EXK - Endeavour Silver: Rising Peso Hurts In More Ways Than One

2023-08-30 15:12:14 ET

Summary

- Endeavour Silver's Q2 report showed increased production and sales, but costs rose sharply year-over-year and margins compressed further despite a higher silver price.

- Endeavour noted that costs were impacted by higher labor, power, and consumables costs, and this could impact capex estimates at Terronera.

- In this update, we'll look at whether Endeavour Silver is offering enough margin of safety to justify a new long position after its ~50% correction.

Just over two years ago, I wrote on Endeavour Silver ( EXK ), noting that while the stock offered growth, it was at an unreasonable price, and that any rally above US$7.20 would provide an opportunity to book some profits. This was because Terronera's first production was still over three years away, more share dilution was likely given the track record of consistent dilution, and free cash flow would remain pressured unless silver stayed above $25.00/oz. Since touching the US$7.20 level the following month, Endeavour Silver has underperformed its peer group, declining ~58% vs. a ~45% decline in the Silver Miners Index ( SIL ). However, despite the magnitude of this correction, I still don't see an investment thesis here, with the stock never belonging above US$6.00 in the first place and the outlook being poorer with sticky inflationary pressures, a sharply rising Mexican Peso, short reserve lives, and further share dilution as I expected (equity offering, Pitarrilla deal). Let's dig into recent developments and the valuation below:

{kind=link}

Endeavour Silver - May 2021 Update - Seeking Alpha Premium/PRO

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

{kind=link}

Endeavour Silver - Quarterly Silver & Gold Production - Company Filings, Author's Chart

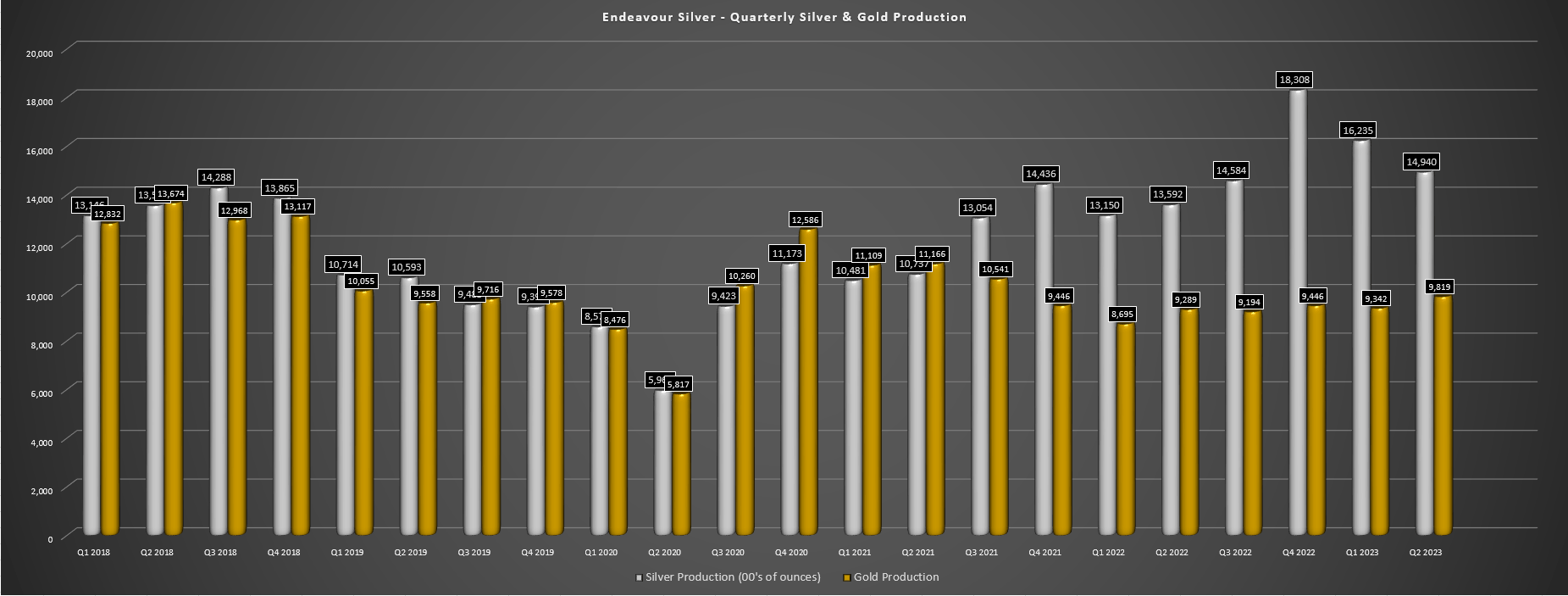

Endeavour Silver ("Endeavour") released its Q2 results earlier this month, reporting quarterly production of ~1.49 million ounces of silver and ~9,800 ounces of gold, an increase from the ~1.36 million ounces of silver and ~9,300 ounces of gold produced in the year-ago period. This represented a 10% and 6% increase, respectively, driven by higher gold grades at Bolanitos and higher throughput at both operations relative to Q2 2022 levels. The result is that Endeavour is tracking well against its FY2023 guidance mid-point of ~9.0 million silver-equivalent ounces [SEOs], with ~4.65 million SEOs produced year-to-date, translating to ~52% of annual production. Plus, the company noted that grades at Guanacevi should tick up in H2, suggesting a high probability of the company meeting or beating its FY2023 guidance mid-point.

{kind=link}

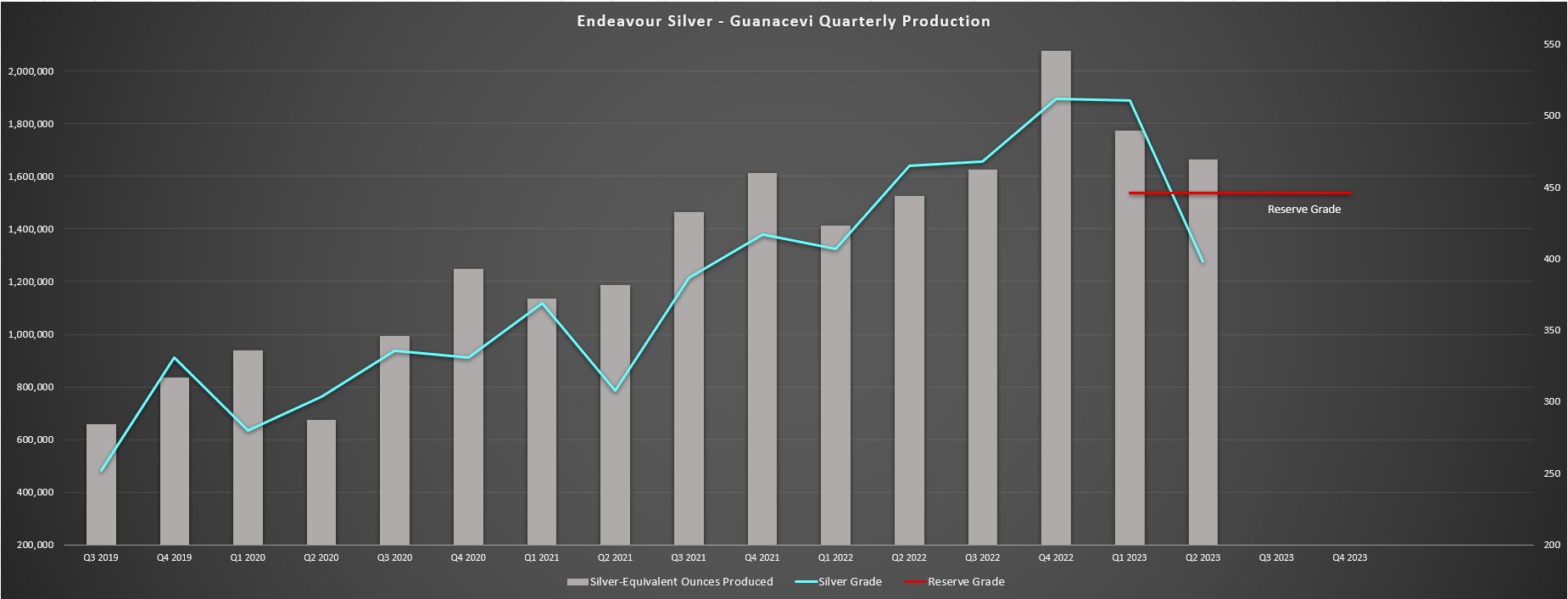

Guanacevi - Silver Grades & Quarterly Production vs. Current Reserve Grade - Company Filings, Author's Chart

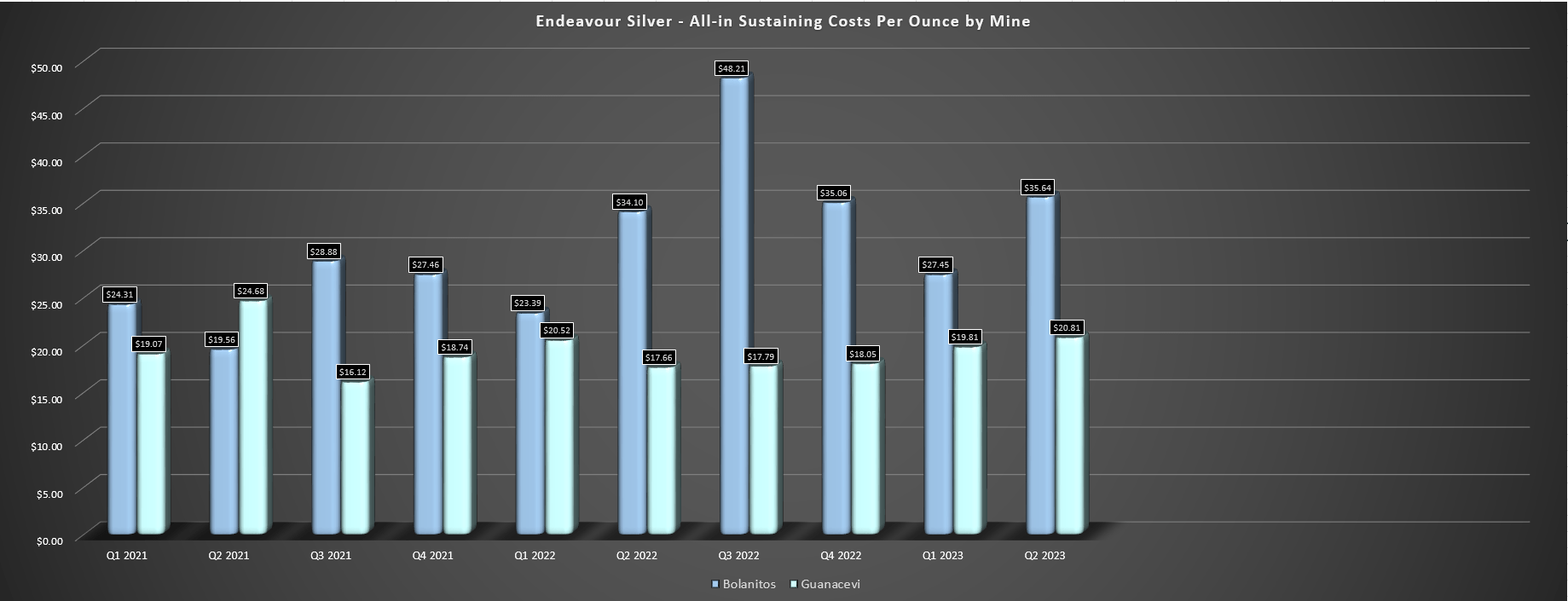

Digging into the operations a little, Guanacevi saw lower grades year-over-year at 398 grams per tonne of silver, and while production was higher at ~1.66 million SEOs, this was throughput driven, translating to higher costs at the asset. The company noted in its prepared remarks that the lower grades were related to mine sequencing changes, with the company losing one of its high-grade stopes in the quarter. However, I remain less optimistic regarding the ability of this asset to maintain sub $20.00/oz AISC post-2024, given that Endeavour has continued to mine at grades above its reserve grade outside of the most recent quarter, and if grades normalize, we could see costs pulled higher related to the lower production profile or reliance on throughput to drive production vs. rising grades which have provided a boost to this asset's overall production.

{kind=link}

Endeavour Silver - Quarterly Revenue - Company Filings, Author's Chart

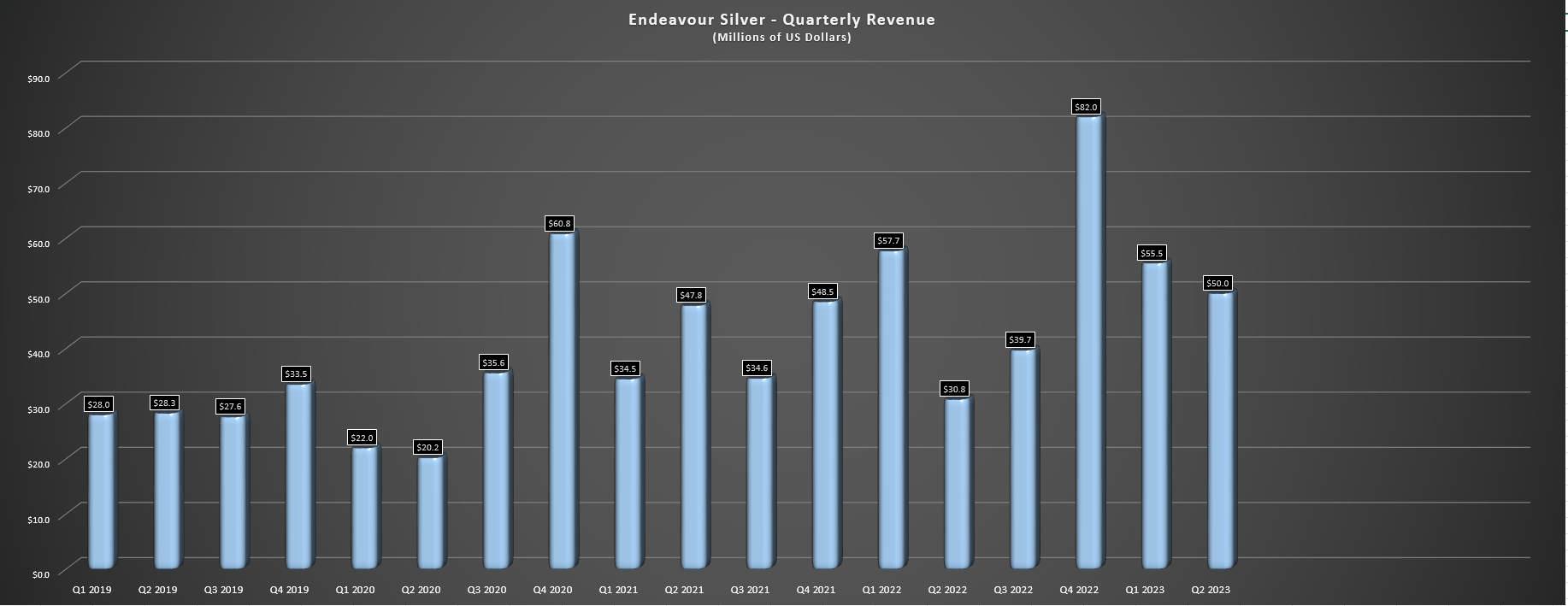

As for Endeavour's sales, the company reported a ~61% increase in revenue to $50.0 million in Q2, which might appear to be a blowout figure and one of the largest sales increases year-over-year sector-wide. However, it's important to note that the company was up against easy year-over-year comps from a sales standpoint, having sold just ~603,000 ounces of silver in the year-ago period because of withholding inventory. Hence, the increase in revenue was hardly anything to write home about, with the primary reason for the increase being the easy year-over-year comps, with further help from a higher average realized silver price ($24.27/oz vs. $22.72/oz). As for cash flow, operating cash flow came in at $11.1 million vs. $3.6 million, and Endeavour finished the quarter with $43.5 million in cash, down from $61.6 million in Q1 2023.

Costs & Margins

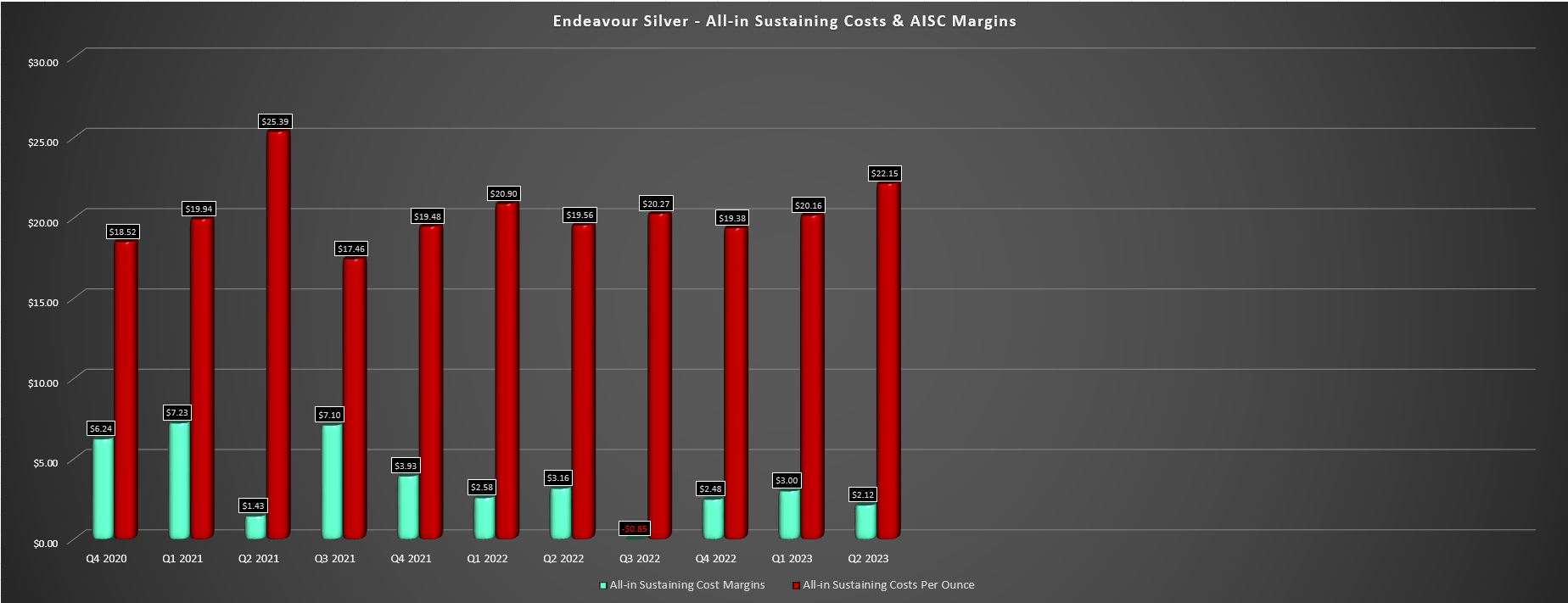

Unfortunately, while production and sales came in at respectable levels despite the lost stope at Guanacevi, the company's costs and margins likely came in below investors' expectations. In fact, cash costs rose 34% year-over-year to $13.52/oz while all-in sustaining costs [AISC] soared to $22.15/oz, giving Endeavour some of the highest costs sector-wide. Endeavour noted that cost increases were attributed to higher labor, power, and consumables costs at both of its mines, with a significant headwind from the Mexican Peso soaring to a new 7-year high vs. the US Dollar ( UUP ). So, with year-to-date AISC of $21.11/oz, management expecting similar costs in H2, and guidance being at $19.00/oz to $20.00/oz, Endeavour has little hope of delivering into cost guidance this year, with costs likely to come in above $20.80/oz (4% above the top end of guidance).

"We're expecting our costs to be above the upper bound range of our guidance. So we're not restating the number, but we do expect for the second half of the year our cost metrics to be similar to H1, which again puts us above the upper bound range of our original guidance."

- Endeavour Silver, Q2 2023 Conference Call

{kind=link}

Endeavour Silver - AISC Per Mine - Company Filings, Author's Chart

Looking at Endeavour's margins, the higher metals prices helped from a by-product and selling price standpoint, but margins still fell 33% to $2.12/oz. As noted, this was related to higher all-in sustaining costs which offset the benefit of the higher average realized silver price, and given the inflationary pressures and the strength in the Mexican Peso, AISC margins are considerably lower than they were in Q4 2020 ($2.12/oz vs. $6.24/oz) when the company benefited from a higher average realized silver price. So, for investors that believe this ~40% decline in the stock is unjustified, the stock has actually held up better than its margins which are down over 60% in the same period while the weighted average share count has increased ~26% as well (~191 million vs. ~151 million), outpacing the rate of share dilution we've seen from the average precious metals producer in the period.

{kind=link}

Endeavour Silver - AISC & AISC Margins - Company Filings, Author's Chart

Recent Developments

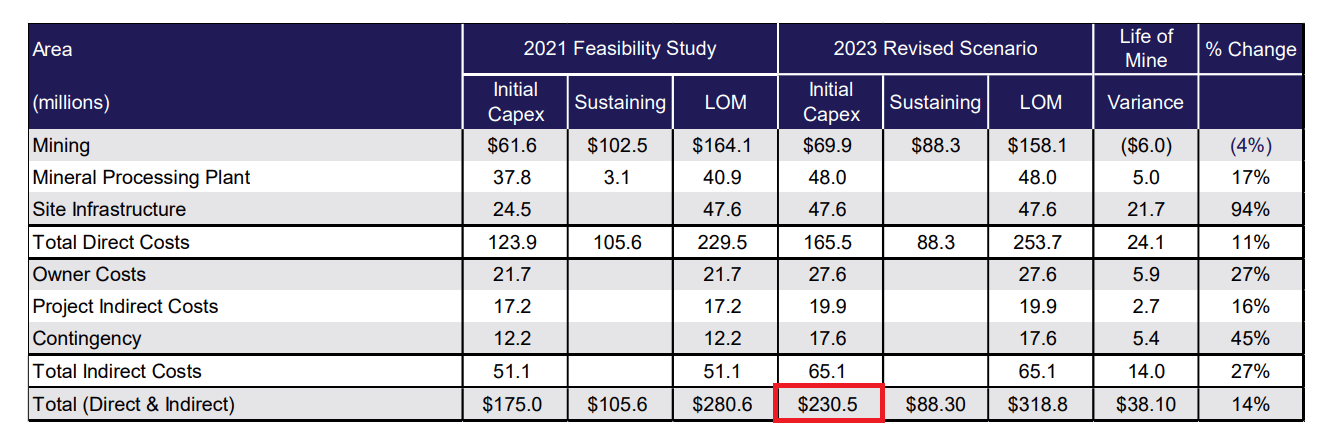

Finally, looking at recent developments, investors can be comforted to know that ~$144 million of the ~$230 million capex budget has been committed at Terronera and project construction is 30% complete as of quarter-end. Plus, the company confirmed on its Q2 2023 Conference Call that roughly $30 million to $50 million is tied to the Mexican Peso, meaning that even if we saw an average increase of 15%, this would translate to just ~$8 million in higher costs. That said, with inflationary pressures remaining in place and headwinds from a currency standpoint, I think a safer assumption when it comes to total upfront capex is $255 million, representing a ~10% increase vs. initial projections.

{kind=link}

Terronera Initial Capex Estimates - Company Filings

Based on this figure and limited free cash flow generation to provide any buffer, I would not be surprised to see more share dilution through an equity financing between now and commercial production. Hence, for investors, hoping that the fully diluted share count would stay below 200 million (currently ~196 million), this seems highly unlikely. Plus, the company noted in its Q2 2023 Conference Call that it would prefer to use equity vs. debt for any cost overruns, confirming that taking on additional debt to pad its expected working capital position while the mine ramps up is not the preferred option. And while this wouldn't be the end of the world if Endeavour was trading at a higher share price, dilution is costly at these levels and if it uses its recently announced ATM ($60 million), this could provide an overhang for the stock.

"And I think for us as the management team we think that's kind of the upper end that we want to take on from a debt standpoint. We did put in the $60 million ATM facility that we haven't drawn -- protection. Ultimately, if we do end up above the $230 million we prefer that to come from equity just because we don't want to get too levered to debt."

- Endeavour Silver, Q2 2023 Conference Call

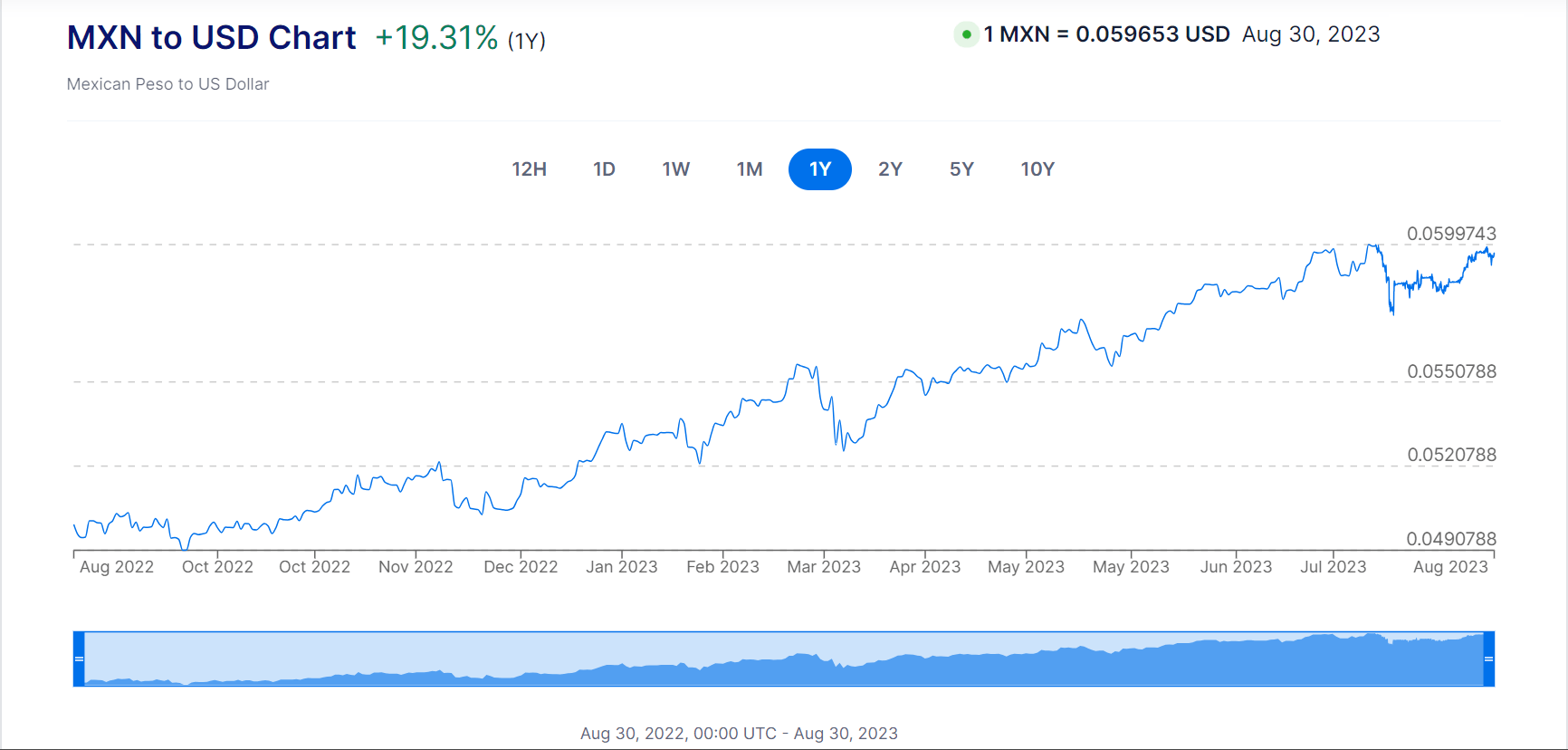

Finally, while a cooling in the Mexican Peso relative to Q2 levels might have inspired confidence that Endeavour could keep costs below $21.00/oz this year, this has not been the case, with the Mexican Peso trying to reach for a new high relative to the US Dollar. This is not ideal for project capex or current operations, and it's not ideal for reserves either, with the potential for cut-off grades to be revised higher yet again this year on the back of mid to high single-digit inflation. And with Endeavour Silver having two relatively short mine lives at its operating assets and it already using $23.00/oz silver to calculate reserves, I think there's risk to unsuccessful reserve replacement this year. So, while the Mexican Peso strength is negative for current operating costs, it's also negative from a reserve replacement standpoint and from a capex standpoint, suggesting risk of further share dilution and the possibility of an underwhelming reserve update at year-end.

{kind=link}

Mexican Peso vs. US Dollar - XE.com

Valuation

Based on ~196 million fully diluted shares and a share price of US$3.00, Endeavour trades at a market cap of ~$590 million, which might appear to be a very reasonable price for a multi-million ounce silver producer and a name that previously commanded a market cap of ~$1.2 billion at its 2021 peak. However, I believe it's less important where a stock has been (since stocks overshoot in both directions) and more important where fair value should be, and while the stock may have traded above US$7.00 previously, this was with four major differences:

- a lower share count

- a weaker Mexican Peso

- significantly higher AISC margin

- higher investment attractiveness scores for Mexico, which is dropping in ranks as a mining jurisdiction

Given these material changes over the past two years and given that Endeavour continues to have razor-thin margins, it's hard to argue that EXK is worth much more than $650 million, and that's using a generous multiple (1.2x P/NAV) relative to where other silver producers like Pan American Silver ( PAAS ) trade today (~0.90x). This is because EXK's estimated net asset value comes in at ~$575 million, and I've never found any value in paying over 1.0x P/NAV for high-cost producers in Tier-2 ranked jurisdictions. Plus, even if we apply a multiple of 1.2x to assign a premium for its silver exposure (silver producers typically trade at higher multiples than their gold peers), this points to a fair value of ~$690 million or US$3.52 per share. And while this does point to upside from here, I am looking for a minimum 35% discount to fair value to justify buying small-cap names, placing EXK's low-risk buy zone at $2.30 or lower.

Obviously, there's no guarantee that Endeavour Silver trades down to these levels, which it hasn't seen in years. However, I believe in buying at the right price with a significant discount to fair value or passing entirely, and for depleting businesses without pricing power that have high concentration to Tier-2 jurisdictions with no current free cash flow generation, I want to be compensated for that added risk. And for a producer with all of its eggs in one basket (two Mexican mines and one development project), a poor track record of creating shareholder value (lack of production per share growth and steady share dilution), and one not paying dividends, I think requiring a significant margin of safety makes sense, and that is not present today. Of course, some investors might prefer to use $75/oz and $100/oz silver to justify making their investments, but I don't see that generating consistent positive returns and see it akin to gambling.

To summarize, I don't see anywhere near enough margin of safety at current levels, and with some capex risk for Terronera, another weak Q3 ahead because of the persistent strength in the Mexican Peso, and commercial production at Terronera still ~21 months away, I continue to see dozens of more attractive opportunities elsewhere in the market vs. Endeavour Silver.

Summary

Endeavour Silver had a rough Q2 report, and while revenue was boosted by easy year-over-year comps (withholding inventory in year-ago period), margins compressed further to just ~9%, well below the industry average. Unfortunately, the forward outlook isn't much better given the persistent strength in the Peso, with Q3 setting up to be a similarly high-cost quarter. And while Terronera will fix these issues, we're still nearly seven quarters away from the company declaring commercial production here, and we could see continued pressure on reserves, margins, and potential share dilution in the interim if the Peso doesn't cool off. So, with other producers sector-wide trading at cheaper valuations with more attractive jurisdictional profiles, much higher margins, and higher quality ore bodies relative to EXK's average asset, I continue to see EXK as an inferior buy-the-dip candidate.

For further details see:

Endeavour Silver: Rising Peso Hurts In More Ways Than One