ENR - Energizer Holdings Inc: Dividend Makes Me Stick Around

2023-08-09 16:36:26 ET

Summary

- Energizer Holdings Inc. has experienced slow growth in earnings, with a 2.6% YoY increase, but a stronger growth in the bottom line at 36%.

- The company's product line is broad and has benefited them as they established household brands, but they are facing headwinds such as currency fluctuations and inconsistent earnings reports.

- Sales volumes for ENR have declined, potentially due to consumers being deterred by higher prices, and the company may face challenges if demand slows and costs remain high.

Investment Rundown

Growth is not that strong for Energizer Holdings, Inc. ( ENR ) which seems to have been a cause for the lower multiple the company receives. In the last report, the earnings just rose by 2.6% YoY. Stronger progress was made for the bottom line though, which grew by 36%. I worry that ENR will eventually reach a stage where the EPS is also slowing if the top line can't pick up the pace in the coming years.

The company has had a decent run the last 12 months but I think we may be reaching a ceiling here and for those that still want to stick around for the dividend then ENR offers some decent potential. The growth rate for the dividend is however not that high and the payout ratio is quite high at over 40%. I don't want to make a sell rating for the company as the quality of the business model is still very strong. In conclusion, I am rating ENR a hold right now.

Company Segments

ENR engages in the production, marketing, and distribution of a wide array of household batteries, specialty batteries, and innovative lighting solutions. These offerings encompass a variety of battery types and lighting products that serve a broad range of consumer needs. Under the brands Energizer, Eveready, and Rayovac, the company provides an essential array of power sources that fuel both daily convenience and specialized applications.

ENR is included in the household products industry which has a valuation quite a lot higher than what ENR has right now, but that is a discussion we will touch on more below here. Where ENR has set itself apart from peers is that the product line that the company has is incredibly broad and this has benefited them very well as they established household brands.

Company Momentum (Investor Presentation)

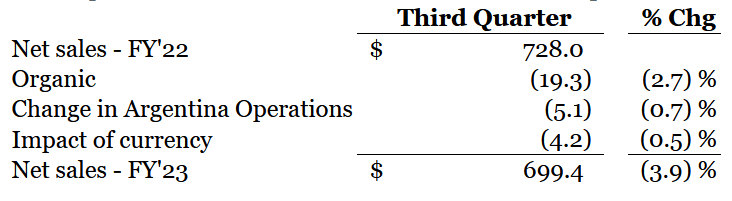

Going into 2023 ENR is expected to see some growth in the net sales, as they grow in the single digits for the year. This is coming as ENR is also facing headwinds like currency fluctuations causing inconsistent earnings reports and other challenges for the business.

Earnings Highlights

During the third quarter of 2023, the implementation of price increases notably played a pivotal role in organic sales for the company, but the last quarter showed difficulties as sales declined YoY. However, an interesting trend emerges as sales volumes seem to be experiencing a decline. This phenomenon could be attributed to consumers, who are already grappling with the strains of inflation, being confronted with the implications of these elevated prices. Consequently, the sticker shock induced by these higher price points could be dampening the demand for the company's offerings.

{kind=link}

Looking closer at the quarter for ENR it shows that the EPS landed at $0.58. The market isn't at its strongest self right now and that means ENR needs to have efficient cost reduction measures. If they fail on this end then EPS will likely fall. Why I do think we might see a decrease in coming quarters comes from the fact that materials goods and expenses are still staying persistent in their price ranges. This will hurt ENR if demand slows and costs remain high. I don't think the recent quarter gave anything for investors to get too excited about honestly.

Risks

Anticipating future trends, it appears that the economic landscape, encompassing factors such as job market stability and the trajectory of interest rates, could exert considerable influence on consumer behavior. As these potential headwinds persist, a likely scenario could involve consumers adopting a more cautious approach to their expenditures. In the realm of battery consumption, this cautious sentiment might manifest in a shift towards cost-conscious choices, with consumers potentially gravitating towards more budget-friendly options, especially in times of economic uncertainty.

Market Outlook (Statista)

In light of these potential shifts in consumer behavior, ENR might need to adopt a strategic approach to navigate this landscape. The scenario of consumers prioritizing cost-effectiveness could necessitate a response from ENR that focuses on maintaining competitiveness while preserving product quality. Balancing these factors will be essential to ensure that the company can continue to meet consumer demands and expectations, even in a more cost-conscious environment. With less excess capital for everyday Americans, there is a far smaller amount of customers flocking to buy products that ENR is offering. This creates a difficult environment to operate in and I don’t think it's impossible we see the net margins further declining for the company going forward.

Sector Comparison

Looking at the valuation of ENR right now it seems to put off a valuation far below the sector. The p/e for example sits at just 11 on a forward basis. That means ENR has a discount of 38%. I think the downside is quite limited from here on, but I also think the upside isn't that strong either for ENR unfortunately.

{kind=link}

Growth going forward seems quite modest and I think the biggest appeal for being in ENR right now comes from the over 3% dividend yield it offers. Historically ENR has traded slightly higher based on earnings, a 13x p/e of so. But as long as growth remains rather modest I think this 11 - 13x earnings range will be where ENR trades. Besides, the p/b of the company is incredibly high too at over 10x. That doesn't really suggest you are getting a very good deal investing in the company right now, unfortunately.

Final Words

ENR has a very broad set of products under its brand which has lent the ability to grow revenues and earnings quite strongly when the capital was circulating more freely in the market. But as rising interest rates are making an impact on everyday people's finances they are cutting in on spending. This hurts demand for ENR and I think we are in for some disappointing quarters going forward here, unfortunately. The company does however have a very decent dividend yield which is why I will be rating it a hold right now.

For further details see:

Energizer Holdings Inc: Dividend Makes Me Stick Around