ETRN - Energy Income Weekly: Improving Oil Market Fundamentals To Drive Energy Outperformance

2023-04-06 03:34:18 ET

Summary

- The energy sector gained 6.3% in response to surging oil prices and improving oil-market fundamentals.

- Oilfield services was the best-performing energy sub-sector.

- With energy fundamentals likely to improve over the coming months, energy equities are set to outperform.

Energy Income Performance

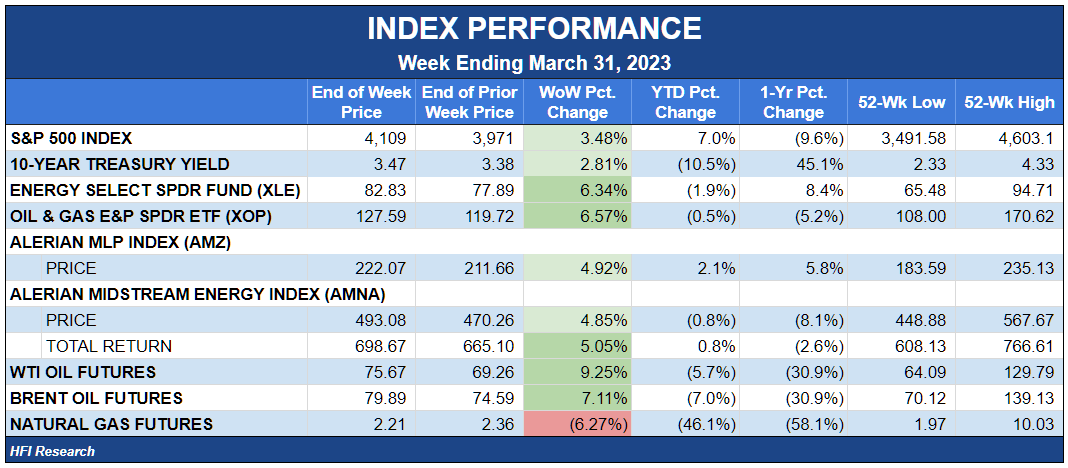

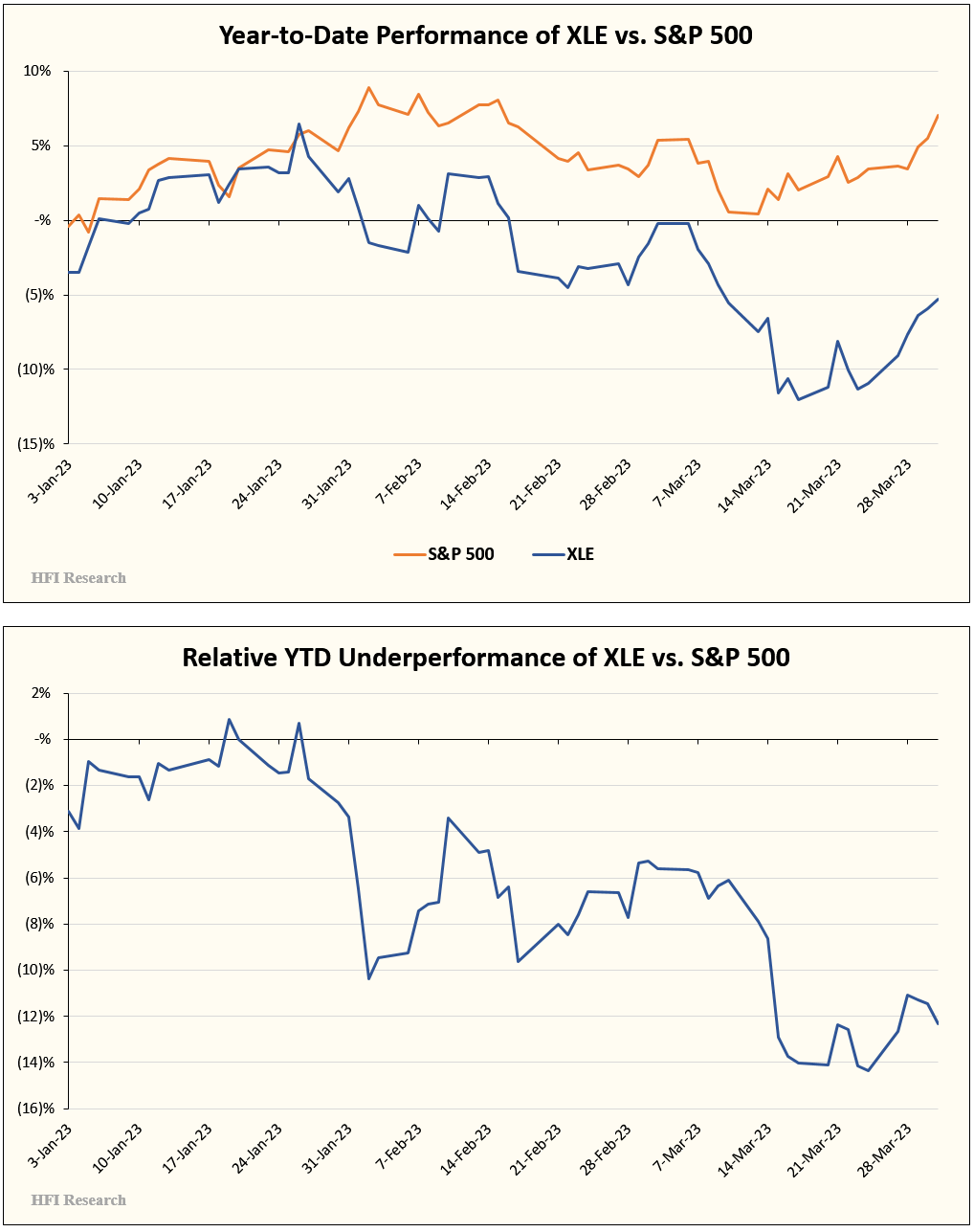

Energy stocks got the green light to rally as oil prices broke out of their multi-month downtrend to end the week at $75.67, above key resistance at $74.55. Positive fundamentals and diminishing macro fears of a metastasizing banking crisis drove the energy sector ( XLE ) up 6.3% for the week. Oilfield services and E&Ps saw the biggest gains and were up 7.7% and 6.6%, respectively. Midstream trailed but posted a respectable 4.9% gain. All sectors outperformed the S&P 500, which rose 3.5% during the week.

{kind=link}

Despite the energy sector's outperformance, it continues to lag well behind the S&P 500 year-to-date. The culprit has been a mixture of weak oil and natural gas fundamentals and risk aversion in the wake of the banking sector's woes.

{kind=link}

We expect energy fundamentals to strengthen over the coming months, which should cause energy names to outperform. Whether the outperformance will arrive through the energy sector falling less than or gaining more than the S&P 500 we can't say, but we believe the relative setup for energy equities from current levels is as constructive as it's been all year.

This week we began work on the oilfield services subsector. It's the first time we've taken a close look at the sector since 2017, and we like what we see. The sector has underperformed the other subsectors since the overall energy sector bottomed in 2020, and we believe it's poised to outperform the other subsectors this year and potentially beyond.

Our favorite niche within oilfield services is the offshore segment. Unlike much of onshore oilfield services, offshore is characterized by large barriers to entry and ownership of longer-lived assets, most of which date from the previous cyclical upcycle in the 2009-2014 timeframe. Importantly, offshore is undergoing a dramatic improvement in bargaining power versus customers. We expect that trend to continue. Since most offshore services companies have high fixed costs, earnings and cash flow surge higher as offshore services contract prices rise. These dynamics can bring about multi-bagger returns for some offshore names over the next few years.

We began our oilfield service coverage with Transocean ( RIG ), which could more than double amid a sustained cyclical increase in dayrates. No doubt there are other attractive opportunities among offshore oilfield service equities, and we'll continue our hunt for them over the coming week.

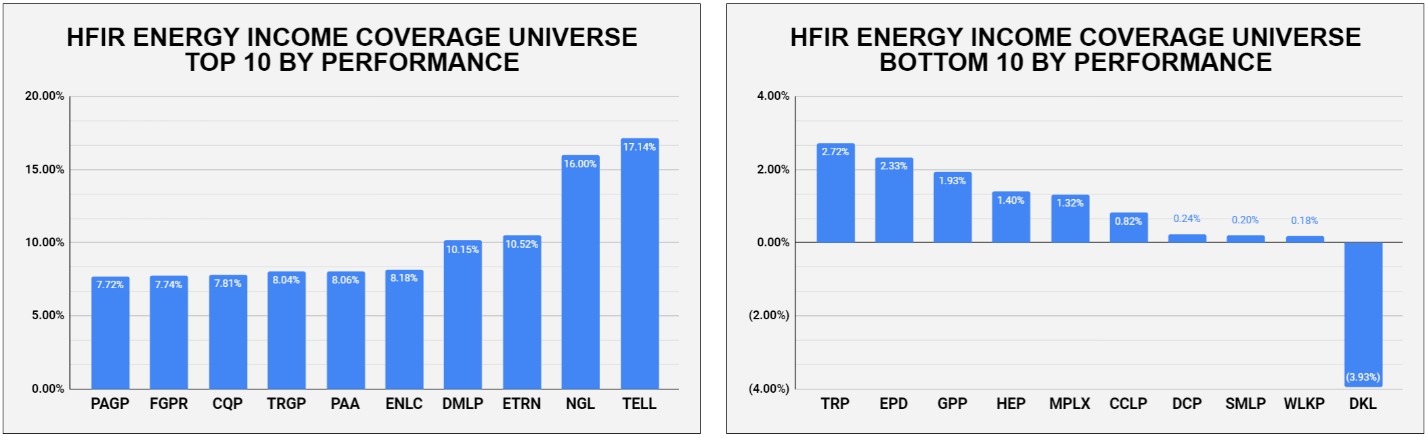

Low-Quality Names Lead the Way Higher

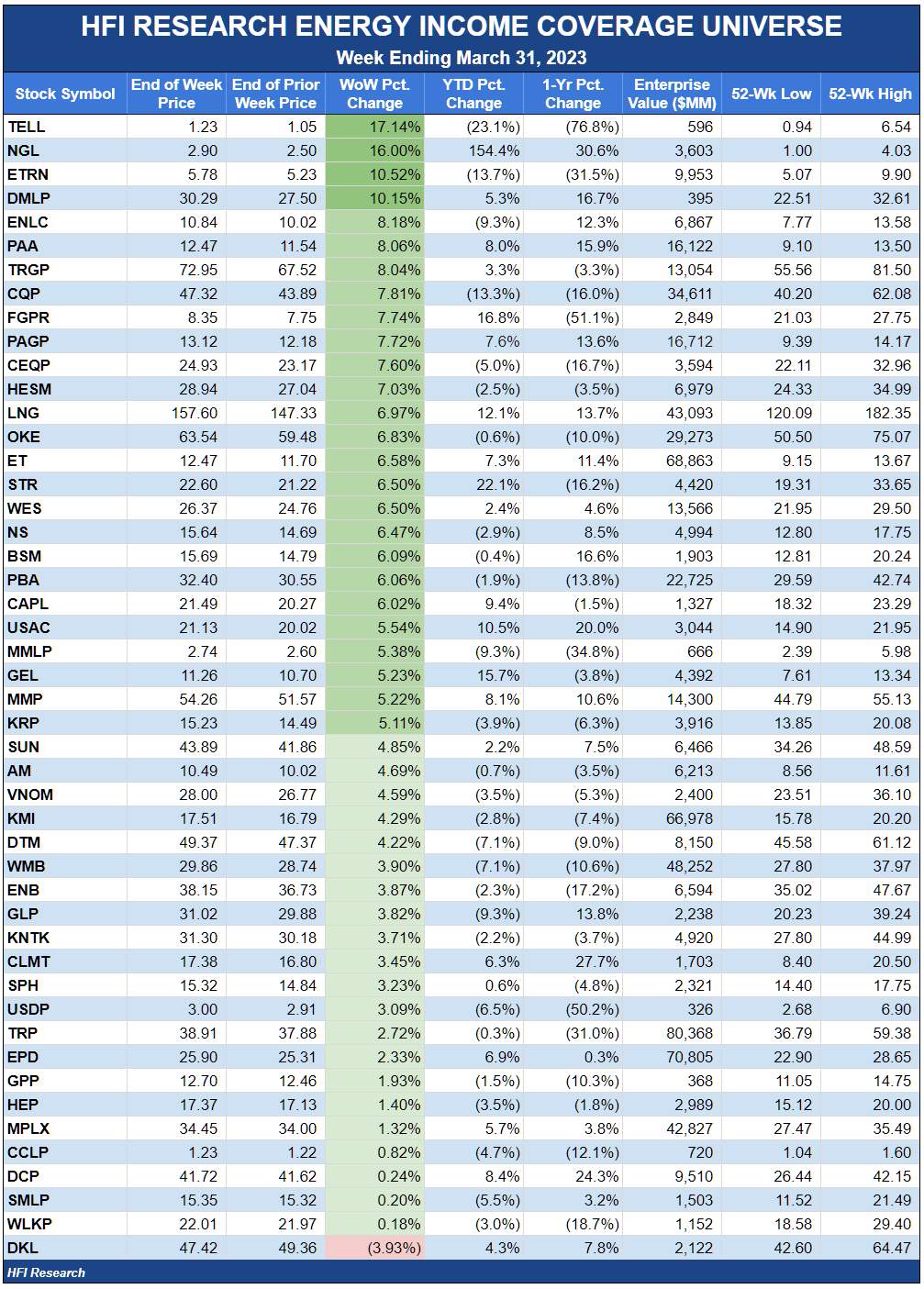

The week saw a massive relief rally in the lowest-quality energy names. Tellurian ( TELL ) was the biggest gainer with a 17.1% pop on no news after a 50% decline from January highs. Tellurian will be in trouble if it can't secure financing for its Driftwood LNG project. We recommend staying away from the shares and rate TELL a Sell.

{kind=link}

Like TELL, NGL Energy Partners ( NGL ) snapped back on no news after a string of weekly losses. Higher oil prices make it likely that U.S. shale oil production will continue to grow, which would benefit NGL's water business, its main growth engine and source of deleveraging. Also like TELL, we recommend avoiding NGL due to management's poor capital allocation track record and the low return on capital generated by NGL's assets.

Equitrans Midstream ( ETRN ) shares were the third biggest gainer during the week, rising 10.5% after the U.S. Fourth Circuit Court of Appeals denied a motion by Mountain Valley Pipeline ((MVP)) opponents to reverse a water protection permit issued by the Virginia Department of Environmental Quality. The ruling made it clear that the permit was issued in good faith with sufficient due diligence.

We flirted with the idea of initiating a position in ETRN, as we have several times in the past. Each time we decided against it due to the persistent opposition of the Fourth Circuit Court, and each time that has been the right call. While this week's ruling by the court offers a ray of optimism, the court has yet to rule on a similar challenge regarding the MVP's West Virginia water permit. Observers of the case noted that ETRN made a poor showing when presenting its West Virginia case to the court. We believe the odds favor the court siding with ETRN's opponents, as it has in all but one decision over the past few years. If it rules against the MVP, it will further delay the project and could imperil its completion prospects. With this risk looming over the project, a wait-and-see posture remains the best course. However, if the court rules in favor of ETRN, we would likely be a buyer of the shares below $7.00.

Other big gainers during the week were operators with more direct oil price exposure. Plains All American ( PAA ) gained 8.1%. The EIA's report on Friday that U.S. oil production rose in January to the highest levels since March 2020 was positive for PAA, as it confirms that Permian growth remains intact. PAA will continue to deleverage this year, and we see greater returns of capital to equity holders in 2024 and 2025. We rate PAA and PAGP equities as Buys.

Targa Resources ( TRGP ) benefitted from the rise in oil prices, which will support the NGL prices to which it has direct exposure. TRGP remains one of the best growth stories among public midstream equities. At Friday's closing price of $72.95, the shares have 20% upside to our $87.50 price target. We rate TRGP shares a Buy.

The only loser during the week was Delek Logistics Partners ( DKL ), which fell 3.9%. DKL has behaved like a defensive equity during the previous weeks' swoon. Its relative price strength was surprising due to the company's rather high leverage, which debt to EBITDA of around 5-times, as well as its aggressive, expansion-oriented management. Given DKL's relative outperformance over previous weeks, we're not surprised that it didn't participate in the sector's rebound.

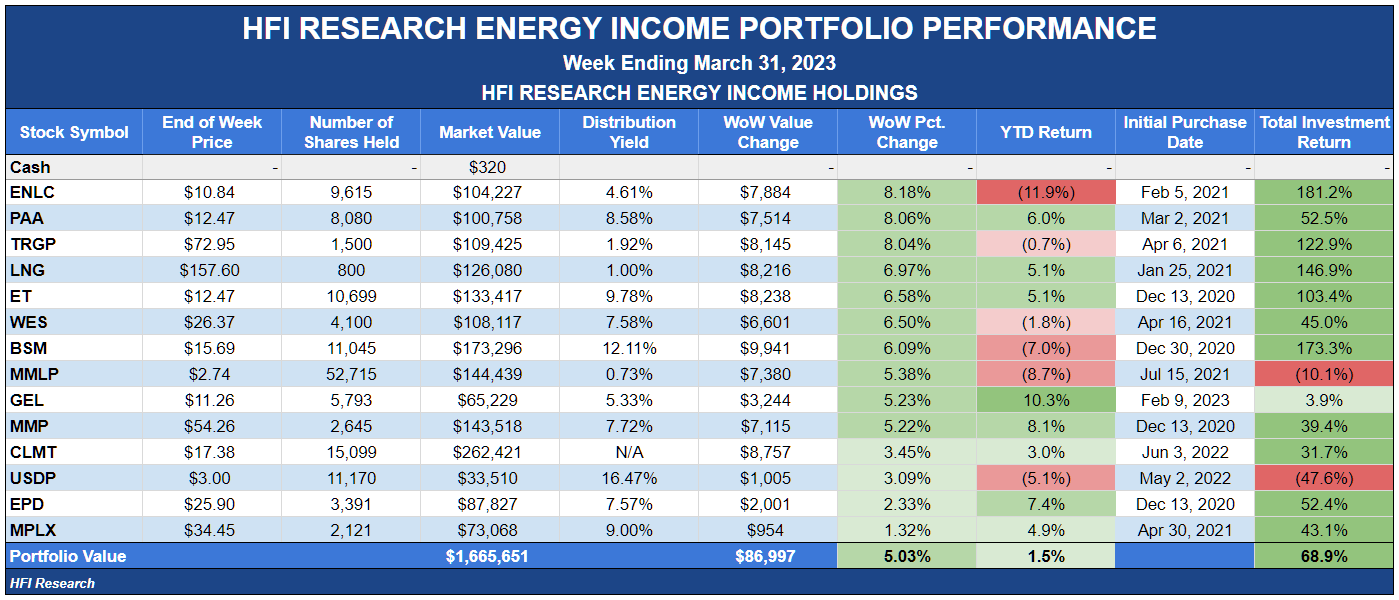

Weekly HFI Research Energy Income Portfolio Recap

Our portfolio was basically flat with its benchmark, the Alerian MLP Index, during the week.

{kind=link}

Our holdings traded in step with broad price momentum. Those exposed to commodity prices performed the best, with EnLink Midstream ( ENLC ) the top performer, up 8.2% after trading lower in previous weeks as oil and natural gas prices sold off.

Cheniere Energy ( LNG ) shot 7.0% higher in response to improved natural gas and LNG prices. The shares continue to be undervalued and offer 14% upside to our $180 price target.

Western Midstream Partners ( WES ) was up 6.5%. The units had underperformed in recent weeks, as WES was the only holding in our portfolio that disappointed on fourth-quarter earnings. WES units are too cheap, with 24% upside to our $32 price target and an attractive 7.6% distribution yield. WES's operational and financial results gain stability from having Occidental Petroleum ( OXY ) as an anchor customer. OXY will continue its pace of development in the Permian, and we believe it's only a matter of time before it steps up development in its DJ Basin acreage. Higher DJ Basin throughput volumes would be a significant benefit for WES's EBITDA growth.

Black Stone Minerals ( BSM ) units have been on a wild ride in 2022, and this week was no exception. BSM gained 6.1%, following the outperformance of royalty companies more generally. BSM's Shelby Trough operator, Aethon Energy, is well-hedged on its natural gas exposure but could pull rigs if natural gas prices stay low, which would hurt BSM's results. Still, BSM's longer-term outlook is strong given the prospects for domestic natural gas production over the coming years. BSM units have 18% upside to our $18.50 price target.

Energy Transfer ( ET ) units were also strong after the company announced its acquisition of Lotus Midstream for $1.45 billion. Consideration will consist of $900 million of cash and approximately 44.5 million newly issued Energy Transfer common units. A contact informed us that the deal came at a 7-times EBITDA multiple, which is in line with recent gathering and processing asset sales. Given the terms and the current discounted price of ET relative to value, the deal will be only slightly dilutive for unitholders unless management can grow the Lotus assets' earning power after the acquisition.

These kinds of deals are par for the course with an expansionist company like ET. We expect more in the future. Unless they're egregiously dilutive, they won't impact our estimate of ET's intrinsic value or our $15.25 ET price target. We rate the units a Buy and expect them to trade up to our price target over the next year or two.

Enterprise Products Partners ( EPD ) units trailed the sector, gaining 2.3% despite the company hosting its annual Analyst Day, where management demonstrated the company's operating and financial prowess.

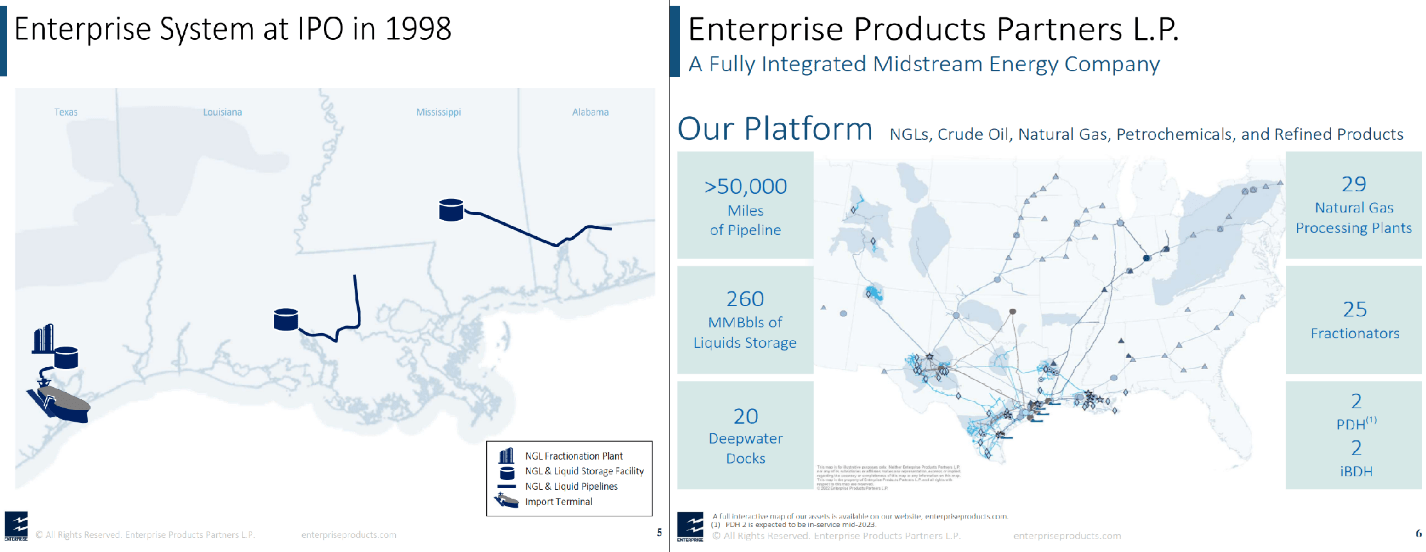

This extraordinary company doesn't get the credit it deserves from the market. Its Analyst Day presentation began by showcasing EPD's evolution from its origins as a localized NGL storage and transportation system at the time of its 1998 IPO to the premier midstream heavyweight with sprawling operations up and down the oil and gas value chain.

{kind=link}

EPD remains one of the cheapest large-cap equities in the stock market today, particularly when its competitive advantages, overall business quality, and returns on capital are factored in relative to its units' trading metrics. We're committed long-term holders and believe the units are a necessary part of an energy income portfolio. We reiterate our EPD Buy rating and $29 price target.

News of the Week

March 28. Hess Midstream ( HESM ) announced the repurchase of $100 million of Class B shares from its sponsors, Hess Corporation ( HES ) and Global Infrastructure Partners. The repurchase will involve 3,619,254 Class B shares at a price of $27.63. While we commend management on once again allocating capital for the benefit of public equity owners, we believe the announced purchase price comes too close to HESM's intrinsic value for comfort. A company that repurchases its stock at intrinsic value is simply exchanging dollar bills for an asset priced at 100% on the dollar. It's not value accretive for shareholders. We would rather see management distribute capital than repurchase equity that trades around intrinsic value, particularly for MLPs. HESM's staunch dedication to repurchases increases the risk that management will repurchase large blocks of equity from its sponsors at prices in excess of intrinsic value, which would reduce HESM's equity value per share.

March 29 . Global Partners ( GLP ) signed an agreement with Exxon Mobil ( XOM ) to form a joint venture to acquire 64 Houston-area gas stations from the Landmark Group, marking GLP's expansion outside of its Northeast and mid-Atlantic base and into the Houston area. The deal's terms weren't disclosed. It's our view that GLP has been managed in a way that favors its founding Slifka family's interests over those of public unitholders. We recommend that investors who seek income-generating equities look elsewhere.

Capital Markets Activity

March 30. Western Midstream Partners ( WES ) used the recent drop in interest rates to price an offering of $750 million of 6.150% senior notes due 2033 at 99.728% of par. It plans to use the proceeds to repay borrowings under its revolving credit facility and for general partnership purposes.

March 30. EnLink Midstream ( ENLC ) announced the pricing of $300 million of 6.500% senior notes due 2030 at 99.0% of par. ENLC plans to use the proceeds to repay outstanding borrowings on its revolving credit facility.

{kind=link}

For further details see:

Energy Income Weekly: Improving Oil Market Fundamentals To Drive Energy Outperformance