ENR - Energizer Holdings: Hasn't Been A Good Long-Term Holding

2023-04-14 02:42:31 ET

Summary

- Revenue growth over the next year or so is going to be very modest.

- I think management guidance is too optimistic because of the potential of disruption in its pricing power from a weak economy in the second half.

- The bottom line is the strength of the company, and a low entry point with a low cost basis could offer a decent risk/reward scenario, and a better dividend yield.

Since I last wrote about Energizer Holdings, Inc. ( ENR ), I pointed out the possibility the company could be facing the type of headwinds that had the potential to produce a steep correction, specifically after it bounced off its 52-week low near the end of September and was trading at levels it hadn't been at since early 2022.

It is trading down by over 5 percent since I made the call, but not to the levels I thought it could have potentially dropped to.

But to get an accurate snapshot of the share price performance of Energizer Holdings, we need to look at a 2-year chart, or preferably 5-year chart, to get an idea of how the company has been doing over the long term. From a longer look at its past performance, it hasn't been doing very well for some time.

Going back to July 2018, the stock was trading at approximately $65.00 per share, and has since been continually dropping, falling to as low as $24.81 per share September 26, 2022, before rebounding to trade at just above $31.00 per share as I write.

After falling off the cliff in November 18, 2018, it has since bumped against a ceiling of around $53.00 per share, which it has hit several times while trading volatile and choppy. From that time on it hasn't been able to find the catalysts that could result in the company's sustainable and consistent growth going forward.

As management has mentioned in the last couple of earnings calls, its focus was going to be on improving margins, reducing debt, and boosting free cash flow. To that end, it appears to have improved in those areas; although the sustainability of the improvement has yet to be proven.

In this article we'll look at some of the numbers, what its growth prospects are, and why the company will probably continue to trade flat for the foreseeable future.

{kind=link}

Some of the numbers

Revenue in the first fiscal quarter of 2023 was $765.1 million, compared to revenue of $846.3 million in the first fiscal quarter of 2022, down 9.59 percent year-over-year.

The major thing to consider in regard to revenue growth in the quarters ahead is how long it'll be able to raise prices, especially with organic growth projected to be flat to low-single-digits. Even with the increase in prices, net sales still dropped almost ten percent year-over-year. That is more likely to get worse over the next three quarters or so as organic growth continues to soften.

Management believes it'll be able to raise prices and recover category volumes through 2023, but I'm not convinced it'll be able to do so because of my expectations the economy is going to get much weaker than it is today, which would likely put a damper on ENR's pricing strategy.

Net income in the reporting period was $49.00 million, or $0.68 per diluted share, compared to net income of $60.00 million, or $0.83 per diluted share for the first fiscal quarter of 2022.

ENR generated free cash flow of $152.00 million in the first fiscal quarter of 2023. That was attributed to an approximate 250 basis point improvement in working capital as a percent of net sales since the beginning of the year. As a result of the boost in free cash flow, the company was able to pay down another $53.00 million of its term loan. The lowering of its long-term debt is helping to alleviate some of the rising interest rate expenses; the company still sees it climbing to a range of $4.00 million to $5.00 million.

At the end of calendar 2022, the company had cash and cash equivalents of $280.3 million, compared to cash and cash equivalents of $205.3 million at the end of September 2022.

The company held long-term debt of $3.506 billion at the end of 2022, about level with long-term debt of $3.5 billion at the end of September 2022.

While the company has been chipping away at its hefty debt load, it's going to take a lot more cuts to bring it to a place where it will have a lower negative impact on the bottom line of the company.

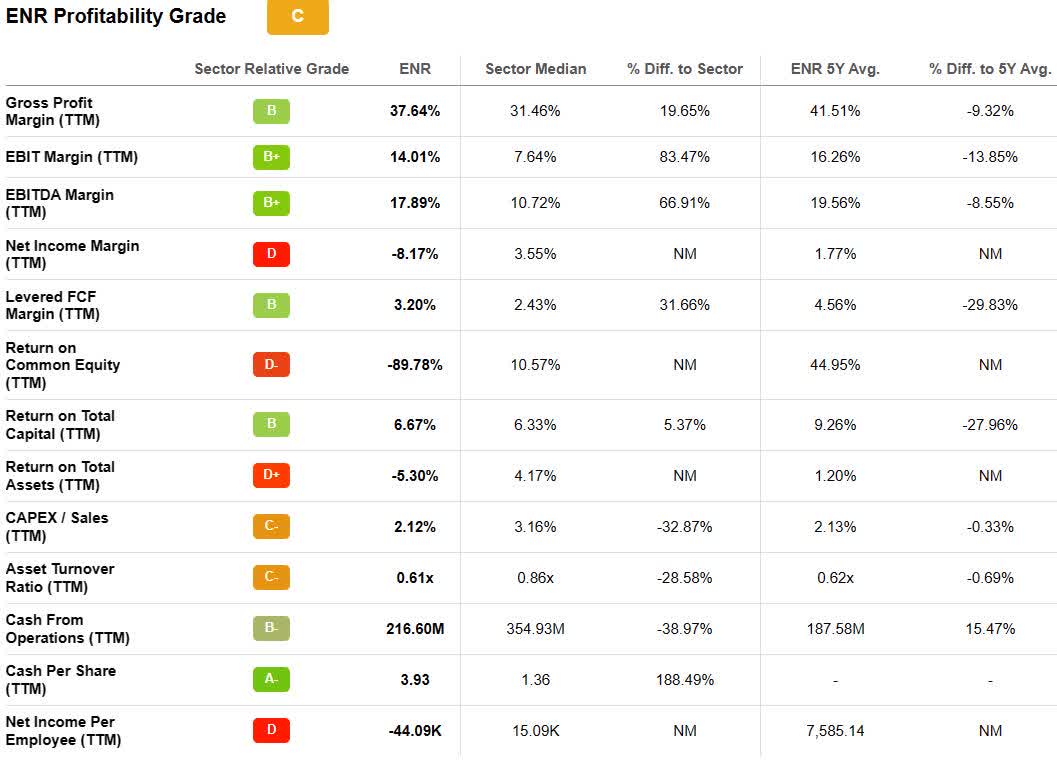

Factor grades and metrics

On a Quant basis, the company is particularly weak in growth and profitability, reflecting its performance over the last year, and how I believe it's going to trade in the next year or so.

As mentioned in its earnings report, revenue growth slowed down, with (YoY) revenue growth of -(1.67) percent, compared to the sector median of 10.59 percent. Revenue growth ((FWD)) is 0.34 percent, compared to the sector median of 6.06 percent - lower by -(94.37) percent.

EBITDA growth (YoY) was -(9.25) percent, compared to the sector median of 3.05 percent. EBITDA growth ((FWD)) is -(1.12) percent, compared to the sector median of 5.08 percent.

These two growth metrics reinforce my thesis that ENR is going to have a tough second half of 2023 and isn't likely to perform as well as management believes it can.

Concerning profitability metrics , the company was especially weak in the important net income margin metric, coming in at -(8.17) percent, compared to the sector median of 3.55 percent.

EBITDA margin ((TTM)) was 17.89 percent, compared to the sector median of 10.72 percent - higher by 66.91 percent.

Return on equity ((TTM)) was -(89.78) percent, compared to the sector median of 10.57 percent. It was also weak with return on assets, which was -(5.30) percent, compared to the sector median of 4.17 percent. It was stronger in return on capital ((TTM)), which was 6.67 percent, compared to the sector median of 6.33 percent.

{kind=link}

While cash from operations wasn't bad at $216.60 million, it was -(39.00) percent lower than the sector median of $354.93 million.

Taking into account its earnings report, management guidance, and its factor grades, the combination points to the company struggling to maintain much momentum over the next several quarters.

At best it looks like it may grow revenue in the low single digits, and I think the bottom line will be under pressure from the growing effect of high interest rates, and what I believe will be less pricing power than the company has had in the recent past.

Macroeconomic headwinds

There are those that are already thinking that economy is turning around and is in the early stages of a rebound. I'm not one of them. I think investors making decisions based upon an assumed economic turnaround at this time have the potential to get burned.

That would also be true with ENR, especially after it bounced from about $25.00 per share to approximately $38.00 per share in early January 2023 before pulling back.

While it's understandable that the stock would bounce after hitting its 5-year low, there's nothing I see that would point to it sustainably rebounding anytime soon, with the economy almost certain to slow down in the latter half of the year.

What I think is going to happen is when the economy, including the job market and interest rate environment remain headwinds, the highly probable outcome will be for consumers in particular to cut back on spending, and in the case of batteries, many are likely to gravitate toward lower-price products if economic conditions get worse.

If that's how it plays out, it would undermine the pricing power of ENR, leaving it with working on ways to cut more costs. In general, that's not necessarily a bad thing, but it's limited as to how much that will improve the company's performance over the long haul, i.e., there are only so many ways you can improve the bottom line without scaling.

Conclusion

Investors need to take a closer look at the long-term trajectory of the share price of ENR in order to get a feel for how consistently it has fallen over the last five years. And with limited revenue upside, I'm not seeing much that would trigger a consistent and sustainable upward move in its share price.

With the way the stock has traded volatile and choppy for some time, it doesn't mean there will never be some significant bounces, because there's sure to be. But as the company stands today, those are likely to be temporary.

The company is relying on pricing power in the quarters ahead to boost revenue growth and somewhat improve margins, but I think it's going to struggle to do so with that strategy. I'm not saying it's the only thing the company is doing to improve margins and the bottom line, only that it's a significant piece of the puzzle that isn't likely to play out like management thinks it will, in my opinion.

It's close to certain that the Federal Reserve has at least one more interest rate increase coming in May, and most likely will pause and see the impact on inflation. Even if there's a prolonged pause, it means ENG is going to experience higher capital costs at minimum, and if interest rates remain high for the rest of 2023 and possibly early 2024, the company is going to have higher expenses related to that.

A couple of strengths the company has had is in increasing free cash flow, and using some of that to pay down its large debt load. That will continue to help if it's able to generate strong free cash flow in the quarters ahead.

The bottom line is where I see the company having some strength at this time, but its topline appears to be weak and could easily underperform over the next year.

For those interested in ENR, I think it would be better to wait for another pullback before considering taking a position in order to improve risk/reward by having a good entry point with a low-cost basis. That would also improve the dividend yield, which I don't think is in any danger for now.

For years the trend for ENR has been down, and I can see no visible catalyst that has the potential to turn that around. Until there is, I would be cautious about taking a position in the company until a lower entry point lowers the risk.

For further details see:

Energizer Holdings: Hasn't Been A Good Long-Term Holding