LNG - Energy Transfer: Strong Upside Warranted From Here

2023-05-04 21:44:04 ET

Summary

- Energy Transfer reported some rather mixed results for the first quarter of the company's 2023 fiscal year.

- Even so, management raised guidance for the year, thanks in part to the firm's acquisition of Lotus Midstream.

- Shares are still cheap at this time and offer investors strong upside from here.

Beyond any doubt, one of my favorite companies on the market today is midstream / pipeline operator Energy Transfer ( ET ). In my hyper-concentrated portfolio of only 10 stocks, it is the fourth largest holding, accounting for roughly 13.8% of my assets. Needless to say, I am very bullish about the enterprise and I believe that it has significant upside potential from here. You can imagine my anticipation, then, leading up to the release of the financial results covering the first quarter of the company's 2023 fiscal year. After looking through this data, which came out after the market closed on May 2nd, I can only say that my bullish stance on ET stock seems justified. Given how the company is performing and how cheap the stock is, I do believe that further significant upside exists for investors from here.

Ignore missed results

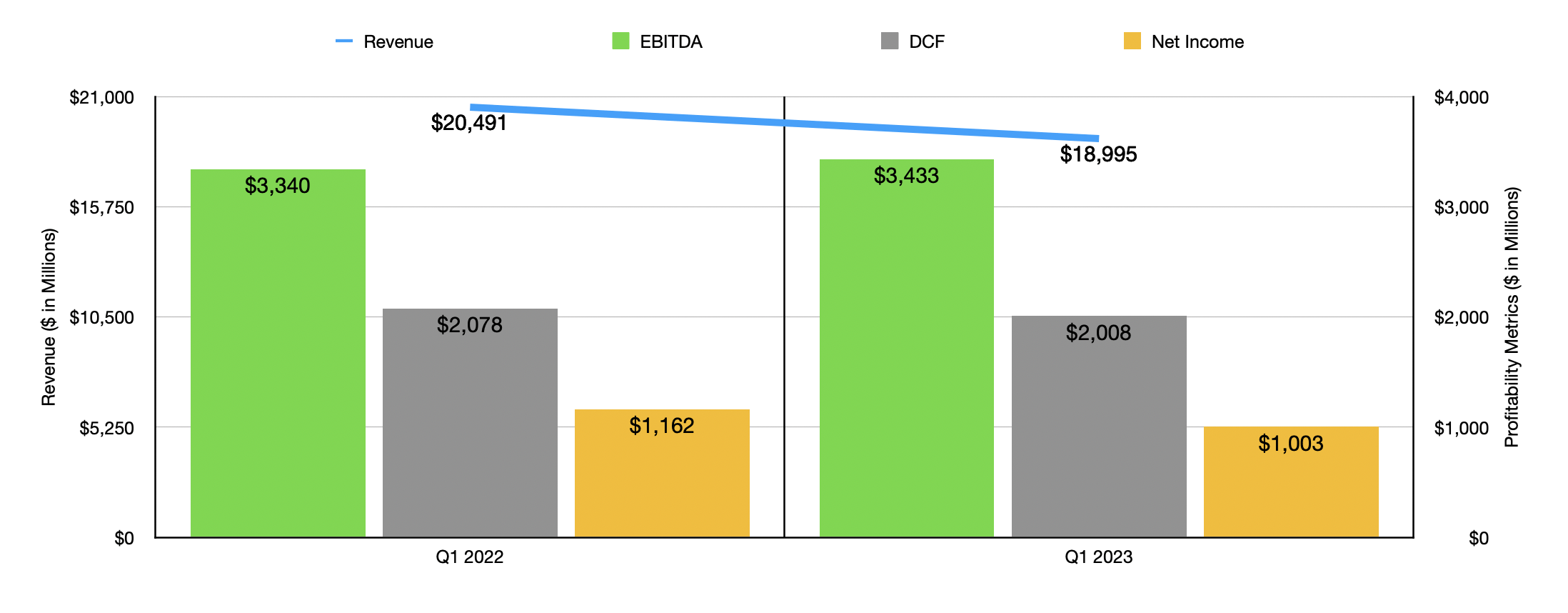

Anybody looking at the headline news regarding Energy Transfer likely would have had a somewhat negative view of how the company performed during the first quarter of its 2023 fiscal year. After all, management missed analysts forecasts when it came to both revenue and earnings per share. For instance, revenue came in at just under $19 billion . Not only was this lower than the $20.49 billion reported one year earlier, it also missed analysts’ expectations by $2.49 billion. In the world of stocks, that's a monumental miss. On the bottom line, earnings per share for the company came in at $0.32 . That's $0.03 per share lower than what analysts thought it would be.

{kind=link}

Author - SEC EDGAR Data

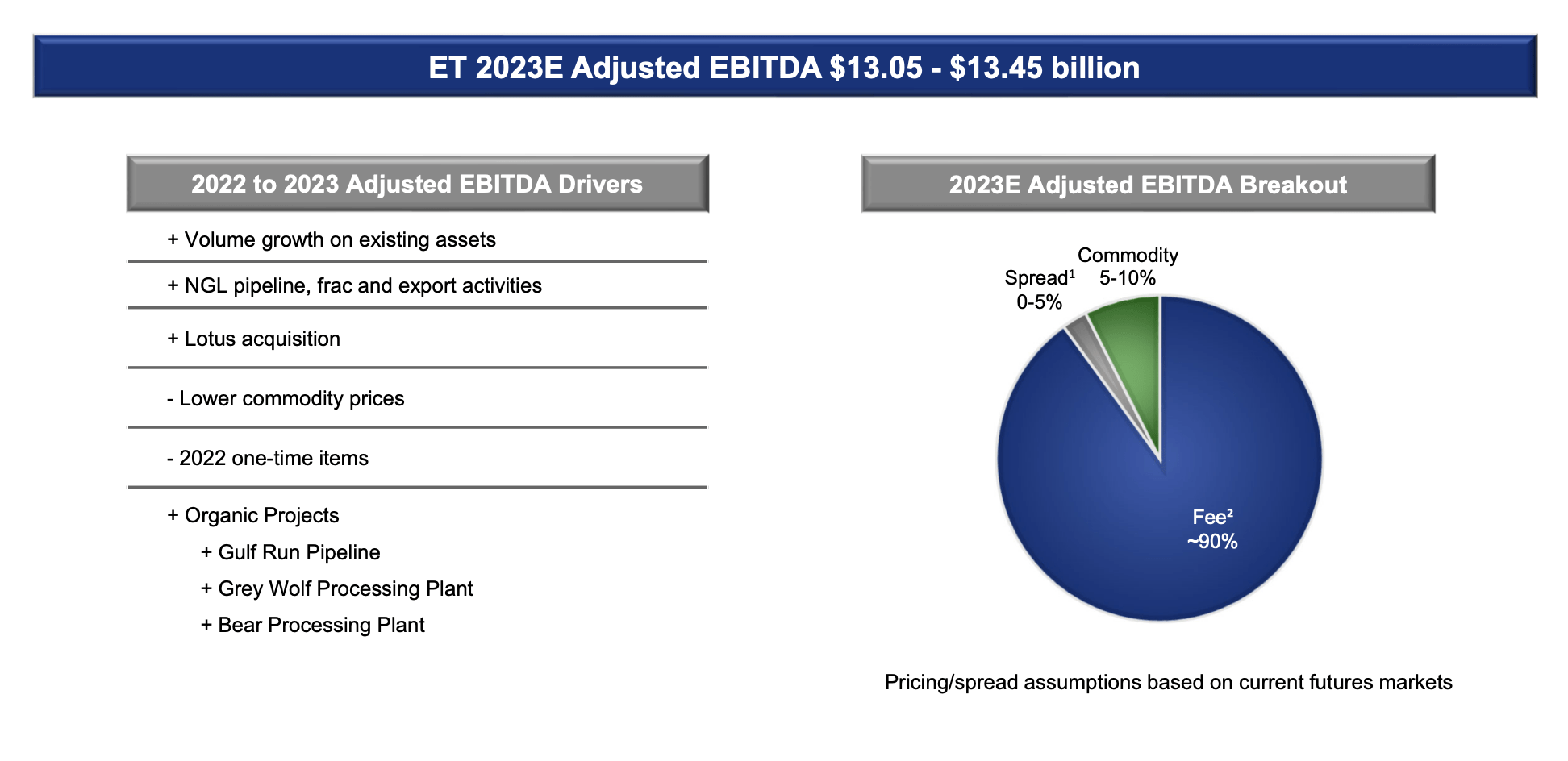

For a company in almost any other industry, I would make the case that such a significant miss on both the top and bottom lines would warrant some downside in the stock in question. But this space is odd because revenue and profits aren't all that important. Revenue for the companies in this space can vary significantly because of commodity prices. However, the firms in question make their profit on the spread between prices paid and prices sold, as well as from fees charged to customers. In the case of Energy Transfer, an estimated 90% of its EBITDA for the 2023 fiscal year we'll come from fee margins that include transport and storage fees from affiliate customers at market rates. Spread margin, meanwhile, could account for up to another 5% of profits.

The more important metrics for investors to be paying attention to relate to cash flow. One of these is operating cash flow, while the other is adjusted operating cash flow. The latter of these basically strips out changes in working capital. Personally, it is my favorite of the profitability metrics to be paying attention to. Sadly, Energy Transfer has not yet revealed these results, in part because they have not filed their 10-Q as of this writing. But there are some other profitability metrics that could be viewed as comparables. Perhaps the most popular when it comes to a business like this is the DCF, or distributable cash flows. This number did decrease year over year, falling from $2.08 billion to $2.01 billion. Higher interest expense, a rise in maintenance capital expenditures, and a few other factors, were instrumental in bringing this down. At the same time, EBITDA for the company expanded from $3.34 billion to $3.43 billion.

In the case of EBITDA, the picture for the company was complicated. There are many working parts, with some having worked out quite well during the quarter, while others performed poorly. The worst aspect of the company involved its Midstream segment. Profits there fell from $807 million to $641 million. This came about even in spite of gathered volumes climbing 13.9% year over year and NGL production growing 7.1%. The biggest hit for this segment came from a $138 million decrease in non-fee based margin because of unfavorable natural gas prices of $70 million and lower NGL prices they hit the company to the tune of $68 million. A $54 million increase in operating expenses, caused by repairs, material, equipment rental costs, employee costs, and other factors, also hit the business.

The biggest bright spot for the company, however, involved its NGL and refined products transportation and services activities. This number spiked from $700 million to $939 million. On this front, the company benefited from A $90 million benefit in marketing margin caused by the optimization of NGL and refined product inventories, as well as in northeast blending and optimization. A further $83 million benefit in transportation margin was driven by higher y-grade throughput and higher rates that were caused by contractual rate escalations in the Texas pipeline system. There were some other factors as well, such as a $49 million rise in terminal services margin and a $25 million benefit in fractionators and refinery services margin.

{kind=link}

Energy Transfer

Factoring in operational improvements, as well as the company's acquisition of Lotus Midstream in a deal valued at $1.45 billion, management felt confident enough to raise EBITDA guidance for this year to between $13.05 billion and $13.45 billion. This compares to the prior expected range of between $12.90 billion and $13.30 billion. We don't really know what to expect when it comes to the other profitability metrics. But if we assume that they will increase at the same rate that EBITDA it's forecasted to at the midpoint, then we should anticipate DCF for the company of $7.58 billion for the year and adjusted operating cash flow of $10.91 billion. Now, before I move on, there is one thing I should mention. Earlier in this article, I said that we don't know what the operating cash flow data for the enterprise just like. We are also out of the loop on some of its balance sheet data. For instance, we know that cash is around $0.3 billion, but we don't know precisely how much since management hasn't reported it yet. For the purpose of valuing the company, I did take some liberties here, using what data we do have and adopting some of the figures from the fourth quarter of last year.

{kind=link}

Author - SEC EDGAR Data

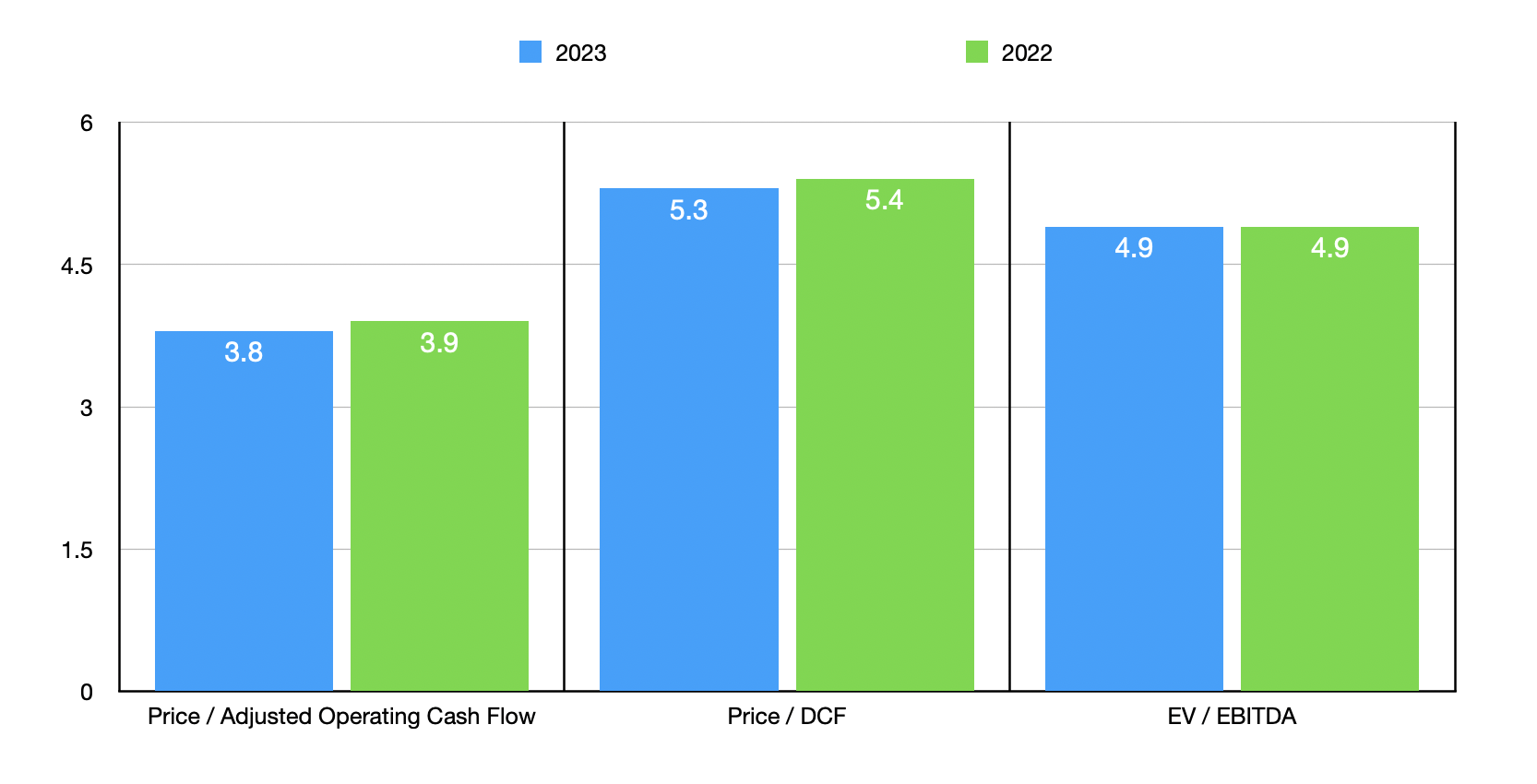

Taking these results, I was able to value the company fairly easily. As you can see in the chart above, on a forward basis, Energy Transfer is trading at a price to adjusted operating cash flow multiple of 3.8 and at a forward price to DCF multiple of 5.3. Meanwhile, the EV to EBITDA multiple for the company should be around 4.9. As you can see in the aforementioned chart, these numbers are not too different from what we get using data from 2022. As part of my analysis, I did decide to compare Energy Transfer to five similar firms. These results can be seen in the table below. On a price to operating cash flow basis, only one of the five companies is cheaper than our prospect. Meanwhile, using the EV to EBITDA approach, it is the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Energy Transfer |

| 3.8 |

| 4.9 |

| TC Energy Corporation ( TRP ) |

| 8.2 |

| 17.9 |

| Kinder Morgan ( KMI ) |

| 7.2 |

| 11.0 |

| The Williams Companies ( WMB ) |

| 7.3 |

| 10.9 |

| Cheniere Energy ( LNG ) |

| 3.6 |

| 11.3 |

| Enterprise Products Partners ( EPD ) |

| 6.7 |

| 9.0 |

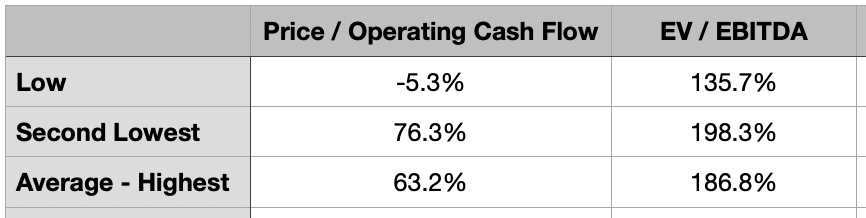

As I did in the earnings preview article that I wrote about the enterprise, I decided to see what kind of upside potential, if any, shares might offer if the firm were to trade at levels that would be more similar to its rivals. In the table below, you can see this using both the price to operating cash flow approach and the EV to EBITDA approach. I looked at three different scenarios here. In the first scenario, I calculated what kind of upside or downside would exist if it were to trade at the same multiples as the cheapest of its rivals. In this case, from a price to operating cash flow approach, Energy Transfer would warrant downside of 5.3%. But when it comes to the EV to EBITDA approach, we get upside of 135.7%. In the second scenario, I looked at what kind of upside would exist if it were to trade at the same level as the second cheapest peer. In this case, upside would be between 76.3% and 198.3%. And in the final scenario, I stripped out the most expensive of the group, averaged out the other four, and calculated its upside based on that. In this case, upside would be between 63.2% and 186.8%. Given how cheap most of the companies our trading at in this space, I would argue that upside it's probably closer to a double from here than anything.

{kind=link}

Author - SEC EDGAR Data

Takeaway

From all that I can see, things are going quite well for Energy Transfer. Although the company missed on both the top and bottom lines, its overall cash flow picture is incredibly attractive. Management is allocating around $2 billion this year toward growth initiatives and plans to invest heavily next year as well. But even without this kind of growth, shares of the business look incredibly cheap and its overall business model is most certainly sound. Recently, management also increased the distribution and is targeting further increases each year moving forward. With an effective yield of 9.7% right now, I don't mind waiting for additional upside to come into play. But when it does, I suspect that investors will find themselves incredibly happy. Because of all of this, I have no problem keeping the company rated a ‘strong buy’ for now.

For further details see:

Energy Transfer: Strong Upside Warranted From Here