BSM - Energy Income Weekly: Volatile Prices Mask Improving Fundamentals

2023-05-03 20:02:54 ET

Summary

- Energy lagged amid volatile commodity pricing and dour investor sentiment.

- Macro fundamentals are holding up and the outlook remains strong.

- Earnings results are coming in strong, a trend that we expect to continue.

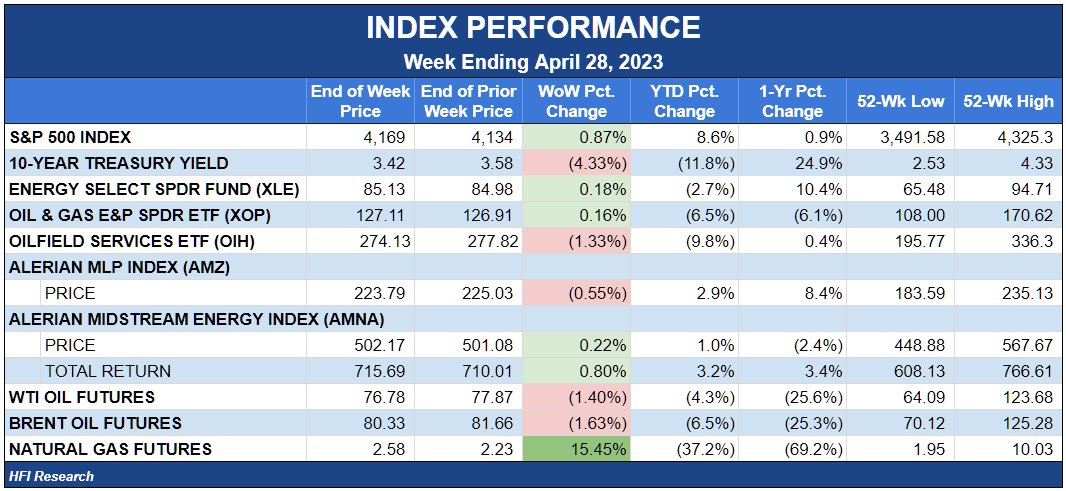

Energy Income Performance

During the week, the energy sector gained 0.2%, underperforming the S&P 500 amid weak oil prices and dour investor sentiment toward commodity stocks. Income-producing equities were the worst performers in the group, with midstream down 1.3% despite a sharp decline in interest rates.

{kind=link}

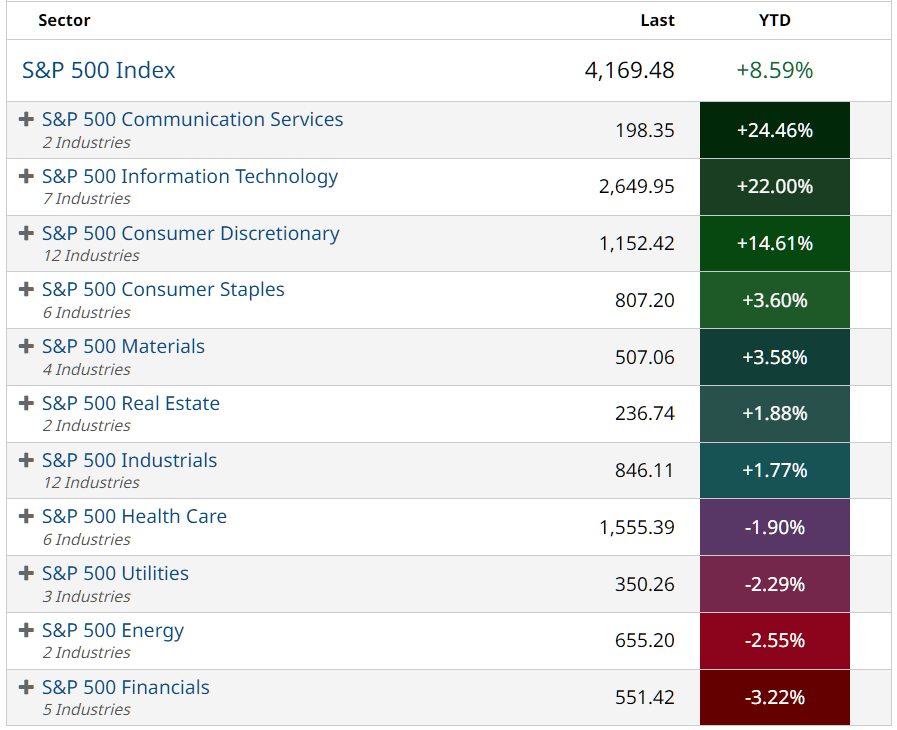

The pricing trends that prevailed all year among the various S&P sectors remained in effect. Lower interest rates and good first-quarter earnings results delivered a boost to technology stocks, while positive economic data sent consumer-related stocks higher. Financials lagged amid renewed concerns about banks after First Republic ( FRC ) headed toward FDIC receivership. And energy was weak as oil prices meandered up and down with little influence from fundamentals. By the end of the week, energy lagged tech by 25% on a year-to-date basis, as shown in the chart below.

{kind=link}

Source: Barchart.org , April 29, 2023.

We expect these trends to reverse once the OPEC+ production cut kicks in and oil inventories begin a sustained decline that will persist through year-end. These inventory declines should push oil prices higher regardless of the speculative interest—or lack thereof—in oil futures because if there’s a supply shortage, refiners will be forced to bid against one another to secure scarce supply.

We were recently asked to be more specific about how we expect near-term oil price action to unfold, and we answered as follows:

“The rate of oil-price increase depends on the rate of inventory draws. It won't take much to push prices above $80, just an improvement in sentiment once the market appreciates that draws are likely to be sustained in the second half of the year. The OPEC+ cuts that are scheduled to begin in May should induce inventory draws and help sentiment improve.

As for $100 oil prices, we'll have to drain the 150 million or so of inventories that have built up in commercial inventories since the last time oil was above $100. To be conservative, if we assume May and June inventories draw by 500,000 bpd, those draws would remove 31 million barrels over those two months. Then assuming Q3 draws average 1.3 million bpd, July-September draws would remove another 119 million of inventories. In total, May-September draws would remove 150 million barrels from inventories. If these draws came to pass, the market would enter the fourth quarter at around $100 per barrel. Then in the fourth quarter, we expect additional draws that average 1.5 million bpd. Significant fourth-quarter draws could push oil prices well above $100.

That's the logic of how I would think about second-half oil prices. The known risks to this price forecast would be a financial crisis that destroys demand or OPEC+ failing to follow through with its production cuts. The impact of the former on reducing demand is unknown, while the latter could reduce second-half draws by as much as 800,000 bpd, depending on how much production actually ends up being cut. On the other hand, if the rate of draws exceeds our forecast, the physical market will tighten more rapidly, the oil price increase will be brought forward, and prices will likely exceed the forecast sketched above.”

Oil macro fundamentals will be supportive for energy company fundamentals, but their impact on energy stock prices is harder to gauge. The wildcard for energy stock performance will be the extent to which resurgent oil prices put upward pressure on inflation and then the extent to which inflation keeps the Fed on its tightening path. Higher interest rates and their adverse impact on the economy and financial asset prices at large—as well as investors’ fear of adverse outcomes even if they don’t come to pass—could keep energy stock prices restrained compared to how they would behave in a healthier economy.

Then there’s the prospect of Fed overtightening combined with higher oil prices delivering a double whammy to the economy, which would reduce oil demand and prices. These are our main concerns for energy stocks if oil prices increase, and we’ll monitor them closely.

Despite these potentially bearish factors looming in the second-half outlook, we’re confident that rising oil prices will cause energy stocks to rise. It’s the extent of the increase that’s open to question.

A Flattish Week for Energy Stocks

Falling oil prices and negative investor sentiment toward energy stocks were countered during the week by strong first-quarter earnings reports by Exxon Mobil Corporation ( XOM ) and Chevron Corporation ( CVX ), both of which beat analyst expectations due largely to outperformance in their refinery segments. Over the next few quarters, the majors are likely to lose this advantage as newly built refineries add throughput capacity and cause refining margins to fall. However, higher oil prices should benefit their E&P divisions, which would support their cash flows and stock prices. Both XOM and CVX shares are likely to perform well in the second half, though not as well as smaller companies with operations that are more concentrated in upstream activities.

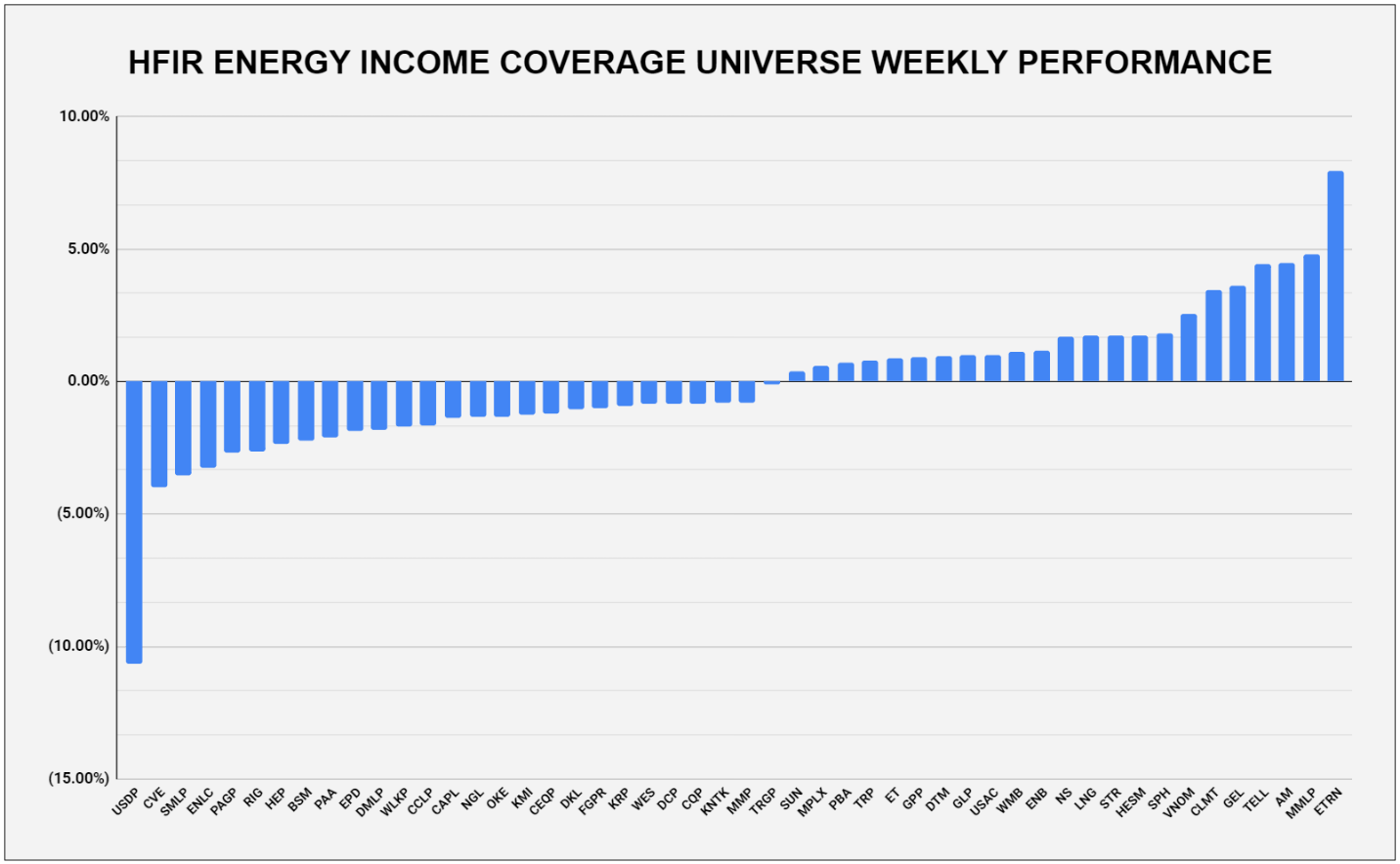

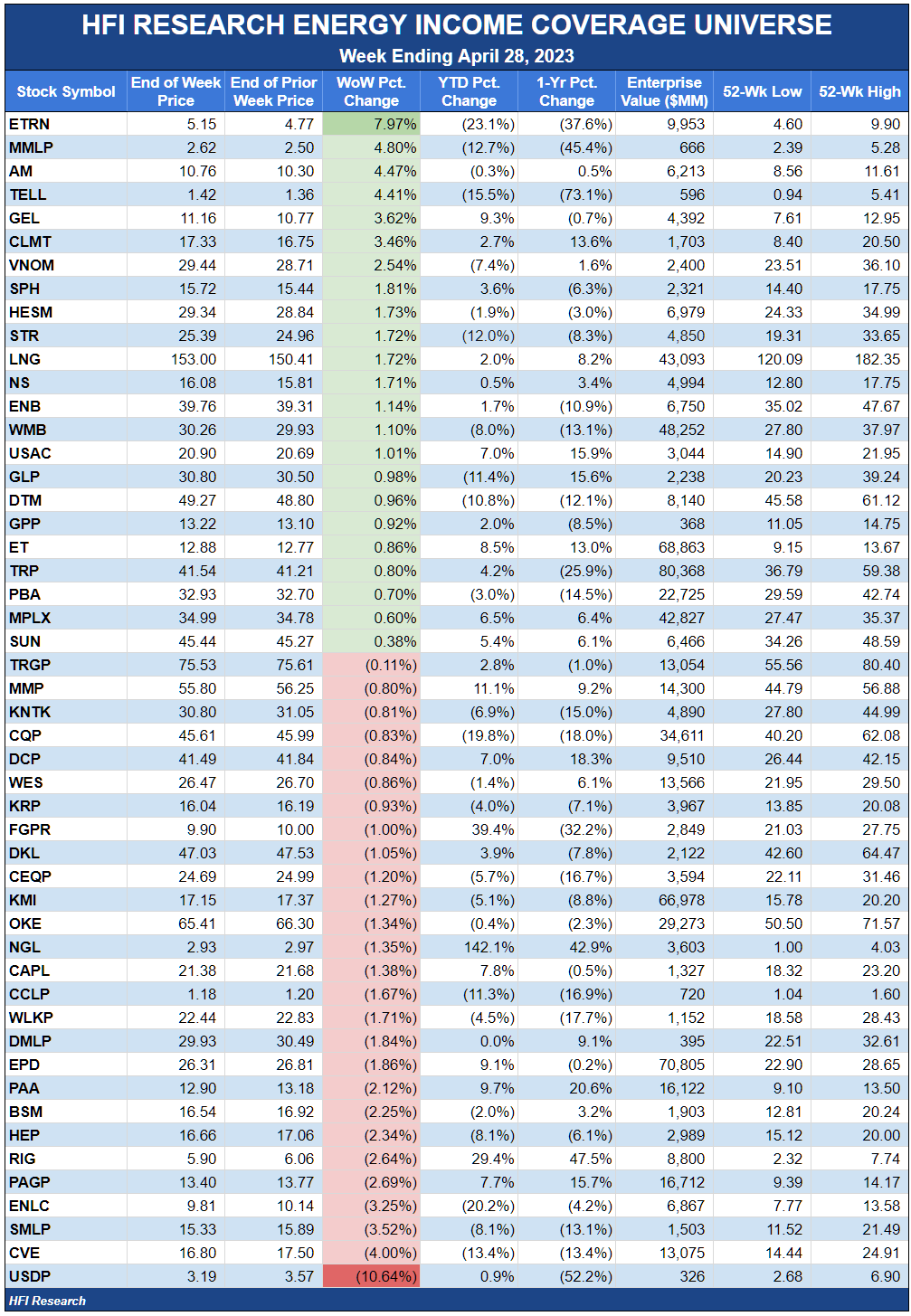

Among energy income equities, it was a rare week in which most names in our coverage universe were evenly balanced between gainers and decliners, and most fluctuated in a narrow band of +/- 2%.

{kind=link}

Equitrans Midstream ( ETRN ) was the best performer in our coverage universe, up 8.0% during the week after Energy Secretary Jennifer Granholm sent a letter to regulators in support of completing the Mountain Valley Pipeline ((MVP)). While the letter stopped short of advocating for federal legislation to fast-track the project’s completion, it stated that the pipeline’s completion would “enhance regional and national energy security” and that the FERC should “fulfill its regulatory responsibilities regarding natural gas infrastructure.”

Unfortunately for ETRN, not all of the week’s developments were positive for the MVP. On Monday, the U.S. Supreme Court revived a lawsuit by property owners who are contesting the pipeline’s use of eminent domain in its construction. The landowners argue that eminent domain should be a legislative power and that it was improperly delegated to the FERC by Congress. A loss by ETRN and MVP in the case would have far-reaching ramifications for infrastructure projects, as well as for the administrative state’s regulatory activities in general.

The lawsuit’s revival introduces another element of doubt into MVP’s completion prospects. It raises the question of whether legislation to fast-track the project would be rendered moot if the project’s prior eminent domain proceedings were invalidated. We still like the prospects for ETRN stock if the MVP is completed, but we’ll stay on the sidelines until we get more clarity.

Antero Midstream ( AM ) was another big gainer during the week, rising 4.5% after beating analyst EBITDA expectations. We discussed AM’s outstanding prospects as an income investment here . After several quarters of superb management execution, AM has become one of our favorite income-producing stocks in the energy sector.

Tellurian ( TELL ) received a 4.4% boost after announcing that its Driftwood Pipeline’s Line 200 and Line 300 natural gas transmission projects received a certificate authorizing their construction from the FERC. The news does little to improve the overall prospects for Driftwood or TELL. Charif Souki, TELL’s Executive Chairman, was recently forced to sell 25 million of his TELL shares to cover a margin call. He had used the shares as collateral for a 2017 loan for real estate investments. His remaining stake totals 1.66 million shares. TELL shareholders should be concerned about the measures the company may take to “reincentivize” Souki to stay put with the company. We recommend that investors avoid TELL stock.

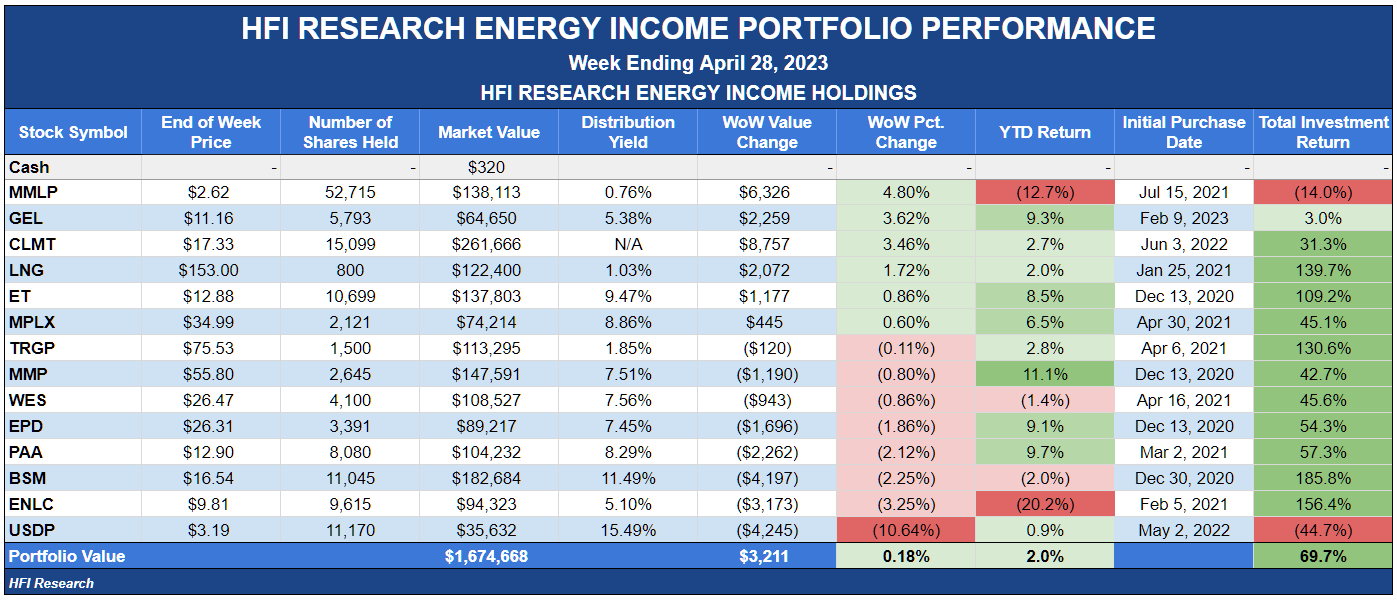

Weekly HFI Research Energy Income Portfolio Recap

The week’s big decliners were concentrated among our holdings. Nevertheless, our portfolio’s gainers’ performance more than offset the impact of its decliners to eke out a 0.2% gain, representing 0.8% outperformance versus its benchmark, the Alerian MLP Index.

{kind=link}

USD Partners ( USDP ) underwent a 10.6% decline after spiking more than 30% on no news. We suspect the spike was the result of Western Canadian oil inventories approaching multi-year highs, which incentivizes transportation of crude by rail. We look forward to an update from management on its efforts to sign contracts for its DRUbit by rail business. At this juncture, with the company’s debt becoming a growing concern in the absence of new business, we could begin to lose confidence in management if we don’t see evidence of progress in the company’s upcoming first-quarter earnings conference call.

EnLink Midstream ( ENLC ) shares fell 3.3% despite a 15.5% weekly gain in natural gas prices. The drop was likely attributable to the concerns that Midcontinent drilling activity could turn lower if natural gas prices stay at current levels. Another bearish element for ENLC was a Morgan Stanley downgrade, though the bank’s price target was lowered from $18 to $17, which is still 73% higher than Friday’s closing price of $9.81. ENLC stock is attractive as a long-term holding at current prices, given its exposure to Permian growth and its natural gas and carbon infrastructure opportunities in Louisiana.

Black Stone Minerals ( BSM ) fell 2.3% on no news. BSM had been unusually strong in previous weeks relative to royalty company peers, so we’re not surprised that it cooled off this week. Like ENLC, BSM faces the prospect of negative effects from reduced natural gas drilling. However, BSM is somewhat insulated, as its major Haynesville operator, Aethon Energy, is well-hedged and plans to maintain its pace of drilling.

On the positive, side, Energy Transfer LP ( ET ) gained 0.9% after announcing that it would increase its quarterly distribution from $0.305 to $0.3075 per unit. The company also pledged to increase its distribution by 3% to 5% annually going forward. We consider any distribution increase from ET to be positive, as it deprives management of cash needed to make poor capital allocation moves. That said, we applaud management for its successful efforts at deleveraging and boosting the distribution. We don’t expect additional quarterly distribution hikes this year, but we rate ET a buy and reaffirm our $15.25 price target.

Calumet Specialty Products Partners ( CLMT ) was up 3.6% after it announced that its Montana Renewables facility entered full operation as the largest sustainable aviation fuel producer in North America. Why these units trade at such a low price is a mystery to us. We keep searching for what we may be missing, but so far, we’ve come up empty. We view CLMT as one of the biggest no-brainer Buys in today’s stock market.

Martin Midstream Partners ( MMLP ) was our portfolio’s biggest gainer, up 4.8% during the week on no news. MMLP’s units are too cheap relative to the huge gains to be had over the coming years from deleveraging. Like CLMT, MMLP is an unusually attractive Buy at its current price.

News of the Week

April 24. The U.S. Department of Energy introduced a new policy that it will no longer consider applications for extending deadlines for commencing LNG export projects. The DOE believes the seven years it grants for projects to start is reasonable. Only if projects have physically begun construction will they be eligible for an extension. The first casualty of the policy was Energy Transfer’s ( ET ) Lake Charles LNG project, which had requested a second deadline extension for its planned Louisiana terminal.

The DOE determined that ET’s Lake Charles LNG project did not show good cause for a second extension, which would have pushed its current deadline from December 2025 to December 2028. We’ll be watching for management’s response on the company’s first-quarter earnings conference call on Tuesday, May 2, after the market’s close.

April 28. TC Energy ( TRP ) reported a strong first quarter, slightly beating analyst Adjusted EBITDA expectations due to a strong performance in its U.S. natural gas pipeline segment. Fortunately for shareholders, management did not report additional cost increases in TRP’s Coastal GasLink project, which is now 87% complete. The company is also on track to complete management’s anticipated $5 billion of asset disposals this year.

Despite TRP’s good financial results, the company remains beset by operational issues. First, the company reported that its recent 14,000-barrel oil spill from its Keystone pipeline in Kansas last December was primarily due to a fatigue crack during its construction. Then, just hours after it released first-quarter results and hosted its analyst conference call, it declared force majeure on its Columbia Gulf Transmission natural gas compression station due to a fire, which had been extinguished. Investors looking to buy TRP shares should hold off until management proves its operational challenges are a thing of the past.

Capital Markets Activity

None.

{kind=link}

For further details see:

Energy Income Weekly: Volatile Prices Mask Improving Fundamentals