ENGQF - Engie: Solid Dividend But Likely No Upside From Here

2023-04-21 15:01:03 ET

Summary

- Engie is a French-based utility company shifting its focus from conventional sources (including nuclear) and doubling down on renewables with a massive CAPEX plan.

- The company has one of the least leveraged balance sheets of any major utility with a net debt/EBITDA of just 1.8x.

- The company also has a minimum dividend yield of 4.2% until 2025, but is very likely to yield 7-9% annually.

- Unfortunately I don't see any upside at this time leading to a HOLD rating.

- I discuss my thesis and strategy for the company.

Dear readers/followers,

Those of you that have been following me for a while know that I like investing in utilities mainly for their stable dividends and renewable energy exposure, which I expect to be the driving force in the industry, especially in Europe as the old continent transitions to a greener, more sustainable future. Currently about 7% of my portfolio is invested in renewable energy oriented utility companies, many of which I've covered here and I plan to increase this to 10% this year. Today I want to start coverage on one more potentially promising utility - Engie SA ( ENGIY ).

Note: As always the article will be based on the EUR-denominated native shares which trade under the ticker ENGI on the Euronext exchange in France. There are also two ADRs available under tickers ENGIY and ENGQF. I recommend you do your own research with regards to the tax treatment of each.

Engie

Engie is a French-based global utility company with operations mainly focused on France (24%), the rest of Europe (32%) and Latin America (17%). The company generates revenue primarily through electricity production and networks (electricity and natural gas). Their production is still heavily concentrated towards conventional source as renewables account for only 38% of their total generated capacity.

Historically a large portion of their capacity has been in nuclear, but recently the French and Belgian governments have pushed to shutdown nuclear power plants and although the shutdown has been postponed, most of the reactors are expected to be decommissioned by 2025. Engie has pushed to postpone the phase-out of nuclear and has reached an agreement in principle with the Belgian government to extend the operations of Doel 4 and Tihange 3 nuclear reactors by 10 years.

Still the direction the firm is heading is clear - they will exit nuclear eventually so they already classify nuclear assets as non-strategic and exclude them from reported figures. Notably, the company is planning to become a lot greener, targeting 58% of production from renewables by 2030. I generally like this direction. In 2022 alone, the company commissioned 3.9 GW of new capacity in renewables (wind + solar), bringing their total installed capacity to 38 GW.

Engie Presentation

Going forward Engie's CAPEX plan is massive as they plan to increase their annual investments by 50% (vs the last few years) and invest EUR 21-22 Billion over the period 2023-2025. 70% of this (EUR13-14 Billion) will be going into renewables to bring their capacity to 50 GW by 2025 and then 80 GW by 2030. That will put Engie's renewable capacity in line with Enel's.

Results

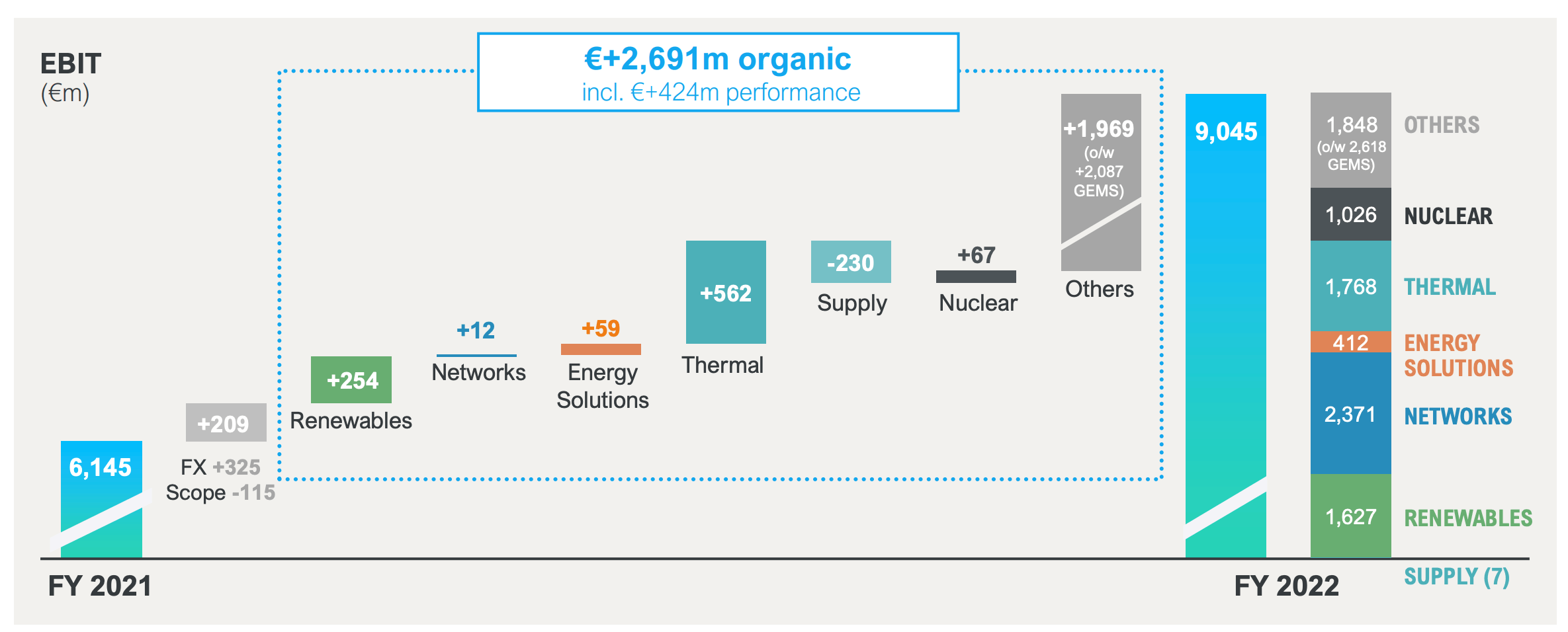

With regards to results , 2022 was a very strong year as EBIT increased by 47% to EUR 9 Billion. Beyond newly added capacity of renewables, this increase was almost entirely attributable to higher energy prices in Europe and is largely unsustainable.

{kind=link}

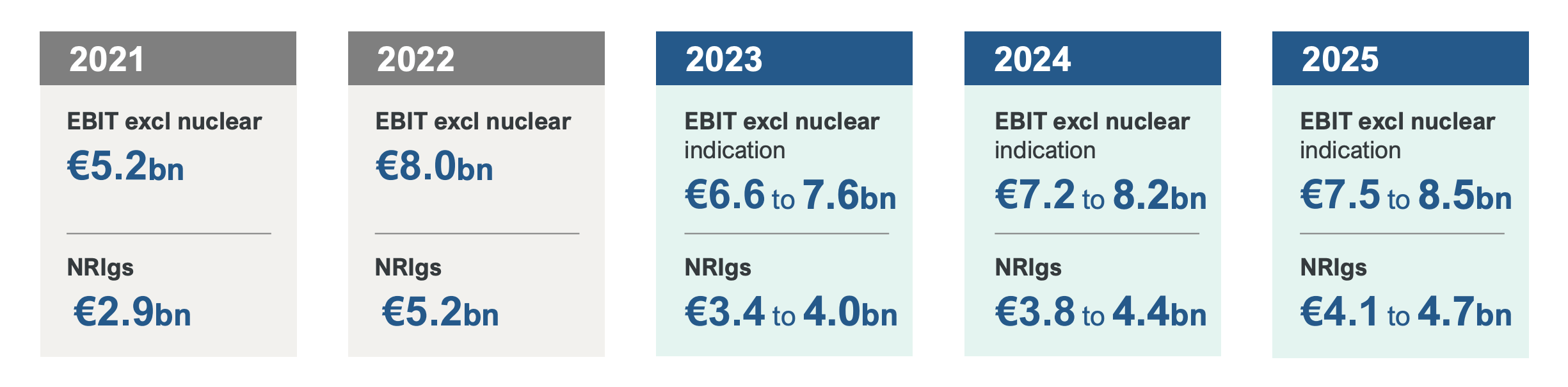

Going forward, management guides towards EBIT of EUR 6.6-7.6 Billion in 2023 - a relatively wide range given that 74% of France and Belgium production has been hedged to 93 EUR/MWh. Beyond this year the company forecasts 8% growth in 2024 and 4% growth in 2025.

{kind=link}

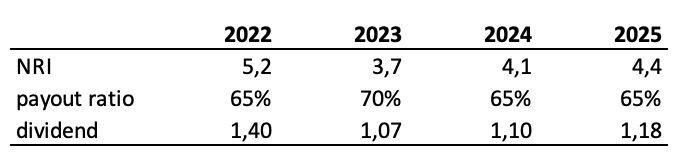

Now let's talk about the dividend which is critical to the performance of the investment. The group targets a payout ratio of 65-75% of net recurring income ((NRI)) and similarly to other European utilities has a floor of EUR0.65 per share for the 2023 to 2025 period. For 2022 the proposed dividend stands at EUR 1.40 per share which translates to a dividend yield of 9.0% and a payout ratio of 65%. That's great, but unfortunately with EBIT and NRI forecasted to drop, the dividend is likely to drop somewhat. For 2023 a 70% payout ratio at the midpoint of NRI forecast means an expected dividend of EUR 1.07 per share (significantly above the floor). At today's price that's a 7.0% yield on cost which is still very solid and it should grow from there.

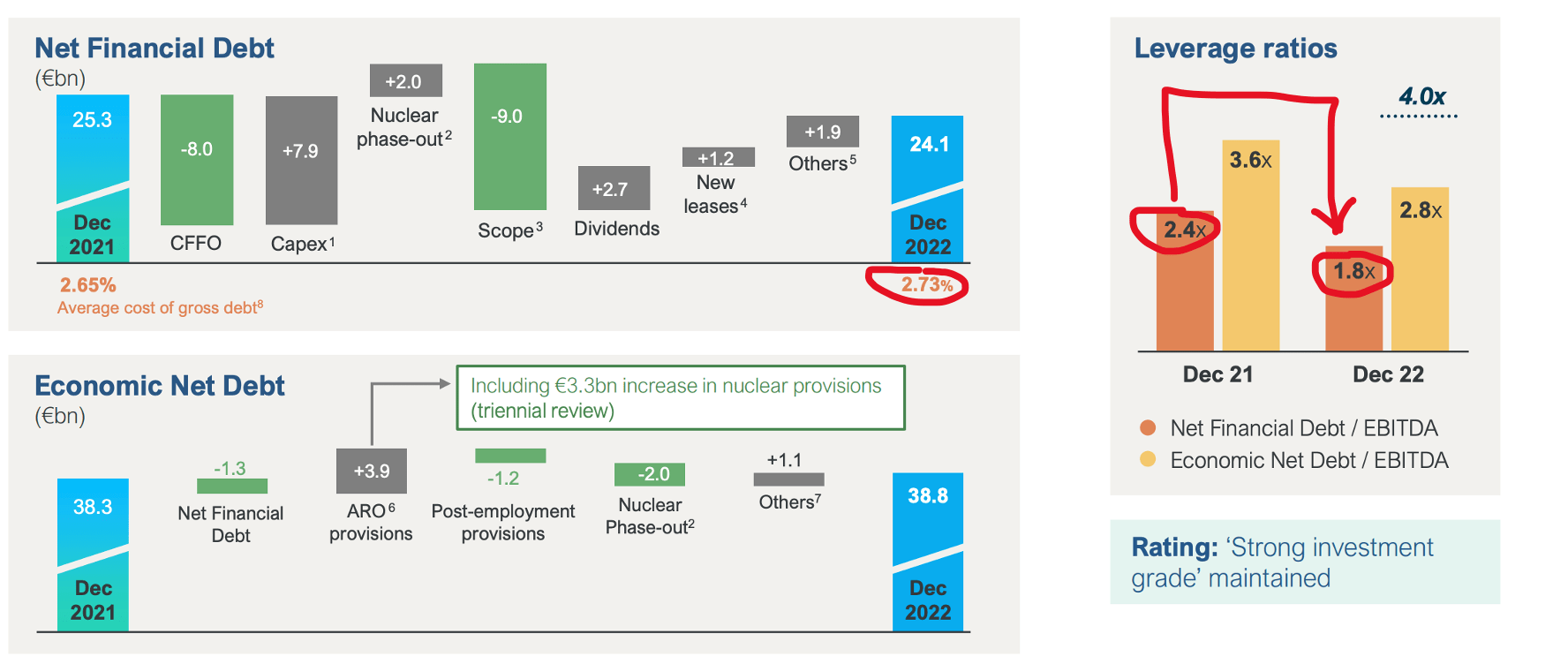

I also want to point-out that Engie has a solid BBB+ rated balance sheet. Their leverage is quite low at only 1.8x EBITDA (as they were able to deleverage from 2.4x EBITDA in 2021) and significantly below that of its peers. Enel for example has net debt/EBITDA of 2.6x. They also enjoy a very low average cost of debt of 2.73% which is unlikely to increase substantially with the majority of debt fixed and an average loan term of 12.5 years.

{kind=link}

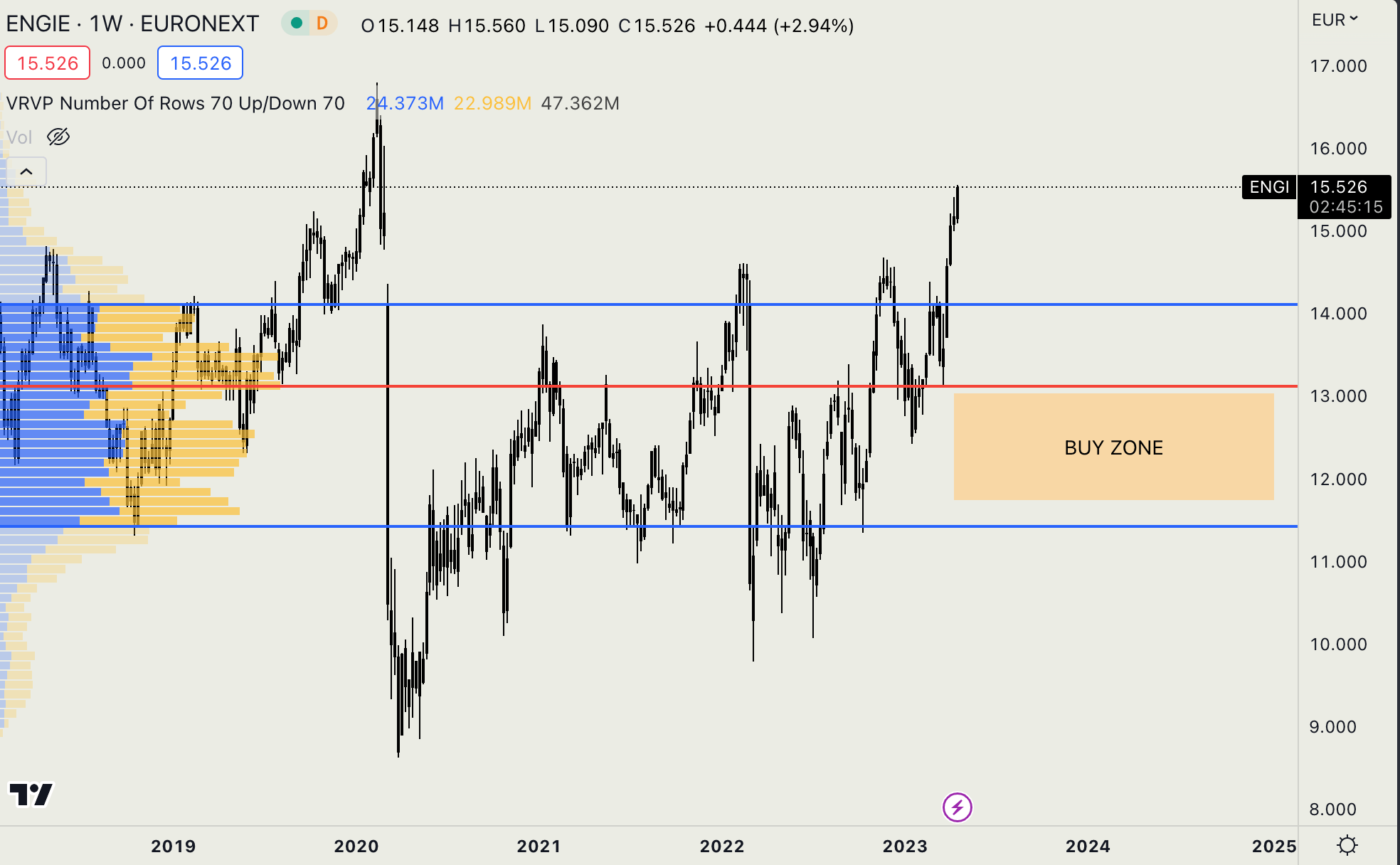

So with Engie you're getting one of the least leveraged balance sheets and a decent dividend yield. But how much is the stock realistically worth? To compute fair value, I'm going to take the average dividend over 2022-2025 of EUR 1.19 per share, assume no growth going forward and a required rate of return of 8%. A dividend discount model ((DDM)) yields a fair value of EUR15 per share equal to the price today of EUR 15.50. That's using a forecast that's neither aggressive nor overly conservative.

{kind=link}

To conclude, I don't see much alpha in Engie at this time. The company offers a (very) safe 7-9% yield, but following the recent rally, the company isn't undervalued anymore. That's why I rate Engie as a " HOLD " here at EUR 15.50 and would only consider adding to my position in the EUR 11-13 per share range (if it gets there). I'll trim a little around EUR 16.00 per share and keep holding.

{kind=link}

For further details see:

Engie: Solid Dividend But Likely No Upside From Here