AMNA - Energy Income Weekly: Opportunity Is Knocking

2023-04-27 18:56:05 ET

Summary

- It was a tough week for the energy sector, with commodity-exposed names underperforming.

- We’re pounding the table for buying equities with oil price exposure for both income and capital appreciation.

- Kinder Morgan kicked off midstream earnings season with strong results.

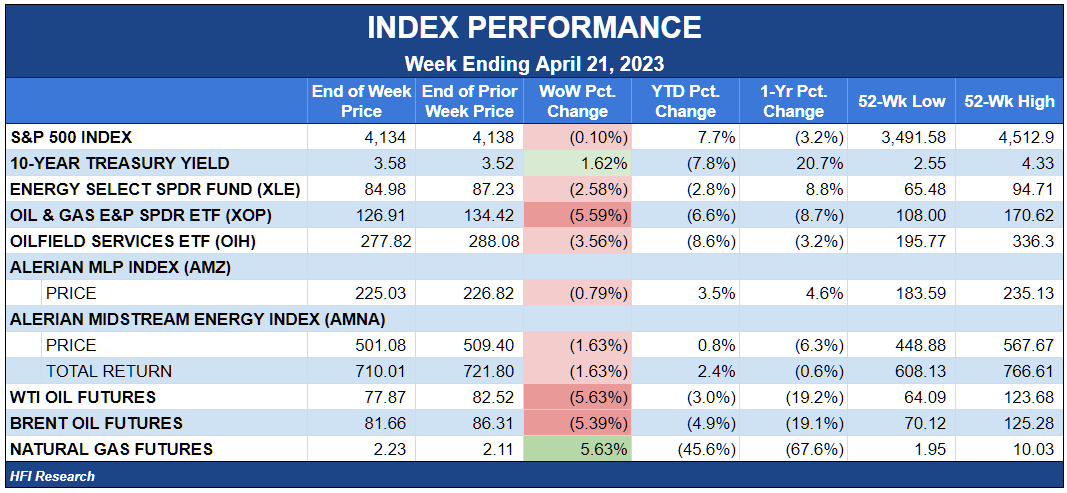

Energy Income Performance

Energy stocks traded lower as oil prices lost the gains they posted after the surprise OPEC production cut announced on April 2. WTI declined by 5.6%, pushing the E&P-weighted XOP ( XOP ) lower by 5.6% and the oilfield services sector, as represented by the OIH ( OIH ), down 3.6%. Midstream was the strongest performer, with the Alerian Midstream Energy Index ( AMNA ) falling 1.6%.

{kind=link}

The past few months have been an endurance test for oil bulls. The experience reminds us of what it was like to hold oil stocks before 2020. At the time, our bullish oil thesis was gradually being validated by incoming data, but the investing public was so indifferent to energy stocks that it wasn’t reflected in energy stock prices. Oil stock drifted about, with no consideration paid to the increasingly bullish fundamental tailwinds that were gaining momentum.

Only after massive global inventory draws forced prices higher were investors convinced that energy stocks had value.

Today’s experience is similar. While we can be gratified that oil prices are well above their pre-2020 averages and that the investing public is attuned to the macro energy supply issues, still, nobody seems to care about the bullish prospects for oil-related stocks. Instead, investors remain fixated on the prospects for a recession and what it has meant for oil stocks in the past.

For this reason, we’re as bullish now as we’ve been since 2020. Back then, we knew our oil stocks had a huge upside amid higher commodity prices—which we believed were imminent—but a multitude of macro unknows clouded the outlook.

This time around, we’re better equipped. Consider, for instance, that we now know:

- oil consumption begins to meaningfully fall when the sum of crude oil prices plus the refining margin per barrel rises above $150 per barrel;

- oil consumption is simulated when crude oil prices plus the refining margin per barrel falls to below $90 per barrel;

- U.S. shale’s days of mega growth are gone.

On the company-specific level, we now know how financial results look at $100 per barrel oil, and we can be confident that management will deliver the cash flow generated at higher prices to shareholders.

All of these factors had been the primary “known unknowns” that oil bulls had to contend with before 2020. As such, they remained risks to a bullish oil thesis and had to be constantly monitored.

Today, the course for oil bulls is clear. OPEC+ is in control of marginal crude supply, and the group is as incentivized as ever to keep oil prices high. The most influential OPEC+ members need high oil prices to fund war and defense budgets, placate potentially restive domestic populations, diversify their economies, and so on.

Given the incentives at play, we’re confident that OPEC+ will drain inventories to levels that put upward pressure on oil prices. The group was determined to reduce inventories throughout 2020 and 2021, and it succeeded with flying colors. We have no reason to doubt its determination and ability to succeed once again in 2023.

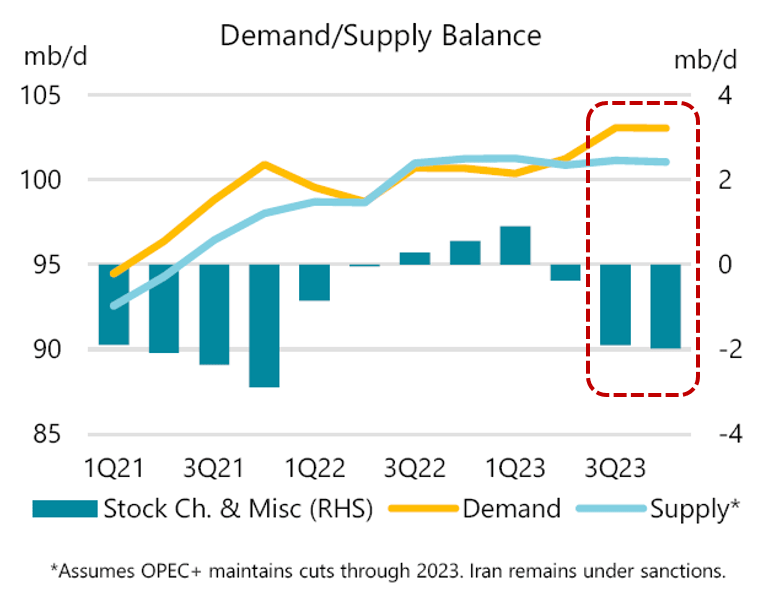

We keep coming back to this chart, namely, the IEA’s supply/demand forecast.

{kind=link}

Source: IEA Oil Market Report, April 14, 2023. Red-dotted line added by author.

This forecast can be wrong by more than half and oil prices will still shoot higher. We discuss the inventory outlook in greater depth here .

If seasonal patterns hold, the supply deficit in the second half of 2023 will fall by roughly 1 million bpd in the first quarter of 2024 as demand falls. However, demand will pick back up in the second quarter and steadily increase thereafter, which will grow the supply deficit in the absence of additional supply. We believe it is likely that the supply deficit will remain in effect in 2024 unless oil prices increase to a level that either reduces demand and/or induces OPEC+ to increase supply.

With this supportive macro backdrop, we can make firmer investment decisions about what to buy, when to buy, how long to hold, and when to sell.

This Week’s Underperformers Are Buys

During the week, energy equities responded to falling oil prices. True to form, those with greater commodity price exposure underperformed. Recall that the most heavily traded oil futures contracts—which set the widely-cited “oil price”—expire in a few months, whereas oil-related equities are entitled to a company’s residual cash flow indefinitely. The mismatch between the stock market’s pricing of oil equities and the futures market’s pricing of short-lived crude contracts is a source of opportunity.

As we head into the second half of the year, oil futures contracts will be responding to the growing demand from refineries for supply, which will grow increasingly scarce. This dynamic will dominate how oil prices are set regardless of speculative positioning. Investors should buy now, while equity and oil prices are soft, in anticipation of higher prices in the second half.

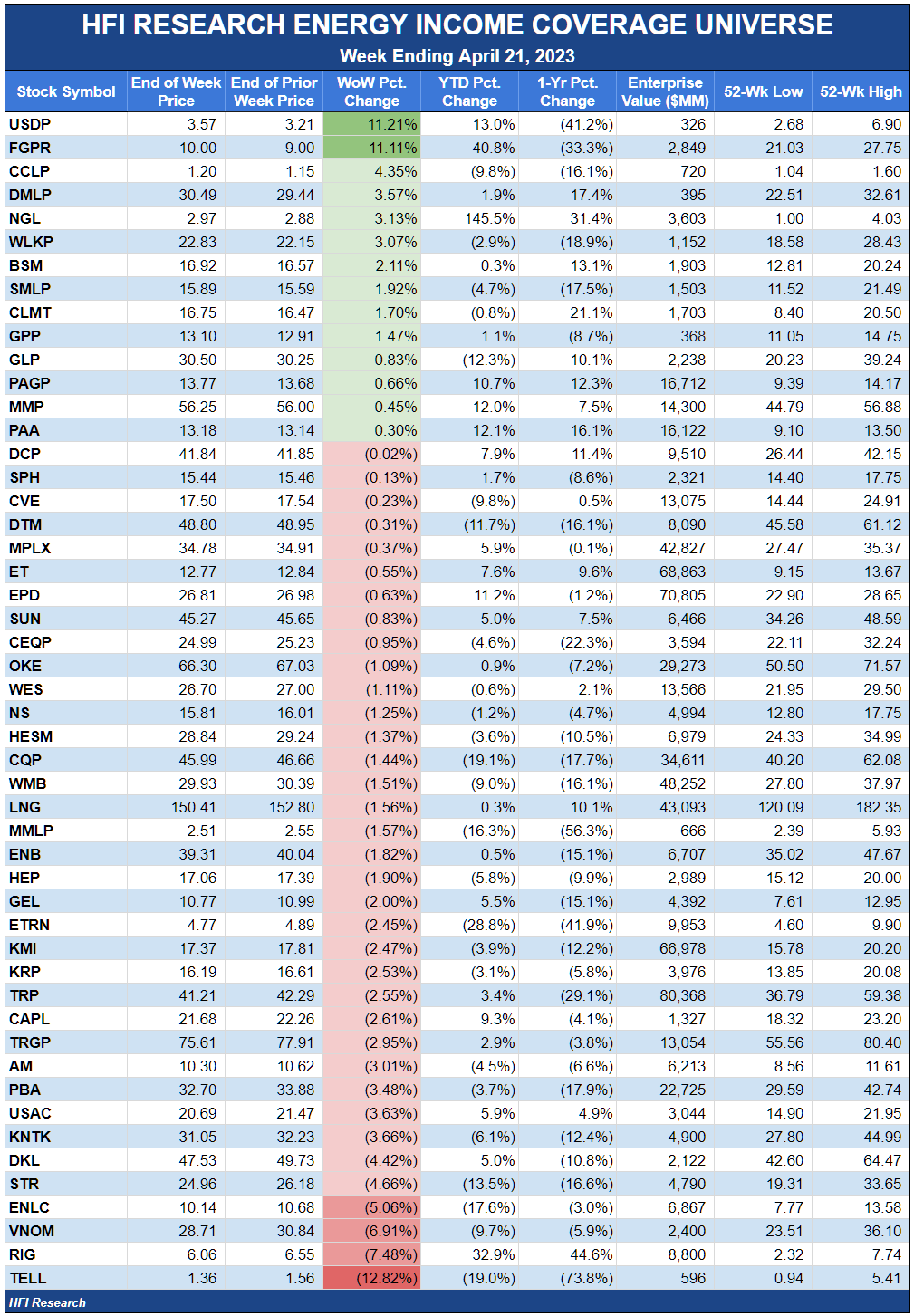

Among income equities, we recommend royalty trusts, which have performed poorly so far this year. Viper Energy Partners ( VNOM ) shares were down 6.9% during the week, the third-worst performance in our coverage universe. VNOM is one of the best-positioned and best-managed royalty trusts, with crude oil accounting for approximately three-quarters of its production volumes. The shares, currently at $28.71, have a 36% upside to our $36.00 price target. Kimbell Royalty Partners ( KRP ) was down 2.5% this week, which is a good opportunity to scoop up the discounted units. Our price target for KRP is $22.50, 39% above its current price of $16.19.

Genesis Energy ( GEL ) was down 2.0%. The units have a 39% upside to our $15.00 price target. We hold the units in our HFI Research Energy Income Portfolio and are considering adding to the name. GEL equity will benefit first from debt reduction and then from its outstanding long-term prospects at increasing throughput in its Gulf of Mexico midstream assets. We expect distributions to increase after leverage is reduced to management’s target in 2024. In the meantime, unitholders are paid a 5.6% yield to wait for fundamentals to improve.

As for equities with an appreciation upside to higher oil prices, Cenovus Energy ( CVE ) is in the penalty box after disappointing fourth-quarter results and pushing back the arrival date of stepped-up dividends and share repurchases. CVE is well-managed and stands to generate nearly $6 per share of free cash flow with oil at $100 per barrel. At that price, we estimate the shares are worth at least $35, double Friday’s closing price of $17.50.

Transocean ( RIG ) was the second-worst performer in our coverage universe during the week, with its shares falling 7.5%. We believe that aside from E&Ps, offshore oilfield services is the second-best positioned segment of the energy sector amid sustained higher oil prices over the next few years. RIG’s higher debt load relative to peers gives it the most financial torque to higher dayrates. We estimate the shares can trade to $15 in the current cycle, which implies nearly 150% upside from their current price of $6.06. Deepwater offshore activity has improved significantly over the past eighteen months, and the improvement is set to continue. This week, Schlumberger’s ( SLB ) management mentioned that offshore activity is surprising to the upside on SLB’s first-quarter earnings conference call. We believe dayrates will hit $500,000 beginning next year. As RIG recontracts at higher rates, it can pay down debt, making it easier to pay down and/or push out its earliest maturities in 2026 and 2027. Once debt is reduced, the company can initiate a dividend.

A Quiet Week for Energy Income

Kinder Morgan ( KMI ) was the first midstreamer to report first-quarter earnings. We reviewed its results here . The company beat analyst expectations, providing a good read-through for Williams ( WMB ) and Oneok ( OKE ), which we expect to post strong first-quarter results in light of KMI’s performance.

It was otherwise quiet on the news front. Things will heat up over the coming weeks as first-quarter results come in.

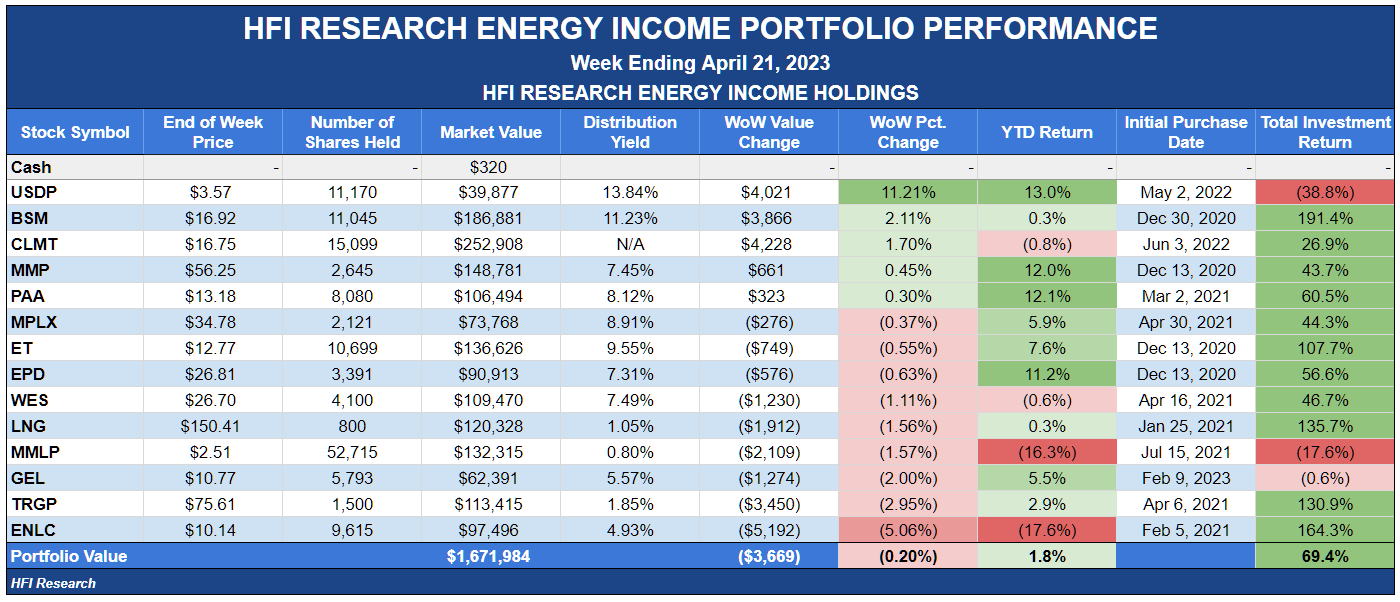

Weekly HFI Research Energy Income Portfolio Recap

Our portfolio declined 0.2% during the week, outperforming its benchmark, the Alerian MLP Index, by 0.4%.

{kind=link}

Our portfolio outperformed because our larger positions held up better than our smaller ones, which fell more in percentage terms.

USD Partners ( USDP ) was our best performer during the week on no news. We hope to hear from management about new DRUbit by Rail contracts soon.

Black Stone Minerals ( BSM ) was up 2.1%. The company declared a $0.475 distribution for the first quarter, flat with the fourth quarter and 19% above the year-ago quarter. BSM units currently trade at an 11.1% yield. We suspect the high yield, strong hedge book, and Aethon’s commitment to maintaining production on BSM’s Shelby Trough acreage are the reasons for the units’ outperformance.

Calumet Specialty Products Partners ( CLMT ) announced that its Montana Renewables facility is operating at its design throughput capacity. Since CLMT units have failed to respond to this obviously bullish news, its investment thesis has become a “show me” story, as the market is unconvinced that Montana Renewables will generate the amount of cash flow claimed by management. Management has executed superbly on transitioning CLMT’s crude oil refinery in Great Falls, Montana, to produce as much as 15,000 bpd of renewable fuels. We expect it to execute similarly well on the financial front. If it does, Montana Renewables will double companywide EBITDA. Our $30 price target implies 79% upside from the current unit price of $16.75.

Martin Midstream Partners ( MMLP ) reported strong first-quarter results, though its units declined by 1.6% during the week. The week’s price action is silly, and we believe the lack of interest in the name provides an attractive buying opportunity for those with a multi-year investment horizon.

Targa Resources ( TRGP ) and EnLink Midstream ( ENLC ) were both weak in spite of the 5.6% bump in natural gas prices. ENLC shares are likely to perform well as oil prices get traction over the coming months. TRGP, meanwhile, is one of the best-managed midstream operators, particularly with regard to capital allocation. Last week, the company boosted its quarterly dividend by 43%. We believe TRGP shares should be a part of every energy income portfolio.

News Of The Week

April 20. The FERC approved NextDecade’s ( NEXT ) Rio Grande LNG Terminal and Rio Bravo Pipeline. New LNG facilities such as this one will provide a boost to U.S. natural gas demand over the next few years, which, in turn, will benefit gas-weighted midstream operators. The news also represents a welcome defeat for the Sierra Club and other well-funded groups dedicated to obstructing the buildout of natural gas infrastructure that is an essential part of an economically viable transition toward electrification.

Capital Markets Activity

None.

{kind=link}

For further details see:

Energy Income Weekly: Opportunity Is Knocking