E - Eni: 3 Reasons Why This Stock Is A Strong Buy

2023-04-09 05:03:08 ET

Summary

- OPEC decision to cut production will boost Eni’s profits.

- Eni’s management policy seems to be very effective.

- The company is really cheap, with a potential upside of nearly +50%.

Eni S.p.A. (E), the Italian oil and natural gas production giant, after a year of record profits, is poised to outperform the market thanks to a mix of good management choices, tailwinds from the recent OPEC+ decisions, and the good positioning in the oil market. Below I explain in the three points why, in my opinion, Eni is a Strong Buy idea for 2023.

1. OPEC+ is doing Eni's profits a favor

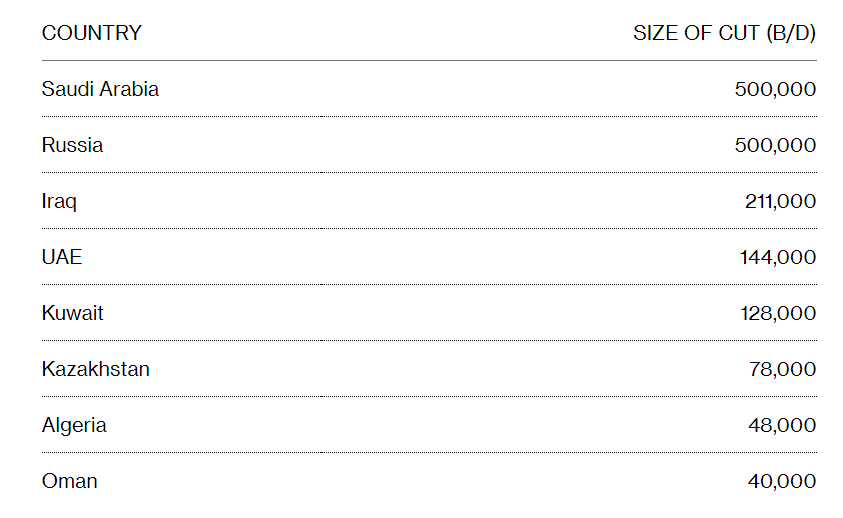

As many have heard, there was a real earthquake in the crude oil market on Sunday April 3rd following OPEC+'s decision to cut production. Saudi Arabia, followed by Iraq, the UAE, and Kuwait, has decided to cut production by 1.1 million barrels per day, which corresponds to 1.1% of global supply. When combined with Russia's 500,000 barrel cut, the result is an extremely tight market and skyrocketing prices.

{kind=link}

OPEC production cut (Bloomberg)

Analysts at major banks revised their crude oil price targets upwards, expecting on average a possible increase of between $20 and $25 from current levels.

Top oil analysts issued calls for $100 crude after the decision, with some expecting worldwide supply-demand balances to be in deficit earlier than expected. That view was reflected in the strengthening of Brent's backwardation — where the premium of prompt shipments rises relative to later supplies in a closely watched signal of tightness.

(Source: Bloomberg )

Goldman Sachs also raised its Brent oil forecast:

This, combined with the extension of the Russian production cuts, led the Wall Street giant (Goldman Sachs) to raise its Brent oil forecast to $95 a barrel for December this year from $90 earlier, and to $100 for December 2024 from $95.

(Source: Bloomberg )

But how can this benefit Eni?

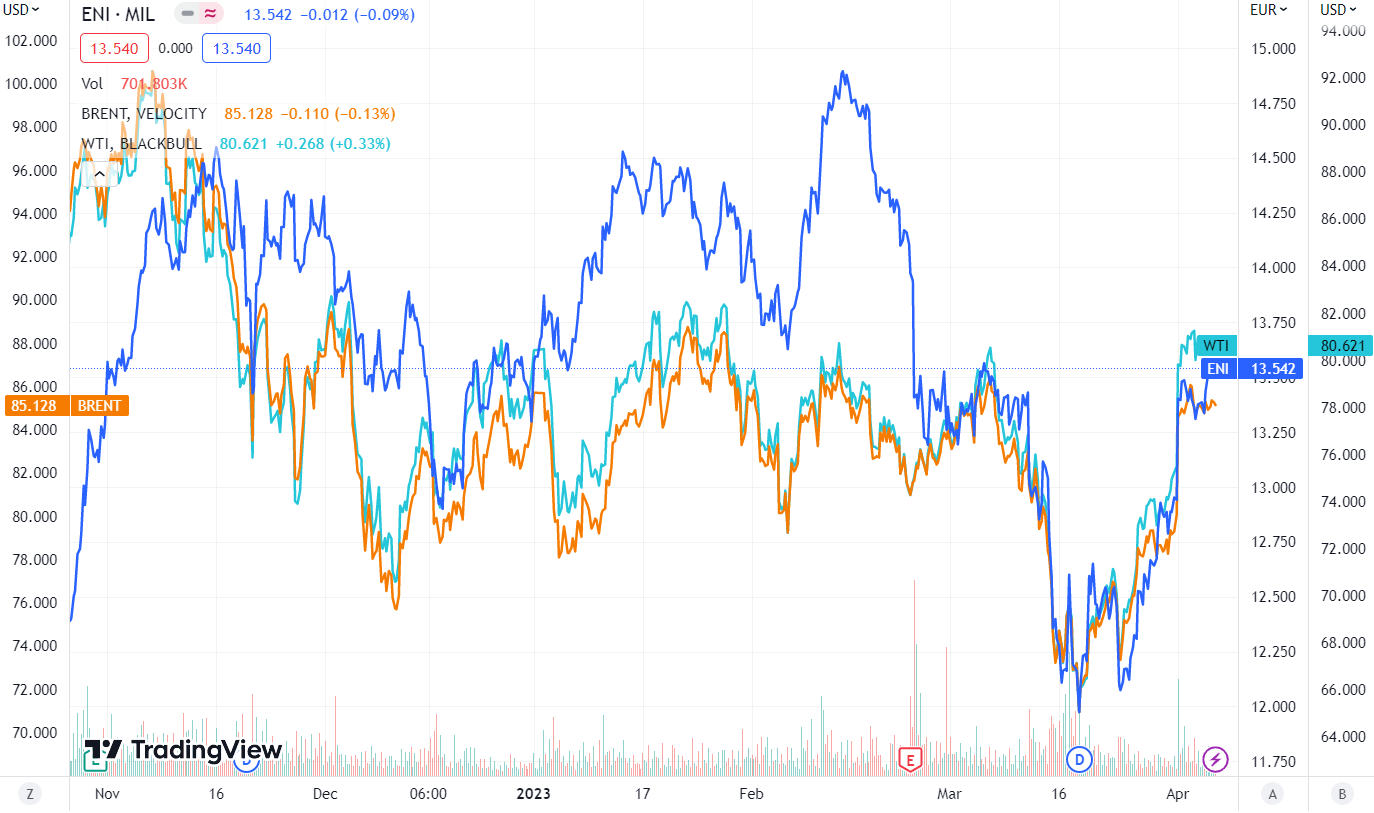

Looking at the charts, it can be seen that Eni has remained closely linked to changes in the price of crude oil. Therefore, a rise in oil prices following a lack of supply due to OPEC+ cuts will certainly lead Eni, which is the leader in the sector in Italy and Europe, to outperform while remaining in line with the rise we are experiencing at the moment.

{kind=link}

Eni correlation with crude oil price - 1Y ( TradingView)

{kind=link}

Eni correlation with crude oil price - 6m ( TradingView )

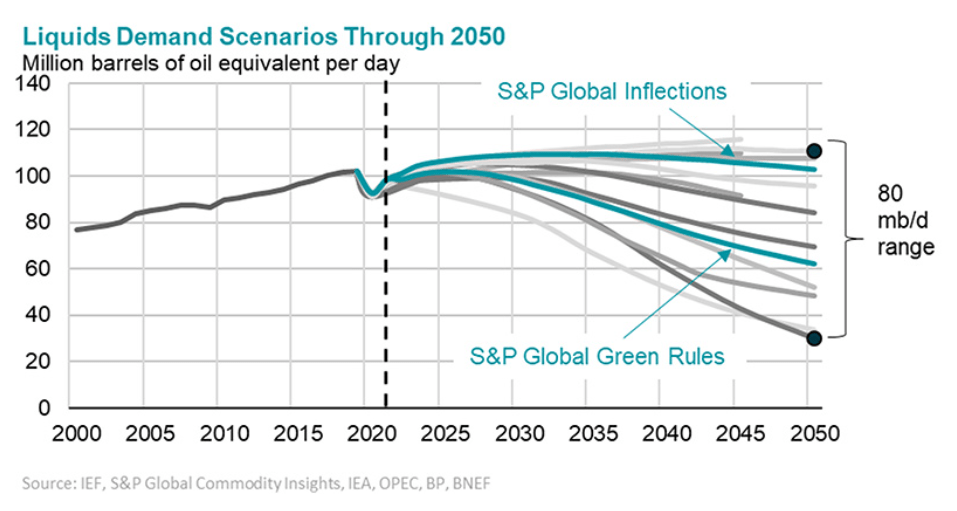

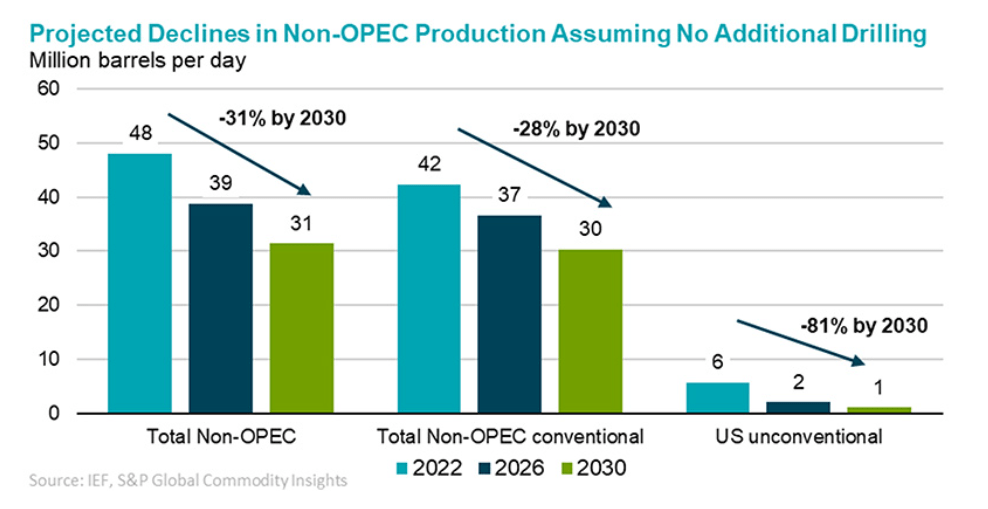

However, this movement that could lead oil price to around $100 can be placed in a much broader context. Due to the green policies adopted both in Europe and the United States, we have seen a decrease in investments in the oil sector and therefore a rigid supply in the short term.

{kind=link}

Crude oil aggregate demand forecast (International Energy Forum (IEF))

{kind=link}

Non-OPEC production forecast (International Energy Forum (IEF))

From the two graphs , it can be seen that despite the expected global aggregate demand of around 110 million bpd until 2040 (S&P Global inflections), the estimated production in the non-OPEC countries is in sharp contrast, with an estimated reduction of 31% by 2030. This imbalance will lead to a higher oil price both in the short and long term and will certainly benefit Eni’s profits.

2. Eni’s management is doing a great job

Another reason why I am bullish on Eni regards its management and the policies they have been adopting, which have proven to be very effective in the last few years.

For example, Eni's recent announcement to acquire the remaining 64% of Novamont , a leading international company in the field of renewable chemistry and bioplastics, through its subsidiary Versalis (which already owns 36% in Novamont) is a noteworthy move. Novamont has a revenue of €414 million and around 1,400 patents and patent applications, and the acquisition aims to consolidate Eni's position on the international market by absorbing the company's know-how.

The operation is in the final stages of negotiations with Mater-Bi (which belongs to Investitori Associati II and NB Renaissance), and the acquisition should be announced in the coming weeks.

What I find very interesting about Eni is the green policy that the company has been adopting for some time now, which is starting to bear fruit. The acquisition of Novamont, together with its green branch Plenitude, is an example.

In fact, this is what we read on the page dedicated to Eni's investors :

Eni's 2021 ratings place or confirm the company in a leading position both in the main ESG ratings and specialized indices: MSCI (confirmed as “A”), Sustainalytics (confirmed as “medium risk”), Moody's ESG Solutions (first in its industrial ranking and confirmed in “advanced band”), FTSE4Good Developed Index (confirmed for the sixteenth consecutive year). In 2021, Eni's ISS ESG rating has been upgraded to Prime Status.

(Source: Eni)

Eni has been ranked highly for its Environmental, Social and Governance activities ESG and is in all the main ESG indices.

(Source: Eni)

This is noteworthy, as Eni can continue to carry on its core activities while benefiting from the enormous inflows of capital that ESG funds have had in recent years.

Another smart move by Eni's management is their confirmation of the IPO of Plenitude . By detaching the green branch of operations and its debt, Eni will bring value to investors in the long run.

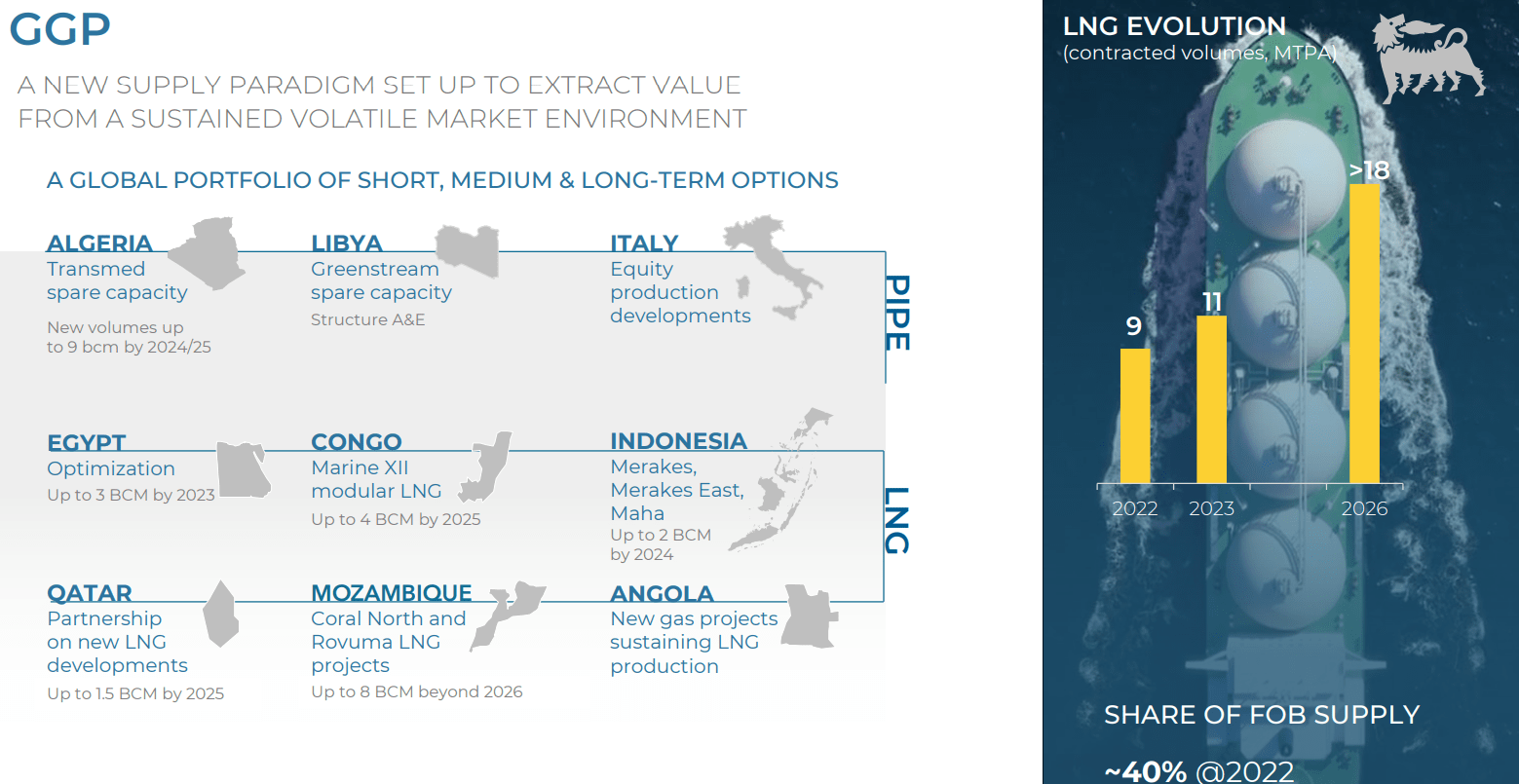

Moreover, I was also impressed by Eni's management ability to deal with the problems caused by the war in Ukraine. The company quickly shifted the production of more than 50% of the natural gas from Russia thanks to its relations with Qatar, Algeria, and Egypt .

{kind=link}

Eni LNG production (Eni Investors Presentation)

In conclusion, there are many other noteworthy points that could be listed, such as the buyback plan starting in May 2023, raising the dividend by 7% this year, or the discovery of the new gas field off the coast of Cyprus (Cronos-1 ) thanks to Eni's enormous investment in technology for the geological and geophysical study of the seabed ( see the green HPC5 supercomputer ). However, the main point remains the same: Eni's management has always made the right choices for its business and has brought value to investors in the last 5 years, making it clear how much Eni is an avant-garde company and therefore a good investment from a fundamental point of view.

3. The stock is a deep-value opportunity

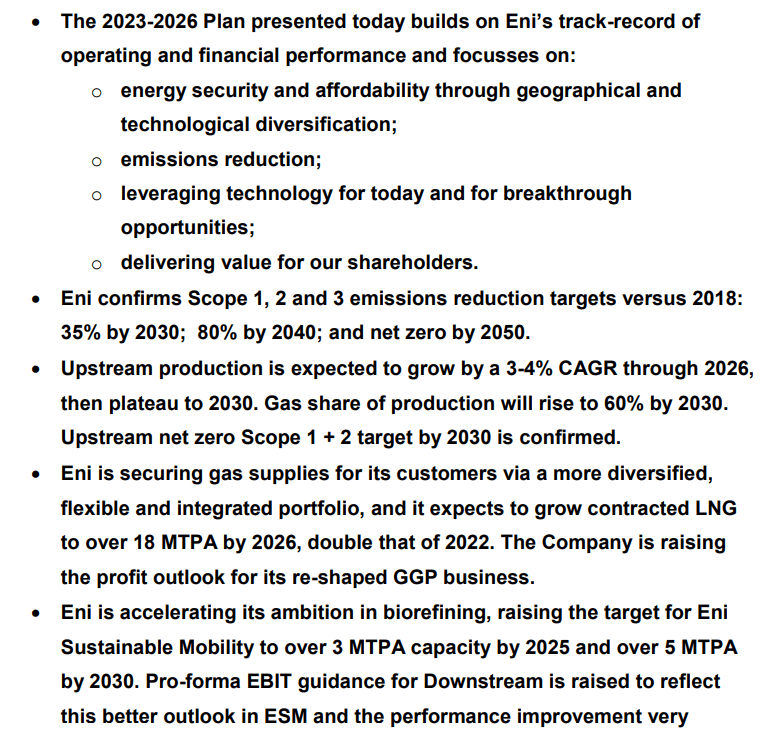

Finally, the last reason for my bullishness on Eni is its valuation. To value the company, I used a discounted cash flow model and I relied heavily on the company's Strategic Plan 2023-2026 for my assumptions. Specifically, I modeled the CAPEX with a 15% upside, as written by the company. Additionally, I assumed a Cash Flow From Operations before Working Capital of €17 billion in 2023 and €69 billion in total for the three-year plan. I also provide below a summary and a link to Eni's Strategic plan 2023-2026 for those who want to explore the details further.

{kind=link}

Eni's Strategic plan 2023-2026 (1/2) (Eni IR)

{kind=link}

Eni's Strategic plan 2023-2026 (2/2) (Eni IR)

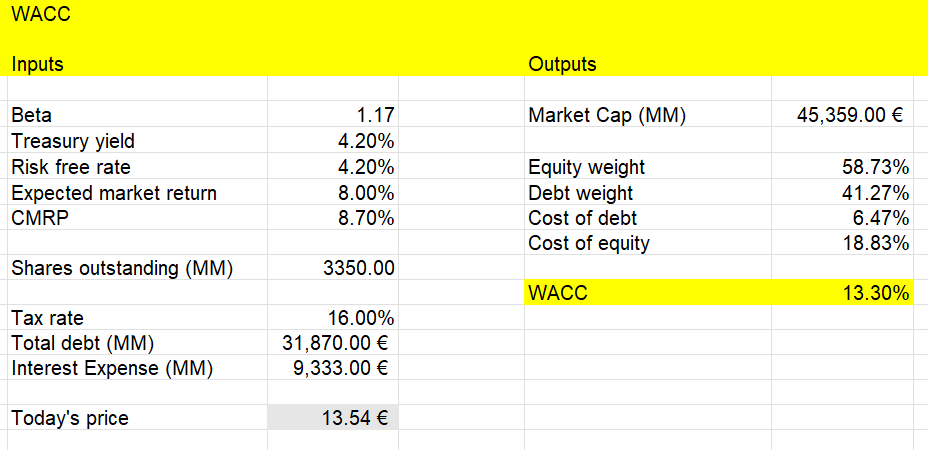

Regarding the calculation of the WACC, I made some assumptions. For the risk-free rate, I used the yield of Italy's 10-year bond. For the Country Market Risk Premium, I took a weighted average that included the countries where Eni operates, which gave me a value of 8.70%.

{kind=link}

WACC calculations (Excel DCF Model)

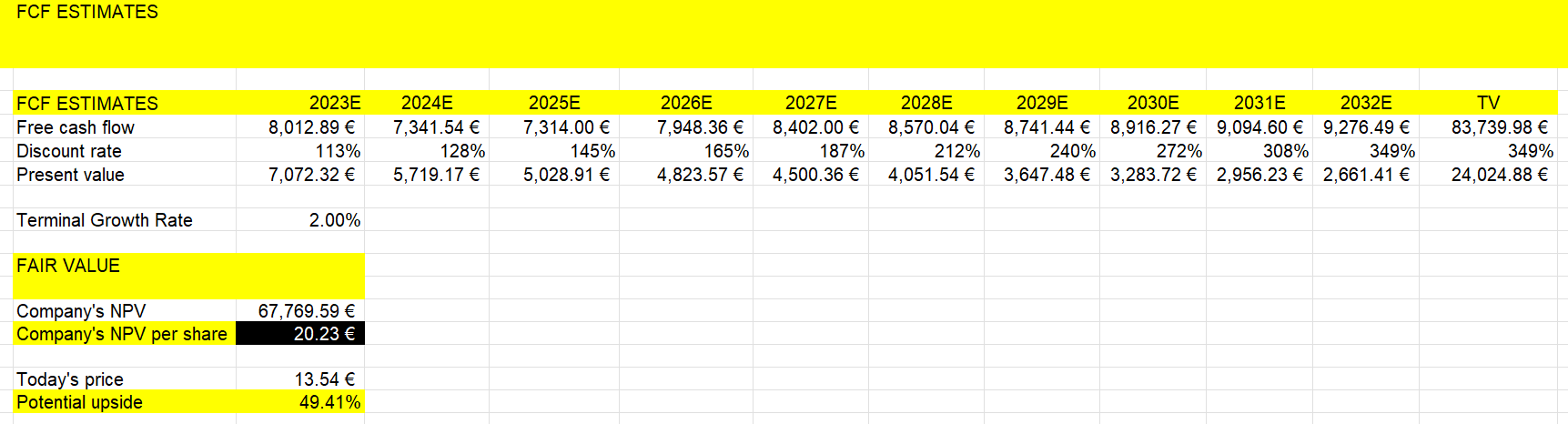

Using the obtained WACC of 13.30% and a terminal growth rate of 2.00% (as I expect a lower growth rate than the GDP in the long term due to green policies), I obtained a Fair Value of €20.23 (for NYSE:E the fair value is $44.22). This indicates that Eni has a potential upside of 49.41%.

{kind=link}

FCF Final Table (Excel DCF Model)

Bottom line

In conclusion, thanks to the combination of all these elements, I am very bullish on Eni stock. The recent OPEC+ statements will be an excellent boost for the company's profits. Additionally, with a Trailing Annual Dividend Yield of 6.55%, the company can be a strong buy not only from a value investing perspective, but also for more dividend-oriented investors.

For further details see:

Eni: 3 Reasons Why This Stock Is A Strong Buy