ENLAY - Enel: Still One Of The Better Utility Investments Out There

2023-10-09 11:07:20 ET

Summary

- Enel has seen significant growth, with a 47% increase in the past 12 months, making it an attractive investment opportunity.

- The company is an integrated utility and one of the largest power companies globally, with strong regulatory relationships and frameworks.

- Enel's financials are solid, with a double-digit increase in EBITDA and a sustainable dividend yield of 7.67%.

Dear readers/followers,

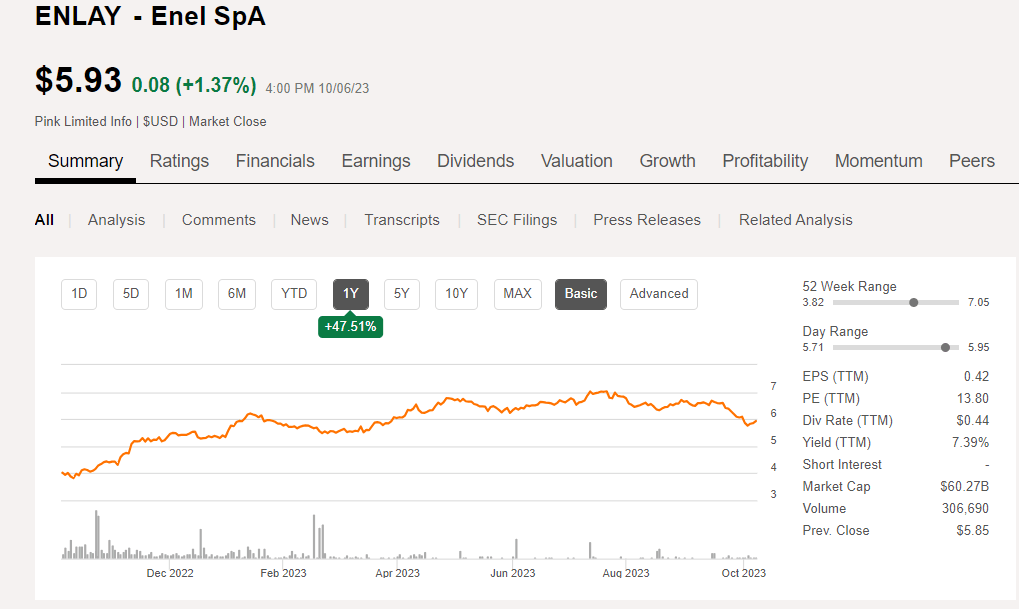

Enel ( ENLAY ) remains one of my favorite utility investments for the past two years. I'm up significantly even with the latest few weeks of decline, and over the past 12 months, the company is up a whopping 47%+ , which makes this an opportunity that more investors really should have bought into.

Enel SeekingAlpha (Seeking Alpha)

{kind=link}

In times like this, I often check myself to see if I could have been more clear, more positive or more convincing about the prospects of a company or a specific investment. In this case, I don't think I honestly could have been. I dug deep, and I was clear that this was going to be my largest utility investment. It still is. Now, with the growth, over 4.5% of my total private portfolio is Enel - and to be clear with you, I don't think the upside is "over" or finished yet.

Enel is an incredibly attractive investment for a multitude of reasons. In this article, I'm revisiting not only the company, but my reasons for going "deep" into this company, and remaining very invested as well.

Let's get going and let me show you what I think the company has going for it here.

Enel - Plenty of upside remains here, despite excellent RoR

So, my RoR since my last article is something I do believe speaks for itself. It, at one point, was close to 50% total RoR.

Seeking Alpha Enel RoR (Seeking Alpha)

And obviously, now that the company is up almost 43% inclusive of everything, it's less appealing than it was at the lower price with the higher yield. Because not much has changed in terms of the company's fundamentals and the visibility of the results. All of the trends and things I am about to show you or speak to you about are things that I was able to at least consider somewhat realistic less than a year ago when I last wrote on this business publicly.

Enel remains one of the world's most significant utilities, not just in its sector but in any sector. It has dozens of billions of euros in revenues and is one of the top 100 largest companies on earth based on annual revenues. It's also one of the largest power companies on earth, and I encourage you to look either at the native listing on the Milan stock exchange, ENEL, or the German-listed ticker if you're interested in investing.

As before, Enel is something I see primarily as an income opportunity with a capital appreciation component. And in this case, it's one of my better performers, and part of the reason why I am up double digits for the YTD period, even with the latest declines.

Being an integrated utility and one of the largest of its kind on earth, Enel owns all levels of the power supply chain - from generating its electricity to transmitting it to distributing it. The company also remains fairly heavily LATAM-focused, with over 20% of operations in LATAM geographies and regions.

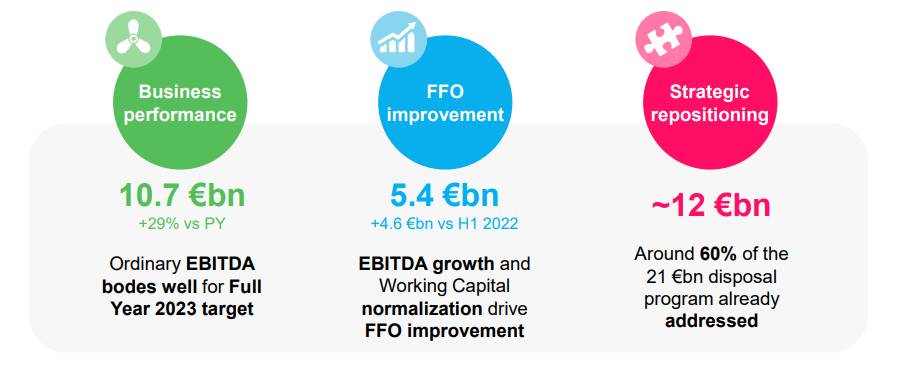

The 1H23/2Q23 period was, for lack of a better word, pretty boring. Boring is good, though - boring is what I look for. The company is fully in line with its deleveraging program, repositioning assets valued at around €21B since the 2022 period. For 2023, €6B of the planned €12.2B is already repositioned, and for 2024 the plan is only €2.8B. So, a near-majority of the repositioning of the company's targets is already finished here.

Results were solid - as expected.

{kind=link}

In many ways, I viewed and still view this company as a bit of a player piano. It's doing exactly what it's set out to do, the dividend is rock-solid and safe, guided by the company for the next few years (much like E.ON (EONGY)), and most KPIs that matter here are showing positive trends.

The company's CapEx is far more mixed than your typical renewable-heavy utility, both in geography and technology. There's an unfortunate heavy emphasis on Wind, but the gross CapEx in terms of other tech is growing faster than wind power CapEx (Source: Enel 2Q23).

That doesn't mean that boring results aren't sometimes surprising. The EBITDA is worth noting here.

Why?

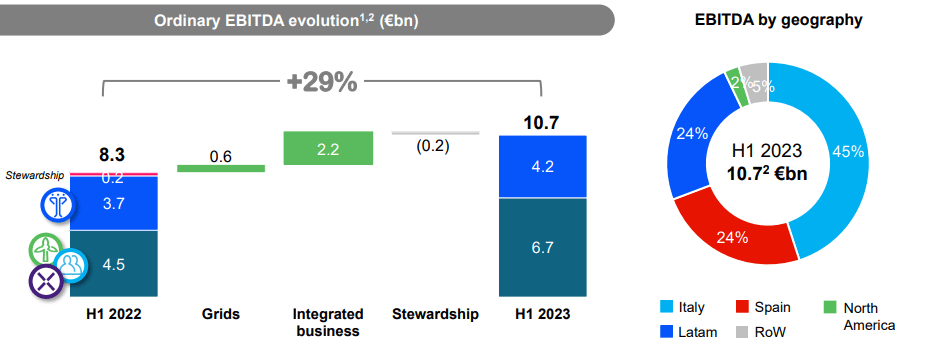

Because Enel managed a double-digit EBITDA increase in a normalizing environment. Also note that Enel has not dropped even close to as much as some of its renewable-heavy peers and competitors.

{kind=link}

I actually view Enel as far better prepared than many of the utilities people on this site seem to love so much. The company also has excellent regulatory relationships and frameworks, with an already-decided tariff increase not only in Brazil (DX Sao Paulo is up 12% since July 4th), but core Italy as well, with a WACC adjustment mechanism implying a non-trivial increase in 2024.

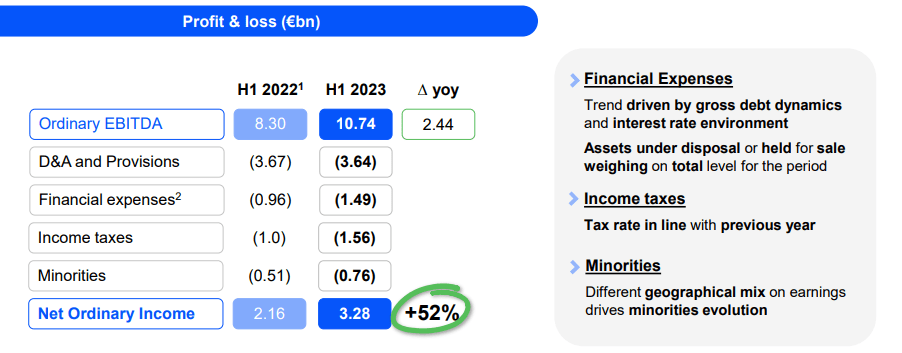

All this has resulted in a net ordinary income improvement of over 50% here, driven by strong EBITDA.

{kind=link}

The P&L's here are absolutely stellar. FFO is up nearly 7x YoY, thanks to a massive recovery in working capital - though this was both guided for and expected by me. (Source: 2Q23 Enel )

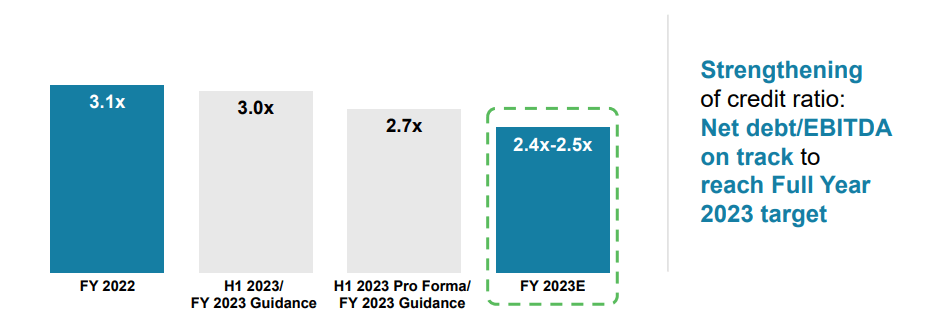

Any quarterly dynamics that were negative here were non-operating items. FX had a slim impact. What I want to point especially to is the company's debt evolution going into a rising rate environment. It's what's causing such worries with NextEra (NEE), among other things. Well, Enel is now down to below 3x Net debt/EBITDA, and it's targeting 2.4-2.5x by year-end 2023E.

{kind=link}

As you can see, the company is on track to deliver just that to you, and it's confirming the full-year guidance, with a continued dividend of €0.43/share for the common. This comes to a yield of 7.67% here, and this is backed by one of the strongest European utility trends out there.

This might sound high, but it's actually a confirmed, sustainable and visible dividend covered by operating cash flow alone. You're quite safe here with this payout, is what I am saying.

The company also has ongoing and working expansion plans, which is where much of its CapEx is going. New assets will primarily be focused on what the company calls "tier 1 asset nations/countries", with geographies such as Italy, USA, Mexico, Brazil, Spain, and others. The company wants to have the potential for an integrated presence before deploying significant amounts of capital into the countries. This is part of what is expected to bring about the 5-7% CAGR in income and EBITDA - note that the company is not guiding for the somewhat "nutty" double-digit numbers guided for by NEE during July of 2023.

Enel, quite interestingly, is the more conservative operator here as I see it. I remind you that last time I wrote about the company the implied yield for Enel was over 9%. That means that my current yield basis for this investment is actually 9.34% for my entire position.

You may understand, knowing this, why I intend to keep my position in the company, but also why it's hard for me to "BUY" more in a company I'm already at a maxed-out position, and where my own YoC is actually better than what's available here.

However, I have added shares to my corporate account. I've also spoken to friends about the company. This is one of those rare businesses where I don't mind "beating the drum" a bit.

And I'll show you why the beating of the drum is not yet over here.

Enel - Why there is more upside potential

The appeal and upside for Enel is a simple valuation-based play where the company, as I see it, is far too cheap for what it offers - even at a 7.6% yield. People are very busy espousing and confirming the advantages of the A-rated NEE while ignoring, or seemingly being unaware of the BBB+ rated and equally/more-interesting Enel.

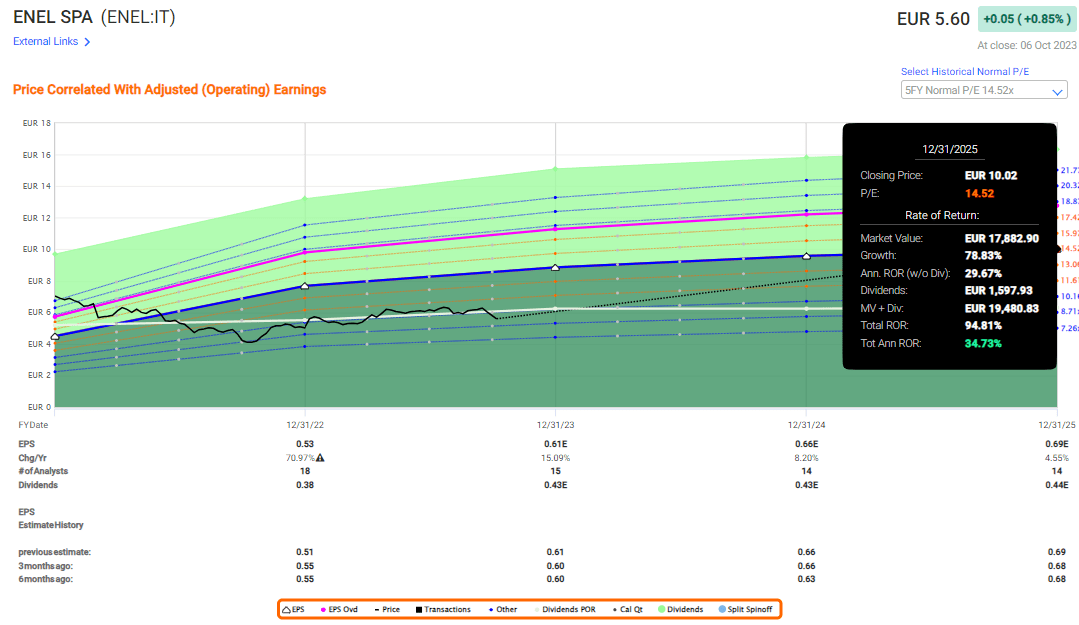

Unlike NEE and its higher-traded renewable peers/competitors, Enel trades at 9.4x P/E blended, with a current market cap of around €57B.

The company typically trades at 14.5x P/E. That's the 10-year normalized average for this business.

The upside to this average is over 34% per year until 2025E, based on estimates that turn out accurate 75% of the time (Source: FactSet).

{kind=link}

Really, that's all I should need to tell you, together with what I showed you above. S&P global targets for this stock are starting at €5.3 on the low side (note the current share price), with a high of €10.8/share. I don't believe the company will reach above €9.5/share or so, at least not easily. But the average of €7.55/share is conservative, and it marks the lowest possible level where I would personally consider divesting this stock to take home profits. Until it hits that, I'm keeping it very close to my heart.

The 22 analysts following the stock are of a like mind. 19 of them are at "BUY" or equivalent, none at "SELL" or negative.

What risks do exist for Enel are not dissimilar from any utility. It's rate changes and in this case, noting that the exposure mix is non-trivial towards LATAM. But LATAM companies, just like PIGS-exposed businesses can't receive the discount hammer on an unending basis simply because of their exposure in my opinion.

As we've seen here, the outperformance of Enel has been significant. At least 4x to the S&P500.

I see no significant risks or impacts that this company is going to see "negative surprises", and the less leveraged it gets, the more insulated from these risks we're getting it.

I wish I wasn't so strict about my rules of concentration or diversification. I have holdings where I don't expect a payoff for 2-3 years. This is a holding where I expect a potential payoff within 12 months, by which I mean a reversal to above €7/share.

If you're not yet aware of this business, I would consider this the potential leg-down to take a look at Enel and see if it matches your investment goals.

Because if you like NEE, I believe you should like Enel as well.

Here is my thesis for the business as it stands today.

Thesis

- My plans for holding Enel are simple. Buy it cheap - and hold it until/if it gets overvalued - which it can. Cash in on an inflation-beating dividend until then. It's not the fanciest plan - but it's certainly a "safe" one in my view, as trends in today's market go.

- There are risks for Enel, but these risks pale in comparison to the through-cyclic stability and dividend safety of this legacy utility with exposures throughout Italy and LATAM. My strategy for this one is as simple as it was with E.ON, and that's my idea for interested investors as well. Buy cheap. Hold.

- Remember the relevant ADR here - ENLAY. You can also choose to invest in specific Enel business activities - this is not what that article is about, and I haven't gone deep enough to consider individual segments like the Americas, Chile, or Russia as their own investments. This thesis is for Enel as a whole.

- I give Enel a price target of at least €7.5/share here, and I fully acknowledge that this is actually on the low end of the potential spectrum of what the company may achieve.

- Enel is a "BUY" to me here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

Enel was cheap when I wrote about it a year ago. I would not call it cheap at €5.6 - but below €5.2 it's cheap again.

I hope it goes there.

Thank you for reading.

For further details see:

Enel: Still One Of The Better Utility Investments Out There