FANG - Energy Crisis: 3 Oil Stocks That Get You Paid Handsomely

2023-04-27 08:30:00 ET

Summary

- In this article, I start by explaining why I believe that we should expect a prolonged period of elevated energy prices, supported by rapidly declining supply growth in the US.

- I present three oil picks that I expect to outperform their peers while generating high dividend income.

- All picks come with healthy balance sheets, strong production reserves, low breakeven costs, and high implied free cash flow yields.

Introduction

While I have written countless energy-focused articles since I became bullish in 2020, I have gotten a lot of questions after I wrote (in this article ) that investments in energy are important to protect our wealth against what looks like a high likelihood of prolonged above-average energy prices.

I believe that a good energy investment is based on two components:

- A capital gains component, as I want energy companies that outperform their peers. After all, what's the point of stock picking?

- An income component. Energy has always been a source of dividend income. Especially in times of elevated oil prices, investors benefit from picking companies that have the ability to distribute most of their free cash flow to shareholders.

In this article, I will give you three picks that I believe will get the job done.

Furthermore, we'll start with an update on my long-term oil thesis, as we're getting overwhelming evidence that supply growth is indeed in very deep trouble.

So, let's get to it!

My Thesis Is Being Reinforced

As most readers know, my oil thesis is based on two things.

- I do not believe in peak demand. I expect global oil demand to consistently rise based on rapid growth in emerging markets. OPEC data supports my case. While someone could make the case that OPEC data might be biased, I think their data displays a compelling case (feel free to disagree with me). While demand for renewables is rising much faster, oil demand is expected to grow by at least 10 million barrels per day until 2024. Furthermore, after 2025, oil demand in OECD nations is expected to decline. This is the result of renewable energy investments and related government policies. However, non-OECD growth is expected to remain so high that we could even see slight total oil demand growth after 2040.

{kind=link}

- While I do not make the case that we're running out of oil (we're not), I am a believer in much slower supply growth rates. As the chart below shows, global oil production hasn't risen in years. It even started to slow before pandemic-related lockdowns threw a wrench in the gears of the global economy in 2020. Slow production is caused by factors like the war against fossil fuels in the West, which has caused oil producers to spend money on shareholder distributions instead of production. After all, boosting production makes it way more likely that temporary declines in demand cause steep oil price declines that could drive players out of business. This happened a lot in both 2016 and 2020. With external funding and insurance protection drying up, oil companies are increasingly dependent on their own (internal) funding.

On top of that, we're now dealing with a third factor, which supports subdued production growth.

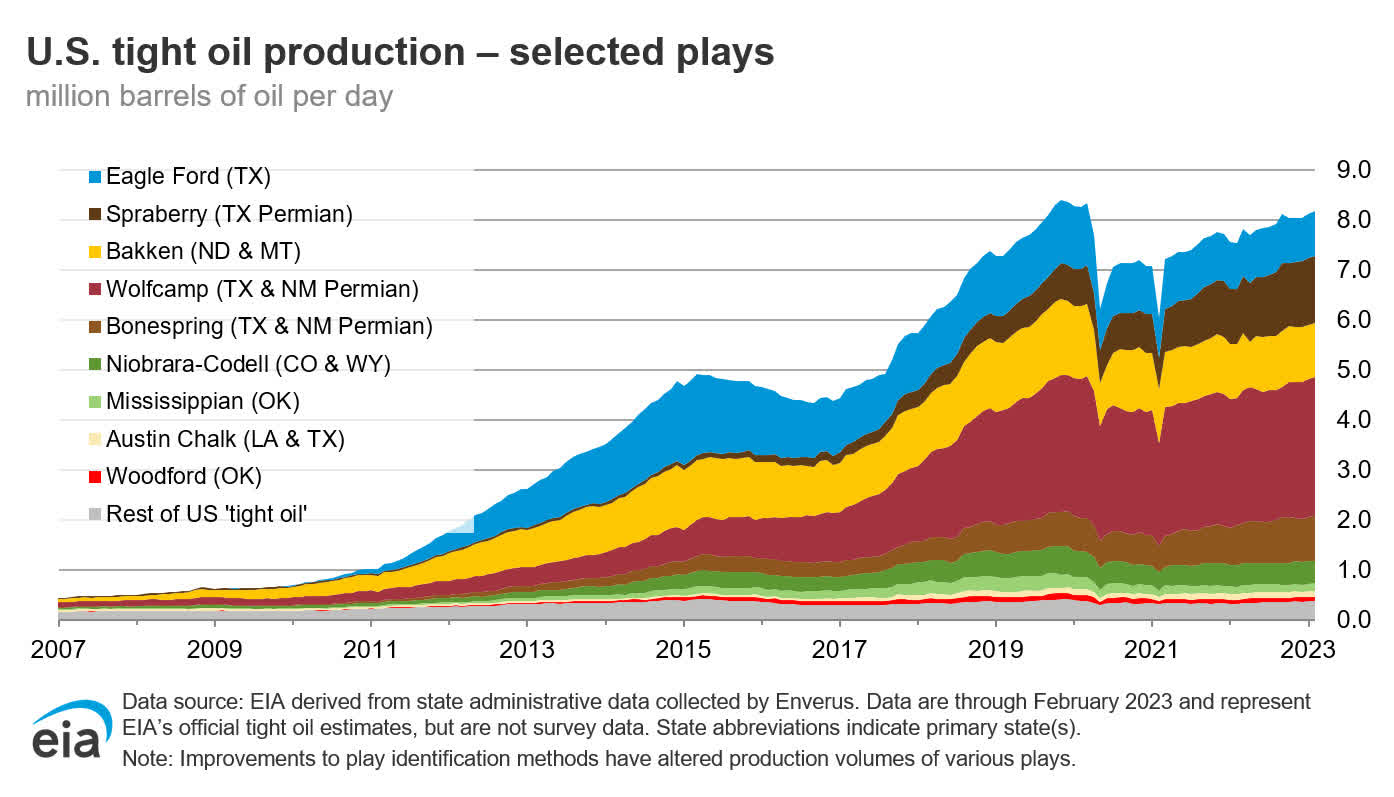

Last month, I wrote an article highlighting the tremendous pressure on supply growth in America's shale basins. The increasing application of unconventional drilling techniques turned the United States into the oil supply growth engine after the Great Financial Crisis. Looking at tight oil production, we see that the US went from roughly 1.0 million barrels of tight oil per day in 2011 to currently 8.0 million barrels. Especially the Permian Basin contributed to accelerated growth.

{kind=link}

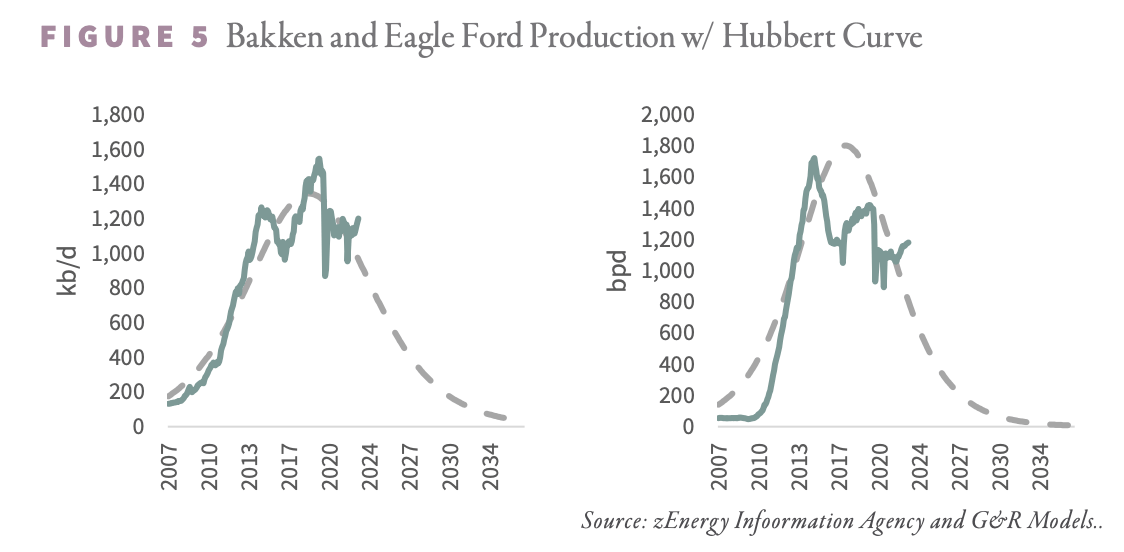

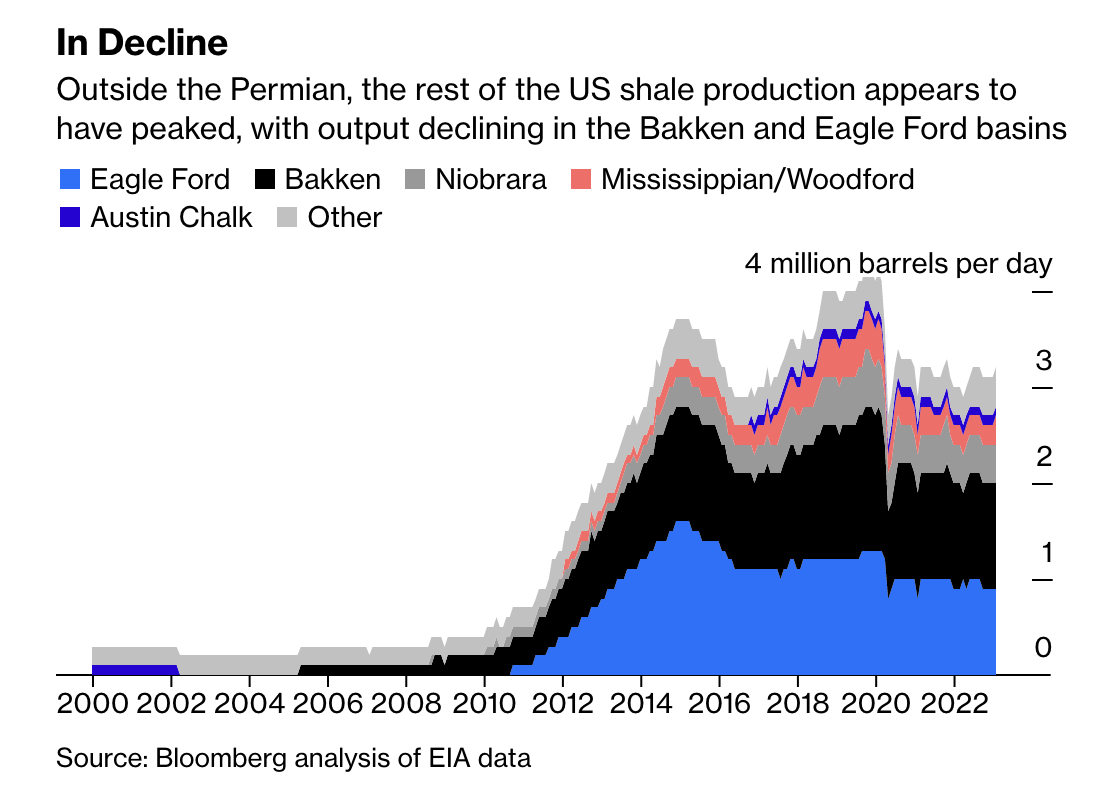

At this point, both the Bakken and Eagle Ford basins have hit peak production, as displayed by the chart below.

{kind=link}

Now, even the Delaware Basin is slowing.

On March 8, the Wall Street Journal reported that frackers are hitting fewer big gushers in the Permian Basin. Major operators are running out of good wells.

Oil production from the best 10% of wells drilled in the Delaware portion of the Permian was 15% lower last year, on average, than top 2017 wells, according to data from analytics firm FLOW Partners LLC. Meanwhile, the average well put out 6% less oil than the prior year, according to an analysis of data from analytics firm Novi Labs.

With that in mind, Bloomberg's energy expert Javier Blas wrote an article highlighting that it's now time for Wall Street to get paid as production growth in the Permian is falling.

{kind=link}

Essentially, he highlighted what I have discussed in various articles as well: the industry is turning from a source of intense capital destruction into a cash cow. I would even make the case that it's the biggest cash cow in North America.

According to Blas (emphasis added):

The go-slow is a business reality. Over the last decade, the US shale industry had become a byword for capital destruction. Shale investors recovered about 50 cents for each dollar they invested during the 2010-2020 period . After riding out the pandemic, the industry is under increasing pressure from impatient stakeholders on Wall Street — the actual embodiment of the financial system, not Midland’s mock version . Shale pioneers once put growth over profit, burning billions of dollars in the process; today, they are focused making money for their shareholders .

While other basins already peaked, it looks like the Permian will peak somewhere in the next five to six years.

This is what non-Permian production looks like:

{kind=link}

At this point, someone can make the case that new drilling technologies in the future can cause production to accelerate again. I agree with that, and I hope it happens, as affordable energy is the basis of every successful economy. However, for the time being, we're stuck with a thesis of slower production growth down the road.

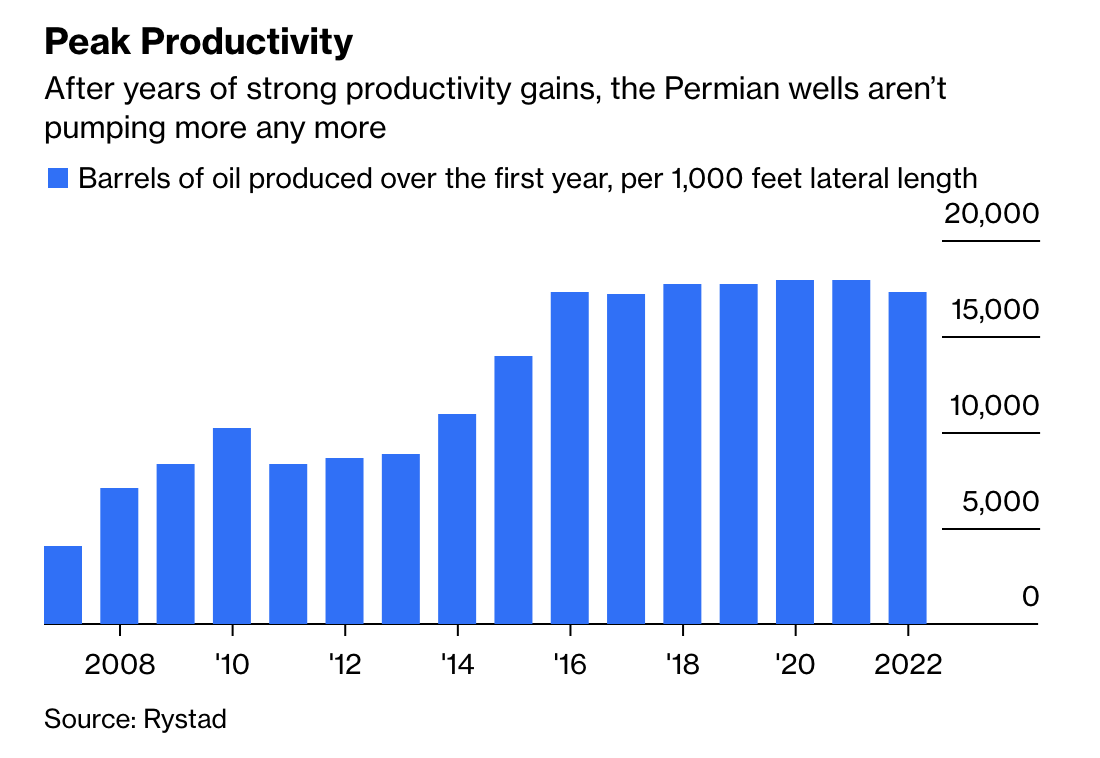

Since 2016, we've not witnessed any productivity gains in the Permian. In 2022, productivity declined for the first time since 2011.

{kind=link}

On a side note, this also shifts power to OPEC, as it will be in a better spot to control prices through production hikes and cuts. This has geopolitical implications.

To quote Mr. Blas again, who perfectly explained why I believe in prolonged above-average inflation:

[...] the tables will be turned: Wall Street is going to profit at the expense of Washington and Main Street. The consequences are likely to be higher oil prices — and inflation — and a weakened hand in energy politics.

Furthermore, we can expect that these developments will accelerate M&A activity. Companies buy peers with high-quality reserves using some of their free cash flow windfalls.

This accelerating M&A trend could lead to the emergence of Shale 4.0, which will be dominated by larger companies such as Exxon Mobil ( XOM ) and Chevron ( CVX ).

However, despite the end of the oil production boom, the industry will adapt and become more focused on profit motives, resulting in better returns for stockholders. This change is similar to the tobacco industry's reduction in capital expenditures, leading to increased profitability.

Although the shale industry will become more domesticated, it will still be a significant force. In 2022, shale contributed to the all-time high of US petroleum output, and it will continue to be the biggest source of additional production worldwide, surpassing countries like Canada, Brazil, and Guyana.

This brings me to my picks.

I'm Going With Cash And Capital Gains

While there are more than three suitable picks in the energy space, I decided to give you three stocks that I consider to be terrific long-term investments.

All of these picks have a few things in common:

- They have high production reserves.

- Efficient production.

- Healthy balance sheets.

- A focus on shareholder returns, including high (special) dividends.

While I am sure that there are stocks on the market that may come with higher capital gains on a long-term basis, I am convinced that dividends are key. In a situation where oil companies are increasingly able to generate high free cash flow, the focus should be on dividends. This also protects investors against the downside of this energy transition, which is a prolonged period of elevated energy prices.

Needless to say, the companies that are able to consistently grow their dividends and/or pay special dividends to distribute their free cash flow are likely to outperform their peers. To me, that's important as well. I want to incorporate a high likelihood of peer outperformance to warrant that we're stock-picking in the first place.

Also, please note that I will provide links to other Seeking Alpha articles for further research.

Canadian National Resources ( CNQ )

This Canadian company has become one of my favorite plays. My biggest mistake was not researching it earlier, as I was somewhat biased against Canadian energy companies - mainly because of its government.

Earlier this month, I finally decided to dive in, and I liked what CNQ has to offer .

- Canadian National Resources is one of the largest oil producers in the world, producing 1.3 million barrels of oil equivalent per day. 72% of this is crude oil and natural gas liquids.

- The company sits on 13.6 billion barrels of oil equivalent in reserves. CNQ estimates that it is sitting on 42 years' worth of reserves. Furthermore, these reserves are consistently rising. In 2022, the company found more new reserves than it pumped out of the ground, resulting in a net addition of reserves.

- The company is breakeven at $40 WTI, which allows for high free cash flow at elevated oil prices.

- After reaching its net debt target of $10 billion this year, the company is looking to distribute up to 100% of its free cash flow to shareholders.

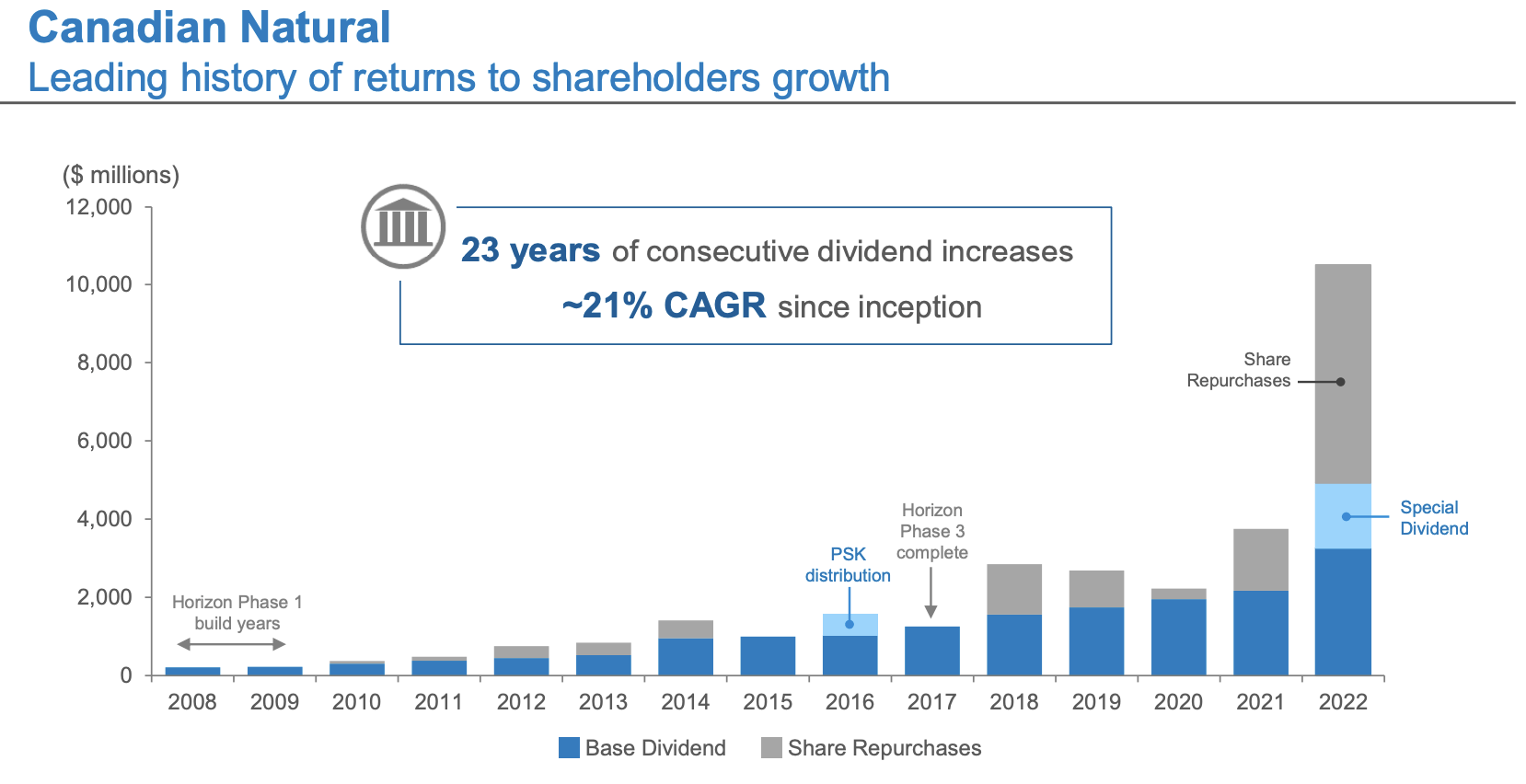

The company has hiked its dividend for 23 consecutive years. Thanks to lower debt levels, it is now using a mix of rising quarterly dividends, special dividends, and buybacks to return cash to its owners.

{kind=link}

In 2022, the company hiked its dividend twice, bringing the total growth rate to 45% to $3.40 per share per year. However, on March 2, the company hiked again (+5.9%), bringing the total to $3.60 per year. This implies a 4.3% yield.

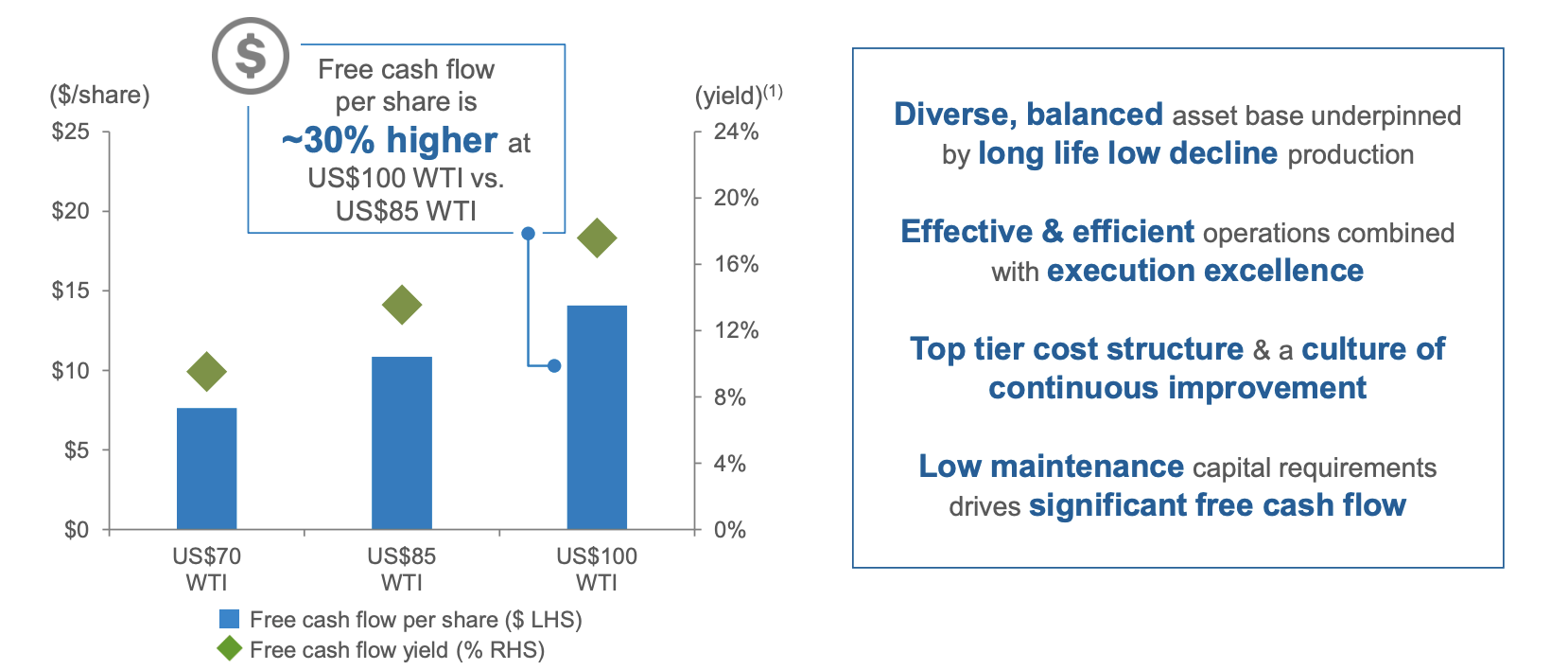

In a $100 WTI scenario, the company could generate an 18% free cash flow yield, which is tremendous news for (special) dividends. The overview below shows that at lower prices, free cash flow is also impressive. Even at $70 WTI, the implied free cash flow yield is close to 10%.

{kind=link}

When it comes to capital gains, CNQ shares have outperformed both the Energy Select Sector SPDR ETF ( XLE ) and the SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ). Please note that I excluded dividends in the chart below (capital gains instead of total returns), as I assume that a big part of energy investors do not reinvest their dividends. So, including dividends, the outperformance would be even more significant.

With all of this in mind, I'm considering combining my CVX and XOM positions to add CNQ. For now, I can still do it tax-free. However, I haven't figured out which one to sell. Once I decide that, I will likely cover it in an article.

Stock number two is smaller, yet not less impressive.

Diamondback Energy ( FANG )

On April 1, I wrote an article covering FANG,

- With a market cap of $25.3 billion, FANG is one of America's largest onshore drillers.

- The company specializes in horizontal development of the Spraberry and Wolfcamp formations of the Midland Basin and the Wolfcamp and Bone Spring formations of the Delaware Basin, both of which are part of the larger Permian Basin in West Texas and New Mexico.

- FANG owns 56% of the limited partner interests in Viper Energy ( VNOM ), a public owner of oil and gas properties. FANG is its largest client.

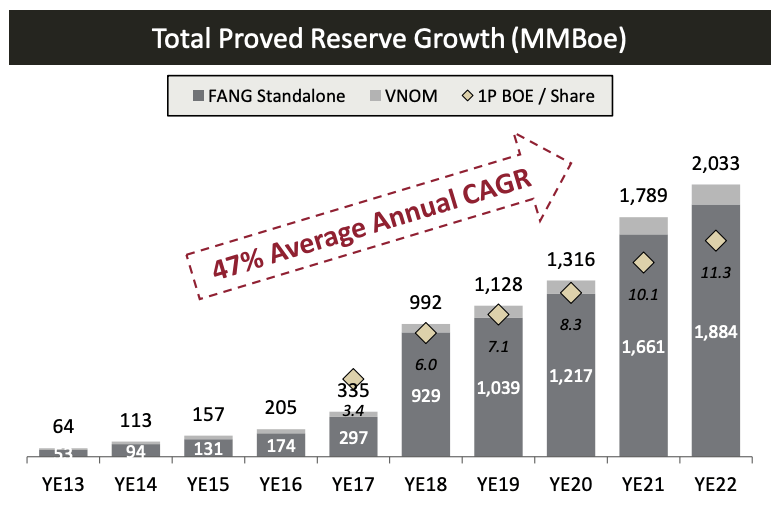

- The company is sitting on $2.0 billion barrels of oil and gas reserves. In 2022, these reserves rose by 14%. 30% of these reserves are untapped. 53% of these reserves consist of oil.

{kind=link}

- This year, FANG is expected to boost production by 16%, which requires 34% higher capital spending.

- The company ended 2022 with a net leverage ratio of just 0.1x EBITDA. Less than 20% of its debt is maturing within five years.

- FANG also benefits from operations. At $40 WTI, the company can cover its base dividend with a 2.4% yield, which is impressive.

- The company consistently hedges between 50% and 60% of its production. This somewhat limits its upside, but it also protects its dividend.

Just like CNQ, the company has high free cash flow at elevated oil prices. As I wrote in my prior article (emphasis added):

At $80 WTI, the company estimates to have a free cash flow yield of almost 15% . This implies that returns to shareholders will be close to 11% . Please note that the current stock price is at levels that were used for these calculations in February. Oil prices of $100 could lead to returns close to 14% of the company's market cap .

On February 21, the company announced a quarterly dividend of $0.80, which is 6.7% higher compared to the prior-year quarter. The company also paid a $2.15 special dividend. This brings the annualized dividend yield to 8.4%.

Furthermore, like CNQ, the stock outperformed its peers in the past ten years, even excluding dividends.

I expect this outperformance to continue.

Devon Energy ( DVN )

Like CNQ and FANG, Devon Energy is a candidate that has decided to reward its investors by distributing most of its free cash flow using regular quarterly dividends and special dividends.

Earlier this month, I wrote an article titled From Tight To Tighter: Why Devon Energy Could Double .

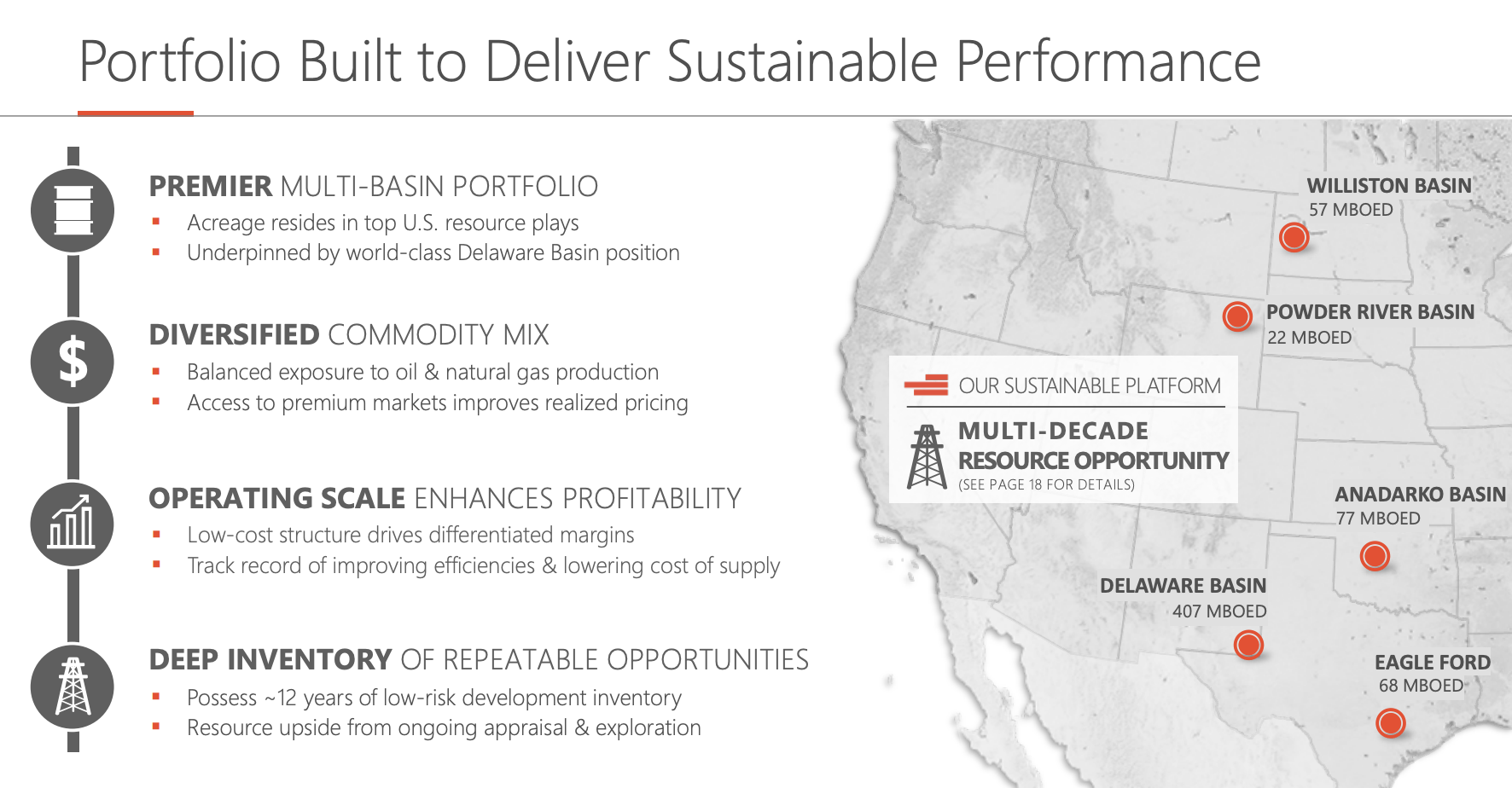

- This year, Devon is looking to produce 643 thousand barrels of oil equivalent per day. Half of it is expected to be oil. The big majority is produced in the Delaware Basin.

{kind=link}

- The company has more than 20 years of unrisked inventory, which incorporates reserves with tighter spacing that will require more investments. It has 12 years' worth of reserves at the current activity pace.

- The company is breakeven at $40 WTI. The company was breakeven at $30 WTI prior to the upswing in inflation. That's not bad news, as it impacted the entire industry. If anything, it shows the increasing challenges to boosting oil production, which proves what we discussed in the first half of this article.

- DVN has a very healthy balance sheet with a net leverage ratio of 0.5x EBITDA and a BBB credit rating.

Now, the company is in a terrific spot to distribute most of its free cash flow to shareholders.

Our strong investment-grade financial position provides us the opportunity to return more free cash flow to shareholders and be less aggressive on debt reduction.

The company's Board of Directors establishes a quarterly dividend that aims for around 10% of its operating cash flow. Apart from this, the company may provide a variable dividend of up to 50% of its extra free cash flow.

The company recently raised its fixed dividend by 11% to $0.20 per quarter on February 14. However, due to lower oil prices, the variable dividend was reduced by 34% to $0.89. As a result, the expected annual forward yield is 8.2%.

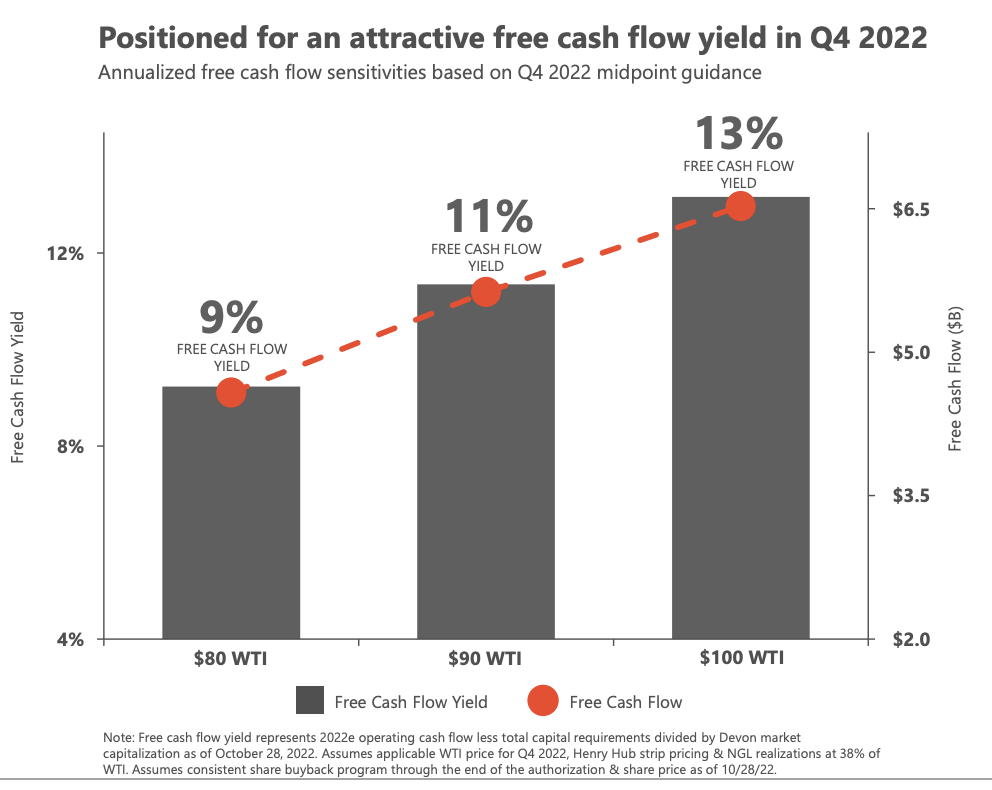

So, what can we expect in terms of future dividend payments? If oil prices average $90 WTI, the company has an implied free cash flow yield of 11%. That number rises by 200 basis points in the event of $100 WTI.

{kind=link}

With that said, while DVN has outperformed its peers by a mile since 2020, it has slightly underperformed the XLE ETF over the past ten years. This was mainly due to severe weakness prior to the current upswing in oil. The company had a high debt load, and the shale industry was in a very tough spot.

Going forward, I expect DVN to continue what it started in 2020: outperforming its peers.

Before I end this article, I want to mention a few sentences regarding volatility.

Risks To Keep In Mind

While I believe that having energy exposure is important to protect one's income and wealth against inflation, investors do need to be aware that energy tends to be extremely cyclical. I have the feeling that a large majority of readers know the risks. However, some tend to go too far when they see investments they like.

Especially if you plan on holding energy stocks on a long-term basis, you will go through some ups and downs.

Takeaway

In this article, I updated my thesis that oil production is peaking. The United States, the engine of post-Great Financial Crisis oil supply growth, is running out of steam. The Permian is the only region with growth left, which is likely to change in the next few years. This could (read: will) have a major impact on energy prices down the road, especially if cyclical demand growth returns.

Hence, I presented three oil stocks that are in a good spot to protect investors against prolonged elevated energy prices. All of my picks come with high production reserves, healthy balance sheets, efficient production, and dedicated management to return most of their free cash flow to shareholders.

I expect these picks to outperform their energy peers and deliver high dividends for many years to come.

For further details see:

Energy Crisis: 3 Oil Stocks That Get You Paid Handsomely