ENIC - Enel: Attractive With A Solid Utility Upside

Summary

- Enel is an attractive and fundamentally safe utility company trading at a massive discount to its overall potential. I've invested tens of thousands into the company.

- I continue to look for undervaluation opportunities - and one of the highest valuation opportunities in utilities is now Enel. I've bought it several times, and keep adding more.

- Let me show you, and update my thesis on Enel.

Author's Note: This article was published on iREIT on Alpha in mid-October of 2022.

Dear subscribers/readers,

You remember Enel ( ENIC ) ( OTCPK:ENLAY ) - the Italian multinational producer and distributor of electricity and gas. The 60-year-old privatized former-public company which owns a huge part of the Italian market, and is still in turn, owned by the government, at over 20% of the shares through its Ministero dell'Economia e delle Finanze.

What we can add to this article is that the company's yield based on the current yield is more than 9% - well above most current inflation. This, coupled with fundamentals and valuation, makes this company even more of a "BUY" today than it was.

Revisiting Enel - An undervalued Utility

So, Enel is one of the largest in the world - not just in its sector, but in any sector. With revenues of over €85B on an annual basis, this is one of the largest companies on earth - at least top 100. The company is also one of the largest power companies in the entire world. Its native listing is on the Milan Stock Exchange, under the symbol ENEL, and it's a solid component of the Borsa Italiana.

Utility and infrastructure investments continue to represent great opportunities, as I see things, with the market in its current shape. Specifically, these are great income opportunities. Their relative yields and relative safety, to my mind, offer superb "fortresses" of safety in a stormy world. Enel, despite some of the challenges I'm going to mention, is no different. Its assets are rock-solid, it's going nowhere. It's investment-grade rated by S&P Global, and A-rated by Fitch.

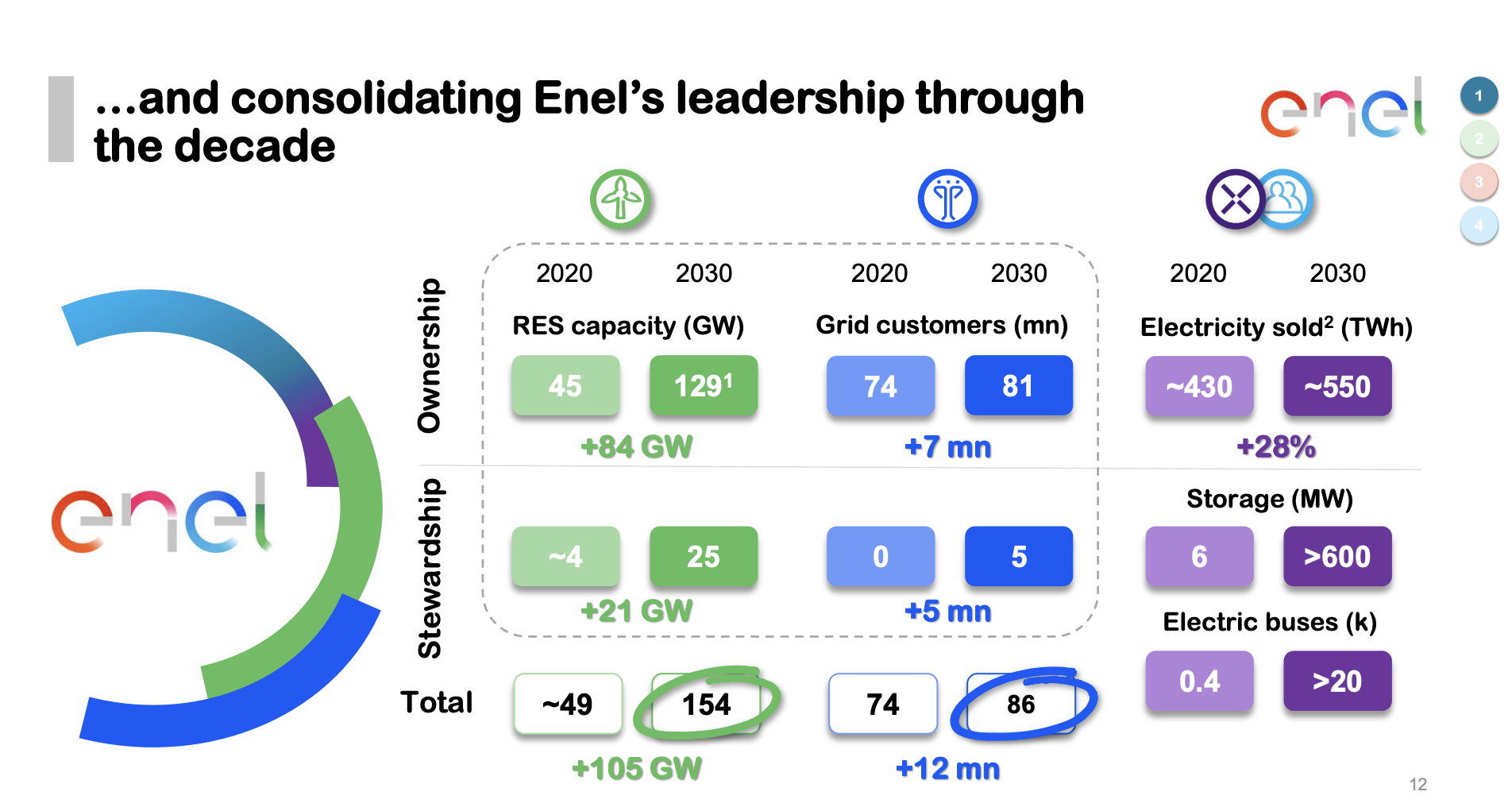

Being an integrated utility and one of the largest of its kind on earth, Enel owns all levels of the power supply chain - from generating its electricity to transmitting it, to distributing it. I've already described that in Enel you'll find a large part of LATAM operations - over 20% of operations and sales are found in Latin-American geographies.

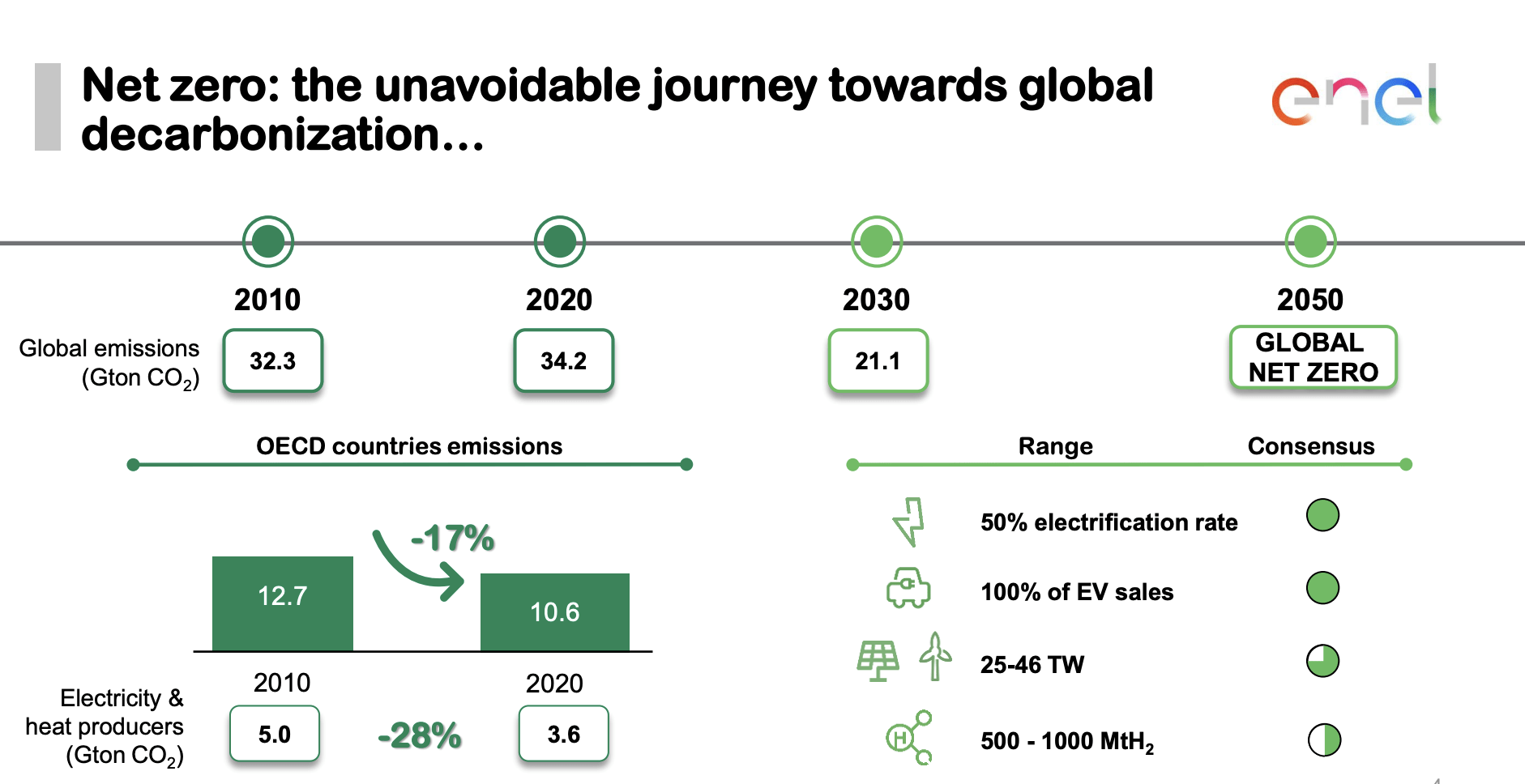

What's more, the company continues to be in the middle of an ongoing transformation to become more "renewable" as things go. Enel has a lot to do here - Much of its capacity is legacy, and while work has begun to change this, there is a lot left. The company's target is the ever-important "net zero".

{kind=link}

The company's CapEx plan is absolutely massive. Over €210B worth of capital is needed, €160B of which is going to ownership of new assets and only small portions are going into the maintenance of legacy. This will turn Enel into a renewable powerhouse starting in 2030 and beyond.

{kind=link}

The company's new assets will primarily be focused on what the company calls "tier 1 asset nations/countries", with geographies such as Italy, USA, Mexico, Brazil, Spain and others. The company wants to have the potential for an integrated presence before deploying significant amounts of capital into the countries.

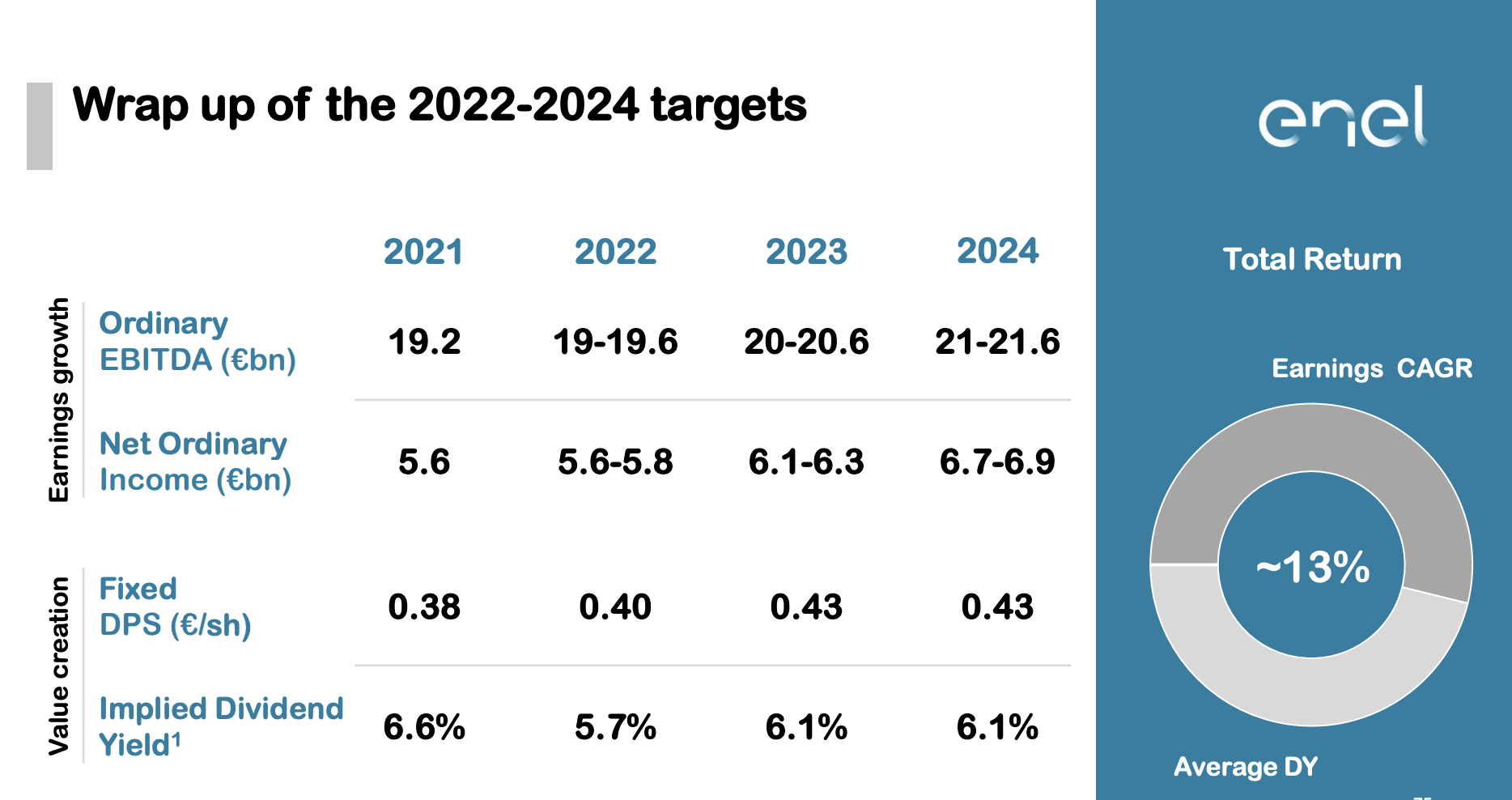

The expectation for this is to generate, in the long term, 5-7% CAGR in income and company EBITDA, increasing the dividend by 13% going forward. The dividend that the company pays is, therefore, very safe here. Take a look at how the company expects EBITDA to develop over the next few years.

{kind=link}

This is expected to come from a mix of networks, customers, and what the company coins as EPG, its generation segment which combines legacy and renewable generation. The company seeks to increase its sustainable financing source to over 70% by 2030, with the target of reducing the cost of debt to below 3% until 2024, from 3.7% today. The company has ample of liquidity available.

Based on the current dividend payout, the current yield on the planned 2022 dividend is 9.7%.

{kind=link}

For the 2023/2024 period, the yield now is closer to 10.5% - by investing in one of the largest utilities on earth. While there are forward risks, none of those risks make this company in any way uninvestable.

Enel still has coal assets and seeks to exit these by 2027-2030. Enel has the underlying customer base to push some of these changes, given that they have the world's largest customer base in the power market, with 95% of even its LATAM customers in Urban areas.

I believe there is enough fundamental upside to justify consideration for why these might materialize. The company doesn't have a high net debt/EBITDA - it's at 2.5-2.7X, stable - for now, even though this might grow going forward. Its renewable operations and ambitions are backed by every government where Enel is active.

That remains a high-level view of Enel. It's the world's largest (by some metrics) utility with absolutely solid core assets and legacy areas, mixed with about a quarter of LATAM. It shares similarities to other utility companies - so you know they have exposures to high CapEx demands, contracts, and WACC rates set by the governments. This means that their earnings are, in many ways, protected, but you also won't see them explode.

You won't see the dividend grow materially either - but I would consider it unlikely that it would drop or decline in opposition to its current plan. There's too high earnings visibility for the company to see this, as I consider things.

That means that the company is 9-10% "guaranteed yield" on an annual basis. I went through some of the fundamental risks to this thesis and to this company in my previous piece - but let's revisit some of the more relevant points:

- Some of the company's 2030E planned CapEx spending is specifically focused on LATAM - almost 38%. FX fluctuations/EM currency exposure will increase .

- The problems with renewables/electricity - things like storage solutions, through-cyclic grid stability, peak hours for things like solar capacities, and so forth.

Enel has both strong upsides and a few risks that should be accounted for. Its latest annual (2021) performance delivered a strong recent beat, tilting things in favor of the positive. However, much of this beat is due to legacy gas-related activities. Enel delivered record-high historical revenues, almost reaching the €90 billion mark, which is nearly a €30 billion YoY revenue increase.

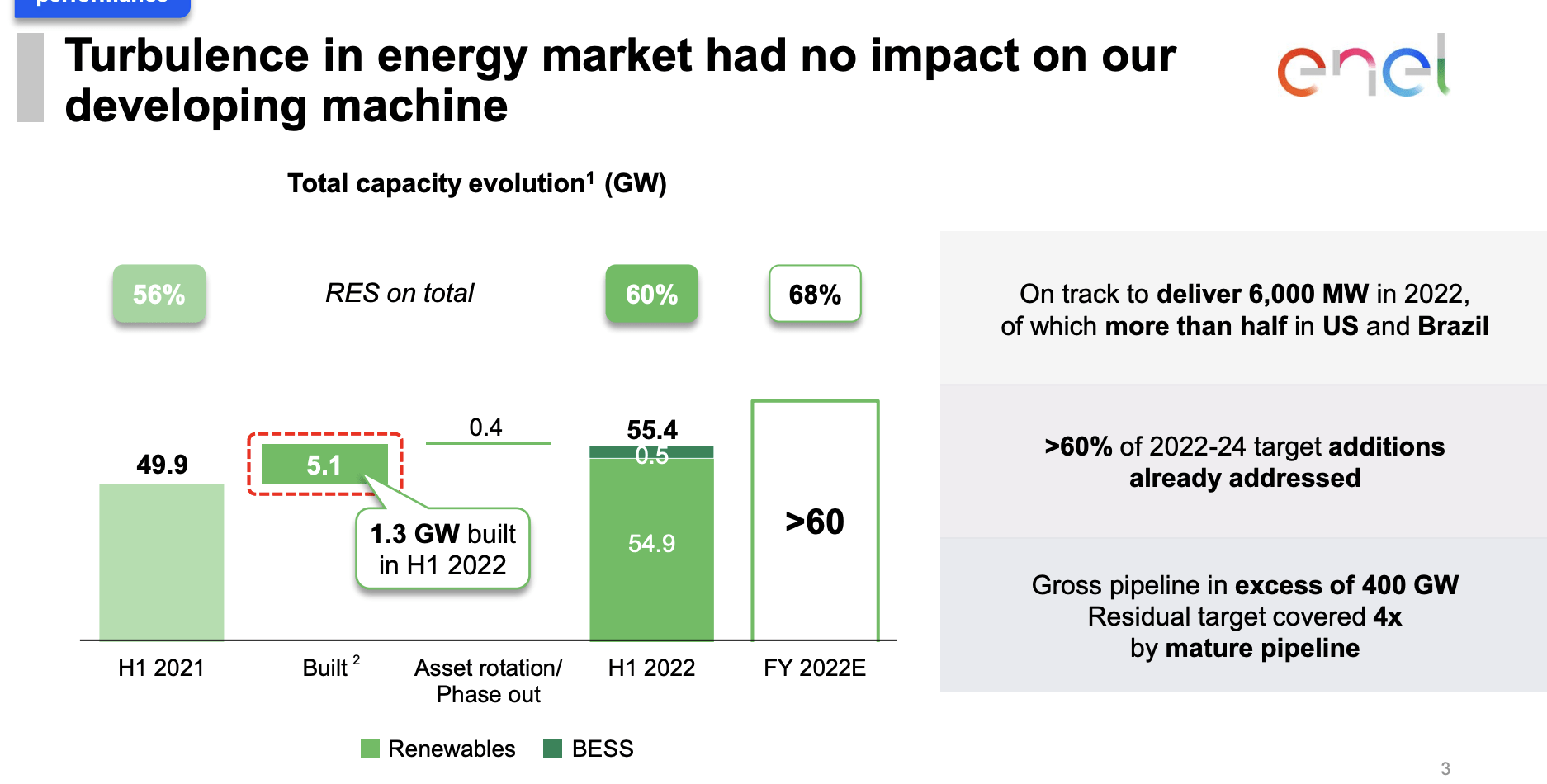

The recent 2Q22/1H22 results are "in line" with expectations. Russia has come to complicate the picture of the company, with exits ongoing, and streamlining of Latin America on track. Any volatility in the market is not impacting current plans for the company - which is of course very positive.

{kind=link}

Overall, the company's targets remain fully intact, and Enel reaffirmed 2022E guidance, with the dividend for the next year that implies close to 10% year being confirmed as of the latest results, with EBITDA of close to €20B.

The company had around a billion in turbulence impact, including current macro, but managed to almost completely offset it through a mix of networks, optimizations, stewardship, renewables, FX, and others.

Debt is growing - as planned, with CapEx being the main drag here as the company deployed nearly €6B during 6 months.

There is nothing impacting the fundamental safety here - which means that Enel continues to be purely a play on conservative utilities and the valuation you pay for those assets.

{kind=link}

So let's take a look.

Enel's Valuation

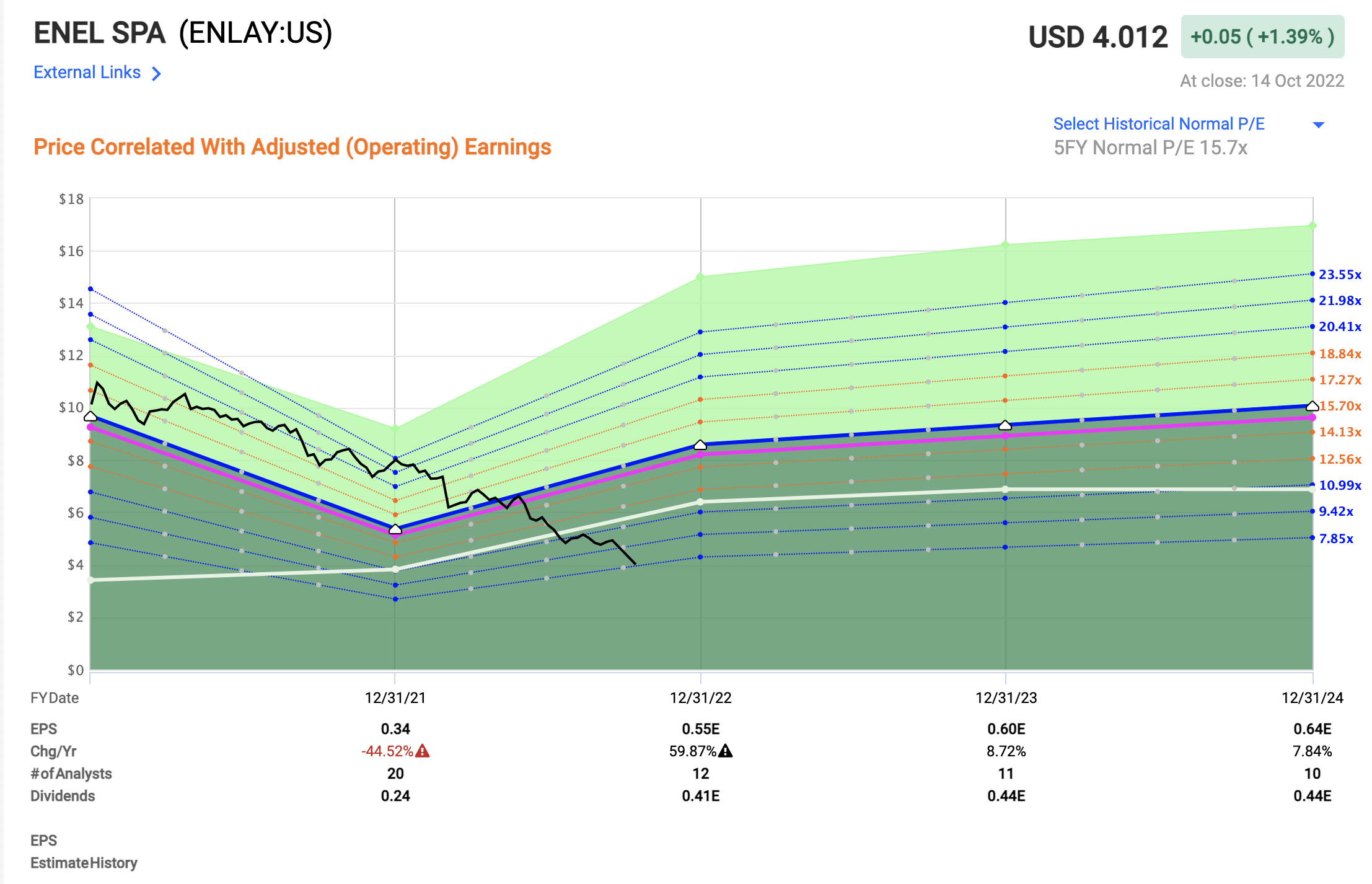

Enel's valuation in relation to its forecasts remains extremely favorable. For those familiar with the intricacies of F.A.S.T Graphs, I give you the following picture.

F.A.S.T graphs Enel (F.A.S.T graphs)

{kind=link}

The market is essentially completely ignoring what this company's assets offer in terms of safety, earnings visibility, and dividend payments. Even estimating only a conservative upside here, you get easy annualized rates of return of over 26% by just expecting a 10.6x forward P/E. A full normalization promises a RoR of 175% in less than 3 years, or 58% per year, in the case of a full 15x P/E, which is where the ENLAY ADR typically trades.

Valuing Utilities is a play of forecasting CapEx spending and acceleration together with its income generation/cash flow. Many analysts use a premium to forecast the company due to the massive growth potential for Enel in the next 8 years.

I will never apply premiums to Enel exactly for the risks involved in this, but I also don't want to downplay Enel's potential simply because it involves things like Mexico and Brazil. From a peer perspective, which I view as one of the best ways to view Enel due to the prevalence of integrated utilities in Europe, the company is being discounted heavily. With public comps such as Iberdrola ( OTCPK:IBDRY ), E.ON, Verbund ( OTCPK:OEZVY ), RWE ( RWEOY), National Grid ( NGG ), and Engie ( OTCPK:ENGIY ), there's no shortage of comparisons, and the comparison is very clear.

Enel was massively undervalued even at almost twice the company's current price, and it's now even more undervalued. At a current multiple of 11.5X to P/E and 7.27X to EBITDA, the company is more than 90% undervalued to the averages, with some comparisons like RWE trading over 18x P/E.

Any way you look at it, I believe there's at the very least baseline potential for Enel. I view utilities as bond-like safety proxies with good yields. if bought cheaply, as I did with E.ON, you can also gain more than 60-70% annualized RoR from normalization. Again, as I did with E.ON, less than 12 months back.

My previous PT for the company's native was around €8.8/share. I will be the first to adjust my targets if the company doesn't justify them, but at this time, I'm not shifting it an inch. Analysts now have targets starting at €3.5 and going all the way to almost €11/share. A wide range with a 21 analyst average of around €7.8, with 16 of them at a "BUY" or equivalent recommendation for Enel, and an upside to 87% to the current target.

My PT remains at €8.8 - I view Enel as the sort of income-generating utility I want to own for its 10%+ yield on a forward basis, while at the same time having the potential to bounce to a massive 200-300% RoR if it normalizes to €7-€9/share.

Unlikely? less than 2 years ago the company was close to that €9/share, and I see it likely that the company's future generation justifies such a premium.

Thesis

My plans for holding Enel are simple.

Buy it cheap - and hold it until/if it gets overvalued - which it can. Cash in on an inflation-beating dividend until then.

It's not the fanciest plan - but it's certainly a "safe" one, as trends in today's market go.

There are risks for Enel, but these risks pale in comparison to the through-cyclic stability and dividend safety of this legacy utility with exposures throughout Italy and LATAM.

My strategy for this one is as simple as it was with E.ON, and that's my idea for interested investors as well.

Buy cheap. Hold.

Remember the relevant ADR here - ENLAY. You can also choose to invest in specific Enel business activities - this is not what that article is about, and I haven't gone deep enough to consider individual segments like the Americas, Chile, or Russia as their own investments. This thesis is for Enel as a whole.

The ADR is unsponsored and somewhat thinly traded - so a native approach with access to either the Milan ticker or the German-traded ENL ticker is a better bet for longer-term ownership. Italian dividend withholding taxes apply for all investments, even if you buy the German ticker, so be sure to discount for this if you invest. For me, I get 99% of this withholding tax returned, so this is a superb investment for me.

It could be for you as well - so take a look and see what you think!

For further details see:

Enel: Attractive With A Solid Utility Upside