ENLAY - Enel: Valuation Is Still At A Discount To Index

2023-06-16 08:39:51 ET

Summary

- Attractive upside if it achieves consensus FY25 EPS and closes its valuation gap versus the benchmark index.

- High debt contributed to the continued discount vs index, but this gap may close as ENLAY strengthens its balance sheet and improves its corporate structure.

- Consolidating European holdings, improving operational efficiency, and delivering on asset disposal plans could unlock significant upside for ENLAY.

Overview

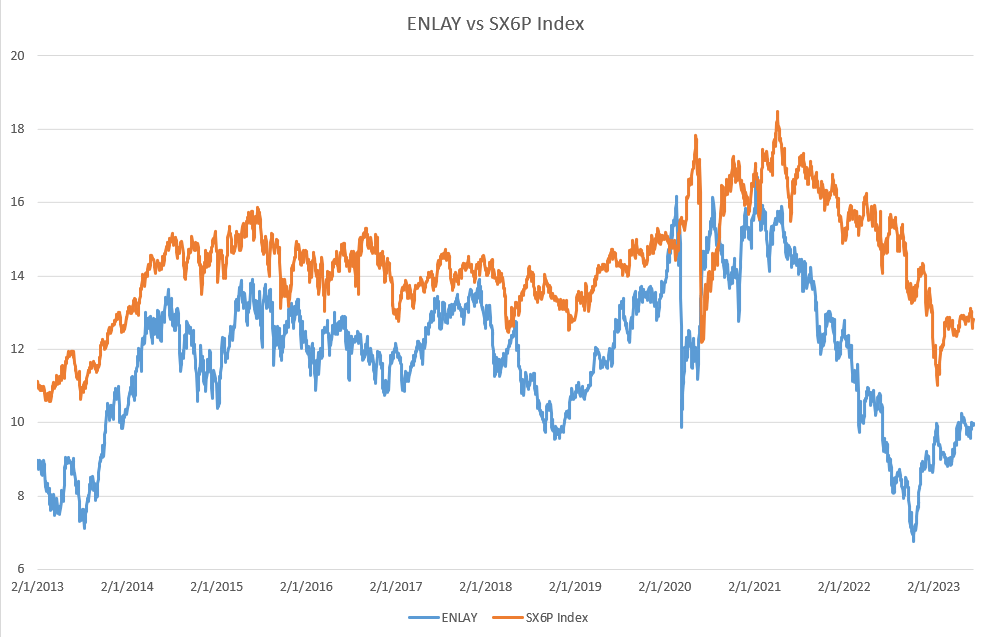

I maintain my opinion ( buy rating ) on Enel (ENLAY) after its business and stock performed as expected. I remain convinced that ENLAY is one of the world's foremost leaders in accelerating the energy transition on account of its global reach and the scalability afforded by its vertically integrated business model. Management at ENLAY has reassured investors that the company will achieve its FY23 goals, despite posting a record-breaking first-quarter ordinary EBITDA and around €400 million in non-cash fair value adjustments. Hence, there is a good chance for ENLAY to beat its own guidance. Despite ENLAY's solid performance and clear outlook through FY23, the stock is trading at a discount to the benchmark index (STXE 600 utilities), a gap I expect to close if the stock keeps performing well or if management takes the steps I outline below. If ENLAY can achieve the consensus FY25 EPS target and close its valuation gap versus the index, I estimate a 40% upside.

Italy free market mechanism

The central premise of my previous thesis highlighted the influence of the free market mechanism in Italy on earnings, which has proven to be successful. There was a massive increase in EBITDA in the free Italian market, from €0.1 billion to €0.7 billion. The unit margin within fixed price contracts more than tripled from €11/MWh to €38/MWh, which was the primary driver of this expansion. The effect of the clawback mechanism was also less than expected, coming in at only €0.1 billion. Although the impact was not fully reflected in the first quarter's earnings due to a non-cash fair value adjustment of €0.4 billion, I expect the remainder of the year's &L to show the full effect. This is so because the non-cash expense is unlikely to recur, allowing the full effect to be felt.

Valuation

{kind=link}

The question now, I believe, should be how ENLAY can close its valuation gap versus the benchmark index, given the success of the earnings growth thesis in Italy. I believe the strength of ENLAY's balance sheet is the primary reason for the valuation's continued discount. Concerning the balance sheet, I anticipate that net debt will experience a favorable impact due to a faster-than-anticipated decrease in regulatory working capital. In the first quarter, regulatory working capital declined from €5.4 billion to €3.2 billion, and unless there is a substantial and unlikely surge in power prices, there is no basis to anticipate an increase in regulatory working capital later in the year. It's worth noting that the company's projections for its net debt reduction through 2023 were based on the assumption that regulatory working capital would not recover at all. Aside this, I also expect to see management stepping up on the corporate actions front to dispose assets. Management has successfully completed or announced sales totaling €5 billion year-to-date, and they anticipate announcing the sale of €2.8 billion worth of assets before the end of the first half of the year. I believe this €2.8 billion worth of disposal to come true as they are already in advanced negotiations. Therefore, I think the path to further strengthening the balance sheet is also going on very well. It would take some time for the net debt figure to come down, but it should eventually, in my opinion.

In addition to financial considerations, I believe that ENLAY has an opportunity to enhance its corporate structure in order to provide the market with a more accurate assessment of its true value. Specifically, ENLAY's European portfolio is primarily comprised of operations in Italy and Spain. While ENLAY holds full ownership of its Italian operations, it maintains a 70% stake in its Spanish subsidiary, Endesa. Given that both entities are vertically integrated utilities with similar operational characteristics, there may be a compelling case for consolidating these European holdings. By combining the operations of these businesses, there is potential to improve operational efficiency and make it easier for investors to value the business.

Suppose ENLAY manages to hit consensus FY25 EPS estimate of €0.66 and the stock trades at inline with index at ~13x PE, the stock will be worth €8.58 which is around 40% upside.

Conclusion

I maintain my buy rating on ENLAY based on its solid performance and clear outlook. The stock currently trades at a discount to the benchmark index, but I expect this gap to close as ENLAY continues to perform well or takes steps to enhance its corporate structure and strengthen its balance sheet. By consolidating its European holdings, improving operational efficiency, and delivering on its disposal plans, ENLAY has the potential to unlock significant upside. If ENLAY achieves consensus FY25 EPS and closes its valuation gap, an estimated 40% upside is possible.

For further details see:

Enel: Valuation Is Still At A Discount To Index