ENR - Energizer Holdings: Slowly Making Progress

2023-05-21 08:16:20 ET

Summary

- Price increases have driven sales growth, but for how long?

- As expected, debt reduction efforts are moving slowly, given the company's limited cash flow.

- The stock has stalled and does not have much upside.

- Investors may consider selling covered calls to generate income.

I suggested taking some profits in Energizer Holdings ( ENR ) in January. The stock had gone on a huge run, and it was an excellent time to book some profits. As expected, the stock has since stalled. The stock has dropped 2.4% on a total return basis since my article, while the S&P 500 Index has gained 4.2%. The company’s growth has come on the backs of price increases amid declining volumes. The company is hoping for a boost to margins due to lower costs. But, as the economy continues to slow, the question remains whether the demand will remain steady. The stock may not see a dividend increase soon, and its price gains may be limited. Investors sitting on profits in this stock may take this opportunity to generate extra income by selling covered calls or selling them outright.

Price increases drive revenue.

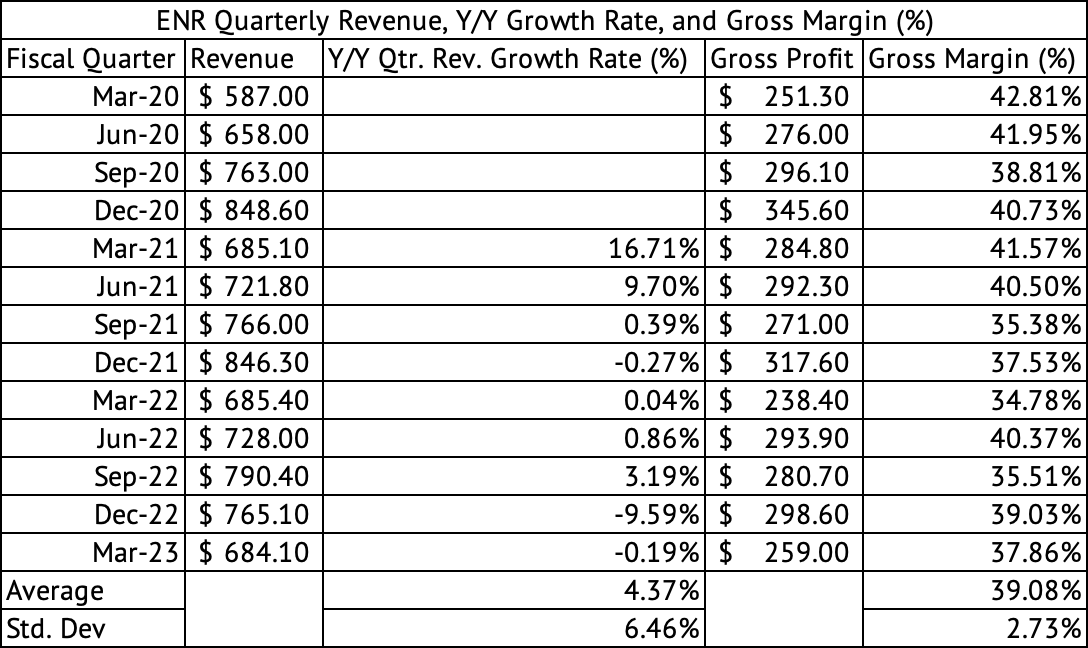

The company sees pressure on its revenues due to tough y/y comparisons to 2022. The December 2022 quarter saw a y/y revenue decline of 9.5% (Exhibit 1) . Revenue declined by a further 0.1% in its March 2023 quarter. The company will be hard-pressed to achieve its 2021 and 2022 revenue numbers, driven by pandemic and stimulus-induced spending. The company’s gross margins have also dropped, despite its ongoing efforts to bolster it with cost-saving programs.

Energizer achieved a 37.8% gross margin in March 2023 compared to its quarterly average of 39% since March 2020. The company has struggled to regain the 40% gross margin mark, achieved in three successive quarters beginning in December 2020. CFO John Drabik commented that the fourth quarter gross margins should improve due to lower input and freight costs and savings from Project Momentum, its cost savings initiative.

Exhibit 1:

Energizer Holdings Quarterly Revenue, Gross Profits, and Gross Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

In Q1 2023, price increases in its Auto and Battery segments contributed 9.5% to organic sales growth . In Q2 2023, price increases contributed to a 13% growth in organic sales. But, the sales volumes are declining as consumers, already strained by inflation, get a sticker shock due to these high prices. The management expects a 3% to 5% growth in revenue in the second half of 2023 due to favorable pricing and moderation of volume declines.

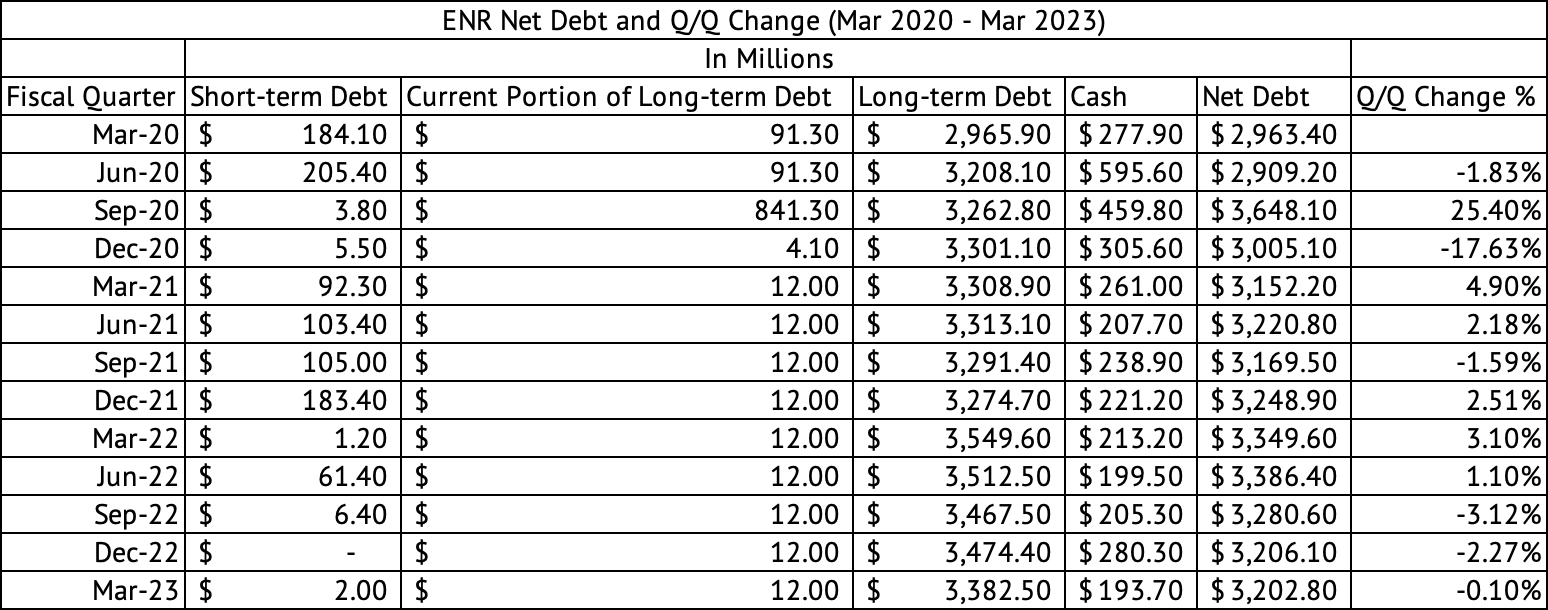

A 5.6x net debt to adjusted EBITDA ratio.

Given the company’s high debt load, management should prioritize debt reduction. The company paid down $100 million in debt last quarter and ended with a net debt to adjusted EBITDA of 5.6x, a decrease of 0.5x, but still a very high ratio. The company needs to be closer to 2x concerning its debt-to-EBITDA ratio. This 0.5x debt ratio reduction is due to solid strength in its brand, good price performance, and a focus on finding cost savings across its operations.

The company is focused on finding more cost savings with its Project Momentum initiative. For instance, Mark LaVigne, the CEO, mentioned that they are using predictive modeling to optimize ocean shipment costs. My last article stated that the company’s debt reduction efforts would move slowly, and that has been the case so far. Assuming the company can achieve a consistent EBITDA of $500 million, which can be challenging, the company can support net debt (after cash) of $1 billion for a 2x net debt to EBITDA ratio or about $1.5 billion for a 3x net debt to EBITDA ratio.

At the end of its March 2023 quarter, the company carried $3.2 billion in net debt (Exhibit 2) . Even if the company pays down $100 million in debt each quarter, which is possible, but challenging given its dividend and CapEx commitments, it would take about 17 quarters or over four years to achieve a 3x debt-to-EBITDA ratio. The company paid $85.5 in total dividend payments and $50.6 million on CapEx, with its operating cash after CapEx and dividend at $183 million over the past twelve months. The company paid $166.2 million in interest payments over the past twelve months.

Exhibit 2:

Energizer Holdings Debt, Cash, Net Debt, and Q/Q Change in Debt (Seeking Alpha, Author Compilation)

{kind=link}

Energizer’s weighted average cost of debt is 4.75% , with 90% of it on fixed interest rates, and does not have significant maturities before 2027. But, after 2027, the company’s interest rate on its debt will jump even when it carries a lower debt load. The U.S. Treasury 2-year bond ( US2Y ), considered risk-free, yields 4.28%. The much longer-term 10-year U.S. Treasury bond ( US10Y ) pays 3.6%. An 8% interest on $2 billion in debt, which would be a substantial reduction for Energizer, would be $160 million in yearly interest payments, similar to its current interest payments. Its debt-to-EBITDA ratio would be around 4x.

Dividend.

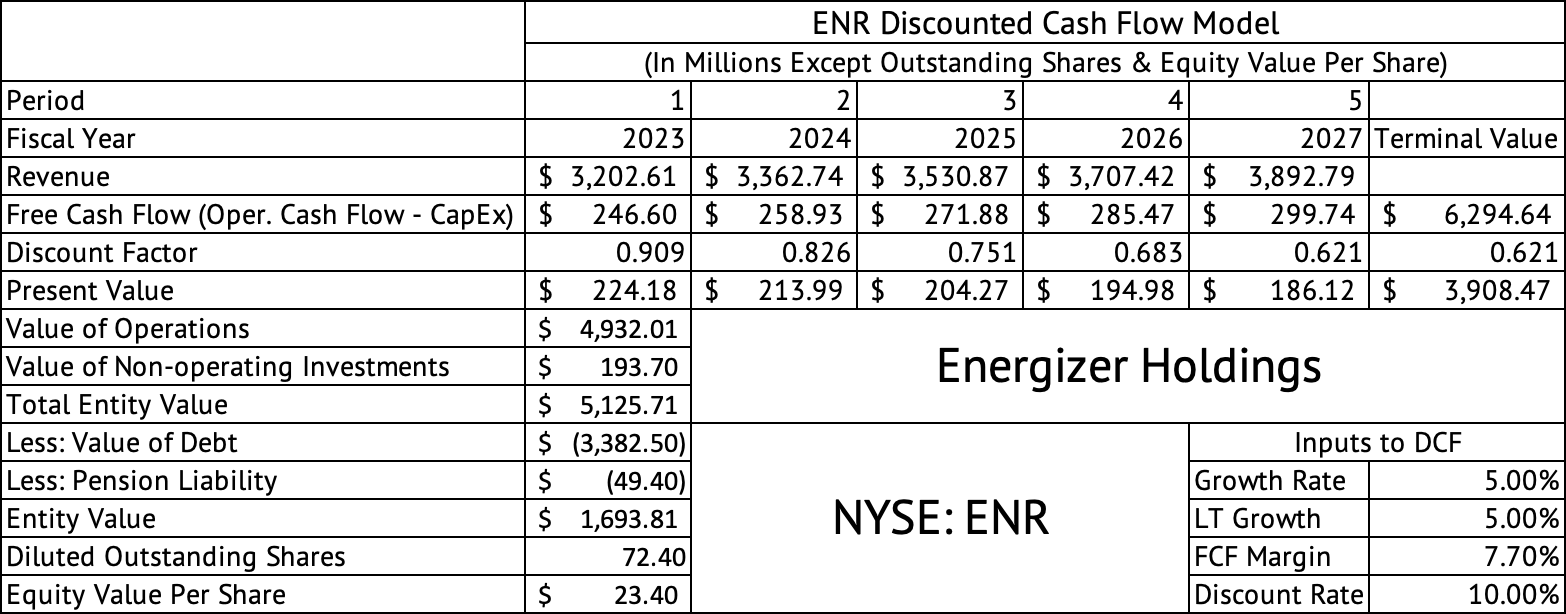

The company offers a reasonable dividend yield of 3.4%, less than the 4.2% yield offered by the U.S. 2-Year Treasury, and a payout ratio of 40%. The Vanguard Industrials Index ETF ( VIS ) provides a 1.47% dividend yield, and the Vanguard S&P 500 Index ETF ( VOO ) yields 1.58%. Given the company’s debt, the management may find it challenging to raise their dividend. The stock is also richly valued based on a discounted cash flow model, with an estimated per-share value of $23 (Exhibit 3) . The model assumes an optimistic revenue growth rate of 5% and a free cash flow margin of 7.7%, its average over the past decade. This model uses a 10% discount rate.

Exhibit 3:

Energizer Holdings Discounted Cash Flow Model (Seeking Alpha, Author Calculations)

{kind=link}

The stock would be undervalued if the company’s cost of capital is 8%, achieves a 5% growth rate, and has a free cash flow margin of 7.7%. It is difficult for Energizer Holdings to achieve a 5% growth rate consistently. But, a 3% growth rate, which is achievable, and an 8% discount rate would put the stock closer to $22. Based on these models, the stock looks overvalued. Investors have no reason to buy this stock at these levels, given its limited revenue growth potential, lack of positive momentum, not much in the way of dividend increases, and high debt. The stock’s 52-week low is $24.81. Investors should only consider this stock if it sells off closer to $25. Before placing a buy order, investors should carefully consider the latest information on the demand environment for the company’s products and its cash flow margins.

Energizer Holdings is undervalued compared to other household product peers, such as Reynolds Consumer Products ( REYN ) or Clorox Company ( CLX ). It trades at a forward PE of 11x, compared to 37x for Clorox Company and 21x for Reynolds Consumer Products.

Energizer Holdings has limited, or no upside, and its dividends may be capped due to its debt load. Investors with gains should consider taking profits or generating an income using covered calls. If the call gets assigned, investors can take heart that they sold near the highs and generated some income to boost their gains. Investors looking to build a position in this stock may be better off waiting for a sell-off before plowing their money.

For further details see:

Energizer Holdings: Slowly Making Progress