ENGIY - Engie: Strong Q3 2023 Results Improve Full-Year Guidance

2023-11-09 11:24:29 ET

Summary

- Engie has reported improved earnings for the first nine months of 2023 and raised its FY 2023 revenue guidance.

- The company has made major investments in renewable energy and acquired a US-based battery company worth $1 billion.

- Engie's stock is cheaper than its peers, clear growth drivers and a healthy cash position, making it an attractive investment option.

Engie SA ( ENGIY ) has reported its Q3 2023 results , which showed an improvement in earnings for the first nine months of 2023. As a result, the company has raised its FY 2023 revenue guidance. Engie has performed well, with improved top and bottom line figures over the year, excluding nuclear. Importantly, the company's stock is currently much cheaper than its larger US-based utility peers. Engie also has an attractive cash flow and a healthy cash position, which will enable it to continue growing its business. In addition to this, Engie has made major investments into its renewable capacity, such as the recent acquisition of a US-based battery company worth $1 billion. Furthermore, the company has secured a nuclear reactor extension deal. At an attractively low FWD price-to-earnings ratio of 6.93, I believe the stock still has significant potential upside for long-term investors. Therefore, I maintain a bullish stance on this stock.

{kind=link}

Company updates

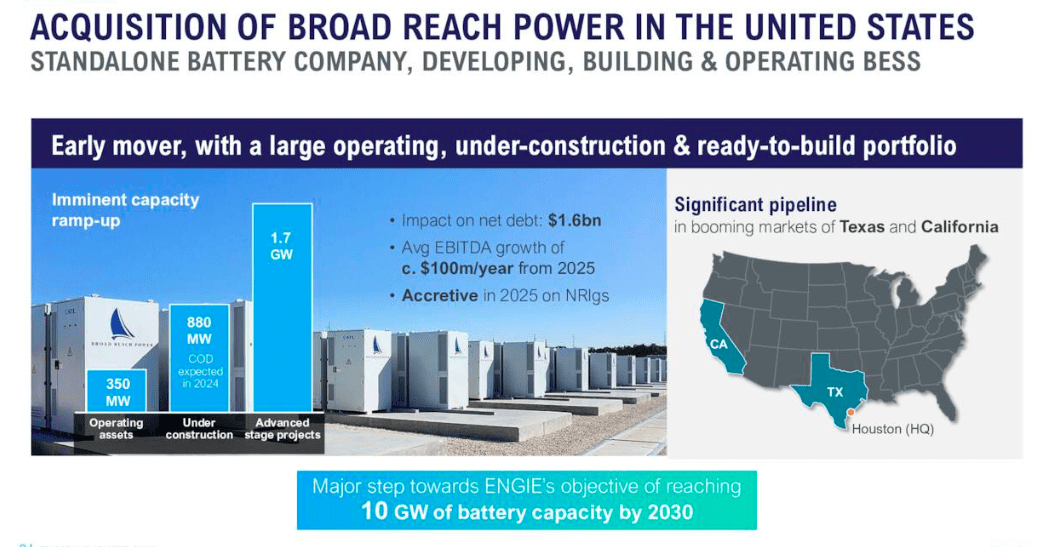

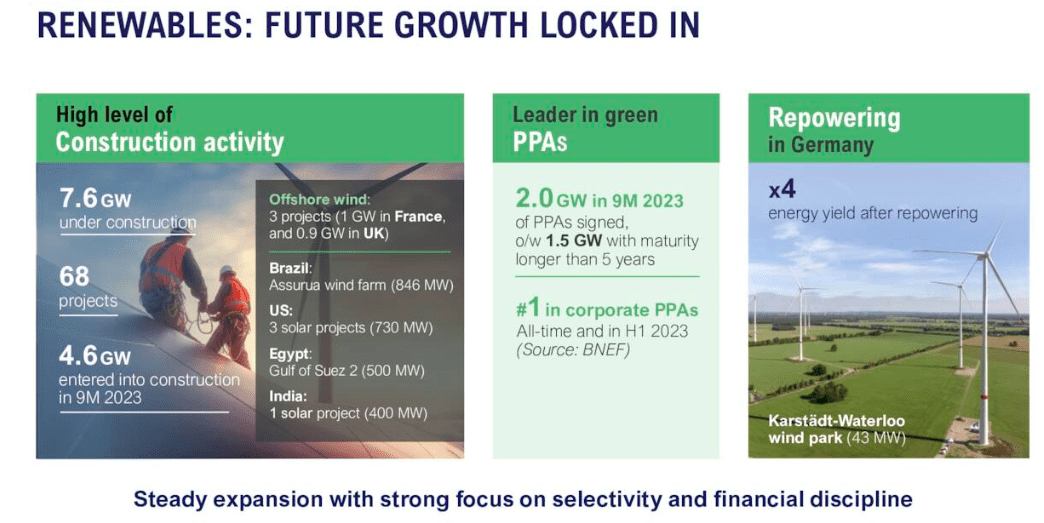

In my previous article , I provided an overview of the European utility company Engie. Over the last year, Engie has been an exciting company to follow, with its record-breaking financial results in FY 2022 and renewed nuclear contracts that will give the company long-term tailwinds within the European energy market. Looking ahead, Engie aims to increase its renewable energy capacity by 4 GW annually , with 7.6 GW already under construction. Recently, the company acquire US based battery company , for $1 billion. This indicates major steps towards growing its company globally within the renewable energy market.

{kind=link}

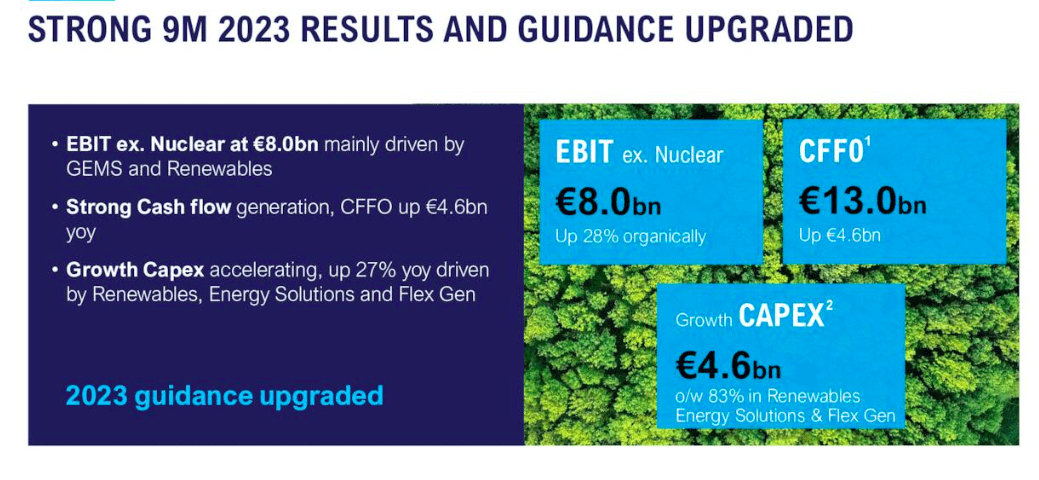

Due to strong performance the company is increasing its FY 2023 forecast from €4.7 billion to 5.3 billion euros in net recurring income to €5.1 billion euros to 5.7 billion. This can give us confidence in the short and long term regarding the company's potential performance.

{kind=link}

Engie versus US based utility peers

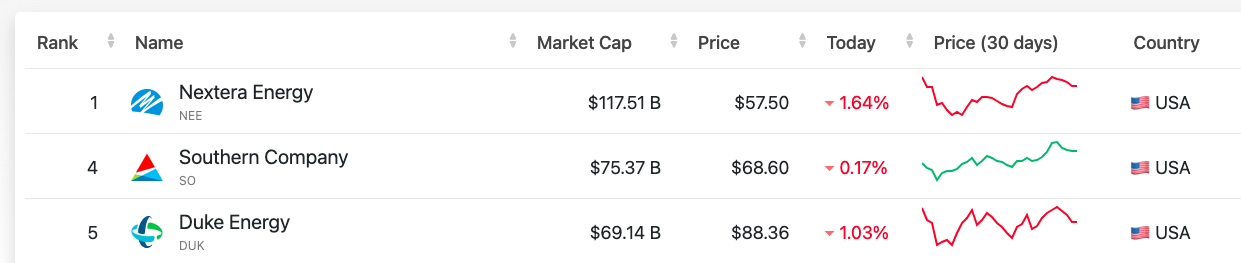

In my previous articles, I give an overview of Engie and compare it to the three largest utility companies in the USA based on market cap, namely NextEra Energy ( NEE ), Southern Company ( SO ) and Duke Energy ( DUK ).

{kind=link}

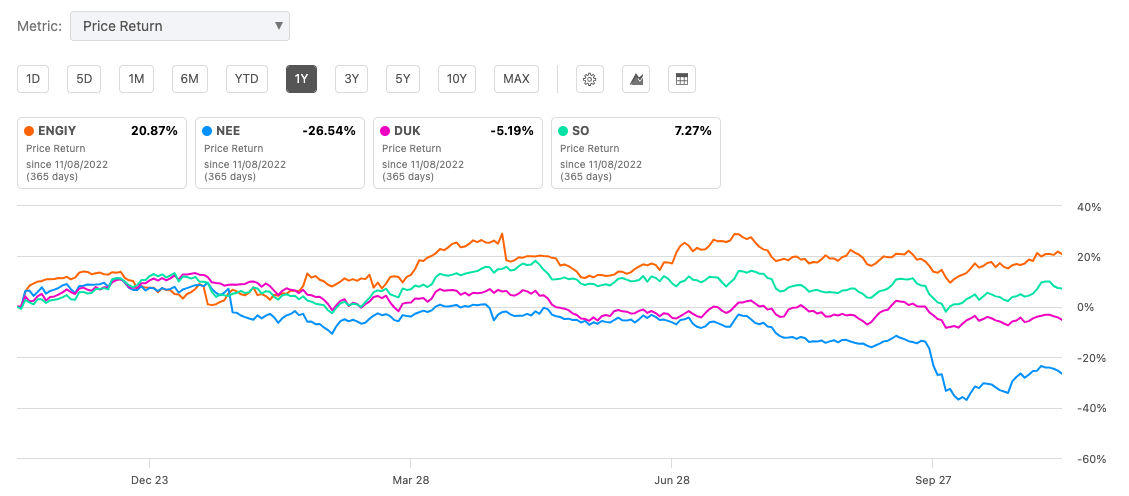

Over the past year, I have been monitoring the performance of Engie's stock and found that it has outperformed the US utility firms in terms of price return, with a return of 20.87%. In contrast, the US utility firms have produced negative returns or, at best, single-digit returns, with Southern Company having a return of just 7.27%.

{kind=link}

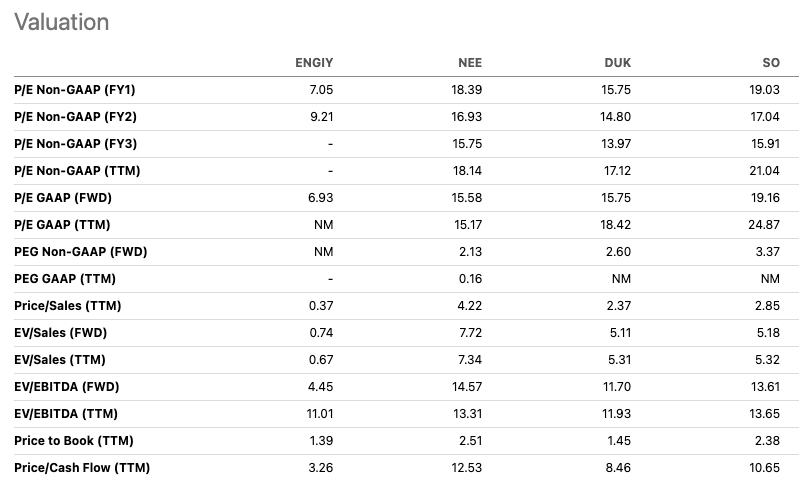

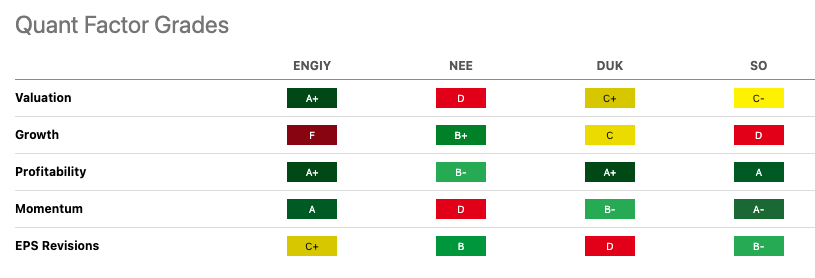

If we look at the FWD price to earnings of Engie versus its peers, we can see that the stock looks undervalued at 6.93 compared to the American utility companies, which have ratios in the higher teens. Seeking Alpha's Quant rating system valuation further strengthens the case of its desirability if we look at its A+ valuation and compare this to NextEra Energy ( NEE ) with a valuation of D, a C+ for Duke Energy ( DUK ) and a rating of C- for Southern Company ( SO ).

{kind=link}

{kind=link}

Growth versus peers

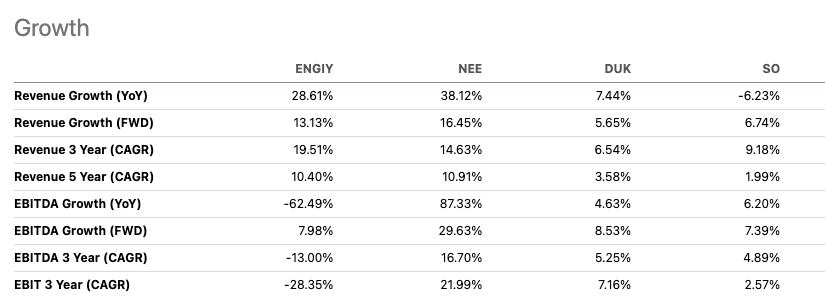

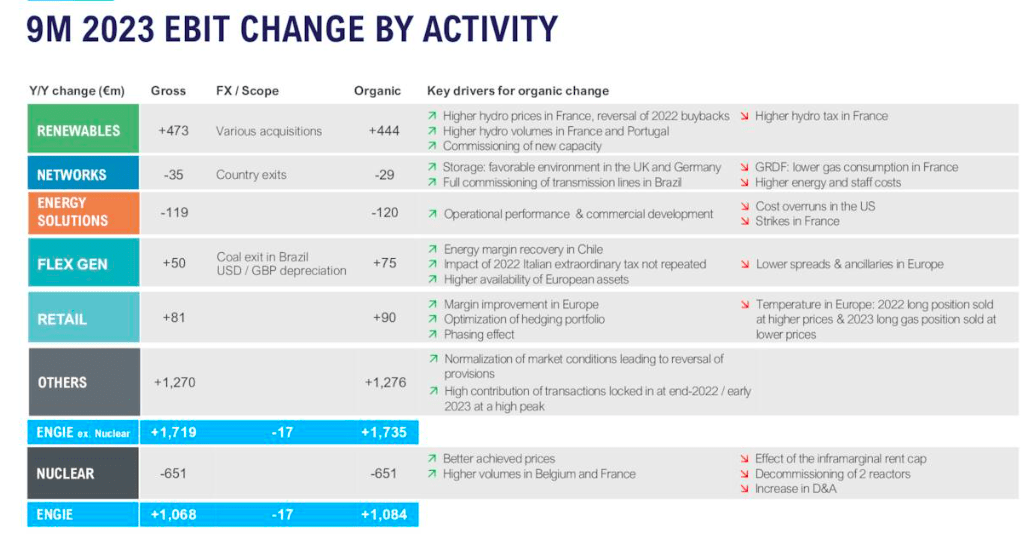

Engie's growth factor has an F grade rating, which might seem concerning. However, the company has shown impressive YoY revenue growth of 28.61%. Only NextEra Energy has a higher growth rate at 38.12%. Additionally, the company has experienced a 12% growth in revenue, excluding nuclear, for the first nine months of 2023, reaching €11.9 billion. With nuclear back in the picture, we can expect significant growth in both top-line and bottom-line results.

{kind=link}

{kind=link}

Balance sheet versus peers

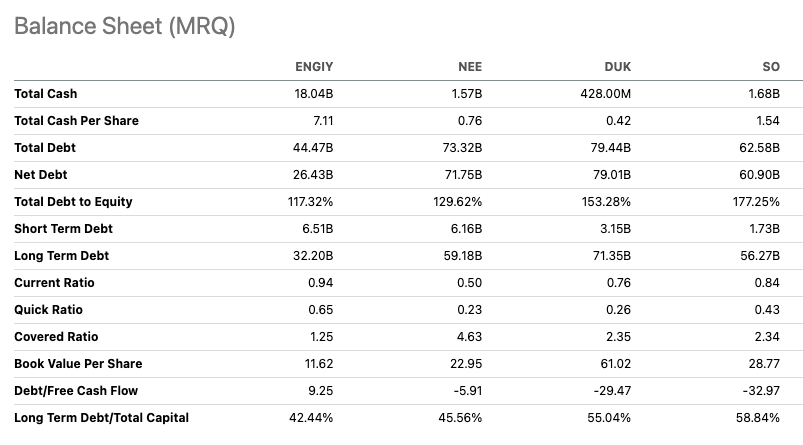

The company has set ambitious goals for growth and investment. However, it is crucial to examine its cash position to determine whether it can successfully fund these plans. In comparison to its peers, Engie appears to have a relatively healthy balance sheet, with $18.04 billion in cash. Although the current ratio has decreased from 1.1 to 0.94 since my previous article, it is still higher than its peers.

{kind=link}

Risks

Engie is a global energy company heavily influenced by geopolitical factors, such as regulatory changes and political events. For instance, in the French market, the company is impacted by higher hydro taxes . Moreover, higher temperatures have delayed the winter gas demand in Europe, which has resulted in a drop in gas prices. Initially, EU regulations were aiming to phase out nuclear energy, which could have weakened Engie's financial position. Future regulatory changes, such as the EU government's effort to decrease energy bills, will continue to significantly affect the company's operations, with the potential for negative consequences.

Final thoughts

Engie has reported strong earnings for Q3 of 2023, which has led to an increase in its FY 2023 forecast. The company has also made exciting moves in the renewable energy space, including the acquisition of a major battery company located in the US. With reinstated nuclear contracts and ambitious global growth plans, Engie is expected to experience long-term growth. Additionally, the company is making investments while maintaining a healthy balance sheet and appears more attractive than its US-based utility peers. Therefore, I maintain a bullish stance on this stock.

For further details see:

Engie: Strong Q3 2023 Results Improve Full-Year Guidance