FANG - Enerplus: Strong Independent But The Focus On Buybacks Is Disappointing

2023-07-24 17:31:01 ET

Summary

- Enerplus Corporation is a Canadian independent E&P that operates in the Bakken Shale and Marcellus region.

- The company's production is a blend of crude oil and natural gas, which is nice as the fundamentals of both products are pretty good right now.

- The company has strong free cash flow, but it is spending it on buybacks instead of dividends and this appears to be handicapping the company's total returns.

- The company has a very strong balance sheet and minimal debt.

- Enerplus is currently trading at a fairly attractive valuation.

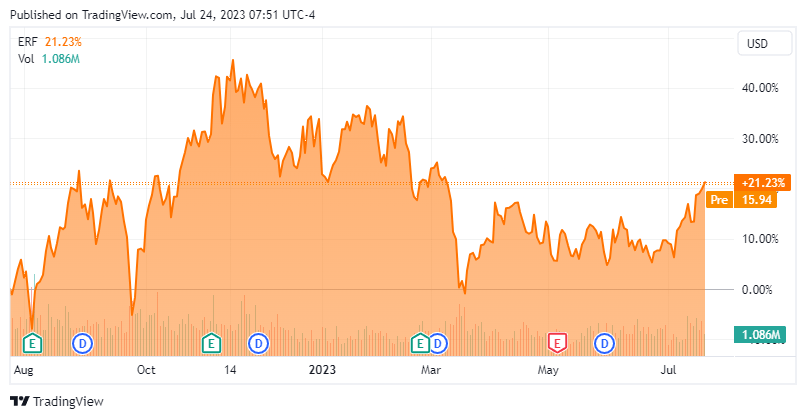

Enerplus Corporation ([[ERF]], [[ERF:CA]]) is a Canadian independent exploration and production company that primarily operates in the Bakken Shale. The company also has some significant exposure to the Marcellus Shale of Appalachia, which gives it some natural gas production. This is nice due to the simple fact that the global demand for natural gas is growing at a very rapid pace, and is likely to continue to do so for quite a while. The company's stock price has delivered a very strong performance recently, as it is up 21.23% over the past twelve months despite both crude oil and natural gas prices being down over the same period:

{kind=link}

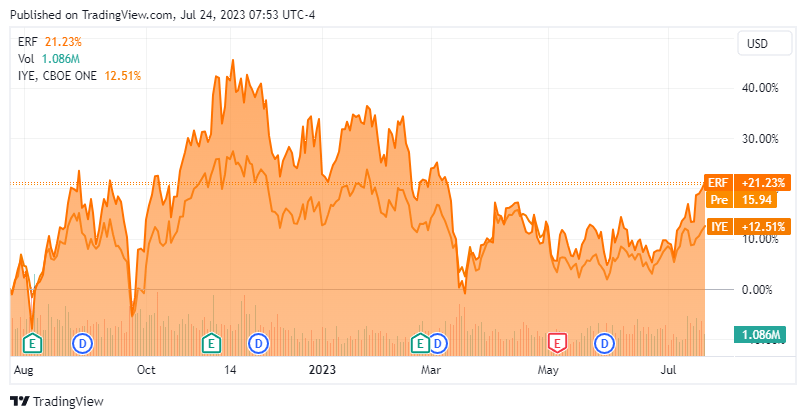

This is quite a bit better than the energy sector as a whole, as the iShares U.S. Energy ETF ( IYE ) is only up 12.51% over the same period:

{kind=link}

Despite this strong performance, though, the stock appears to be very affordable today, and it is certainly much cheaper than the market. We will discuss this later in this article. The company has also been growing its production at a reasonably rapid pace, so it is not simply a value play but a value and growth play. Let us investigate and see if this company could be a good addition to your portfolio today.

About Enerplus Corporation

As stated in the introduction, Enerplus Corporation is a Canadian independent exploration and production company that primarily operates in the Bakken and Marcellus Shale plays in the United States. The company has a fairly long history, which is detailed on its webpage :

Founded in 1986, Enerplus was Canada's first oil and gas royalty trust with a proven track record for delivering competitive returns for our shareholders. As we transitioned our assets to focus on unconventional, organic growth opportunities, we have continued to prioritize responsible development and thoughtful investment to create value for our shareholders.

Today, we're an independent North American exploration and production company focused on developing our high-quality assets through a disciplined, returns-based capital program. This focus, our accountability and our people will help us deliver differentiated long-term shareholder value.

The company was originally a Canadian royalty trust, which was a Canadian company similar to a real estate investment trust that was able to effectively avoid taxation on a corporate level in exchange for paying out nearly all of its income to investors. They were largely eliminated as a business model in 2011 when Canada decided to change the taxation of them in order to collect about $500 million in extra taxes. This was more than ten years ago so is largely irrelevant now, but it does show that the company has a long history of returning its income to the shareholders. This is something that continues today, as we will discuss later.

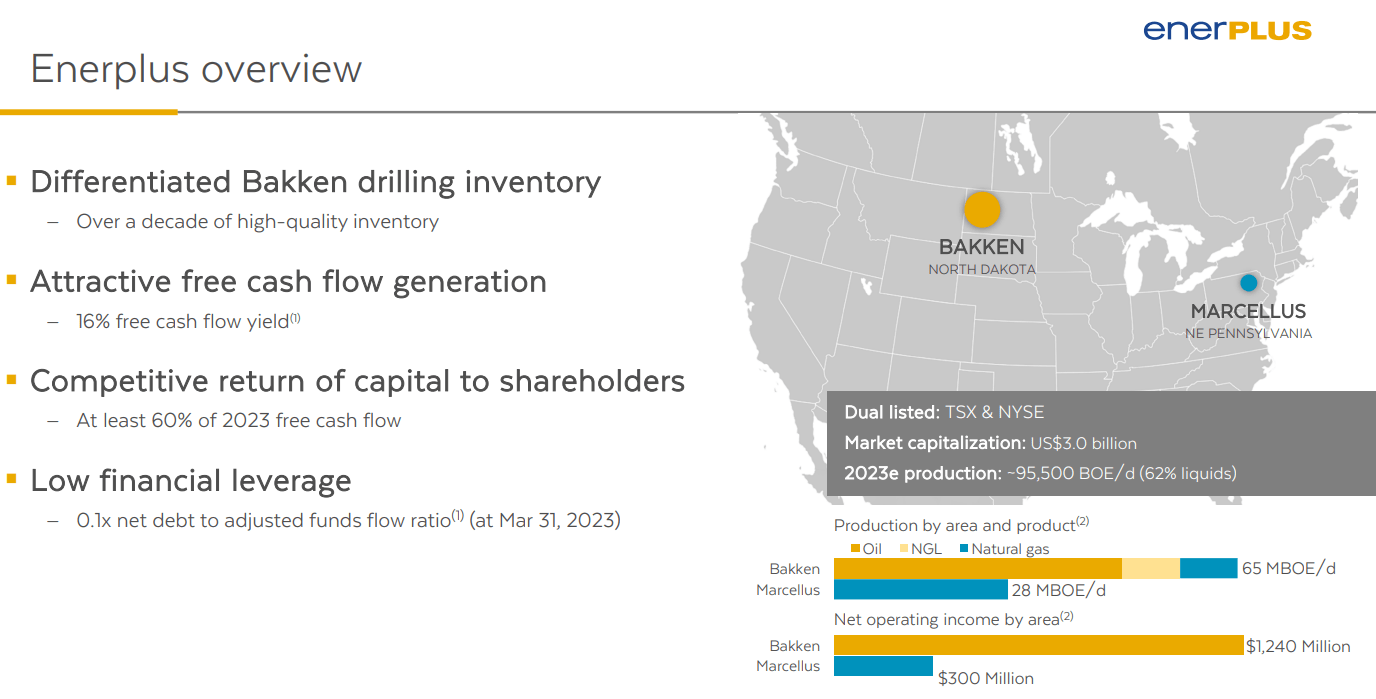

As just stated, Enerplus operates mostly in the Bakken and Marcellus Shale plays in the United States:

{kind=link}

The company formerly had operations in the Western Canadian Sedimentary Basin, but it sold them last year to Journey Energy. The company's reason for the sale appears to be that its Canadian assets were earning lower returns than its operations in the United States and so were reducing the effective return on capital that it was able to provide for its shareholders. This fits with our narrative of this being a company that is focused on maximizing shareholder returns. The fact that the majority of its operations are in the United States has induced the company to report its financial results in U.S. dollar terms, making this one of the only Canadian companies to do so.

The fact that Enerplus's operations are split between the Bakken and Marcellus Shales provides it with a split between crude oil and natural gas production. After all, the Bakken Shale is generally considered to be a crude oil play but nobody goes to the Marcellus Shale in search of crude oil. The Marcellus is a natural gas and natural gas liquids play. We can see this reflected in the two charts above, as the company's Bakken Shale production is split between crude oil, natural gas liquids, and natural gas but its production in the Marcellus is entirely natural gas. In aggregate, Enerplus has provided guidance of an average production of 93,000 to 97,000 barrels of oil equivalents per day in 2023. Of this, about 57,000 to 61,000 barrels of oil equivalents per day will be liquids. At the midpoints, this makes the company's production about 62.15% liquids (crude oil or natural gas liquids), which is reasonable.

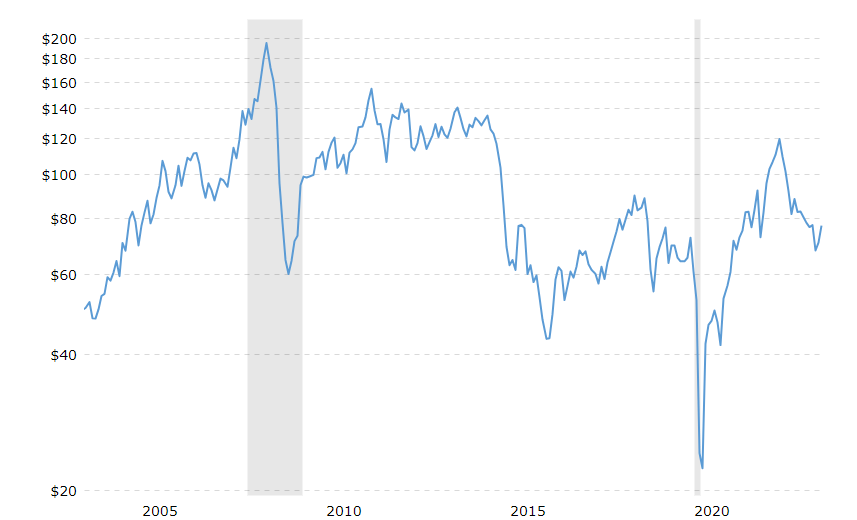

Admittedly though, this is less important than it was a decade ago. In the few years following the financial crisis and recession, we had some of the highest inflation-adjusted crude oil prices that have ever been seen. As we can see here, crude oil prices during that time were actually broadly higher than they were even during 2022:

{kind=link}

However, this was only true for crude oil, not natural gas. Natural gas prices were actually quite depressed. In fact, natural gas prices were so low that it was normally flared off as it cost the company more to bring the natural gas to the market than the producer could obtain by selling it. As such, investors were most attracted to those upstream companies that had most of their production in the form of crude oil. This is not the case today though as natural gas can be produced profitably at today's prices and it is likely to see much stronger demand growth than crude oil over the coming years.

In fact, the production of crude oil and natural gas is quite cheap today. Enerplus's 2023 guidance has a company-wide cash flow breakeven of $17.30 per barrel of oil equivalent produced before taxes:

{kind=link}

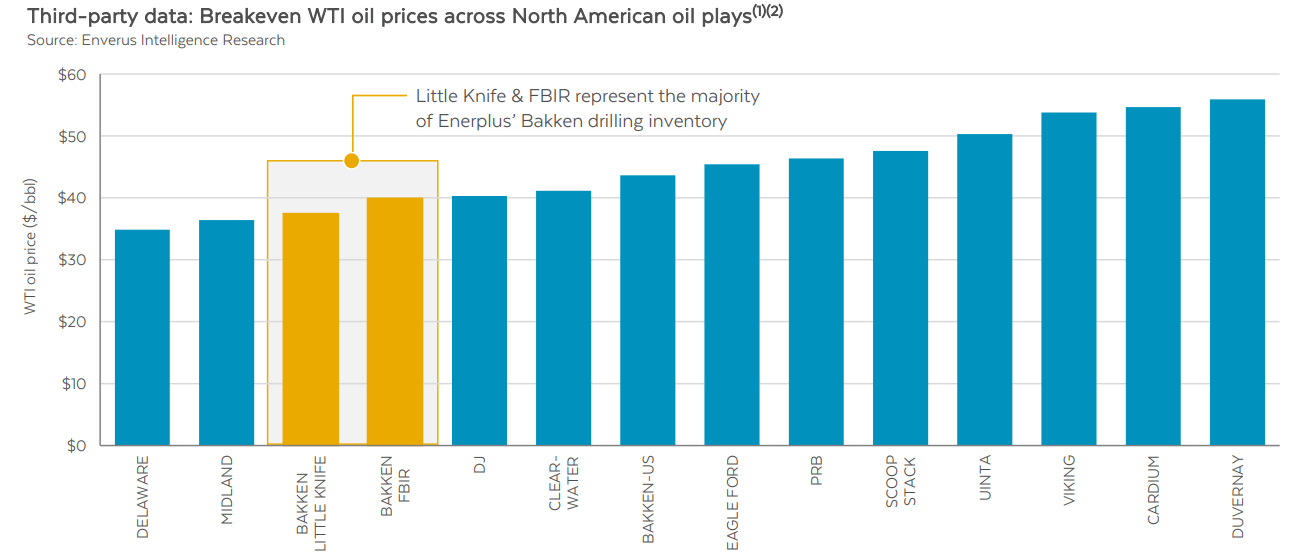

This does vary somewhat depending on the basin, however. The majority of Enerplus's crude oil production is in the Little Knife and Fort Berthold Indian Reservation regions of the Bakken Shale. The average cash flow breakeven in these areas is between $35 and $40 per barrel, which is one of the lowest production prices in the United States:

{kind=link}

As of the time of writing, the price of West Texas Intermediate crude oil is $77.79 per barrel. That is substantially above the cash flow breakeven for the majority of Enerplus's production, which is nice as it positions the company very well to enjoy strong profits today. Enerplus has a 16% free cash flow yield based on its expected 2023 free cash flow assuming an average of $80 per barrel West Texas Intermediate price and $3 per thousand cubic feet of natural gas. These average prices are both very reasonable considering that both crude oil and natural gas are close to those levels today.

The fact that Enerplus enjoys a high free cash flow yield is something that any shareholder should appreciate. After all, this is the money that can be used for things that benefit the common stockholders such as reducing debt, buying back stock, or paying a dividend. Enerplus is, in fact, doing exactly that. The company has committed to return at least 60% of its annual free cash flow to investors through dividends and share buybacks. This is similar to the promises that have been made by other shale producers such as Diamondback Energy ( FANG ), Pioneer Natural Resources ( PXD ), and Devon Energy ( DVN ). Unfortunately, in the case of Enerplus, the company has opted to focus its efforts on share buybacks. The dividend is only a meager $0.055 per share quarterly, which is a 1.38% yield at the current price. As regular readers are no doubt well aware, I generally prefer dividends to share buybacks because dividends represent actual cash in your pocket that can be reinvested, used to pay bills, or any number of other things.

In theory, a share buyback should raise the stock price and thus represent a tax-efficient way to provide a return to shareholders but in practice, they do not always work as advertised. A variable dividend as some of Enerplus's peers have implemented would still give the investor the ability to increase the value of their holdings by reinvesting it in shares of Enerplus. Alternatively, that money could be used to invest in another company for diversification purposes, or even used to pay bills rather than selling your assets for money. If the shares are held in a retirement account, we do not need to worry about the tax implications. Thus, a variable dividend would probably work out better for the average retail investor than the share buybacks that Enerplus is dedicating its free cash flow towards.

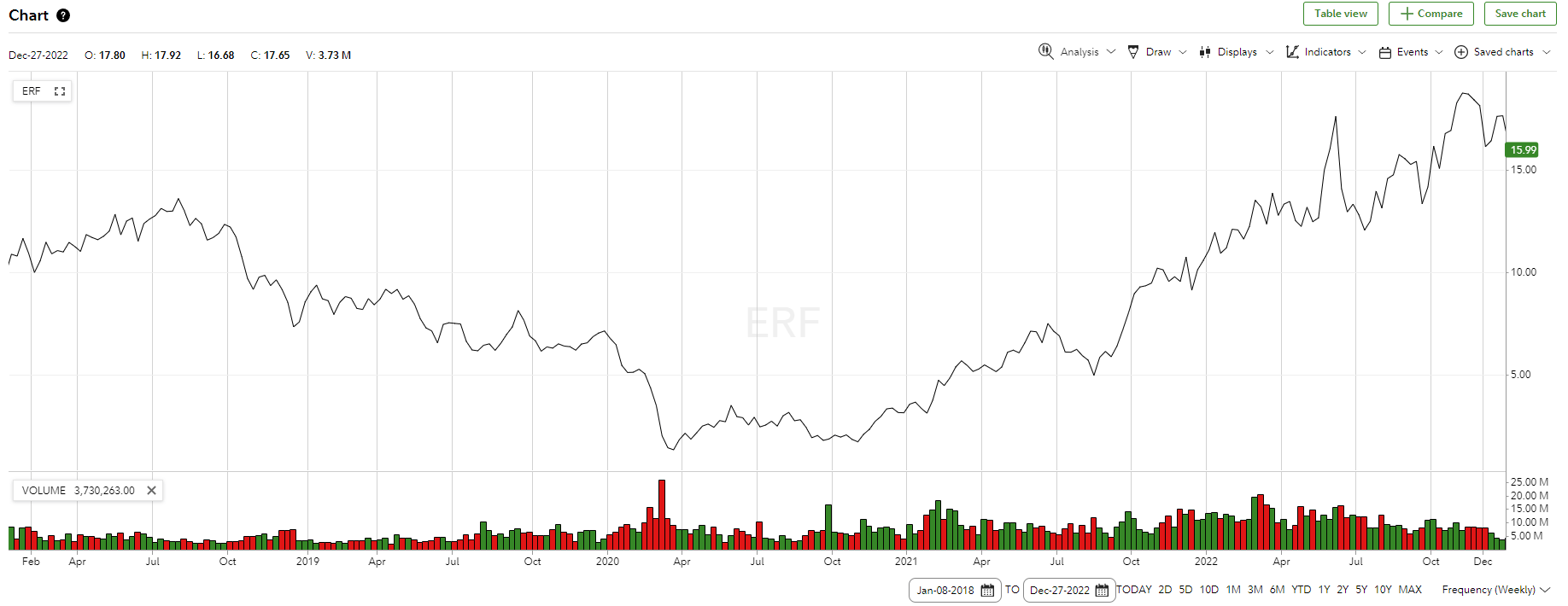

We can very clearly see the company prioritizing its share buyback over its dividend in the fact that it spent $730 million on buybacks between January 1, 2018, and December 31, 2022. Over the same period, Enerplus spent $135 million on dividends. Here is the stock chart for that period:

{kind=link}

The company's shares went from $9.99 per share to $17.65 over the period. That is a 76.68% increase over the five-year period. That is a 12.05% compound annual growth rate, which is not too bad but it is still much worse than the S&P 500 Index (SP500) managed to deliver over the same time period. The stock has since declined to $15.99 though, thus reducing your returns. This actually knocks it down to an 8.79% compound annual growth rate from January 1, 2018, through today. If the company would have opted to pay out the $730 million as dividends and you had reinvested the dividends, you would be much better off today, especially if you are investing in some sort of tax-advantaged account.

Financial Considerations

It is always important that we investigate the way that a company finances its operations before we make an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is normally accomplished by issuing new debt and then using the proceeds to repay the existing debt since very few companies have the ability to completely pay off their debts with cash as they mature. This can cause a company's interest expenses to increase following the rollover in certain market conditions. When we consider that interest rates in both the United States and Canada are currently at the highest levels that we have seen in years, this is a very real concern today. In addition to interest-rate risk, a company must also make regular payments on its debts if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. When we consider that Enerplus's cash flows will vary with commodity prices, this is a risk that we should not ignore.

One method that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity will cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of March 31, 2023, Enerplus had a net debt of $145.8 million compared to $1.1386 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 0.13 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| Enerplus Corporation |

| 0.13 |

| Diamondback Energy |

| 0.44 |

| Pioneer Natural Resources |

| 0.23 |

| Matador Resources ( MTDR ) |

| 0.21 |

| Devon Energy |

| 0.53 |

| Coterra Energy ( CTRA ) |

| 0.13 |

As we can clearly see here, Enerplus Corporation is somewhat less dependent on debt as a source of financing for its operations than nearly all of its peers. This is a good sign as it indicates that we probably do not need to worry about the risks of the company's leverage since it is not excessively dependent on it.

Another ratio that we can use to judge a company's leverage is the leverage ratio, which is defined as net debt-to-adjusted funds flow from operations. This ratio essentially tells us how many years it would take the company to completely pay off its debt if it were to devote all of its cash flow to that task. As of March 31, 2023, Enerplus had a leverage ratio of 0.1x based on its trailing twelve-months adjusted funds from operations. This is a very reasonable ratio that is well below comparable ratios from its peers. This tells us that the company should not have any difficulty carrying its debt, even if its cash flow declines somewhat. Overall, there should be nothing for us to worry about here.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of an independent exploration and production company like Enerplus Corporation, we can value it by looking at the forward price-to-earnings ratio. This ratio basically tells us how much we have to pay today for each dollar of earnings that the company is expected to generate over the next year.

According to Zacks Investment Research , Enerplus Corporation currently has a forward price-to-earnings ratio of 7.68 at today's stock price. Here is how that compares to the company's peers:

| Company |

| Forward P/E Ratio |

| Enerplus Corporation |

| 7.68 |

| Diamondback Energy |

| 8.06 |

| Pioneer Natural Resources |

| 11.10 |

| Matador Resources |

| 8.90 |

| Devon Energy |

| 9.05 |

| Coterra Energy |

| 11.12 |

As we can clearly see, Enerplus Corporation currently appears to be cheaper than any of its peers. The company looks even more affordably priced when we consider that the S&P 500 Index has a forward price-to-earnings ratio of 19.40 at the current level. This reinforces the statements that I have been making for quite some time now about the entire traditional energy sector being ludicrously undervalued. Enerplus is among the most undervalued companies in the sector though, so it might be worth considering.

Conclusion

In conclusion, Enerplus Corporation is an independent shale energy producer with a very reasonable production split between crude oil and natural gas. This is nice as it gives the company exposure to the fundamentals of both substances and crude oil and natural gas are both expected to see forward demand growth globally over the coming years. Enerplus is also highly profitable, but it has been using its profits to fund a massive share buyback program instead of dividends. This is disappointing since shareholders would probably be better off with dividends. Enerplus Corporation appears undervalued and has a very strong balance sheet , though, so it might still be worth considering.

For further details see:

Enerplus: Strong Independent But The Focus On Buybacks Is Disappointing