EGIEY - Engie Brasil: A Defensive Stock Losing Luster

2023-12-12 17:36:19 ET

Summary

- Engie Brasil operates in electricity generation, transmission, and gas transportation, creating a resilient business model.

- The company exhibits consistent growth in net revenue, EBITDA, and net profit, maintaining strong profitability ratios.

- Q3 2023 faced hurdles, including a revenue decline and lower volumes from complementary sources, impacting EBITDA.

- Engie Brasil has a robust history of dividend distribution, targeting a minimum of 55% of adjusted net profit, making it an attractive income stock.

- Despite being a defensive asset, a neutral stance is maintained due to concerns about a slightly stretched stock valuation and the potential for greater appreciation in other companies like Eletrobras.

Engie Brasil ( EGIEY ) is Brazil's second-largest power generation company, ranking only behind Eletrobras ( EBR ). The company operates in power transmission and gas transportation segments.

The most significant shareholder of Engie Brasil is Engie Participações, the exclusive controller holding 68.7% of the shares. This holding company channels investments from the country's French multinational Engie S.A. ( ENGIY ), a global leader in energy, operating in electricity generation and transmission, nuclear energy, natural gas, and oil in multiple countries.

Engie Brasil has its own installed capacity of 8.5 GW across 27 plants, representing about 4.6% of the country's centralized generation capacity. The company's energy matrix is entirely from renewable sources, with hydroelectric (76%), wind (20%), solar (3%), and biomass (1%) plants.

With a secure position in long-term concessions and a track record of prudent capital allocation, the investment thesis revolves around considering Engie Brasil as a defensive asset due to its robust dividend payouts, reaching up to 100% of its profits.

The conservative strategy, avoiding reliance on excessive growth, depending on concession renewals, and factoring in high energy prices, safeguards against principal risks in the Brazilian market, such as asset replacements and hydrological challenges.

However, the current emphasis on short-term investments in renewable energies, like solar, diminishes the attractiveness of the investment thesis, particularly in terms of dividends and earnings growth. This is further compounded by the potentially high valuation of the company.

Engie Brasil's Business Model

Engie Brasil is an energy company operating in various segments of the electricity sector. Its comprehensive business model covers generation, transmission, commercialization, and energy services.

{kind=link}

Energy Generation

Operating under concessions typically spanning 30 years, Engie Brasil's Energy Generation revenue is based on the volume of energy sold (MWh) and the price (R$/MWh). Contracts can be signed on the regulated market for auctions with distributors or on the free market for company negotiations.

Throughout the concession period, the energy's selling price is readjusted by a chosen inflation index, usually, the IPCA, measuring inflation in Brazil. This segment is crucial for the company, contributing to 68% of net revenue and 77% of the adjusted EBITDA.

With a diverse portfolio, the company maintains a weighted average term (by physical guarantee) of around 17 years for its concessions, with no maturities until 2030. This positioning provides stability for maintaining and potentially expanding results, given the company's numerous projects in the development phase that could materialize in due course.

Energy Transmission

In the energy Transmission business, operating under 30-year concessions, bills are based on the Permitted Annual Revenue ((PAR)) established in bidding auctions. PAR has adjusted annually for inflation, running in biannual cycles from July 1 to June 30 of the following year. Results are linked to the operation (availability) of the lines rather than the volume of energy transmitted.

The weighted average term by PAR is approximately 26 years due to the company's recent entry into the segment. Engie Brasil holds RAP concessions primarily indexed to IPCA for readjustments, with older IGP-M concessions. This segment is the least representative, contributing 6% of net revenue and 10% of adjusted EBITDA.

Gas Transportation

Engie Brasil has a 32.5% stake in Transportadora Associada de Gás [TAG] jointly controlled with Engie S.A. (32.5%) and CDPQ (35%). TAG is the largest natural gas transporter in the country, extending along the entire coastline of southeast and northeast Brazil.

The segment represents 14% of the company's adjusted EBITDA, contributing to the company's sustained profitability year after year.

Risks

However, considering the characteristics of its business model, we can also highlight the main associated risks, which primarily include:

Energy Prices: As Engie Brasil focuses on energy generation, it is significantly impacted by declining prices and their persistence at deficient levels. Renewing contracts on less attractive terms during these periods could affect the growth and viability of new expansion projects.

Asset Replacement: In the primary segments in which the company operates, particularly in auctions for acquiring transmission assets, intense competition can make it challenging to implement new ventures. The uncertainty surrounding the renewal of current concessions, subject to contractual conditions and revisions, may impact cash generation, distribution of earnings, and the value of shares.

Hydrological: Excessive dependence on favorable hydrological conditions, given their predominance in the generation matrix. In cases of a deficit in hydroelectric generation, Engie Brasil shares the burden proportionally, exposing it to the short-term energy market and potentially resulting in negative impacts on results due to high prices.

Engie Brasil's Financial Overview

Over the past decade, Engie Brasil has demonstrated a compound annual growth rate [CAGR] of 5.8% and 9.2% in its net revenue and EBITDA. This growth aligns primarily with the expansion of installed project capacity (2% YoY increase during the period) and the inflationary adjustments in energy sales contracts.

These effects are reflected in the company's margins. It's important to note that, as Engie Brasil recently expanded into transmission (a segment operating with an EBITDA margin of around 85%), the new margin levels should not be considered non-recurring.

The company's net profit demonstrates a consistent annual growth pattern of 8.9%. However, the 2021 result stood out due to several factors. Firstly, there was an impairment of R$1.1 billion. Additionally, there was the impact of inflation on concession payable adjustments, amounting to R$1.0 billion. Moreover, there were increased costs associated with energy purchases in the short-term market, totaling R$628 million. This represented a substantial 106.6% increase compared to 2020 and was necessary to address the deficit resulting from the hydric crisis in Brazil.

Concerning profitability, Engie Brasil maintains robust indicators within its sector, consistently achieving a historically high return on equity [ROE], currently at 40%, and a return on invested capital [ROIC], currently at 12.6%.

Regarding indebtedness, Engie Brasil operates with higher leverage compared to the period from 2014 to 2017, reflected in a net debt/EBITDA ratio ranging between 1.8x and 2.5 since 2018. Throughout this period, the increase in gross and net debt balances was offset by the expansion of results, maintaining the leverage indicator within a range that allows the balance sheet to accommodate dividend distributions and absorb new investment opportunities.

However, the company's level of leverage is deemed safe for a business model dependent on insensitive demand, price pass-through ease, and predictability in generating results.

Latest Financial Results

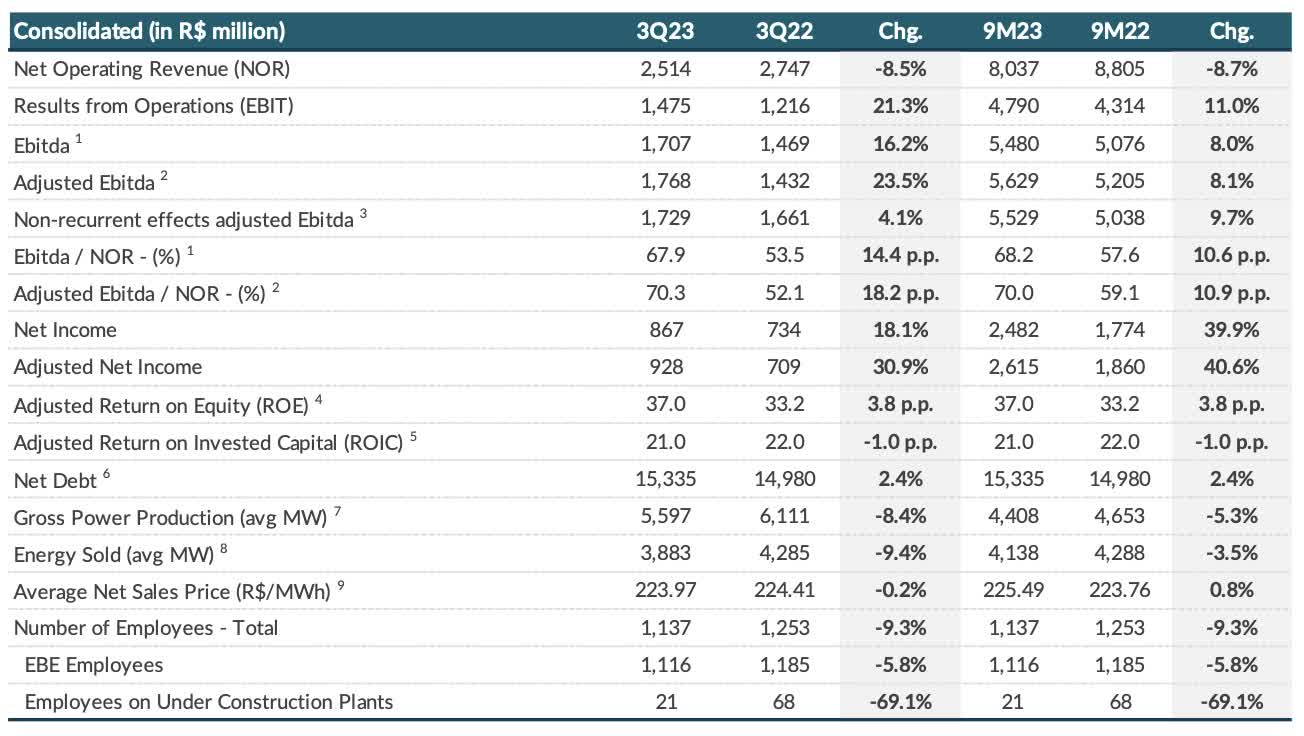

In the most recent quarter, Q3 2023, Engie Brasil experienced a challenging outcome amid low energy prices and disappointing volumes from complementary sources. The company reported operating revenues of R$2.5 billion for the quarter, marking an 8.5% decline compared to 3Q22.

{kind=link}

The primary factor contributing to the decrease in operating revenue was the negative impact of the Pampa Sul (coal plant) sale, which affected the company's net revenue by R$162 million. Lower volumes generated from complementary sources (wind and solar) at less favorable prices also weighed on the final result.

The average price of energy sales was R$223.9/MWh, showing a marginal decrease of 0.2% year-on-year. This occurred against the backdrop of lower prices and was also influenced by the average effect of the Pampa Sul contracts, which were higher than the current ones.

Consequently, the company's EBITDA closed the quarter at R$1.768 billion, marking a 16% increase compared to 3Q22. The operating performance of the "core" business (electricity generation) was disappointing due to low generation in the wind and solar segments amid an uninspiring price scenario. However, TAG's (gas segment) results were crucial in maintaining annual profitability. Excluding the impact of an impairment on one of its projects and construction revenues in the transmission segment, EBITDA would have been R$1.5 billion.

Moreover, the financial result for the quarter was negative at R$326 million (compared to -R$283 million in 3Q22) due to a decline in debt costs resulting from lower inflationary indices in the period and the settlement of debt instruments throughout 2022. As a result, the company's net profit amounted to R$867 million.

Dividends and Valuation

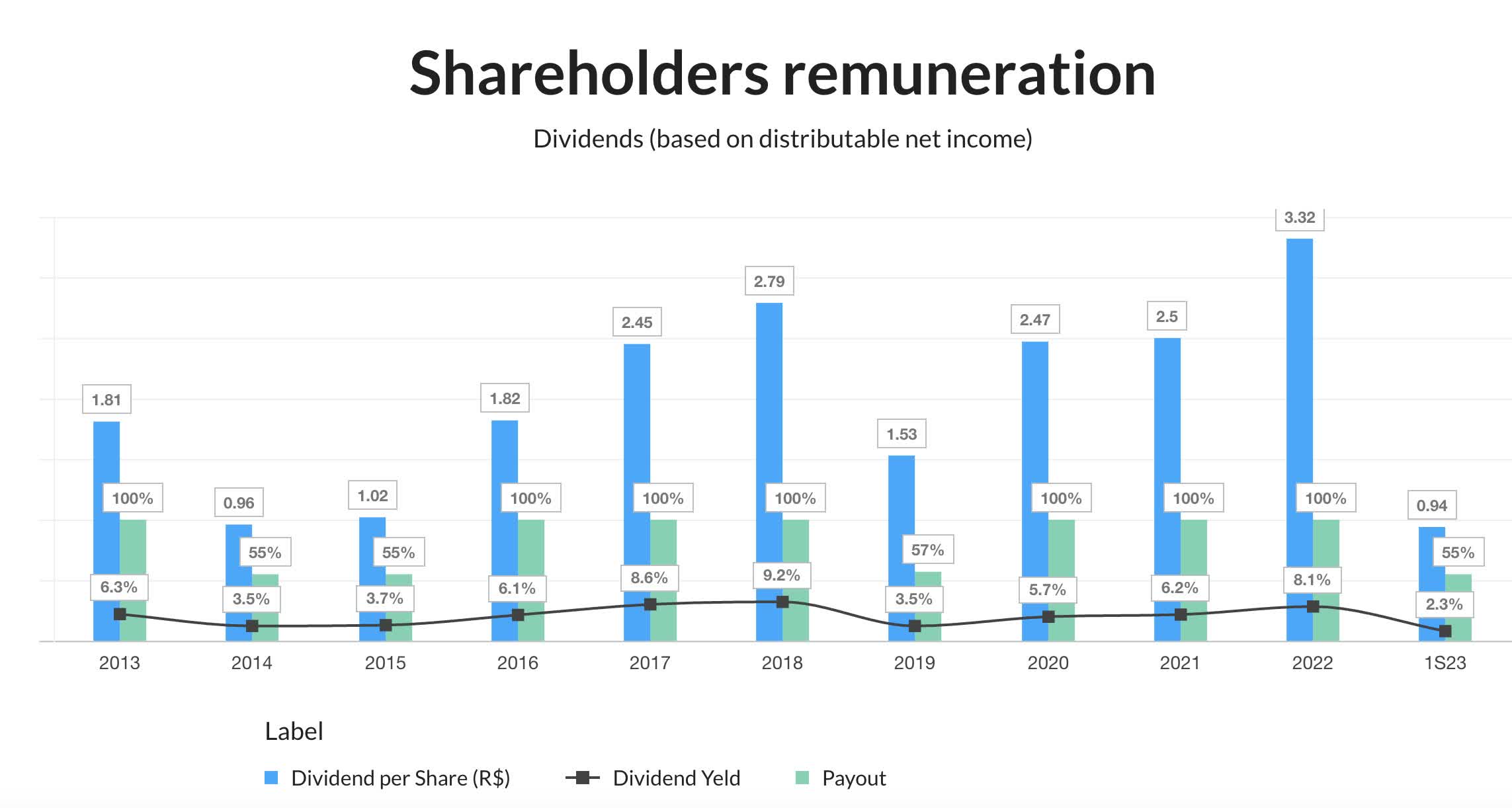

Under Engie Brasil's bylaws, it is obligatory to distribute dividends to shareholders, constituting no less than 30% of the company's net profit, as stipulated by corporate legislation. However, the company surpasses this requirement, following an indicative policy of disbursing a minimum of 55% of the adjusted net profit.

As a French company Engie S.A. subsidiary, Engie Brasil is dedicated to a robust distribution of its earnings to its controller, rendering it an appealing income stock with a defensive profile.

The company has consistently distributed nearly 100% of its profits in recent years, maintaining an attractive yield in the same proportion, particularly notable between 2020 and 2022.

{kind=link}

In 2023, during the year's first half, the company only distributed its minimum payout, resulting in a yield of 2.3%. In the third-quarter earnings call, the company announced a conservative decision to reduce its dividend distribution. This strategic move aimed to maintain a robust balance sheet, allowing the company to seize short-term opportunities.

Despite the dividend reduction, with a leverage of 2.7x in the second half of 2023, the company still possesses the financial flexibility to pursue further acquisitions in the sector without compromising its dividend-paying capacity.

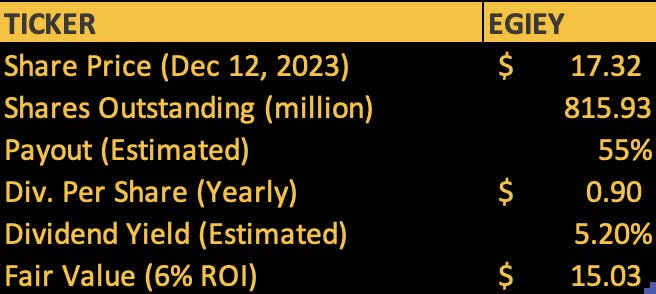

Considering the results from Q3 and estimating a minimum payout of 55%, Engie Brasil could potentially achieve a yield of 5.2%, projecting a net profit of $669 million for the year. Assuming an ROI of 6%, reflecting a low-interest-rate environment according to economic expectations, this would correspond to an implied price of $15. This valuation is slightly below the current share price of $17.32, suggesting that the stock might be considered potentially expensive.

Company's filings, compiled by the author

{kind=link}

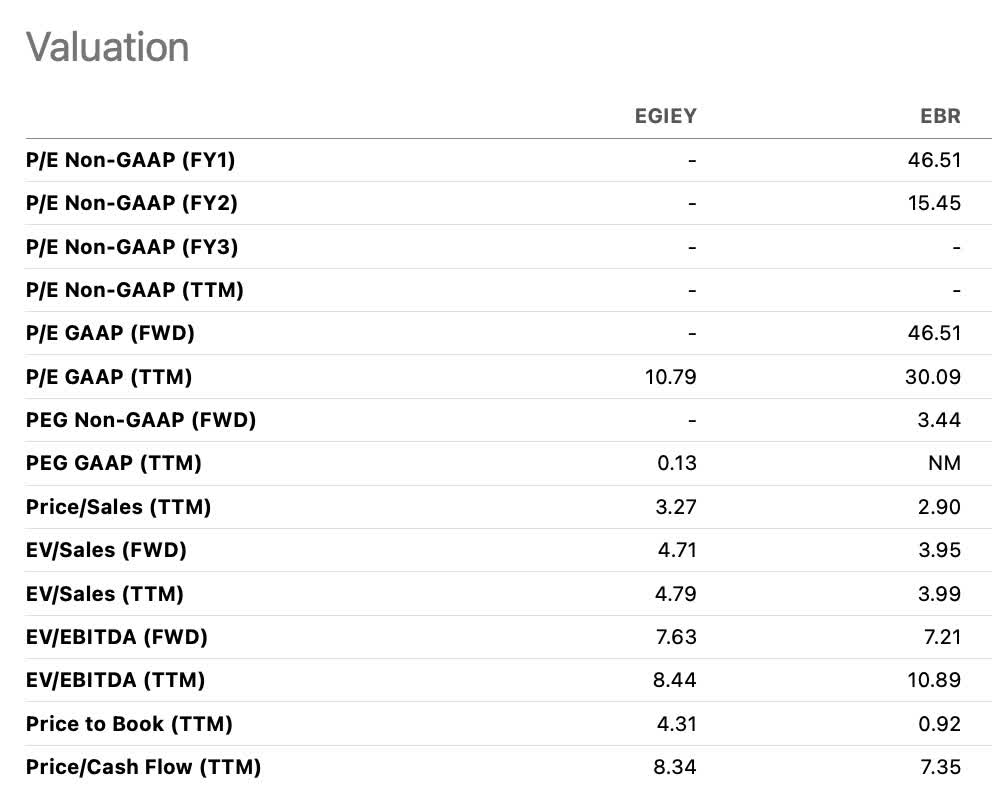

Comparing Engie Brasil with its leading peer in Brazil, the recently privatized Eletrobras, Engie Brasil trades at a more discounted EV/EBITDA multiple of 8.44x. However, it has a forward multiple that aligns more with Eletrobras's for the following year.

{kind=link}

The Bottom Line

The investment thesis for Engie Brasil positions it as a defensive asset suitable for the portfolios of conservative investors seeking reliable dividend-paying companies. Despite the absence of dividend announcements in the third quarter, there is anticipation for news in the following quarter, aligning with the company's policy of biannual dividend declarations.

Given that the company's shares are currently trading at a slightly stretched valuation, the assessment is that Engie Brasil's stock already reflects the company's potential. The belief is that other companies in the power generation sector have more significant potential for appreciation, such as Eletrobras, which is expected to benefit from its impending privatization. Therefore, my stance on Engie Brasil is neutral at this time.

For further details see:

Engie Brasil: A Defensive Stock Losing Luster