ERII - Energy Recovery Deserves More Downside Unless Earnings Paint A Better Picture

2023-10-27 10:56:41 ET

Summary

- Energy Recovery's business model is interesting, but shares are expensive relative to cash flows, leading to a 'sell' rating.

- The company's sales, profits, and cash flows have declined, with revenue particularly affected in the Middle East and Africa.

- Despite having no debt and a strong cash position, the company's growth rate is not enough to justify its high valuation, though we will see how earnings turn out.

I have always found myself attracted to companies that have interesting business models. There is something about the novelty of something I have not seen or have rarely seen that interests me. You can imagine how much, then, I became fascinated by Energy Recovery ( ERII ) when I first found out about the business and its operations. In a prior article , published in June of last year, I dug into its business model in more detail. But in short, its primary offering is a pressure exchanger that is composed largely of ceramic and that helps to save costs for desalinization plants. It does this by transferring energy within a desalinization and industrial wastewater process flow system from a high pressure reject concentrate into seawater that then flows back into the system where it meets the stream of seawater coming from high pressure pumps. This combined stream then makes its way into membranes where it can be processed into potable water.

Unfortunately, it doesn't matter how much I like a business if that business does not make sense to buy into. While I sometimes feel as though I give perhaps too much slack to companies that I do like, this one I could not walk away with a bullish feeling about. Shares looked very expensive relative to the cash flows the company was generating. And as a result, I ended up rating the company a ‘sell’ to reflect my view that it should underperform the broader market for the foreseeable future. And underperform shares did. Since the publication of that article, the S&P 500 is up an impressive 13.9%. By comparison, Energy Recovery has seen downside of 18.3%. You might think, given this drop, that I would now turn bullish on the company or at least neutral. But because shares are still very expensive, I do still think that a ‘sell’ rating is appropriate at this time.

Cash flows look bad

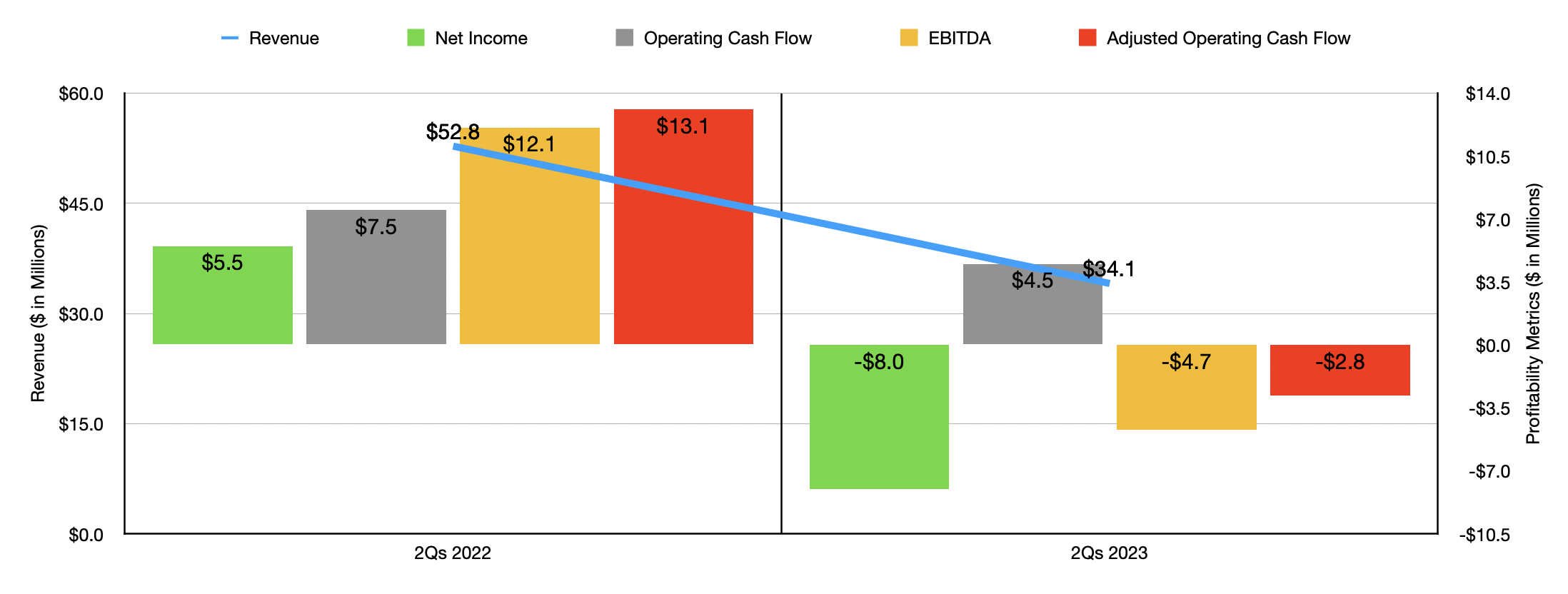

Fundamentally speaking, Energy Recovery is not doing all that well. Because of a bad first quarter, sales for the first half of the year have totaled only $34.1 million. That compares to the $52.8 million in revenue generated one year earlier. While the company did see strength in some markets, particularly throughout Asia, the Middle East and Africa proved to be a problem. Revenue plunged from $37 million in the first half of 2022 to only $13.8 million the same time this year. The good news though is that this is not revenue that appears to be permanently lost. Management said that project timing throughout the Middle East and Africa resulted in much of this pain.

{kind=link}

Author - SEC EDGAR Data

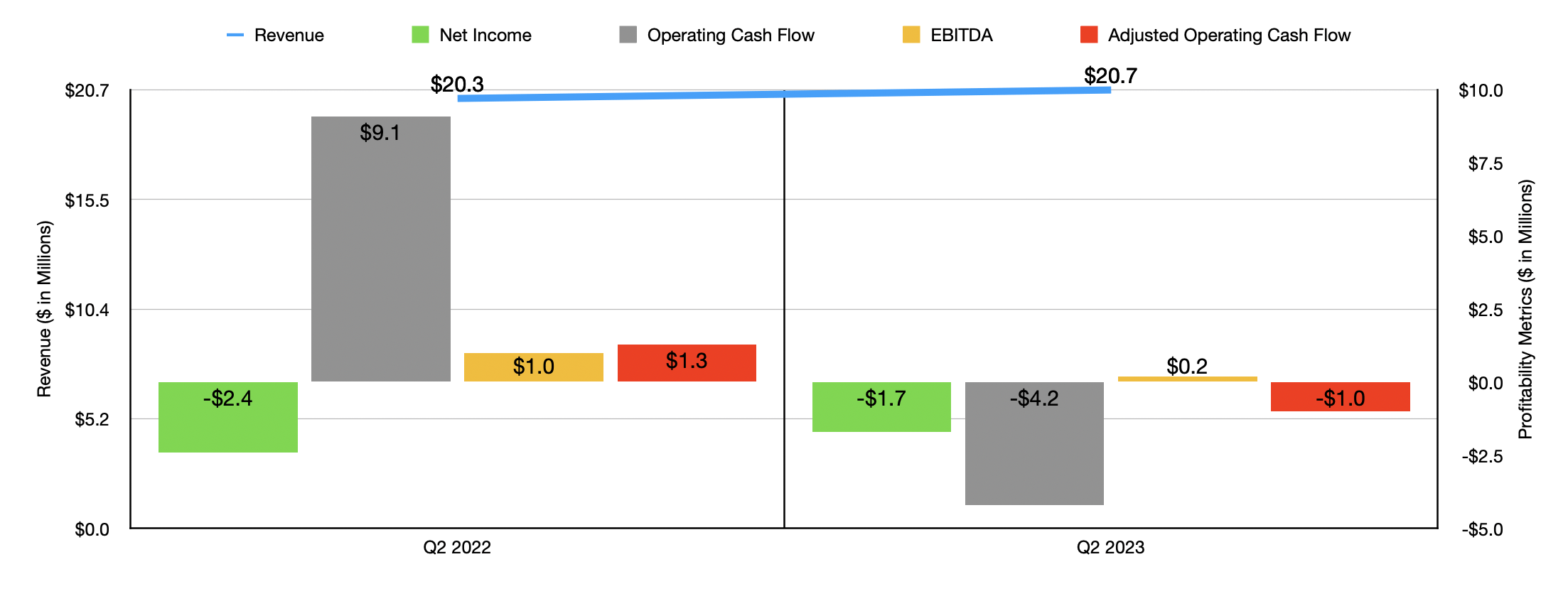

This drop in revenue brought with it a decline in profits and cash flows as well. Net income went from $5.5 million in the first half of 2022 to negative $8 million the same time this year. Operating cash flow was slashed from $7.5 million to $4.5 million. If we adjust for changes in working capital, the picture was even worse, with the metric going from $13.1 million to negative $2.8 million. And finally, EBITDA for the firm went from $12.1 million to negative $4.7 million. As you can see in the chart below, financial results for the second quarter on its own were similarly bad from a cash flow perspective. But revenue did improve compared to the first quarter, even coming in marginally higher than what the company generated one year earlier. I do know that pricing increases were part of its sales resilience during this time.

{kind=link}

Author - SEC EDGAR Data

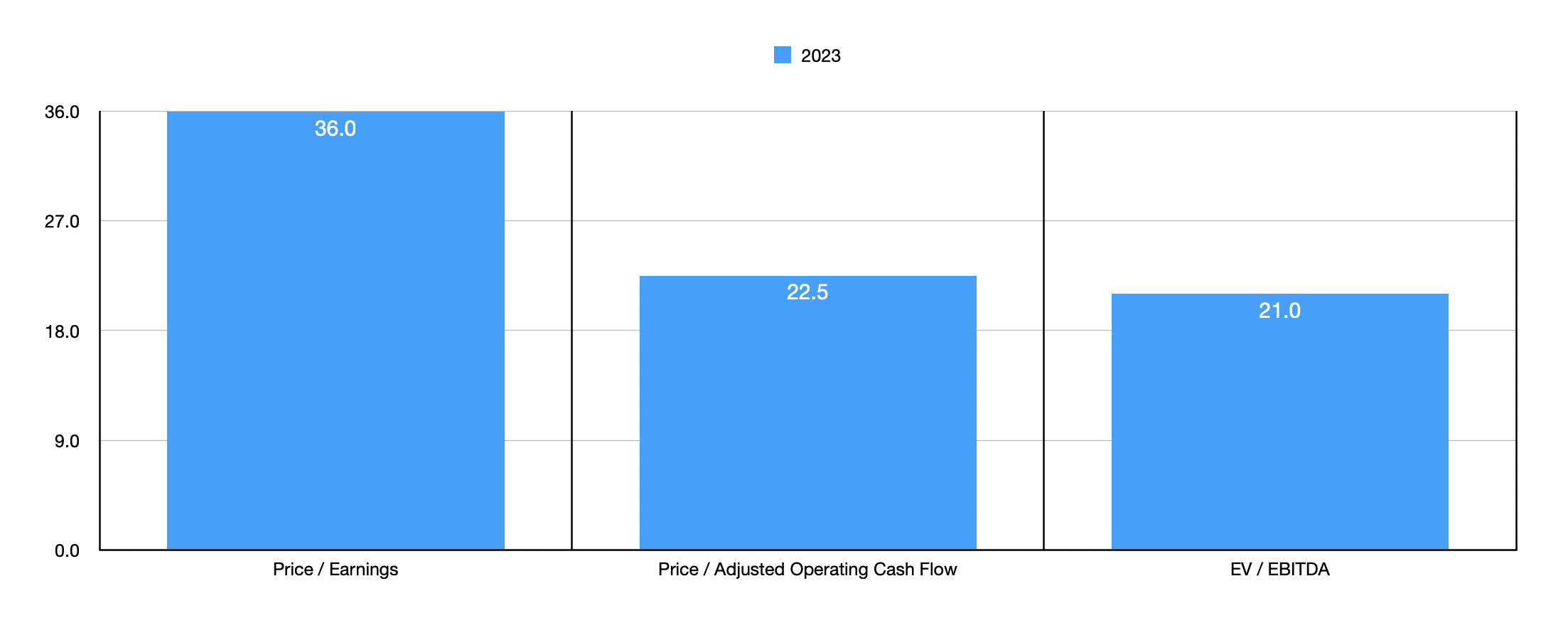

It would be nice to be able to value the company based on more recent financial results. But management has not provided bottom line guidance for 2023. If we use data from last year, shares do still look very expensive. For instance, it is trading at a price to earnings multiple of 36. The price to operating cash flow multiple should be 22.5, while the EV to EBITDA multiple should be slightly lower than that, at 21. Even more astronomical is the 36 reading that we get for the price to earnings multiple.

{kind=link}

Author - SEC EDGAR Data

This is not to say that the company doesn't have anything good going for it. It actually has no debt, and it enjoys $95.1 million of cash and cash equivalents on its books. This makes it fundamentally sound for now. That does deserve something of a premium, but the price the market is asking does not make sense to me. It would be different if the company happened to be growing rapidly. But that's not the situation we are dealing with. Although management has said that revenue should be between $330 million and $570 million by 2026, this year revenue is expected to only be between $131 million and $138 million. Even if it hits the high end, that would be only 9.9% above the $125.6 million the company generated in 2022. That's not a fast enough growth rate to deal with a company this pricey, especially when you consider that financial results are worsening this year, implying that shares should be even more expensive on a forward basis.

{kind=link}

Author - SEC EDGAR Data

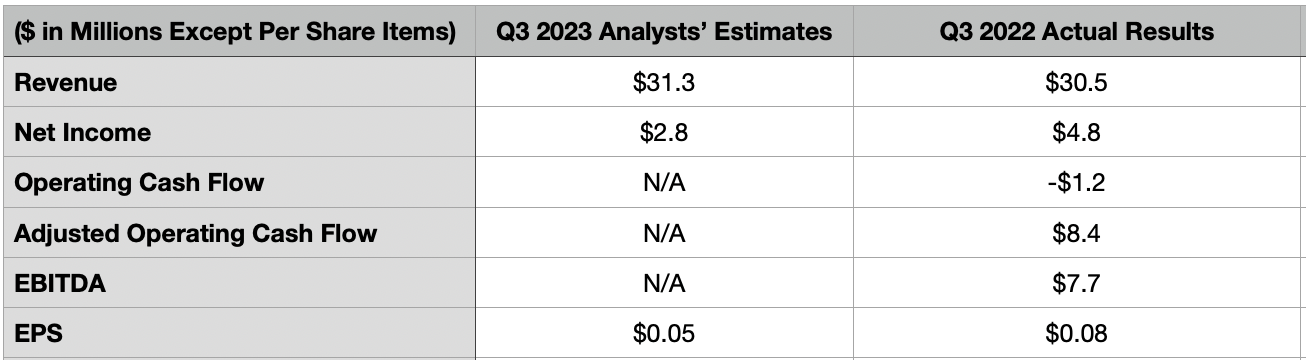

Of course, this picture can change based on new data that comes out. And it just so happens that, on November 1, after the market closes, the management team at Energy Recovery will be announcing financial results covering the third quarter of the company's 2023 fiscal year. Leading up to that time, analysts expect sales to weaken, hitting $31.3 million. That's down from the $36 million reported one year earlier. Analysts believe that earnings per share will be only $0.05, which would be down from the $0.08 reported last year. That would bring net profits down from $4.8 million to only $2.8 million. Given the track record that we have seen, investors should expect weakness on the profitability front. For context, in the third quarter of 2022, operating cash flow was negative to the tune of $1.2 million. On an adjusted basis, it totaled $8.4 million. And finally, EBITDA for the company was only $7.7 million. All of these should be items that investors pay close attention to. And that's because they will go a long way toward determining how the market views the company over the next few months.

Takeaway

As much as I like the business model championed by Energy Recovery, I cannot usher up the courage to rate the company anything other than a ‘sell’ right now. While the stock has gotten cheaper, fundamentals are looking mixed. Yes, the company has a nice chunk of cash on hand. But that's not enough when you add in growth expectations to offset all of the negative points. In the event that shares do fall further, perhaps another 20% or so, I could change my stance to a neutral one. But I don't believe that will happen in the near term unless management comes out with some really interesting data covering the third quarter. In the meantime, all I can do is sit on the sidelines and see what transpires.

For further details see:

Energy Recovery Deserves More Downside Unless Earnings Paint A Better Picture