ENLAY - Enel: Growth Target Too Ambitious (Rating Downgrade)

2023-06-25 08:00:00 ET

Summary

- After several years of massive capacity expansion, Enel has to dispose assets to reduce net debt.

- Secondly, capex is reduced in spite of rising development costs.

- Consequently, the targets of the company seem too ambitious.

- Political interference and a change in management add further uncertainty to Enel's future strategy and performance.

- All this is undermining the business case for Enel’s transition, consider it a 'Hold'.

Previously covering Enel ( ENLAY ) a buy recommendation was given in spite of the significant debt burden. Also, the rising costs for development of renewable energy generation capacity was highlighted as a point of attention. Currently, the upward trajectory of costs is undermining the business case for Enel's transition. As a consequence, I rate Enel as 'Hold'.

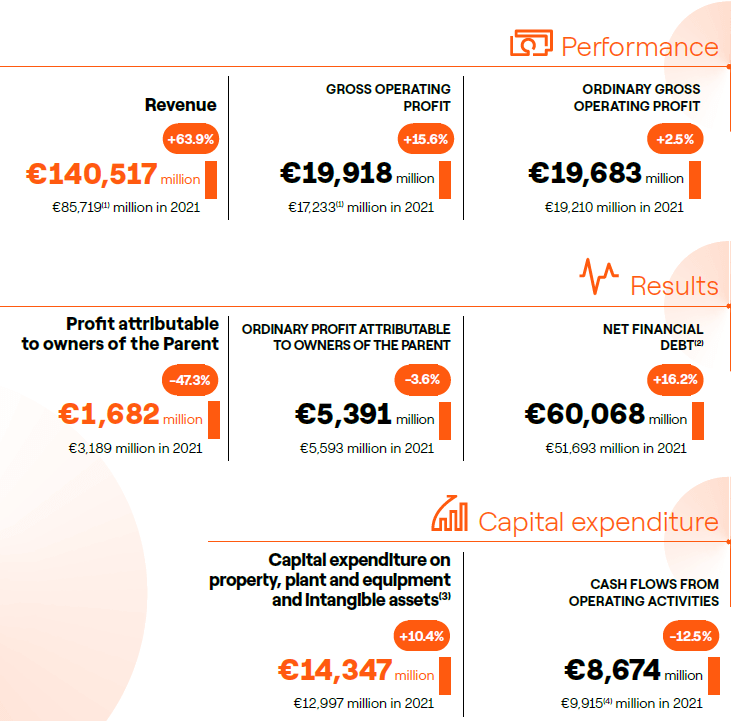

FY22 results

The FY22 results of Enel are summarized in figure 1. The performance of the company showed some impressive numbers such as an approximately 64% gain in revenues. However, actual results declined with profit plummeting by nearly 50% and debt rising by a substantial €8.5Bn.

Figure 1 - FY22 results (AR FY22; enel.com)

{kind=link}

Even though less profit was made against significantly higher revenues, the company increased capital expenditures and distributed €4.9Bn in dividends. The reason being Enel has committed itself to the energy transition, requiring massive investments, as well as a progressive dividend policy.

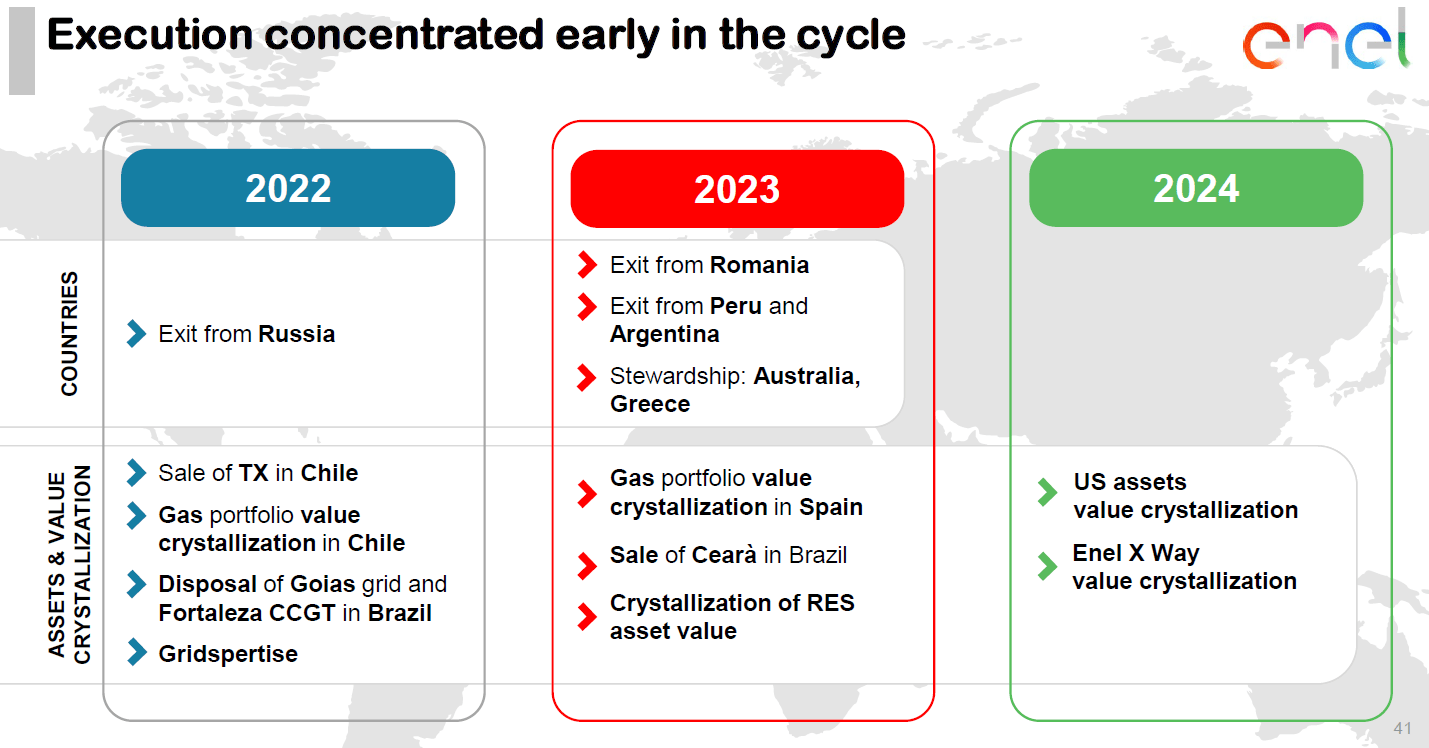

Debt in focus

As argued, debt development is a point of focus for Enel. Management was well aware and consequently announced the intention to focus on six geographies and dispose of assets outside of these markets, see figure 2.

Figure 2 - Planned asset disposal (CMD22; enel.com)

{kind=link}

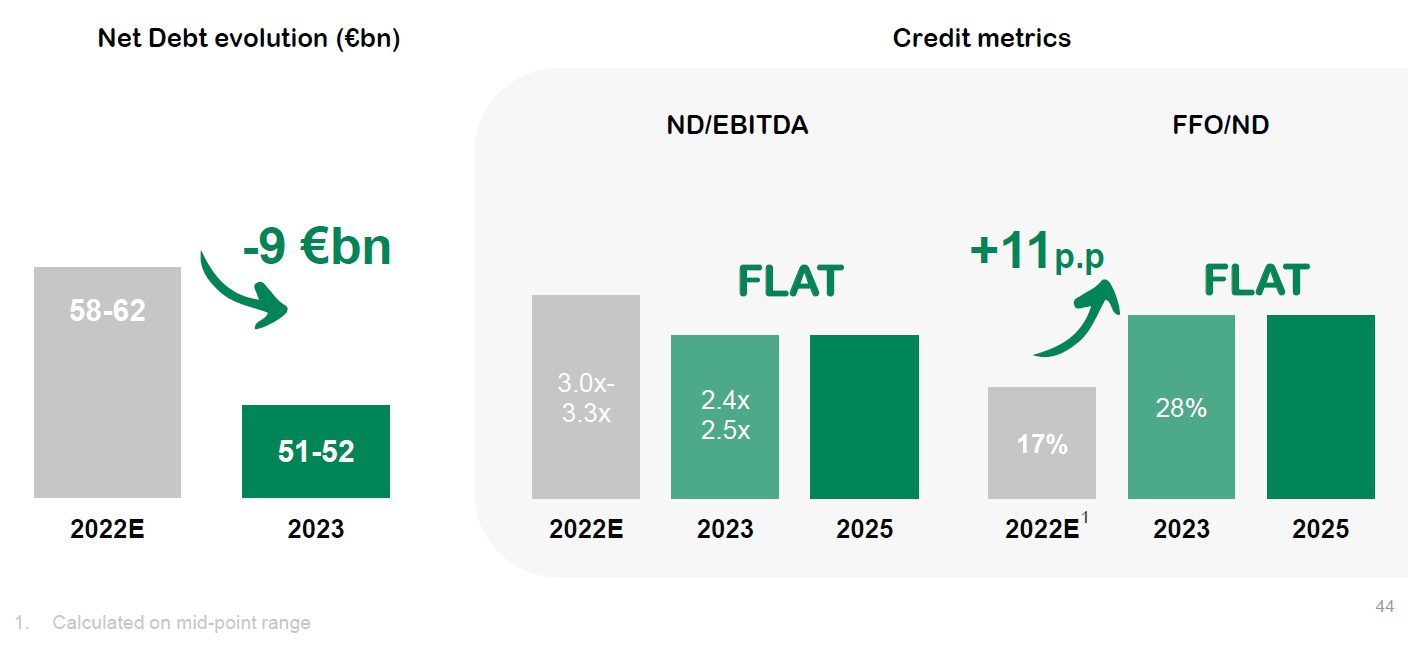

What's more, after several years of massive capacity expansion, combined with the associated detrimental effect on debt, the company will now take a more disciplined approach, see figure 3.

Figure 3 - Debt metrics (CMD22; enel.com)

{kind=link}

Management has leveraged the company during times of low interest rates, and now takes decisive action to prudently manage the desired capacity expansion in renewables versus net debt. One of the result thereof is the attention for the net-debt-to-EBITDA ratio which management intends to keep constant. This implies the growth rate will potentially reduce as EBITDA expansion needs to keep up with growth of net debt.

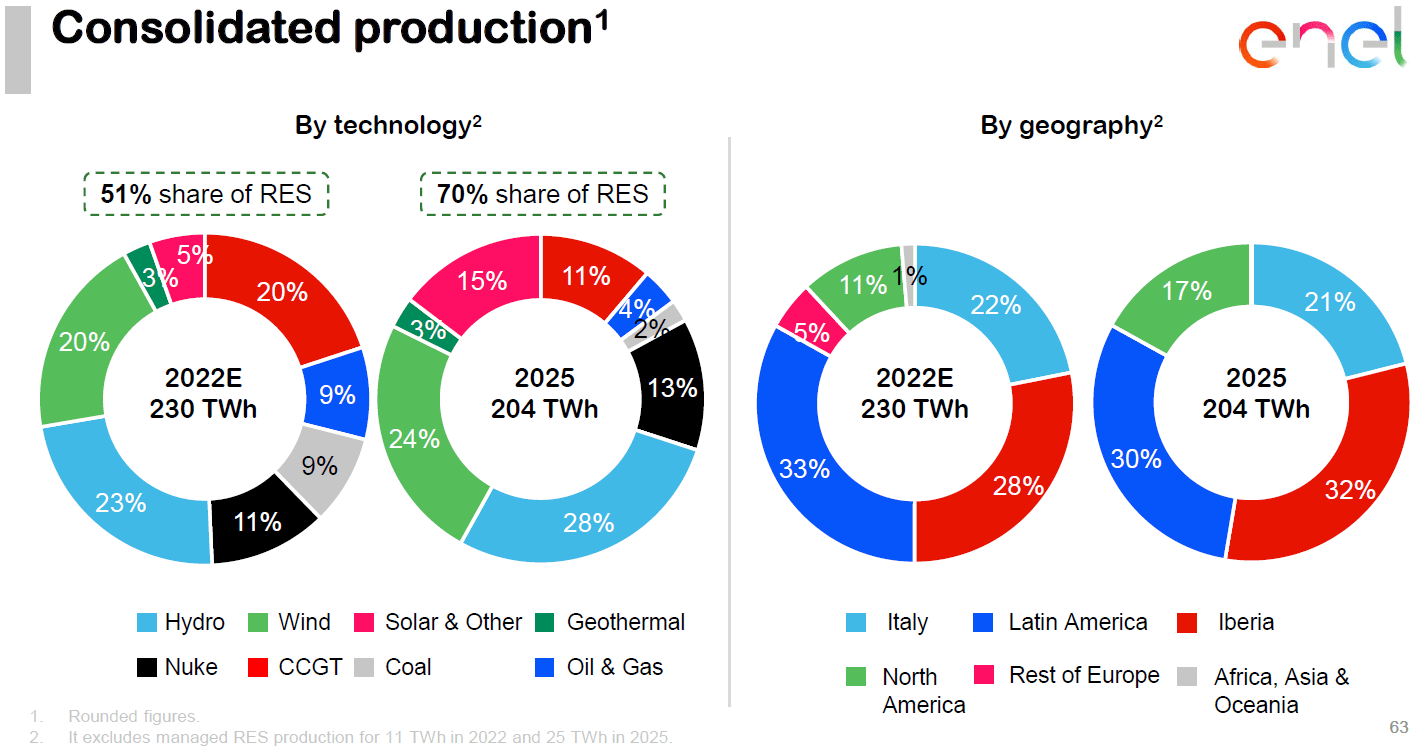

Another implication of the transition is that total generation capacity will actually be sacrificed over the short term. From the 2022 Capital Markets Day presentation follows the capacity will reduce as the company phases out fossil powered generation, see figure 4.

Figure 4 - Production development until 2025 (CMD22; enel.com)

{kind=link}

Clearly, fossil fueled generation capacity will be phased out in favor of renewable options. Renewable production capacity of which part still needs to be build.

Development costs

With Enel, I always keep a close eye on the evolution of the renewable development costs. The first reason to do so stems from the fact renewable technology is still maturing. While solar and wind energy, for example, are both accepted forms of energy generation, there is ample room for improvement of both technologies.

Yield compression

Secondly, development costs matter as ever more companies are moving into the renewables space which, according market theory, should drive up prices as demand rises. In addition to driving up costs, increased competition means developers have to win licenses against ever lower sale prices.

For offshore wind farms, for example, the developer offering the lowest cost per megawatt hour will secure a license. Despite rising development costs and falling sale prices, the upside is further limited, the Guardian summarised this neatly as follows:

Offshore windfarm operators will sell power for as little as £37.35 per megawatt hour, 5.8% below the lowest bid in the most recent auction in 2019.

The "contracts for difference" guarantee wind-power companies fixed prices to sell electricity for the following 15 years. If the market price falls below the contract price, the government subsidises the difference. If the market is higher, the companies pay money back to the government.

Since wholesale energy prices began to rocket last year, windfarms have begun paying back money to the government.

While onshore renewable generation will not remain exempt from these mechanisms, the initial investment are much lower, the technology has matured further compared to offshore and consequently the risk profile is superior. Enel management is fully aware of this and so far has not ventured into uncharted waters, it has kept focus on onshore renewable generation. From an investor point of view, this makes sense.

Cost decline stalling

Even so, the company is experiencing rising costs for renewable development. Table 1 shows the evolution of the capex costs per gigawatt ((GW)) installed. While these costs trended downward over the last years, in 2022 this trend reversed and the costs per gigawatt rose by nearly 13%.

Table 1 - Asset development capex for Enel's Green Power (EGP) Business Line (FY22 results presentation; enel.com)

As the development of energy assets is generally a long term endeavor, it may be expected the costs will rise further in 2023 as the 'cheap' projects will disappear from the pipeline. This raises the question how Enel will fund its expansion plans. As noted before :

Although Enel is managing the development costs well, it is anything but certain the forecasted capacity will be built. The downward revision for the goal of the Infrastructure and Network business line can also happen for the Green Power division. For example, during the H1 2021 presentation the company planned to build 5.8GW capacity, but this number was revised downward to 5.1GW when the Capital Markets Day was held in November of the same year.

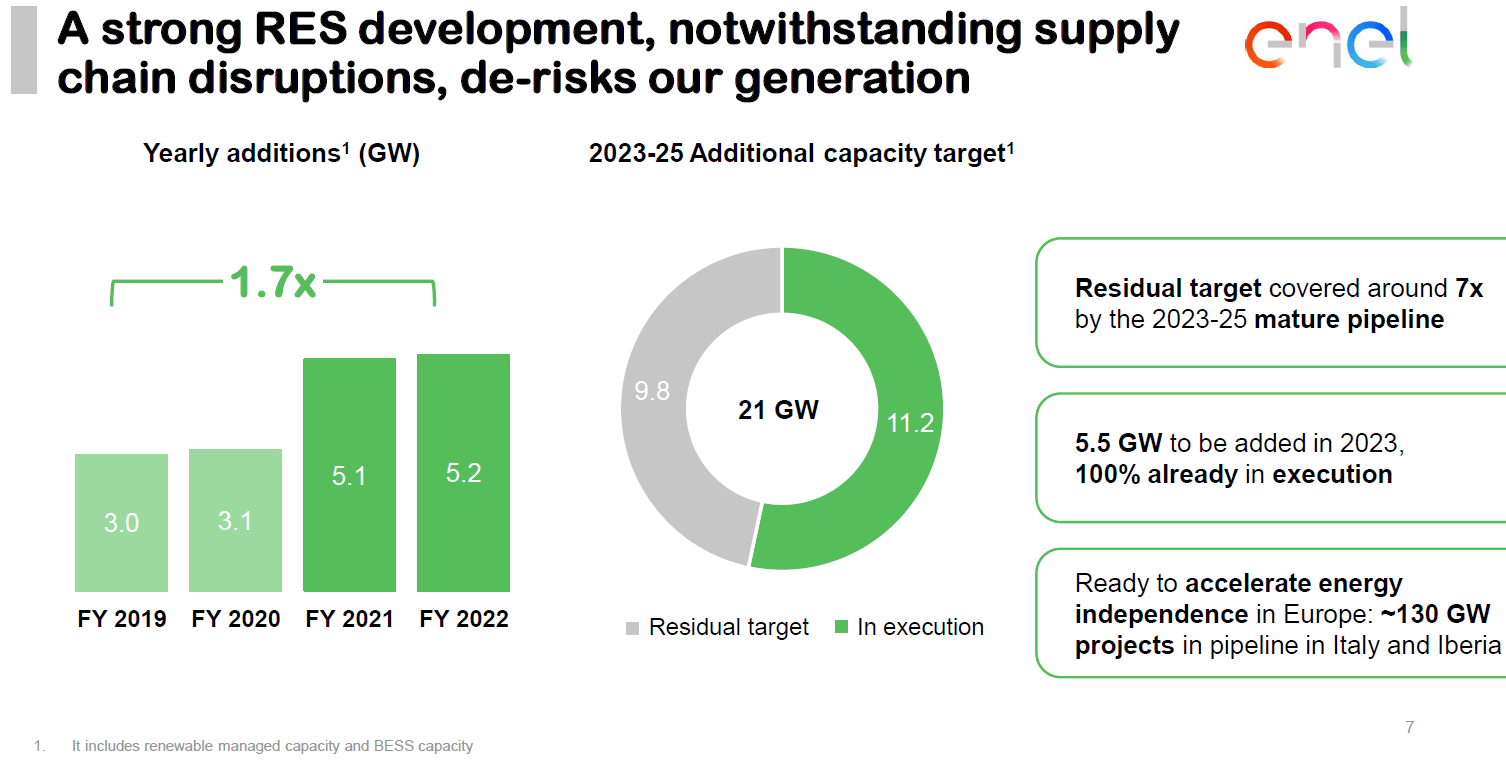

Judging by the numbers, it appears this is exactly what will happen; a downward revision of the for the goal of the Green Power division. The numbers in figure 5 show renewable capacity expansion remained flat in 2022, and for this year an expected 5.5 GW will be brought online.

Figure 5 - Renewable development (FY22 results presentation; enel.com)

{kind=link}

This shows Enel is lagging behind its own targets of achieving an annual capacity expansion of 15GW by 2030, as discussed here. Moreover, it is hard to imagine a renewed acceleration of capacity expansion as it was demonstrated development costs are rising, while management intends to keep a lid on net debt. Given the net-debt-to-EBITDA ratio is also expected to remain flat, either net debt has to reduce significantly, or EBITDA must grow.

EBITDA target too ambitious

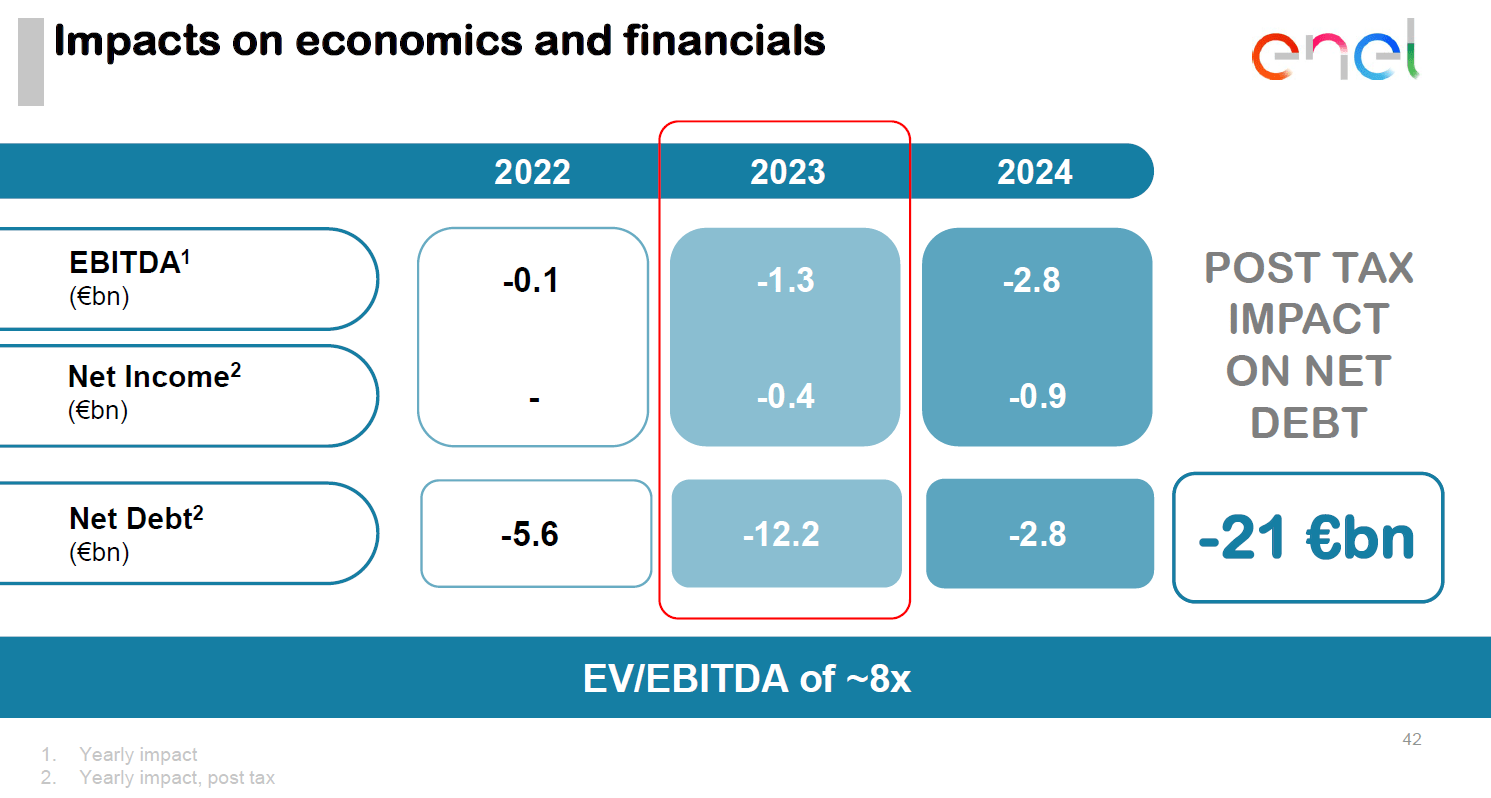

As it stands, however, the disposal of assets is expected to lower EBITDA by approximately €4.2Bn to achieve a €21Bn debt reduction, see figure 6.

Figure 6 - Effect of disposals on net debt and EBITDA development (CMD22; enel.com)

{kind=link}

Taking the FY22 EBITDA of €19.7Bn as a baseline, it is hard to understand how the company intends to 'lose' a combined €4.1Bn in EBITDA during 2023 and 2024, but still achieve earnings of at least €21.4Bn in 2024, see figure 7.

Figure 7 - Financial targets till 2025 (AR FY22; enel.com)

{kind=link}

After all, EBITDA will need to grow by 7% in 2023, and subsequently by more than 16% in 2024 to merely offset the decline in earnings resulting from the disposals.

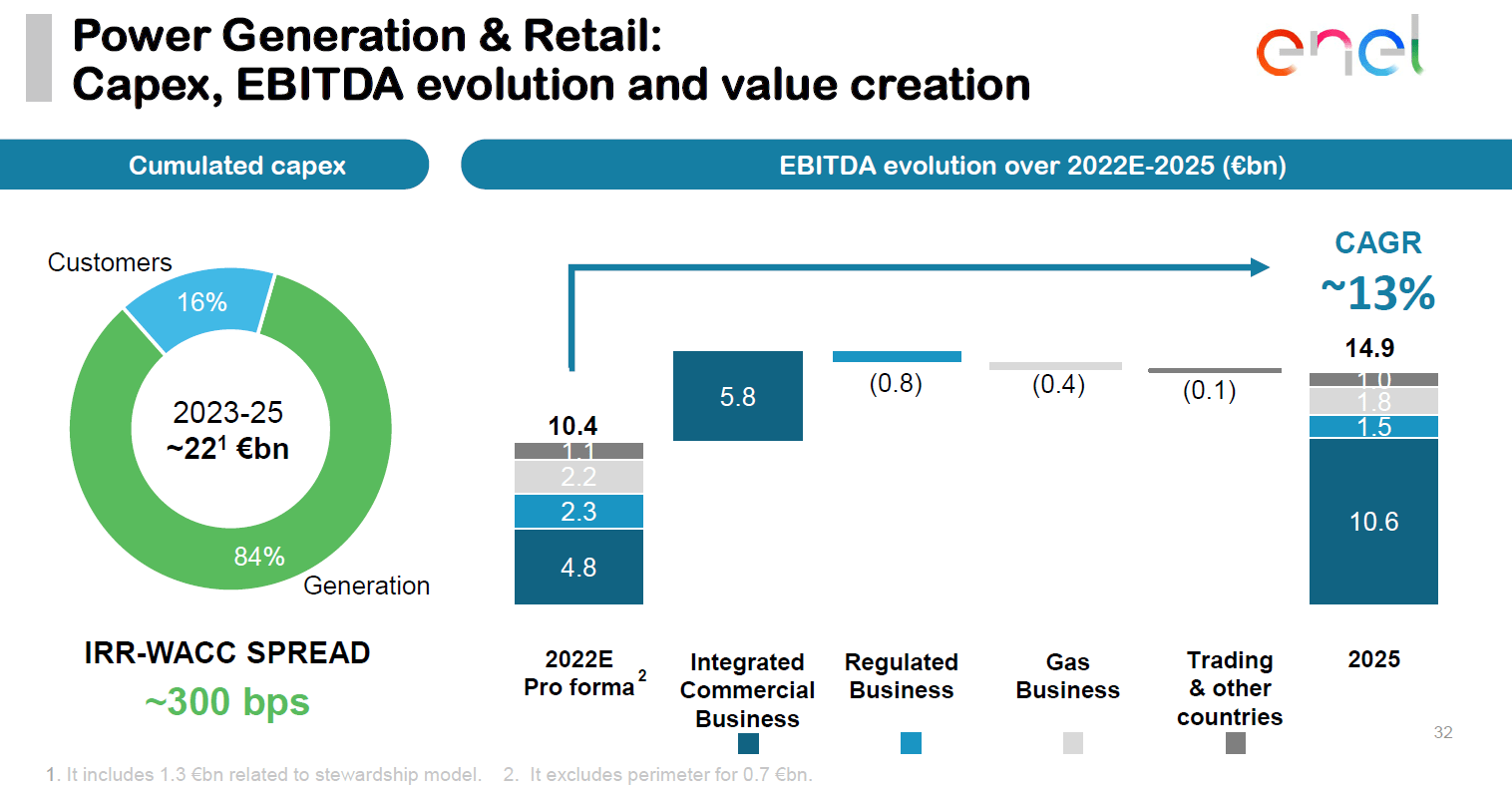

Without the disposals, the forecasted compound annual growth rate of EBITDA should reach 4.1% to meet the lower-bound target for 2025. Including the disposals, the CAGR must reach at least 12.5% to meet the envisaged targets. This adds up to the forecast CFO Alberto de Paoli shared at the Capital Markets Day in November 2022, see figure 8.

Figure 8 - EBITDA evolution Power Generation and Retail (CMD22; enel.com)

{kind=link}

The numbers so far line up, but it nevertheless seems hard to achieve this target given the CAGR of EBITDA was only 5% over the period running from 2018 to 2022. Mind I have chosen 2018 as the starting point of this calculation as this results in the most favorable growth rate. In other words, the company needs to achieve a growth rate which is nearly triple the value it has posted over the last four years.

This could potentially be possible if the company significantly supercharges the earnings driver; Renewables. As demonstrated before, this implied annual capex would need to grow by €1Bn annually to a level of €19Bn per annum.

Chances of this happening are small as management shared the intent to spend €37Bn in capex until 2025. This means capex will be reduced to €12.3Bn annually on average (2022: €14.3Bn) for the period 2023-2025. Tie this to the fact the development costs went up, and one can only conclude the EBITDA target seems too ambitious.

This in turn implies net debt can't evolve as planned, as management intends to keep the net debt-to-EBITDA ratio constant at a level of 2.5x. In the end, something's got to give. And it did.

Politics

In May, it was announced CEO Francesco Starace was replaced by Flavio Cattaneo. This outcome was a big win for the Italian Treasury as they were at loggerheads with institutional and private investors about the influence exerted by the government over a listed company. As noted by Reuters:

Outgoing CEO Francesco Starace has been in charge since 2014 but failed to win favour with the inner circle of Prime Minister Giorgia Meloni's right-wing government.

The Treasury has told investors it wanted Enel to continue to play a leading role in renewable energies while accelerating the disposal of assets and maintaining its dividend policy, two sources had told Reuters.

The problem here is that the Italian government, headed by prime minister Meloni, is interfering with the way the business is run. It remains to be seen what the new management team will do, whether they will continue as planned or redraft the strategy, but it is questionable to which extent it can act independently.

In this context, it should be noted prime minister Meloni has committed herself to alleviate the burden of energy prices on Italian households. To do so, however, the government has limited room to maneuver as Italy still wants to be eligible to receive the remainder of its share from the post-pandemic recovery fund. By replacing a large part of the management team, the fear that politicians will use Enel as a mean to achieve political gains seems to be materializing:

Several shareholders had signalled to Rome that they did not want an abrupt change in Enel's strategy, in particular a drastic reduction in the group's international footprint. Some investors fear that Enel may come under government pressure to focus on its domestic market.

Conclusion

After several years of massive capacity expansion combined with the associated detrimental effect on debt, the company will now take a more disciplined approach going forward. Nevertheless, total generation capacity will be sacrificed over the short term while earnings are forecasted to improve.

This target must be achieved in an environment of rising development costs and falling sale prices. Therefore, the planned capacity expansion potentially needs to be revised downward. A first sign is the reduction in capex for the coming years. Tie this to the fact the development costs went up, and one can only conclude the EBITDA target seems too ambitious.

As the upward trajectory of costs is undermining the business case for Enel's transition and political interference creates uncertainty, it's a 'Hold'.

For further details see:

Enel: Growth Target Too Ambitious (Rating Downgrade)