ERII - Energy Recovery: Is CO2-Refrigeration Thesis Already Getting Cold? (Rating Downgrade)

2023-08-08 04:57:24 ET

Summary

- Energy Recovery's CO2-refrigeration effort has the potential to replace environmentally dangerous HFCs and reduce electricity consumption in refrigeration systems.

- The company estimates that CO2-refrigeration is a $1 billion TAM and could impact 100,000 supermarkets in the U.S. and EU.

- Despite a disappointing Q2 earnings report, Energy Recovery's wastewater revenue is ramping up, but CO2 revenue recognition remains flat.

Energy Recovery ( ERII ) is the global leader in energy recovery devices ("ERDs") for the salt-water reverse osmosis ("SWRO) market. However, the company has been on a mission for many years to establish new vertical markets for its patented PX pressure exchange technology. Today, I'll take a look at how that strategy is progressing - especially with its new CO2-refrigeration effort - and what we can learn from the Q2 earnings report that came out last week. One thing we already know: the stock fell 7.7% in after-hours trading on investor disappointment when the Q2 results were released. That said, the stock is still up 20.8% over the past year and was trading at an all-time high prior to the report:

Investment Thesis

Energy Recovery's patented PX pressure exchange devices and its dominance in the global SWRO market is well known and has been reported on extensively here on Seeking Alpha by myself and others. So too was the company's ill-fated attempt to open-up a new vertical market by commercializing its Vor-Teq product for use in the O&G shale fracking industry.

More recently, ERII has been working on two new markets to deploy its PX technology: wastewater and CO2-refrigeration. ERII's CO2-refrigeration solution has two primary catalysts going for it:

- A strong regulatory tailwind to replace environmentally dangerous HFCs.

- Reducing refrigeration electricity consumption.

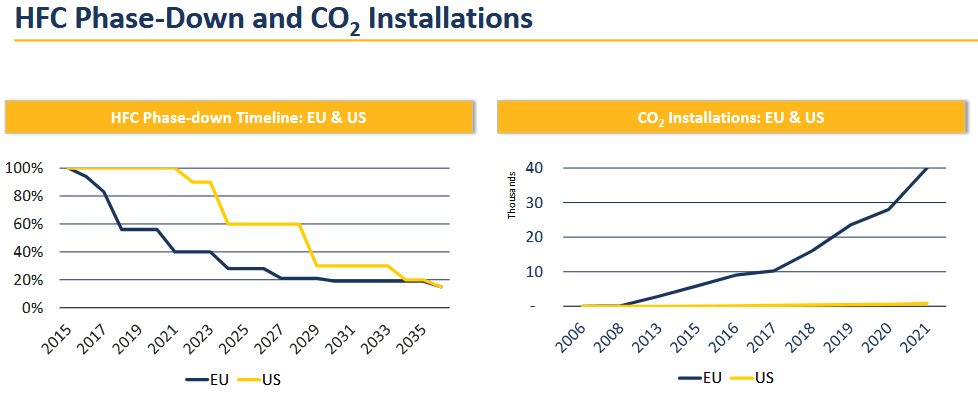

HFCs (hydro-fluorocarbons) used for refrigeration are up to 13,000x worse than CO2 and, as such, there is strong regulatory phase-out legislation (especially in the EU) that is causing a rapid increase in the number of CO2-based refrigeration installations. The slide below - taken from a June Investor Presentation - shows, the HFC phase-out timelines and the corresponding jump in CO2-based refrigeration installations:

{kind=link}

Energy Recovery estimates CO2-refrigeration is a $1 billion TAM and that roughly 100,000 supermarkets will be impacted in the U.S. and EU alone.

So, let's see how the company is doing in its efforts to make inroads into the CO2-refrigeration market.

ERII's CO2 Refrigeration Solution

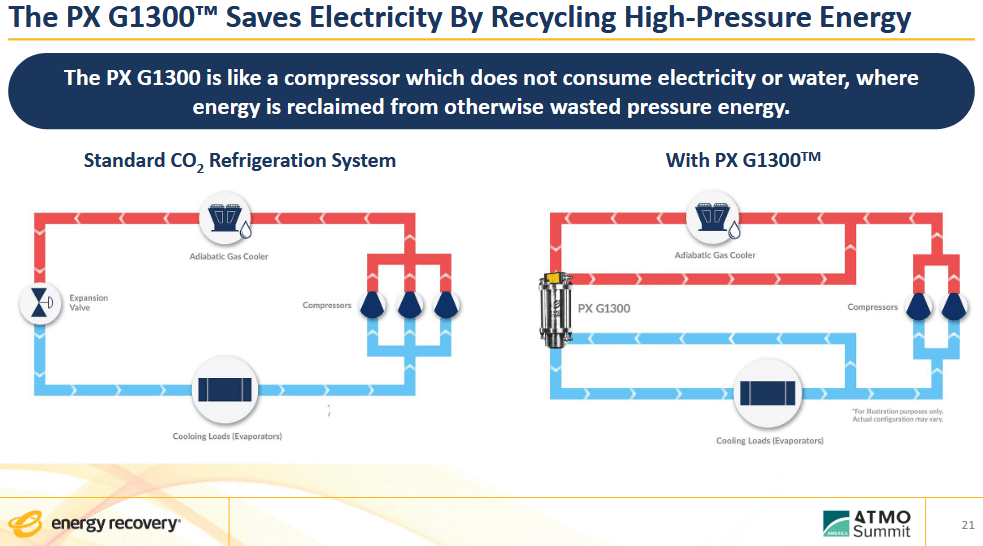

In a nutshell, ERII's solution to displace HFCs and save energy in CO2-based refrigeration systems is by using its PX-G1300 devices to recycle high-pressure energy:

{kind=link}

The system above effectively reduces the amount of energy consumed by compressors in the system - and of course the PX device itself uses no electricity at all.

And while progress has been slow in my opinion, ERII has been making progress in the CO2-refrigeration market:

{kind=link}

However, note that I wrote my first Seeking Alpha article on ERRI's attempt to establish this new CO2-refrigeration vertical over two years ago (see ERII: CO2-Refrigeration Opens Up A Whole New Market ). So, let's see how much this new market is contributing to the bottom line.

Q2 Earnings

As mentioned earlier, last week ERII released its Q2 earnings report and it was a disappointment:

- Revenue of $20.72 million (+2.1% yoy) missed by $3.79 million .

- Non-GAAP EPS of $0.00 actually beat by $0.03.

- Free-cash-flow was a negative $4.7 million.

However, on the Q2 conference call , investors learned that the top-line miss was primarily a result of timing for mega-shipment revenue recognition:

Note that we actually shipped out over $26 million in product during the quarter, but due to GAAP revenue recognition rules nearly $6 million of revenue of from a specific mega project shipment will be recognized early in the third quarter.

So taking that into account, the company actually would have exceeded its previous guidance for the quarter ($20-$25 million).

As for the new vertical markets, wastewater revenue was $600,000 or $2 million YTD. On the Q2 conference call, CEO Bob Mao said:

In wastewater, our overall signed contracts and pipelines remain robust, and we now believe we should land at the mid to high end of our $6 million to $8 million guidance by the end of the year.

So, wastewater revenue appears to be ramping up nicely.

However, CO2-refrigeration revenue recognition in Q2 was only ~$100,000, roughly flat with Q1 , and from what I could tell, there were no new order announcements. This is pretty disappointing considering the company started on its CO2-refrigeration commercialization efforts over two years ago. Could this be another Vor-Teq debacle? I don't think that will be the case.

I say that because the good news is that ERII's PX-G1300 was awarded the Refrigeration Innovation of the Year at the ATMO America Summit in Washington, DC in June. In addition, the PX-G1300 and Epta’s XTE refrigeration system (that uses the PX-G) were, separately, selected as finalists for Refrigeration Innovation of The Year Award for the annual RAC Cooling Industry Awards.

Valuation

That said, arguably much of the good news and CO2-refrigeration potential appears to already be priced into the stock:

From my perspective, the problem here is that despite all the positive talk about new market verticals over the many years I have been following ERII, the company has never really had that "special moment" or quarter where it just blows away expectations. It always seems to be the case of overly optimistic expectations and then under-delivering. However, the market clearly thinks the CO2-refrigeration and wastewater verticals will be successes in the long-run, otherwise the valuation levels shown above do not seem to be substantiated by the SWRO market alone - and make no mistake, ERII is still, today, an SWRO centric company.

Summary & Conclusion

Despite the pull-back after the Q2 EPS report was released, ERII stock is still up nearly 28% since my Seeking Alpha BUY article in February. However, do to the lack of follow-thru on CO2-refrigeration revenue/orders, and considering the high-valuation level, I am reducing my rating on ERII to a HOLD. In addition, I have ERII on my watch list and if the company does not announce some concrete CO2-refrigeration orders over the remainder of this year, and if the valuation level stays this lofty, I may downgrade the stock to an outright SELL. Meantime, the company ended Q2 with $97.5 million in cash - which equates to an estimated $1.73/share.

For further details see:

Energy Recovery: Is CO2-Refrigeration Thesis Already Getting Cold? (Rating Downgrade)