ENLAY - Enel Remains My Favorite Renewable Energy Investment

2023-10-10 07:44:19 ET

Summary

- Enel is my favorite renewable energy investment.

- The company has an ambitious plan to increase its share of renewable energy to 75% and deleverage its balance sheet.

- So far, they're on track to deliver double-digit returns.

Dear readers,

The renewable energy space is vast and complicated, making it difficult for investors to pick the right companies for their own unique circumstances.

I've recently published an article on many investor's favorite - Brookfield Renewable Partners (BEP) where I argued that this YieldCo's upside is significantly limited by the fees it pays to Brookfield Asset Management (BAM).

Since then, BEP shares have underperformed significantly, as another renewable energy YieldCo - NextEra Energy Partners (NEP) has slashed its growth guidance in half, leading to fears that the sector might come under pressure.

These developments left many investors wondering which stock to buy to get renewable energy exposure. Today I want to present my favorite, an Italian-based utility company with global operations - Enel (ENLAY).

Last time I wrote about Enel was right after Q1 earnings. The company had made significant progress towards fulfilling its ambitious 2022-2025 plan and was positioned to deliver 20%+ annual returns using relatively conservative assumptions. Since then, the company has released its Q2 earnings and the price has dropped by about 10%.

Note: Throughout the article, I'll be referring to the EUR-denominated native shares trading under the ticker ENEL on the Milan stock exchange.

Enel Overview

Enel is a global fully integrated utility company, which means that it operates throughout the electricity supply chain from power generation to distribution.

It is Italian-based and has most of its operations in its home country (30%), followed by Latin America (28%), Spain (24%), the US (8%) and a smaller presence in the rest of Europe and Mexico.

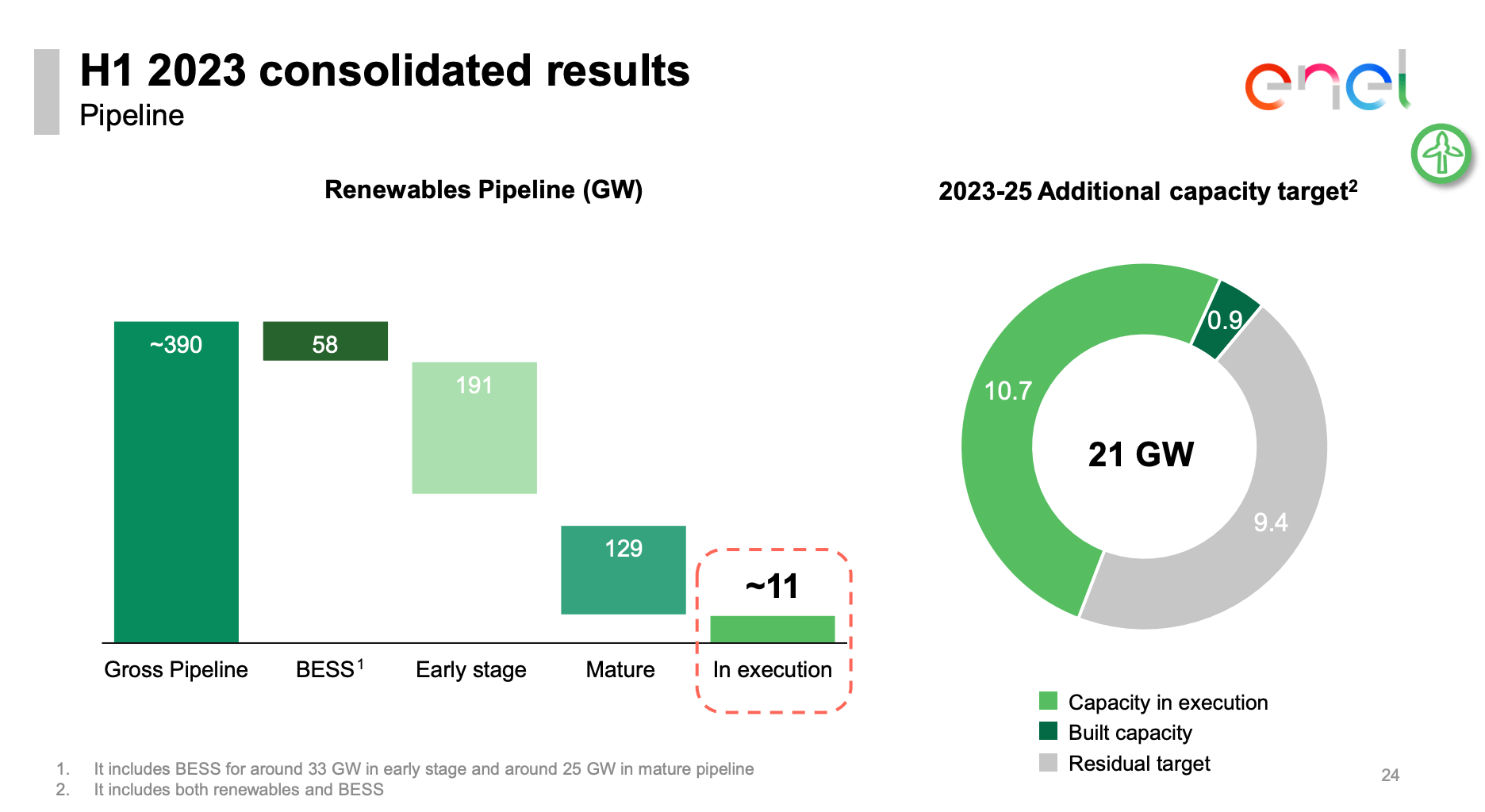

Currently, Enel produces about 55% of their energy from renewables, mainly from hydro (25%) and wind (20%), but their goal is to increase this to 75% by 2025. The company currently has 11 GW of capacity under construction and is therefore well on its way to hitting the 75% target with only 9.4 GW left.

Although little (no) progress has been made on this front over the second quarter, I see a clear way towards fulfilling this target, especially with Enel's vast pipeline which has 129 GW of projects in the "mature" stage of development (i.e., ready to begin construction).

{kind=link}

Beyond increasing the share of renewables, the company has very actively (and successfully) tried to divest from conventional energy generation and assets in Tier-2 markets to fully focus on their Core markets. These are Italy, Spain, the US, Brazil, Chile, and Colombia.

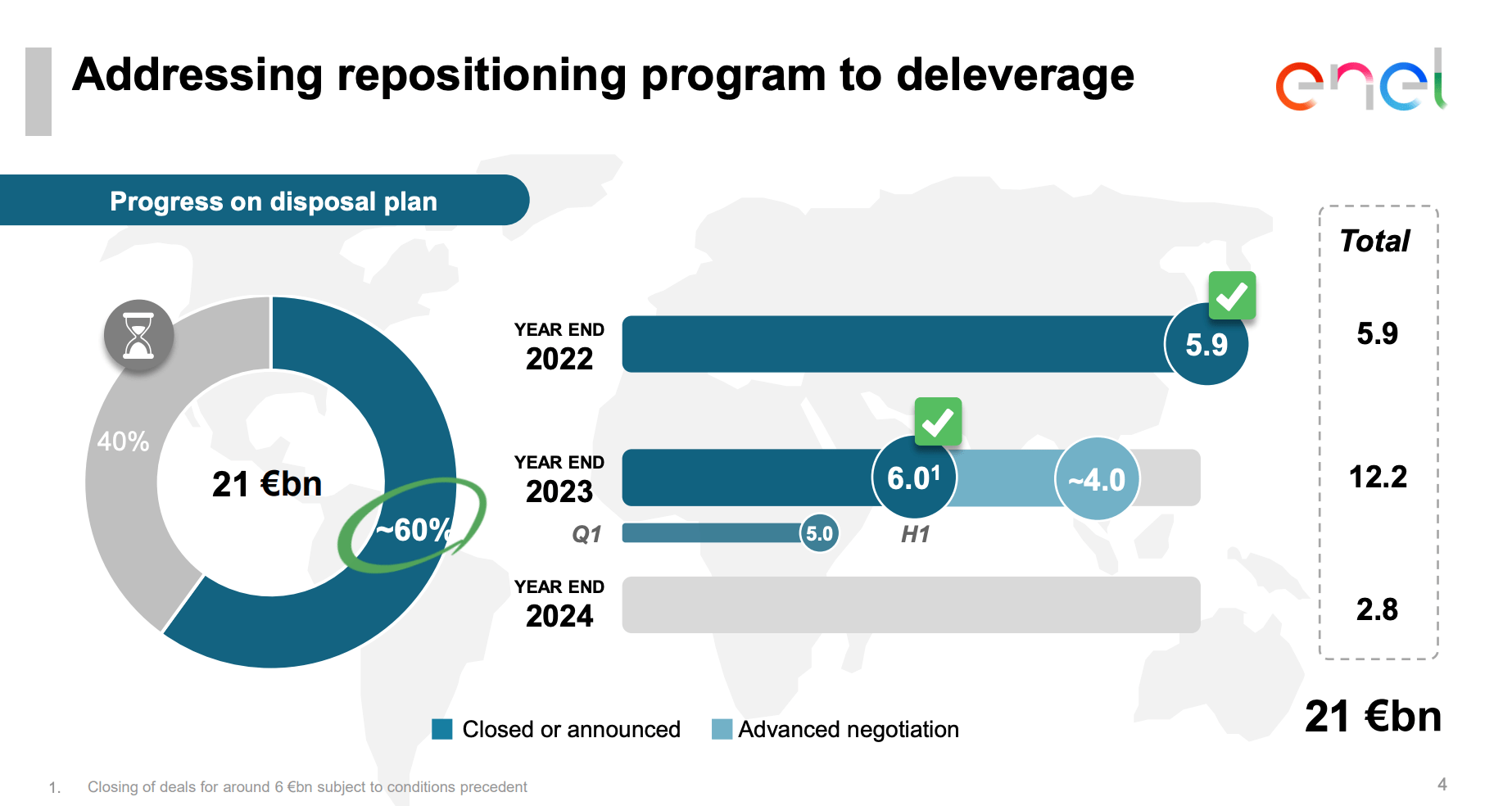

As part of the strategic plan set for 2022, management announced a plan to dispose of EUR 21 Billion of non-core assets and use the proceeds to lower their (high) debt load. So far, Enel is on track to meet the target, with EUR 5.9 Billion of disposals last year, EUR 6 Billion year to date and EUR 4 Billion under advanced negotiations. Importantly, the disposals closed year to date were priced at relatively high average prices of 8x EV/EBITDA.

{kind=link}

Following really significant disposals in Romania, Peru and Argentina last quarter, sales have slowed in Q2 with only EUR 1 Billion of additional disposals. These came mainly from the sale of assets in Chile (EUR 500 Million) and a partnership on their Australian operations with a major Japanese group involved in oil extraction and processing.

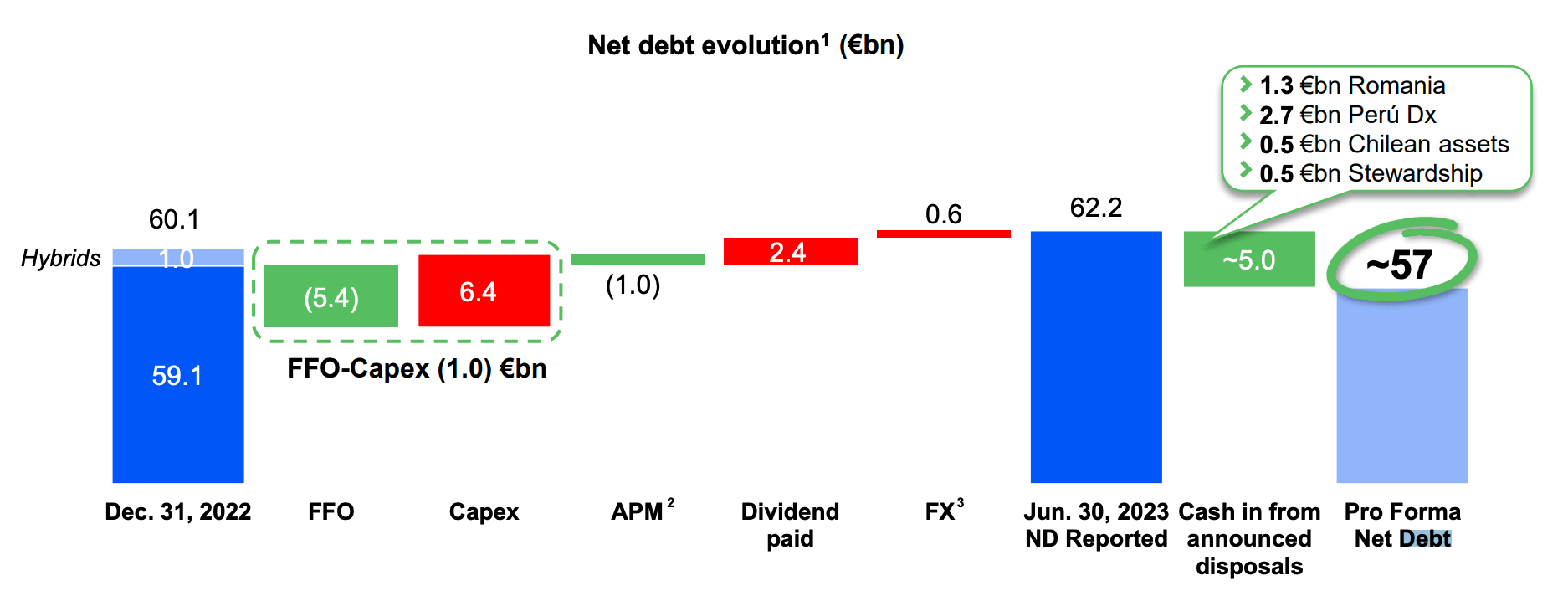

As planned, Enel has been using the sale proceeds to lower their debt, which currently stands at EUR 57 Billion (adjusted for proceeds from disposals). So far, the company has managed to lower net debt/EBITDA from 3.1x in Q4 2022 to 2.7x by Q2 2023. And guidance for year-end calls for a further decrease to 2.4-2.5x as net debt is expected to drop to EUR 51-52 Billion and EBITDA is expected to rise.

{kind=link}

A higher share of renewables and a portfolio focused on core markets is nice, but at the end of the day everything comes to Enel's ability to deliver on their earnings growth target of 9-10% per year.

During Q2, ordinary EBITDA has increased by 29% to EUR 10.7 Billion and net income has reached EUR 3.3 Billion. More importantly, management has confirmed their 2023 full year guidance for EBITDA of EUR 20.4-21 Billion and for net income of EUR 6.1-6.3 Billion.

Valuation

Similarly to other renewable energy YieldCos, Enel pays a high dividend of 7.6% (EUR 0.43 per share).

Moreover, the stock remains relatively cheap at a P/E of 9.1x and a forward EV/EBITDA of 5.5x. For comparison, Enel's historical 10-year average stands at a P/E of 13x and its most relevant peer, the Spanish-based Iberdrola ( IBDSF ) trades at a P/E of 13.6x and a forward EV/EBITDA of 7.5x.

I've previously set my 2025 price target at EUR 8 per share. This assumed 6% earnings growth in 2024 and 2025 and an exit multiple of 11.5x. With strong earnings growth results in Q2, I see no reason to move my target and continue to expect high double-digit returns from Enel.

In particular, I expect:

- 7.6% dividend yield (likely to grow around 4-5% per year)

- 6% earnings growth (below management's target of 9-10%)

- a P/E multiple of 11.5x (below historical average and Iberdrola)

Significant insider buying from the new CEO also helps. He has only been with the company for a couple of months and has already accumulated 1.5 Million shares worth about EUR 9 Million.

Risks

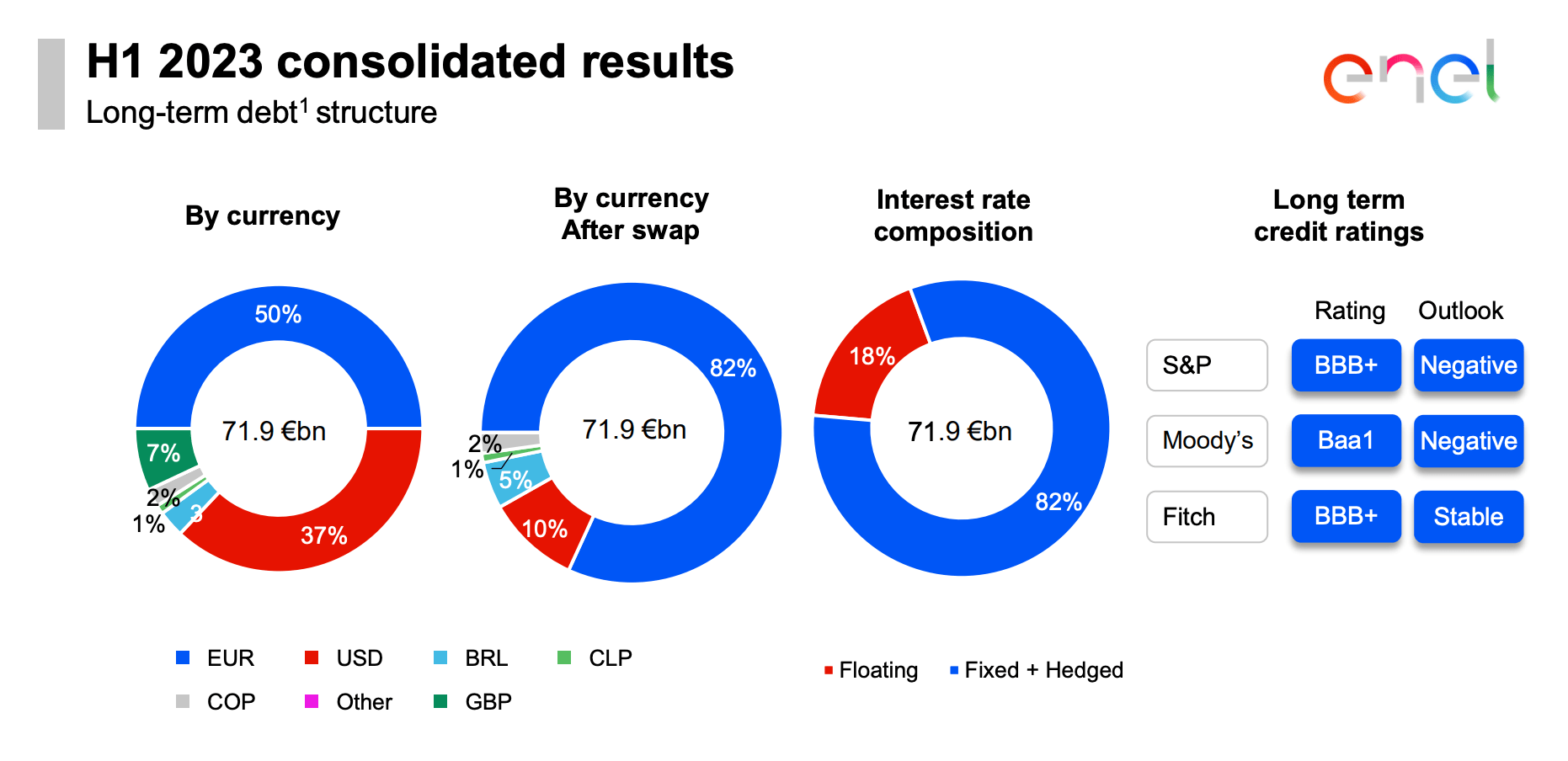

One of the biggest risks for Enel remains their high level of debt. It is not all negative, the company has a BBB+ rating and 82% of the debt is fixed-rate. Nonetheless, a high interest rate environment translates into higher interest expense, which in turn results in lower earnings. I like the way management is taking with their debt-reduction plan, but leverage is definitely one thing to keep an eye on here.

{kind=link}

For further details see:

Enel Remains My Favorite Renewable Energy Investment