ESOCF - Enel: Strong 9M Results With Outlook Improved

2023-11-19 08:21:36 ET

Summary

- Enel is reorganizing its e-mobility business in North America, focusing on more profitable activities.

- Rumors on a new disposal in India. Business simplification is ongoing.

- Higher guidance and lower projected debt development. Our buy rating is still confirmed.

Here at the Lab, we started the year with a Strong Buy Recommendation on Enel ( ENLAY ), releasing a publication called the company " Is Set To Outperform In 2023 ." Looking at the stock price performance and also considering the fact that the magnificent seven sisters made the S&P 500 return, we are delighted with Enel's total return, which is almost up by 40% vs. the index at a plus 17.5%. As a reminder, we had a target price of €8 per share, and despite the YTD performance, we believe the company's valuation is still inexpensive. The company trades at 8.5x 2023 P/E multiple, 6.6x EV/EBITDA multiple, and offers a dividend yield of 6.7%. Aside from a compelling valuation, solid & inline results and a deleveraging story supported our buy rating. Today, we are back to check Enel's Q3 results and disposal update.

{kind=link}

Q3 Recap

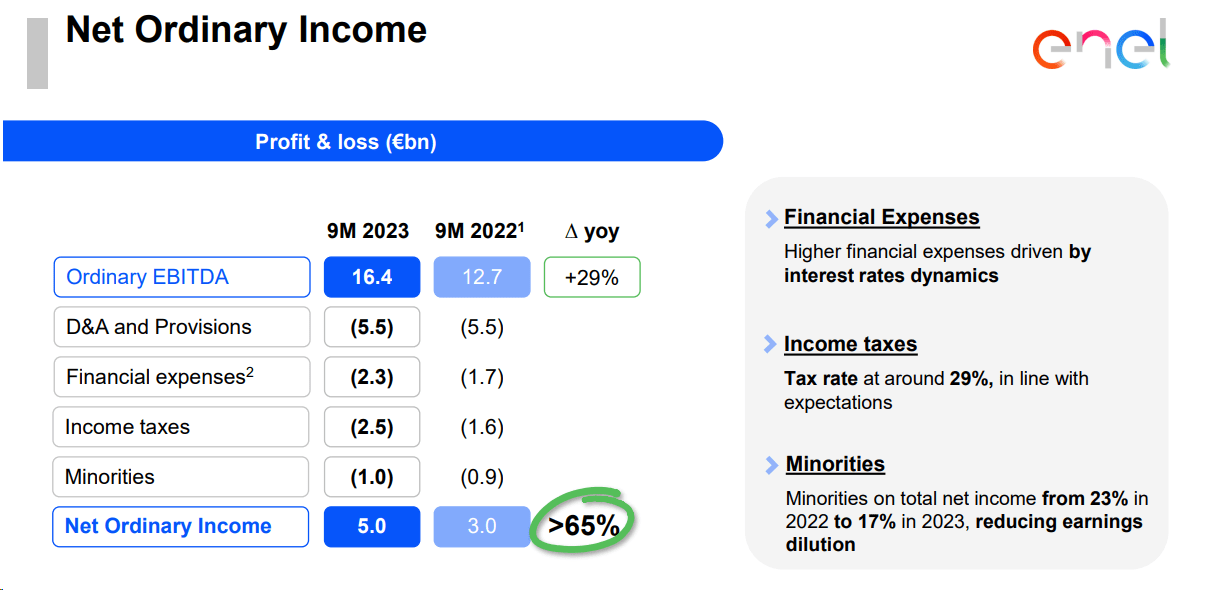

Before we proceed with our analysis, it is important to report Enel's Q3 operational performance. The company closed the 9M accounts with an EBITDA of €16.4 billion, up 29% yearly, and a net profit uplift to €5 billion with a 65% jump. Regarding our investment thesis, Enel confirmed a 2024 interim dividend of €0.215 per share with an increase of 7.5% compared to the dividend distributed in January 2023. The overall DPS is set at €0.43 with a yield of 6.7%. Revenues are going down at €70 billion, in line with the energy prices stability and also due to the different scope of consolidation. The company's guidance was upgraded in light of the solid operating performance. In particular, Enel now expects an ordinary EBITDA between €21.5 and €22.5 billion, with an increase compared to the previous target of between €20.4 and €21 billion (Fig 5). Also, net income has been increased. EBITDA growth was mainly due to integrated business performance and better-than-expected Enel X performance, which led to an overall increase of €3.3 billion. Italian hydro level normalization was also supportive of the EBITDA results.

{kind=link}

Source: Enel Q3 Results presentation - Fig 1

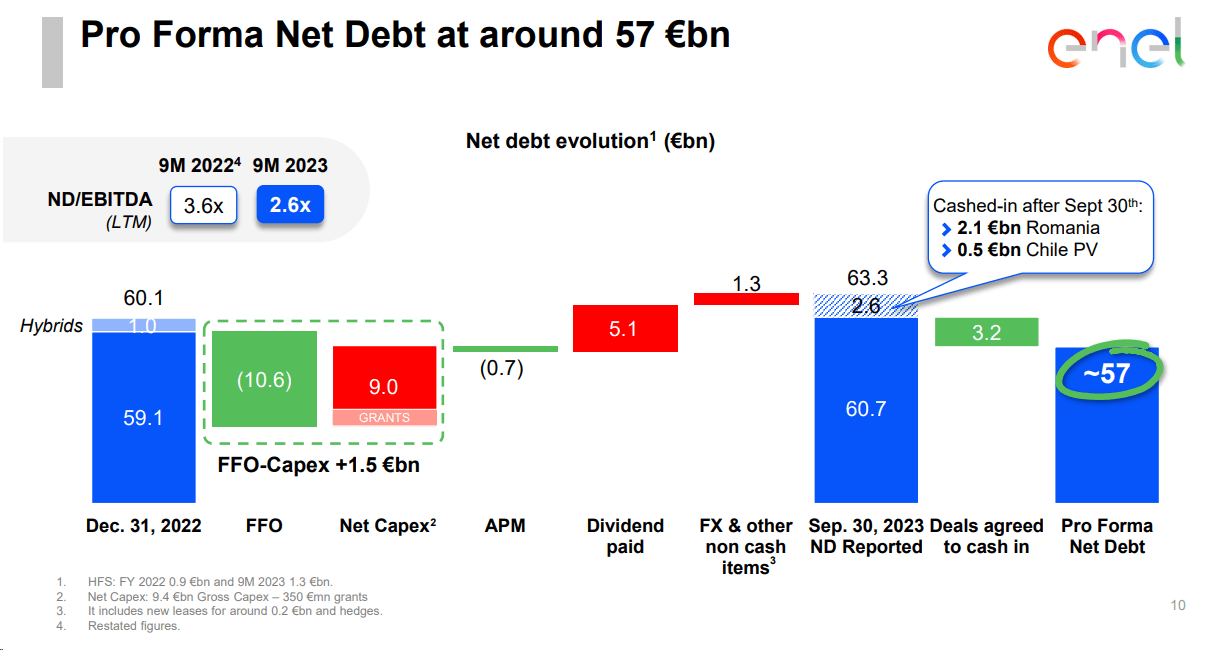

Net financial debt, which has always been under a noteworthy observation, increased to €63.3 billion from around €60 billion at 2022-end. Debt was up by 5.4%. The organic cash flows, company disposals, and hybrid subordinated non-convertible bond loans only partially offset the needs of CAPEX and the unfavorable trend in exchange rates. However, looking at the presentation, the pro-forma debt, calculated with the proceeds of post-September-end, sees a drop in total debt to €57 billion thanks to €2.1 billion disposal from Romania and €500 million disinvestment from Chile . Enel is in the process of additional disposal for another €3.2 billion value.

{kind=link}

Fig 2

Additional positive news and Changes in Estimates

- According to the latest rumors, Enel's reorganization strategy continues. After the latest USA sales, now could be the time to divest from India. Indeed, Enel is evaluating the sale of Enel Green Power India, the renewable energy division in the country. The Italian conglomerate would have entrusted a mandate to the investment bank HSBC. The potential sales concerns a " mixed " asset portfolio. There is a package of 760 MW of operational wind and solar facility with and alongside the installed base; there is a prospect pipeline under development for a total capacity of 2 GW. We understand that the sales process is in its early stages, and according to our estimates, the enterprise value could be around $300 million;

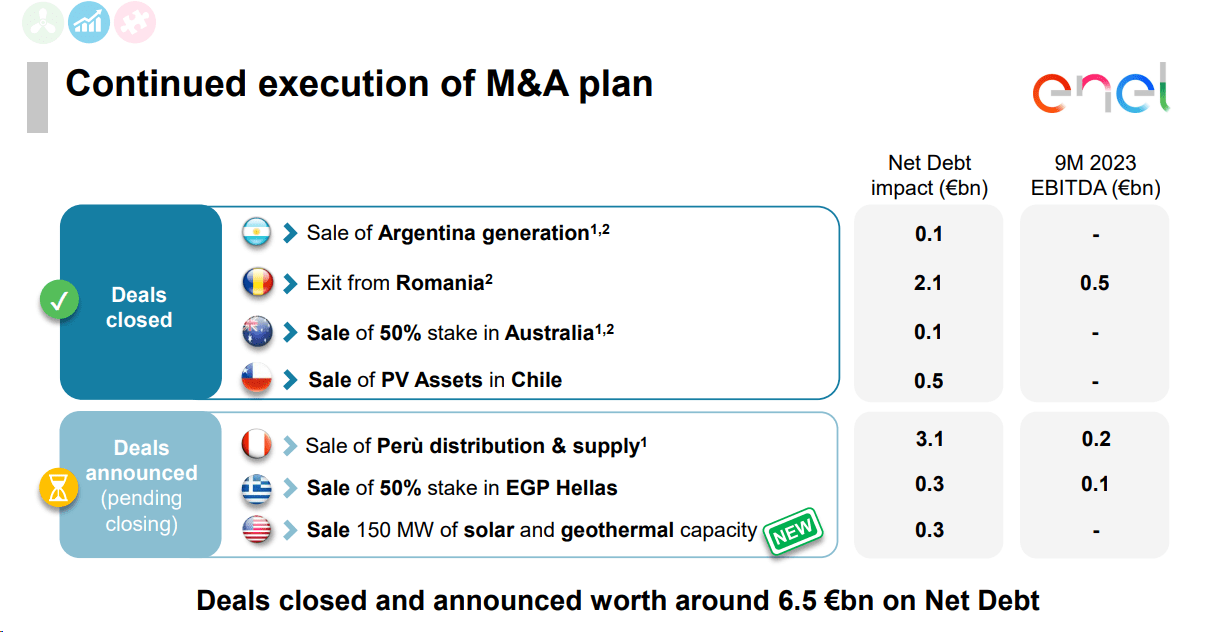

- Enel is moving on with three primary operations to reach the year-end target. The largest concerns the Perù asset, a value of €3.1 billion. Another €300 million is expected from the Greece sale, and a similar figure is also attributed to the most recent disposal of 150 Megawatts of geothermal capacity in the United States (Fig 3). Enel year-end net debt/EBITDA could be at 2.4/2.5x (from the 3x at 2022-end). Post Q3 results, we are moving our 2023/2024 year-end net debt estimates to €54.9/€52.2 billion, respectively. In Q3, working capital had a positive contribution of €0.8 billion, and Enel reported that WC is normalizing;

- Another supportive key takeaway from the Enel buy case is the business simplification. Enel is working on reorganizing Enel X, especially in North America. The aim is to restore a balance favoring profitable business activities. In the United States, Enel built a larger company structure. EV tenders for charging networks still need to be materialized. Therefore, the CEO decided to streamline a few activities and reduce the fixed costs. Considering the disposals, following the latest results, we are guiding a 2023 EBITDA of €21.9 billion, and we forecast a 2024 EBITDA of €21.8 billion. In detail, EBITDA is supported by renewable energy divisions and networks;

- On the DPS estimates, we leave unchanged our estimates (2023 and 2024 DPS at €0.43 and €0.45, respectively).

{kind=link}

Fig 3

Enel Performance of the Period and net debt/EBITDA target

{kind=link}

Fig 4

Conclusion and Valuation

Even if pending asset sales may not be completed before 2023, we believe the net debt target is just a question of timing. CAPEX is now towards safer countries, and business simplification is ongoing. The company increased the guidance and confirmed the dividend hike. In Enel's analysis, the net uplift reflects the positive trend of Enel's cash flow and the lower incidence of minority interests. According to our estimates, this development almost offset the increase in net financial charges due to higher rates. Regarding the valuation, Enel is still discounted vs. the sector. Currently, Enel trades at a P/E of 8.5x and a 6.6x EV/EBITDA vs. an industry mean of 14.85x and 9.81x, respectively. We are now aligned with the company's new guidance, and our EPS reached €0.66 in 2024. Valuing Enel with a 12x P/E (still below its peers), we confirmed our valuation of €8 per share .

{kind=link}

Fig 5

For further details see:

Enel: Strong 9M Results With Outlook Improved