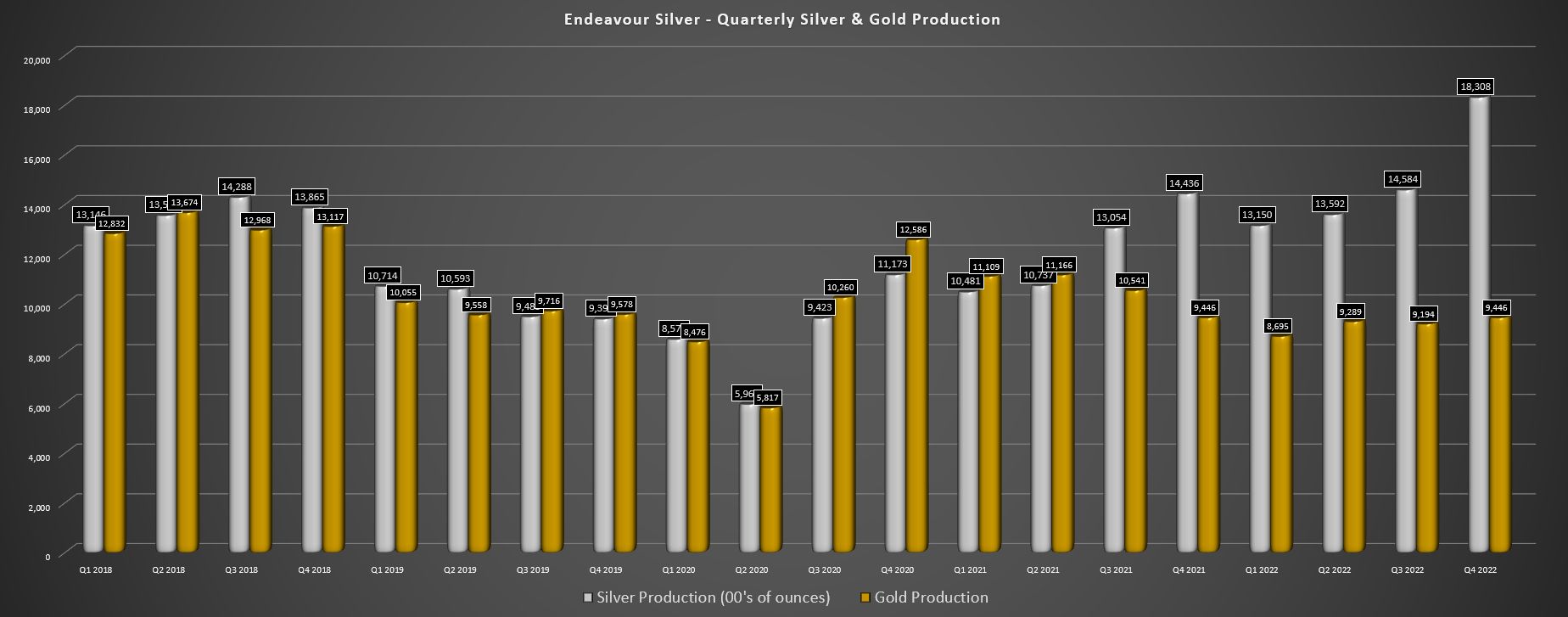

Endeavour Silver released its Q1 results last week, reporting quarterly production of ~1.62 million ounces of silver and ~9,300 ounces of gold. This translated to a 23% and 7% increase in silver and gold production, respectively. This was driven by higher production at Guanacevi, which enjoyed a much higher average grade of 511 grams per tonne of silver and 1.42 grams per tonne of gold and flat production at its smaller Bolanitos Mine which made up for slightly lower gold grades (1.70 grams per tonne of gold vs. 1.73 grams per tonne of gold) with higher throughput (~108,700 tonnes processed).

Endeavour Silver - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

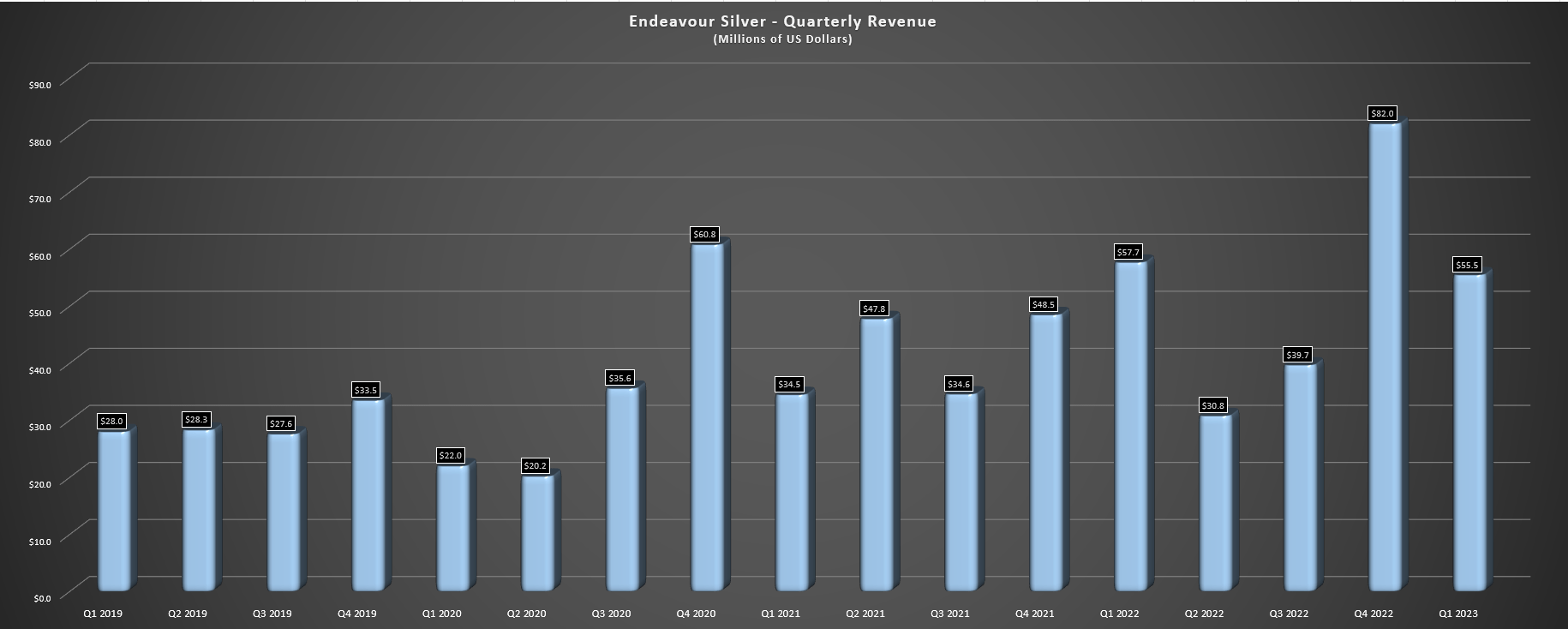

Digging into Guanacevi a little closer, we can see that the mine has continued to benefit from higher grades, which have trended up over the past two years, and while production was slightly lower sequentially (Q1 vs. Q4), this was primarily because of maintenance in February that resulted in lower throughput (1,138 tonnes per day). The combination of higher ounces of gold sold offset by slightly lower average realized prices of $23.16/oz and $1,917/oz for gold and silver respectively translated to revenue of $55.6 million in the period. Unfortunately, operating cash flow before working capital slid to just $12.5 million, down 39% year-over-year.

Endeavour Silver - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

Regarding FY2023 guidance, Endeavour Silver is tracking well against guidance with ~2.37 million SEOs produced in Q1, tracking well ahead of the guidance range of 8.6 - 9.5 million SEOs. That said, the key will be if the company can maintain its grade profile at Guanacevi, which continues to benefit from grades well above reserve grades with no guarantees that this continues. I have shown this in the below chart, with the average silver grade (blue line) and the average silver reserve grade per 2022 reserves (red line), with grades clearly continuing to outperform expectations (albeit at the cost of higher royalties).

Finally, at Terronera, the company has green-lighted the project with an expectation of first production by Q4 2024. While capex increased materially to $230 million from the previous estimate of $175 million, this was partially because of a change in scope (2,000 tonnes per day vs. 1,700 tonnes per day) and the company has spent over $50 million on development and has a solid head-start on construction due to progress on early works. This includes site access road improvements (7 kilometers), the receipt of mobile mining equipment (jumbos, bolters, scoops, dump trucks and scissors lifts, plus other support equipment), and Portal #1 site preparation, with underground development underway.

As discussed in past updates, Terronera will be a game-changer for the company, with the ability to significantly increase production at much lower costs, helping to transform Endeavour Silver from a high-cost producer to a mid-cost producer and potentially a low-cost producer depending on grades at Guanacevi starting in H2-2025.

{kind=link}

Costs & Margins

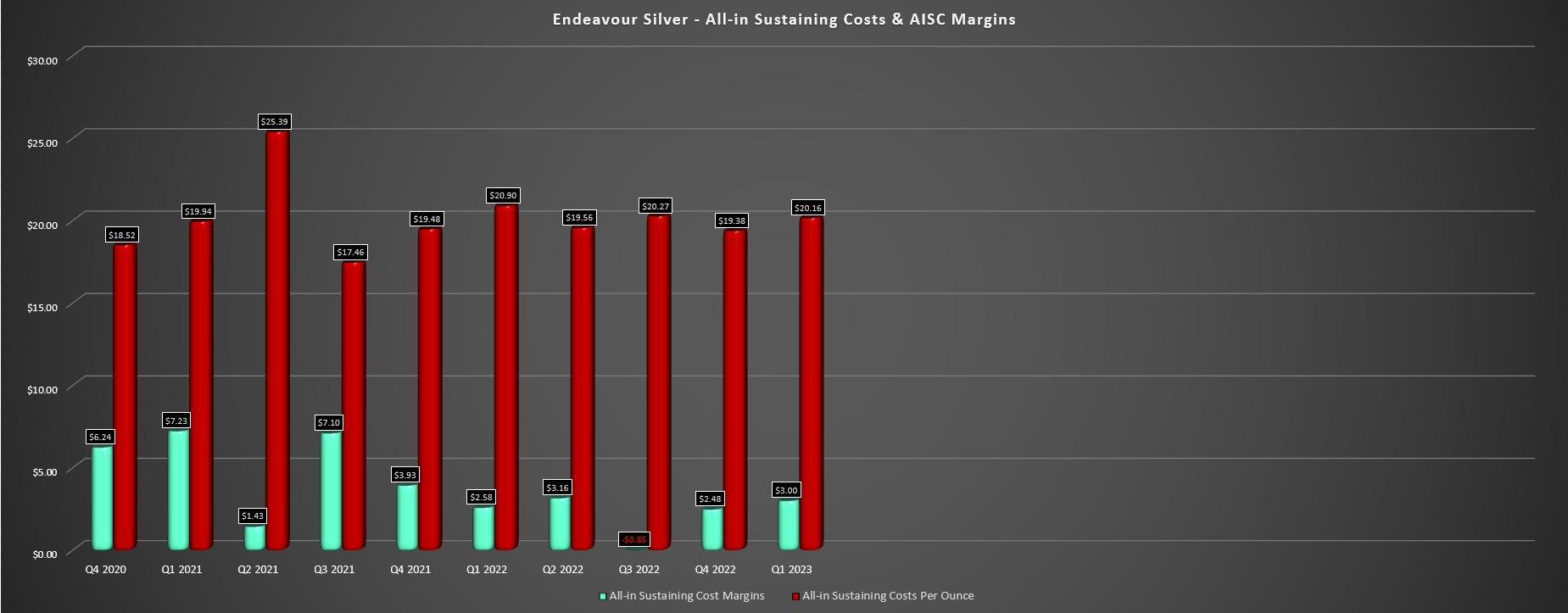

Moving over to costs and margins, Endeavour's cash costs came in at ~11.12/oz in Q1, a 9% increase from $10.21/oz in the year-ago period. Meanwhile, although all-in sustaining costs dipped 4% from $20.90/oz to $20.16/oz, these continue to be some of the highest costs sector-wide, especially given that these costs are net of gold by-product credits. The company noted that the strengthening Mexican Peso was one culprit for the rising costs (~33% of costs in Pesos), but inflationary pressures also continued to bite, with rising labor, power, and consumables costs.

Endeavour Silver - All-in Sustaining Costs & AISC Margins (Company Filings, Author's Chart)

{kind=link}

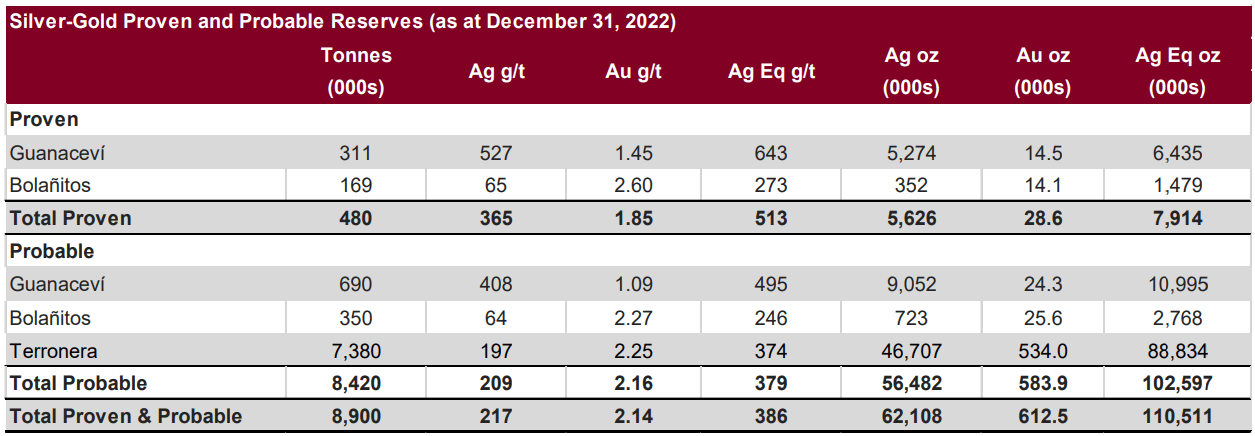

Although some investors might rejoice with the lower AISC reported year-over-year, Guanacevi continues to benefit from head grades above its average reserve grade of ~446 grams per tonne of silver and ~1.20 grams per tonne of gold, with average grades of 511 grams per tonne of silver and 1.42 grams per tonne of gold in Q1. This is helping to drag down costs, but if costs are already coming in near $19.50/oz at the mine ahead of a potential normalization in head grades, this is certainly not encouraging from a unit standpoint and keeping costs below $20.00/oz long-term. Plus, Bolanitos continues to operate at negative AISC margins, with AISC margins of [-] ~$4.00/oz in Q1 2023.

{kind=link}

From an all-in cost standpoint (including growth capital), Endeavour's all-in costs came in at $29.98/oz, up from $26.53/oz in the year-ago period. This continues to be one of the worst margin profiles sector-wide, and these costs are still well above the company's average realized silver price even after the rally we've seen in silver. So, while Terronera will turn things around, it's difficult to be bullish on optimistic about the future of Bolanitos' future operationally given its much higher costs, and although Guanacevi is carrying the company today, it has just less 2.5 years of mine life on tonnes in reserve inventory, so the key will be to add more ~550 gram per tonne silver-equivalent material to reserves to keep costs down, which may not be easy.

As it stands, Guanacevi has a solid M&I resource base backing up reserves (~611,000 tonnes) but grades are lower at 390 grams per tonne of silver and 0.95 grams per tonne of gold, or a silver-equivalent grade of ~460 grams per tonne silver-equivalent, 20% lower than the current reserve grade of 536 grams per tonne silver-equivalent. Silver-equivalent grades are based on a 75 to 1 gold/silver ratio.

Finally, it's worth pointing out that all-in sustaining costs are already tracking above the guidance midpoint of $19.50/oz for 2023 and the Mexican Peso certainly isn't helping in Q2 with it sitting at 5-year highs vs. the United States Dollar ( UUP ) and stronger than Q1 levels. In addition, sustaining capital is sitting at just ~23% of the annual guidance of $34.7 million, with the potential for slightly higher sustaining capital than planned because of inflationary pressures. So, with some minor catch-up on sustaining capital in the following three quarters to meet the guided expenditures and the stronger Peso, I'm less optimistic on Endeavour's ability to meet its guidance midpoint of $19.50/oz on costs.

Let's dig into Endeavour Silver's valuation:

Valuation

Based on ~197 million fully diluted shares and a share price of US$3.40, Endeavour trades at a market cap of ~$670 million. This has left the company trading at a premium to its estimated net asset value of $600 million when factoring in an estimated $80 million in corporate G&A. And while the current P/NAV multiple of ~1.10x is a deep discount to peers like First Majestic Silver ( AG ), I have found minimal value in paying a 20% plus premium to net asset value for precious metals producers unless they have exceptional assets that are in top mining jurisdictions. While Terronera is a solid asset, it's hard to argue the same for Bolanitos, and Mexico certainly isn't a Tier-1 jurisdiction.

Even if we use a fair multiple of 1.35x P/NAV once Terronera is in production to account for the higher multiples that silver producers often command, this points to a fair value for Endeavour Silver of ~$820 million or US$4.15 per share. And although this points to a 21% upside from current levels, I prefer a minimum 40% discount to fair value for small-cap producers. After applying this discount to an estimated fair value of US$4.00, Endeavour's ideal buy zone would come in at US$2.50 or lower.

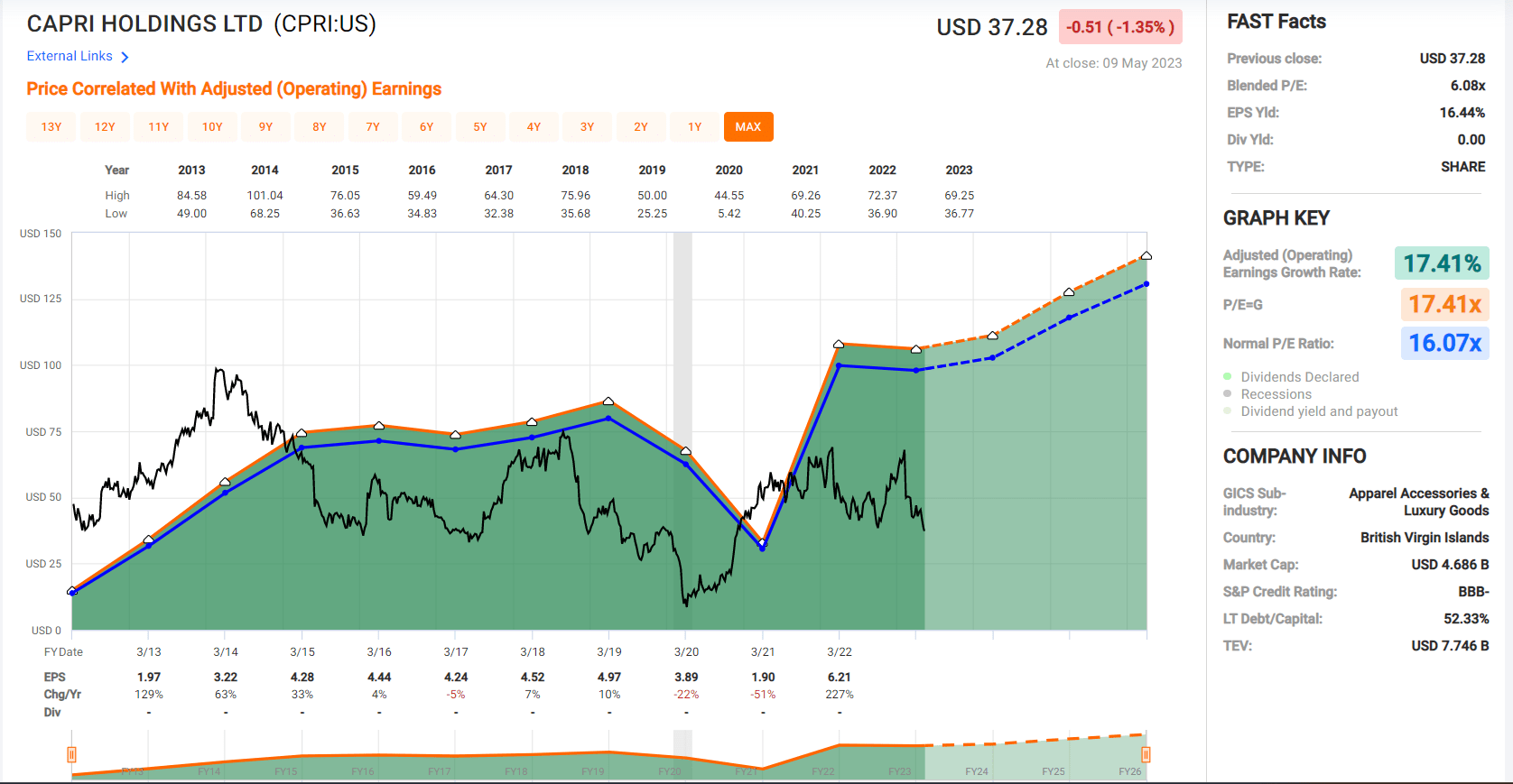

Capri Holdings - Historical Earnings Multiple & Current Valuation (FASTGraphs.com)

{kind=link}

Some investors might argue waiting for these prices could be an opportunity cost and that may be the case, but I prefer to buy at a deep discount to fair value or pass entirely. And with businesses like Capri Holdings ( CPRI ) trading at 6.0x FY2024 earnings estimates, I see far more value here than paying ~35x FY2024 earnings estimates for Endeavour Silver, with Capri having much higher margins. As for looking solely within the precious metals space and comparing to Endeavour's valuation, I see more attractive opportunities here as well, with one example being Marathon Gold at less than 0.70x P/NAV which is expected to start production at the same time as Terronera but in a more attractive jurisdiction (Canada vs. Mexico).

Summary

The investment case for Endeavour Silver has finally improved with Terronera green-lighted, but with commercial production nearly two years away, Bolanitos' future being uncertain, and a potential normalization in grades at Guanacevi after a phenomenal six-quarter stretch, it's tough to justify paying up for the stock. And while Endeavour is certainly more reasonably valued than First Majestic, this isn't saying much when First Majestic continues to trade at the highest P/NAV multiple sector-wide. To summarize, I continue to see more attractive opportunities elsewhere, and I would need to see a pullback closer to US$2.60 for EXK to become interested in the stock from a swing-trading standpoint.

For further details see:

Endeavour Silver: Inflationary Pressures Continue To Pressure Margins