ENLAY - Enel: 8.1% Dividend Yield From This Growing Utility

2023-03-08 18:33:02 ET

Summary

- Recently I wrote an article on a global Spanish-based utility Iberdrola praising it for its growth prospects and high renewables exposure.

- Today I cover an Italian-based utility giant Enel which offers even higher return potential.

- This conservative utility company pays an 8.1% dividend yield and trades at a substantial discount to peers.

- See my thesis for Enel which is one of my highest conviction stocks for 2023.

Dear readers/followers,

Following my recent article on Iberdrola I want to present my analysis of another global utility company I have in my portfolio - Enel ( ENLAY ). Similarly to Iberdrola the company offers an interesting opportunity for defensive income oriented investor to add significant yield as well as renewables exposure to their portfolio. Recently Enel disposed of all of their energy generating assets in Russia, significantly improving the perception of the company.

Note: The native EUR denominated shares trade on the Milan Stock Exchange under the ticker ENEL. As a European investor, these are the shares I prefer and these are the shares I'll be referring to in my article. There is an Italian withholding tax for foreign investors, but you should be able to recover it if your country has a double tax treaty with Italy (almost all developed countries do), so check with your tax advisor and take that into account. There is also a USD denominated ADR that trades under the ticker ENLAY, but has low liquidity and I haven't checked it in detail so do your own research before investing.

Basics

Enel is one of the largest utility companies in the world. The Italian-based company is fully integrated meaning that it is involved in the entire electricity supply chain from power generation to distribution. Their operations are mostly concentrated in Italy (30%), Latin America (28%), Spain (24%) and the USA (8%) followed by smaller exposures to the rest of Europe and Mexico. Their Latin America exposure is spread across most of the continent with major operations in Chile, Brazil, Argentina, Colombia and Peru.

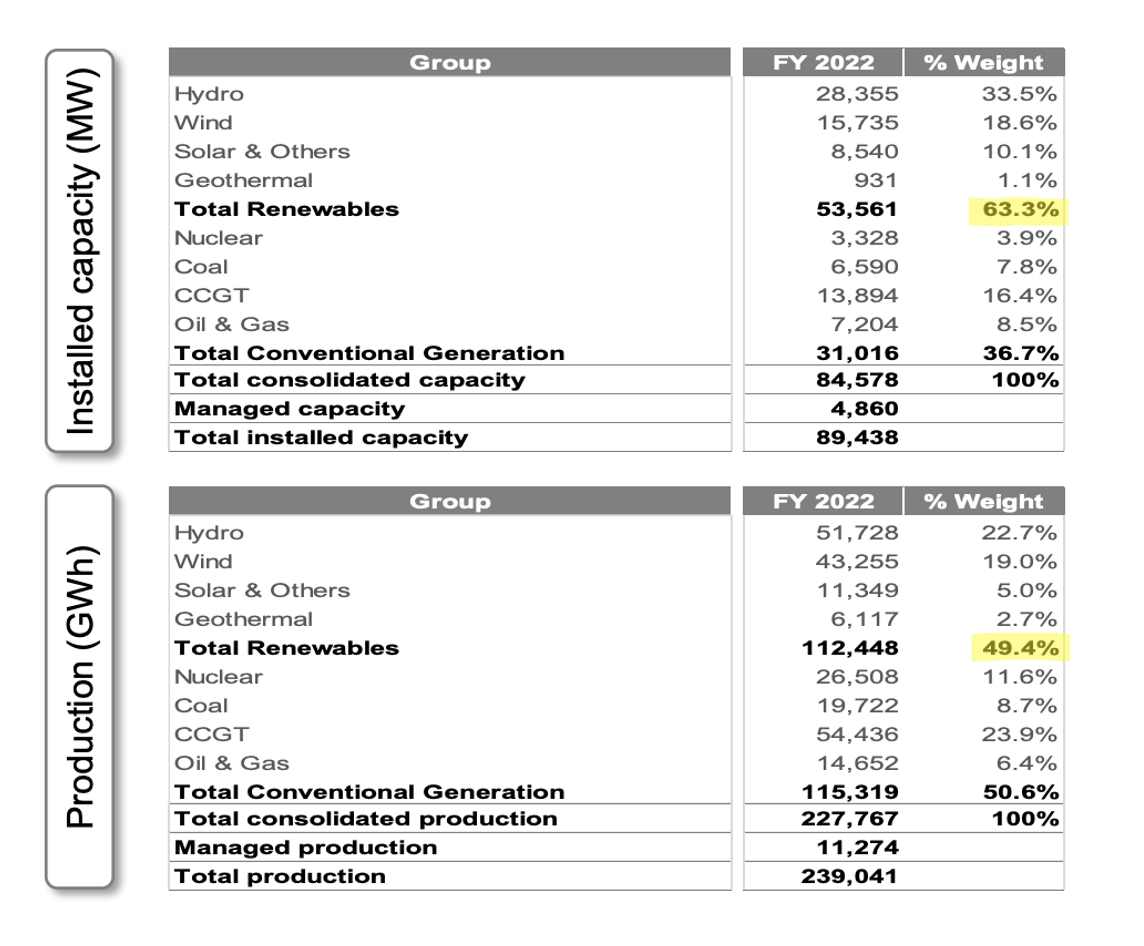

Enel is also shifting towards renewable Energy, but at a slower pace than Iberdrola as the company still has significant exposure to fossil fuels, including coal, which it aims to eliminate by 2030. As of today 63% of installed capacity and 50% of production comes from renewables, dominated by hydro and wind. In terms of conventional sources of energy, the majority is generated by combined cycle gas turbine (CCGT) facilities followed by non-negligible amounts in nuclear, oil & gas and coal.

{kind=link}

Financials

Enel released their 2022 preliminary results statement and operating data presentation in February. Revenues increased by more 60% YoY, primarily driven by higher energy prices, although the company did see an 11% increase in the volume of energy sold in Italy and Spain and a 21% increase in the volume of energy sold in Latin America. Ordinary EBITDA increased by 2.6% YoY to EUR 19.7 Billion, exceeding the higher-end of guidance for the year. EBITDA, which includes some non-ordinary items (mainly gains on M&A transactions), increased by 9.3% YoY.

The company has massive expansion plans going forward as they plan to deploy over $200 Billion into new energy producing assets by 2030. This money will primarily be going to expanding their renewables production. This will put Enel on the forefront of renewables energy production as one of the largest global players. Management plans to deploy capital in strategic/growing Tier 1 markets where they already have an established presence and exit from non-core countries. The geographical relocation plans have mainly focused on exit from Russia. In Q3 2022, Enel sold its entire stake in Enel Russia completing a full exit from power generating assets in Russia. This transaction has significantly improved investors perception of Enel, especially in light of the Ukraine-Russia conflict, and improved the renewables/legacy production ratio as nearly all Russian assets were conventional generation assets. Since the timing of the exit corresponded with a market bottom, unsurprisingly it helped spark a 40% rally in stock price.

Going forward the company expects to grow its ordinary EBITDA by 5-6% per year, fueled mainly by increased energy production. What's important is that dividends that stood at EUR0.40 per share in 2022 (7.5% dividend yield) are expected to grow by a similar percentage going forward. This means a forward 2023 dividend yield of 8.1% and by 2025, today's investors could have a yield on cost of almost 9%. That's really impressive considering that you're investing in one of the largest utility companies in the world and one that has solid growth prospects as it transitions to renewables.

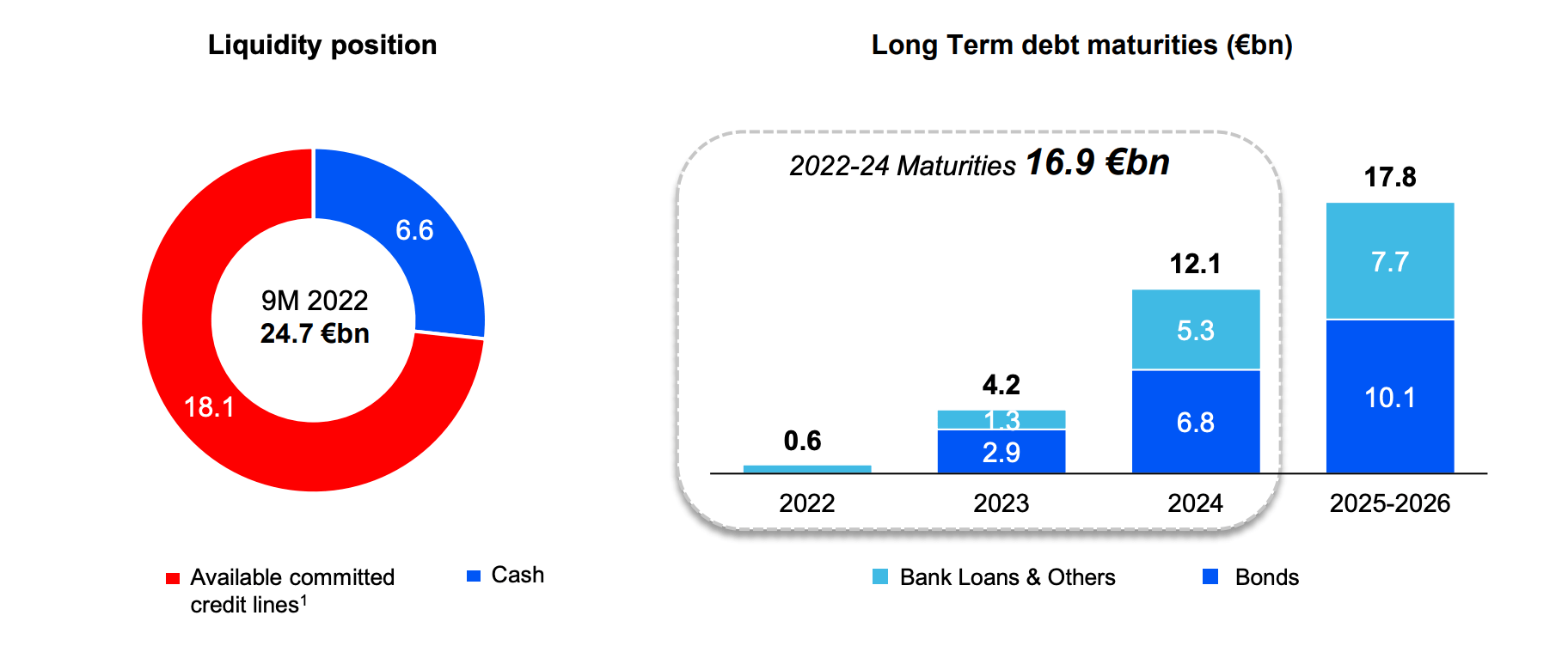

Of course no investment comes without risk. For Enel, as interest rates remain high, part of the risk comes from their level of debt. The company finances most of their expansion from debt, which currently stands at a EUR 60 Billion. That's a lot of debt and it's up 16% YoY, mainly due to aggressive CAPEX and the negative effect of FX. With aggressive future expansion plans, I don't expect the debt to decrease materially any time soon, though with a very reasonable net debt/EBITDA of 2.6x I also don't expect it to be a major problem for the company. This is affirmed by the abundant liquidity of almost EUR25 Billion that the firm has access to, of which EUR 6.6 Billion is in cash.

{kind=link}

To sum-up Enel is fundamentally a healthy company that is doing all the right things to grow and capitalize on the transition to the renewable energy future. There are no significant red flags here making this a relatively conservative investment.

Valuation

In order to be a buy though, we also need to be able to buy at a reasonable price so let's have a look at the valuation. Enel currently trades at a forward PE of 9x, despite the fact that historically it has traded at an average closer to 14x. Compared to peers it also trades as very reasonable levels and below some of its European peers with significantly lower renewables exposures and significantly lower growth outlooks. I'd argue that it should trade at a premium, not a discount, compared to companies like Engie ( ENGIY ) and RWE ( RWEOY ) for the reasons discussed.

| Company |

| P/E |

| Enel |

| 9.0x |

| Iberdrola |

| 16.0x |

| Engie |

| 9.6x |

| E.ON |

| 10.5x |

| RWE |

| 9.4x |

This leads me to conclude that Enel is still undervalued, even after the 40% rally it has seen since October. Assuming that management will deliver on their forecast and grow the company by 6% per year going forward (quite likely) and assuming a conservative multiple of 12x, I get a PT of EUR 8.0 per share. That's assuming a 12x earnings which is significantly below the historical average as well as the multiple of Iberdrola which I consider a solid buy at this level, though Iberdrola likely deserves a premium because it's greener and expected to grow even more than Enel.

The price target allows for a 50% upside which I see as very achievable in the next two to three years in addition to collecting an 8.1% growing dividend.

With that said, as always, let's have a look at what we can reasonably expect from the company going forward:

- 8.1% dividend yield (growing at 6% per year)

- 6% EPS growth for the next two to three years

- 10% annual return from multiple expansion as the company returns to 12x earnings

- -> total return potential of 24.1% per year

Remember how I generate alpha:

- Start with a thesis why a given industry/sector should outperform

- stay overweight in those sectors for as long as the thesis is valid

- look for companies with sound fundamentals that are either undervalued or fairly valued with exceptional growth prospects

- if a company becomes overvalued, trim the position and rotate into another stock/sector that is still undervalued

- if a company becomes increasingly undervalued and the thesis is still valid, add to the position

- generate alpha and repeat.

My total return then comes from the dividend yield, EPS growth and multiple expansion as the valuation normalizes over time. I always target a total return in excess of market returns (>8%) to generate alpha.

What things do I look for when selecting individual stocks to buy?

- strong and safe fundamentals

- good management teams with a track-record of caring about shareholders

- healthy EPS growth

- well-covered dividend

- discount relative to peers and/or historical fair multiples

- other catalysts.

Takeaway

Enel is a world-class integrated utility company determined to grow their renewables portfolio to become a leading player in the space. The stock currently offers a safe dividend yield of 8.1% which is expected to grow by 6% per year. This makes the stock very attractive especially when we consider that this is a conservative utility company that is doing all the right things. Their recent exit from Russia significantly improved my perception of the company and now the potential for growth vastly outweighs the risks that mainly have to do with high interest rates. With a 50% upside to my price target I rate Enel as a " BUY " here at EUR 5.3 per share and a PT of EUR 8.0 per share. I already have a large position in the company as Enel and Iberdrola represent my two largest utility holdings.

For further details see:

Enel: 8.1% Dividend Yield From This Growing Utility