ETRN - Energy Income Weekly: The Risk-On Trade Prompts A Dash To Low-Quality Equities

Summary

- Energy equities shook off declining commodity prices to end the week with a gain.

- Low-quality names caught a bid from the "risk-on" trade.

- Natural gas-weighted names underperformed as the commodity plunged 10%.

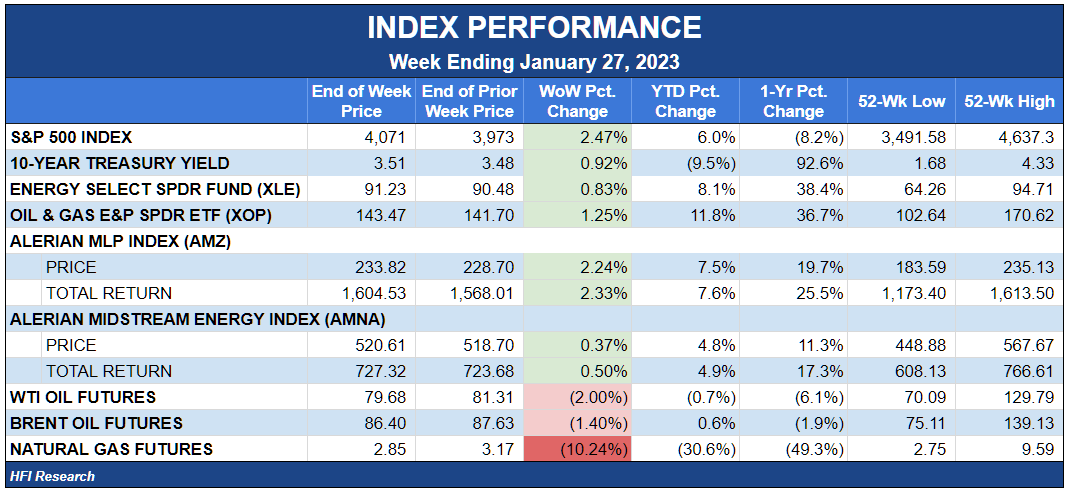

Energy Income Performance

The S&P 500 surged 2.5% during the week amid positive economic data and investor anticipation of a Fed pause. Interest rates rose slightly but remained below recent highs and without the volatility seen in recent months. The 10-year Treasury yield gained 0.9% to end the week at 3.5%.

{kind=link}

Energy income equities caught a tailwind from the rise in the general market. The broad midstream sector rose 0.5%, and MLPs outperformed with a 2.3% gain, despite the week’s 2.0% decline in WTI and 10.2% plunge in natural gas. Based on our recent conversations with generalist fund managers, we’re sensing an upswing in enthusiasm for energy names, both from investors seeking the “hot new thing” after the sector’s unprecedented 2022 outperformance and from those who appreciate the bullish long-term setup for energy commodity fundamentals, particularly for crude oil.

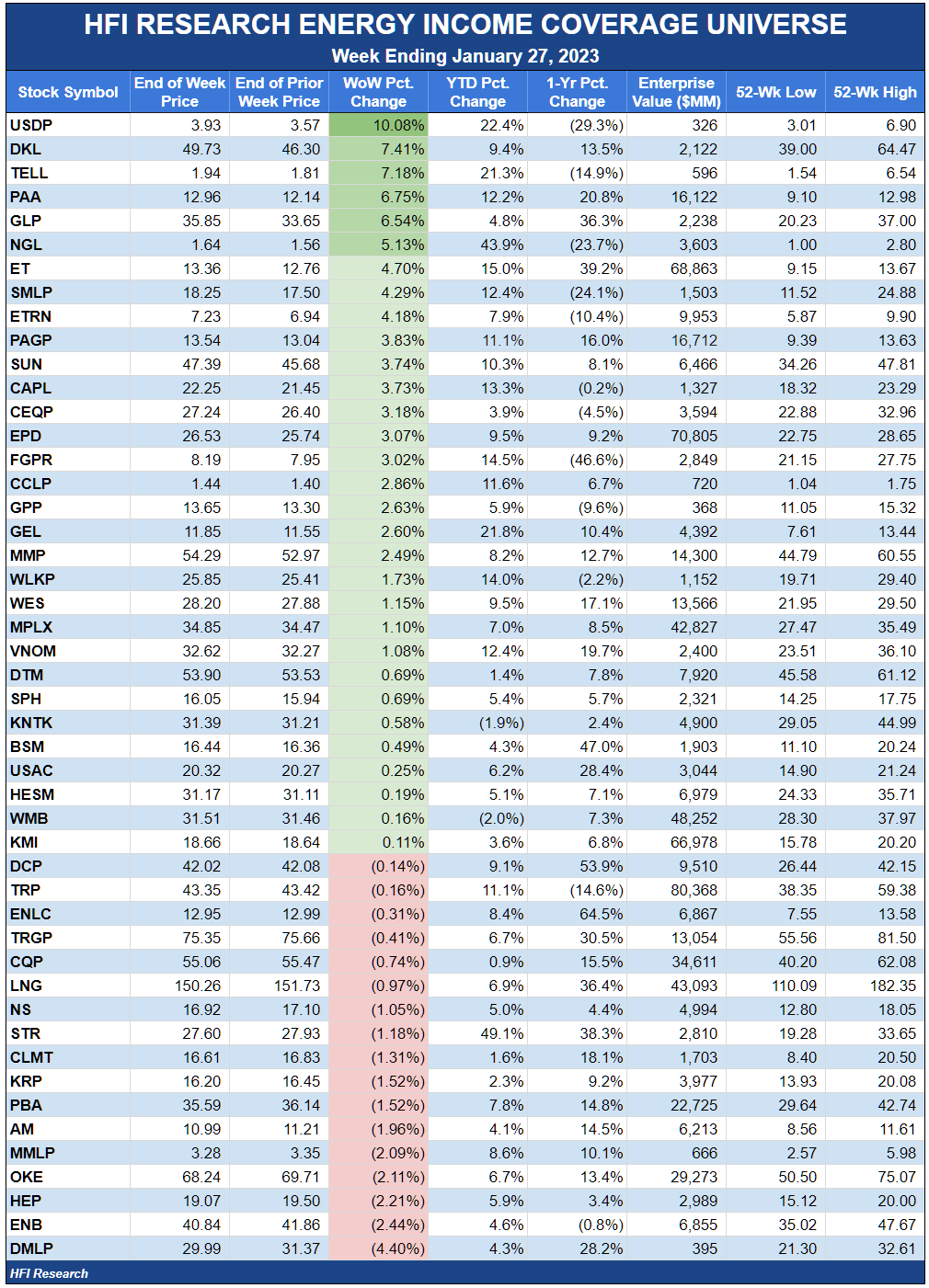

Our energy income coverage universe saw gains with impressive breadth due in part to the abundance of MLPs. Despite the MLP outperformance, we continue to view these equities as some of the cheapest relative to intrinsic value and dividend yield in today’s stock market.

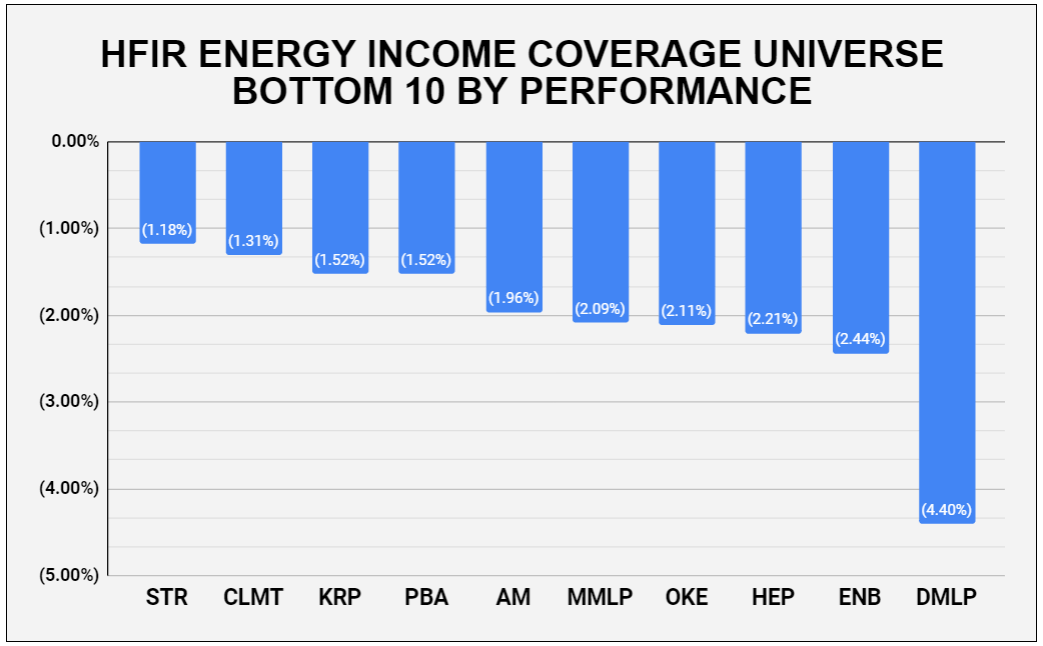

Consistent with the week’s “risk on” tenor, the best performers in our coverage universe were those with uncertain outlooks and/or weak financial positions. More speculative names tend to catch a bid when investors turn optimistic about the outlook for the economy and financial markets, but that doesn’t change the fact that they offer an unusually high likelihood of saddling their long-term holders with permanent capital losses.

USD Partners ( USDP ) was the best performer. Its units can be put in the “uncertain outlook” bucket. They have crept up over recent weeks on no public news. However, management issued an update this week that reiterated its prior assertions that it sees crude-by-rail economics changing for the better and implying that it's continuing to wait for the right time to sign new contracts. As holders of the name, we believe management can execute, and we base our judgment on the company's superior new service offering, management’s generally good character, and its exceptionally good track record when it comes to rolling out new crude-by-rail innovations.

{kind=link}

Delek Logistics Partners ( DKL ) was the second biggest gainer after it increased its quarterly distribution from $0.99 per unit to $1.02 per unit. With the new distribution, DKL units yield a juicy 8.2%. DKL routinely generates a cash flow surplus that should make it easy for it to afford the distribution increase. At $49.73, the units trade just below our $50.00 price target. We rate DKL as a Hold, though we’re considering reviewing the name for an upgrade if we deem its new distribution safe and sustainable.

Tellurian ( TELL ) caught a bid during the week on no news. The company is arguably the most speculative in our coverage universe, as it continues to build a multi-billion dollar project without having secured proper financing. The stock is essentially a bet on the charisma of its leader, Cherif Souki, and his ability to attract funding. But it's also a bet that Souki does not consume enough of TELL’s upside through his compensation practices to leave multi-bagger upside for public shareholders. Until we see evidence that the company can secure proper financing and that Souki can restrain his compensation, we recommend avoiding TELL shares, which we rate as a Sell.

Plains All American ( PAA ) was up 6.8% during the week. PAA does not have an uncertain outlook, nor does it have a weak financial position. We view the units' gain during the week as a catch-up trade in which their multiple advances to a level more closely in line with peers. It was notable that PAA outperformed its C-corp. twin, Plains GP Holdings ( PAGP ), which was up 3.8%. We’ve long believed that PAA was a superior investment alternative to PAGP due to its persistent discount to its own value and to PAGP, and its corresponding higher yield relative to PAGP. The most recent trade in our portfolio was to increase our weighting in PAA due to its relative underperformance versus peers and its positive long-term prospects for increasing distributions and repurchases. Even after this week’s rally, we continue to favor PAA over PAGP. We rate both as a Buy, with a $13.50 price target.

Global Partners ( GLP ) rose 6.5% after it announced a one-time special distribution of $0.9375 in addition to its regular quarterly distribution of $0.6350. The company has been performing well financially, sending its units to 52-week highs. However, we prefer to avoid units of MLPs with skewed incentive schemes that favor management at the expense of public unitholders. We’d note that management’s IDRs entitle it to a large portion of the quarterly distribution, as shown in the table below, sourced from the company’s 2021 10-K.

{kind=link}

The company could have used the cash flow distributed as a special distribution to pay down debt in anticipation of margins reverting to historically normal, lower levels, which would reduce Adjusted EBITDA and dramatically increase GLP’s leverage ratio, but the incentives in place for management clearly favor a large distribution.

The other notable gainers included Energy Transfer ( ET ), which announced a quarterly distribution hike to the pre-pandemic level of $0.305. We commend management for its execution on the financial goals it laid out in 2020. Granted, ET received a boost from its $2.4 billion windfall from Winter Storm Uri, but management also made smart moves to reduce leverage as per the credit rating agencies’ models. ET units at $13.36 yield an attractive 9.1%. If the company can continue to deleverage and refrain from irresponsible capital allocation, we see them increasing toward our price target of $15.25, 14.1% above their current price. At our target price, ET units would trade at an 8.0% distribution yield, in line with large midstream peers and slightly below the midstream sector average.

NGL Energy Partners ( NGL ) and Summit Midstream Partners ( SMLP ) rose 5.1% and 4.3%, respectively. Despite the week’s gains, both remain financially weak and at risk of bankruptcy in a cyclical downturn. We rate both as a Sell.

The week’s underperformers were a hodge-podge of names, some of which are directly or indirectly exposed to weak natural gas prices. ONEOK ( OKE ), Antero Midstream ( AM ), and Kimbell Royalty Partners ( KRP ) are in this group and were down 2.1%, 2.1%, and 1.5%, respectively. Canadian names were also down after experiencing a series of outages and operational problems that curtailed throughput on their systems.

{kind=link}

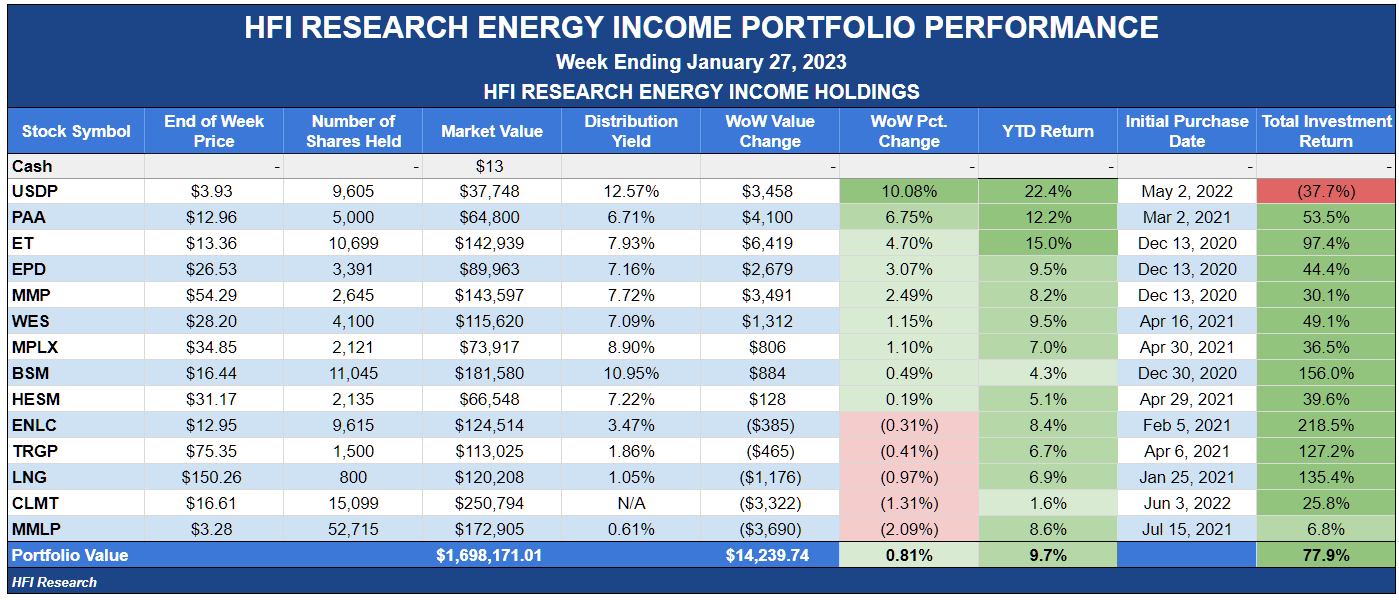

Weekly HFI Research Energy Income Portfolio Recap

Our portfolio underperformed its benchmark, the Alerian MLP Index, by 1.5% during the week due to the underperformance of our larger holdings, Martin Midstream Partners ( MMLP ), Calumet Specialty Products Partners ( CLMT ), and Cheniere Energy ( LNG ).

{kind=link}

MMLP was down 2.1% after management pre-released disappointing fourth-quarter results. All operating segments performed in line with our expectations during the quarter with the exception of the butane blending business. The business involves loading up on inventory during the low-demand summer months, blending the butane so that it meets winter fuel specifications, and selling it during the high-demand winter months, presumably at a higher price. In 2022, butane prices were higher in the summer than in the winter, so the company’s summer purchases ended up generating losses during the winter sales season. In response to the disappointing result, management has decided to exit the butane blending business, which we view as a positive in light of its large working capital requirements and their impact on the company’s financial position and credit profile. We refer readers to our chatroom for a more detailed rundown of MMLP’s butane blending situation.

CLMT fell 1.3% on no news. The persistently weak pricing of CLMT units relative to the company's obviously higher intrinsic value if its Montana Renewables renewable fuel manufacturing facility is successful points to the market’s belief that it is likely a flop. However, the facility is already up and running, and the company has been transparent in its disclosures that Montana Renewables remains on track to fulfill management's cash flow and EBITDA expectations. We disagree with the market’s verdict at the current price and look forward to positive news on the facility’s success over the coming months.

Cheniere Energy ( LNG ) traded down by 1.0% in response to weak natural gas and LNG prices. We continue to believe the company’s intrinsic value lies above its current trading price due to its long-term contracts that lock in a margin. Moreover, we believe the LNG market could heat up again in the fall as Europe attempts to build enough natural gas inventories to make it through winter in the face of reduced Russian inflows.

Among our portfolio's better performers, Hess Midstream ( HESM ) was up 0.2% after reporting fourth-quarter results in line with our expectations. HESM also released an update on management’s guidance and capital return framework through 2025. We’ll have an update on developments in the next few days. HESM is poised to benefit from Hess Corp.’s ( HES ) cash flow needs related to its Guyana investment.

News of the Week

Jan. 24. Equitrans Midstream ( ETRN ) received some rare good news on the regulatory front, as the company received a final environmental impact statement for its 350 mmcf/d Ohio Valley Connector expansion project from the FERC. With the fate of ETRN’s Mountain Valley Pipeline ((MVP)) now dependent on legislation for its completion, the company needs all the good news it can get on its other growth initiatives. ETRN shares languish in the low-$7.00 range, likely due to the risk of a distribution cut if the Mountain Valley Pipeline is canceled. However, the shares offer explosive upside if the MVP gains approval for its completion.

Jan. 25. Kinder Morgan ( KMI ) held its investor day, in which management spoke of its intention to use the Inflation Reduction Act as a springboard for further investments in renewable natural gas and carbon sequestration. KMI’s Investor Day presentation can be found here . KMI generates sub-par returns on capital employed and is among the worst capital allocators among its large-cap midstream peers. We’d rather see management stick to its knitting and improve its assets’ returns than venture into new territory. We rate KMI as a Hold with a $19.00 price target.

Capital Markets Activity

None.

{kind=link}

For further details see:

Energy Income Weekly: The Risk-On Trade Prompts A Dash To Low-Quality Equities