E - Eni: Cash Flow Growth And Shareholder Distributions Driving Double-Digit Returns

2023-09-15 17:32:30 ET

Summary

- Eni offers strong earnings and cash flow growth, supported by exploration success and capabilities in gas and LNG.

- The company has a strong portfolio of projects that will drive production growth and profitability.

- We believe Eni offers double-digit total shareholder returns over the mid-term and we recommend buying Eni shares.

We present our note on Eni ( E ), an international oil major, with a Buy rating. We believe Eni offers attractive embedded returns, driven by strong earnings and cash flow growth, underpinned by exploration success and capabilities in gas and LNG. We will provide a brief overview of the company, analyze the key drivers of our thesis, review the acquisition of Neptune Energy, and value Eni’s shares.

Introduction to Eni

Eni is an Italian multinational energy company engaged in the whole value chain from exploration, development, extraction, refining, and marketing of oil and gas, to the generation of electricity and circular economy processes development. Eni’s upstream operations are mainly located in Italy, Norway, the UK, Nigeria, Angola, Libya, and Mexico, while downstream operations are concentrated in Europe. Eni is one of the largest companies by revenue and equity value in Italy, and it is listed on the Milan Stock Exchange and the NYSE with a present market capitalization of €51 billion.

Improving portfolio driven by exploration success

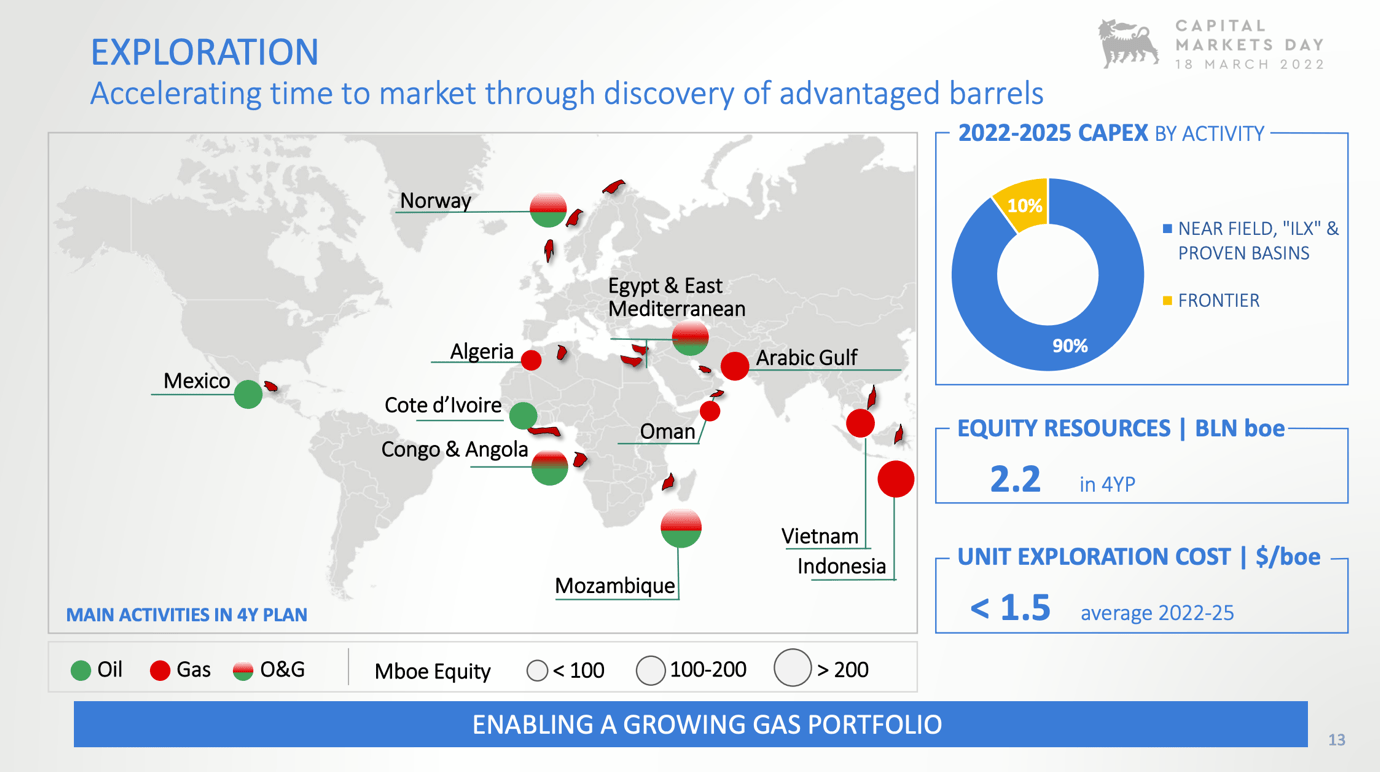

Similar to Shell, discussed in our previous note , Eni has an improved project portfolio with attractive embedded IRRs and higher-than-peers structural profitability, driven by exploration success and superior project delivery. Eni’s projects will drive a 3-4% CAGR in Upstream through 2026, arriving at ~ 1.80-1.88 Mboed, and effectively pushing the production plateau to the year 2030. The payback periods of the new projects are around five years and breakeven prices are close to $20/bbl. Key projects include Johan Castberg and Balder X in Norway, Agogo West Hub in Angola, A&E Structure in Libya, and Baleine in Ivory Coast.

Significant value creation has been achieved thanks to successful explorations, outperforming peers, and leading to major discoveries such as Baleine, Mexico Area 1 , Agulha in Mozambique, and Zohr in Egypt. Eni’s explorations in the last decade roughly amount to 35% of its current enterprise value.

{kind=link}

Strength in gas and LNG

Eni expects to fully replace Russian gas volumes by 2025. It has signed new supply agreements with Qatar, Algeria, Mozambique, and Egypt aiming to deliver more than 18 MTA by 2026. In addition, liquefaction volumes will grow by 10% CAGR through 2026 to 10MTA. Gas’s segmental EBIT should more than double by 2026 arriving at ~ €4+ billion. Robust performance in GGP has also been demonstrated in Q2 2023, with a record quarterly EBIT coming in at more than double sell-side consensus estimates, as a result of trading results and contractual triggers. As highlighted by Eni’s CEO in the Q2 call, Eni’s GGP model is more integrated into the gas value chain and is benefiting from recurring arbitrage and trading opportunities. It is superior to the previous wholesale pass-through model and results in higher profitability.

Navigating the green transition

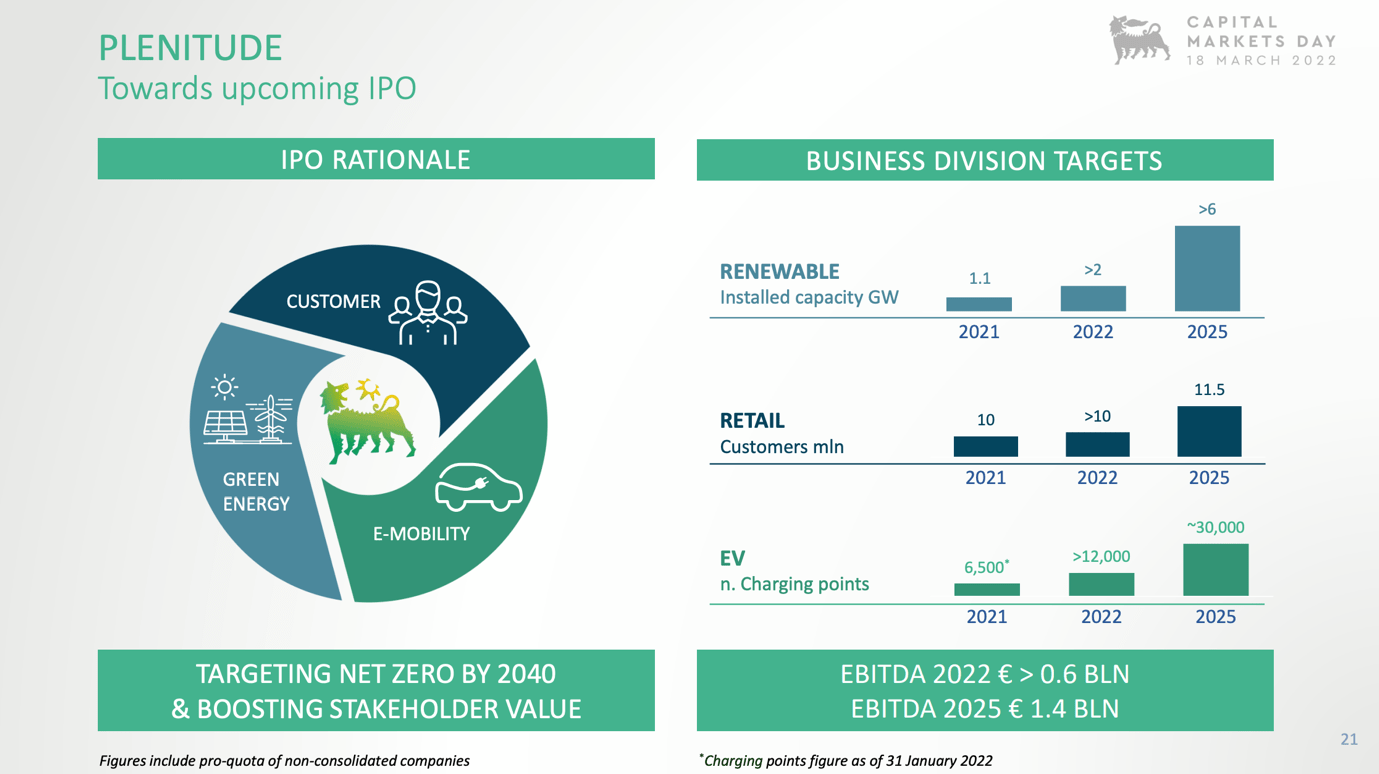

Plenitude includes renewable energy assets, energy services, EV charging, and retail. Eni expects its renewables capacity to double to more than 6GW by 2025 and grow to more than 15GW by 2030. The company’s unlevered IRR target is 6-8%, with additional upside coming from financing. Moreover, Eni expects 15 million customers and up to 35k EV charging points by 2030. Divisional EBITDA should triple by 2026 to €1.8 billion. In addition, we would like to highlight Eni’s 20% stake in CFS, a start-up in fusion energy. We view this as an attractive option value. While we are generally cautious of oil majors’ heavy investments in renewables, we believe Eni is navigating the green transition well so far.

{kind=link}

Q2 Results

Following a strong Q1 beat, Eni reported Q2 numbers above consensus expectations with the beat being driven by performance in GGP (gas and LNG). Group EBIT guidance for the fiscal year has risen by €1 billion to ~ €12 billion, largely driven by GGP divisional guidance upgrade – half from trading and arbitrage opportunities and half from contractual triggers. Production guidance remains the same, and capex guidance has been lowered by €200 million to €9 billion. Moreover, on the call management pointed out there is upside to the 2024-26e GGP EBIT guidance of €700 million. We believe the latter could reset higher by at least 20%. We are encouraged by the Q2 print and believe it further substantiates our thesis.

Neptune Deal

Eni has announced the acquisition of Neptune Energy, one of Europe’s largest independent exploration and production companies, in a three-step transaction. Eni will acquire Neptune’s ex-Germany ex-Norway assets with ~250mboe 2P reserves and a daily production of 63k boe for a cash consideration of ~ $2.6 billion. Meanwhile, Var Energi, Eni’s listed subsidiary will acquire Neptune’s Norwegian assets for $2.3 billion. The deal is expected to close in Q1 2024. Eni estimates $500 million of synergies on an NPV basis and $1 billion of value creation on an NPV basis. The group, under its strategic plan, has announced net divestments of $1 billion, leaving room for $4.5 billion of divestments coming until 2026 including the sale of a minority stake in Plenitude and non-core E&P assets. We have a positive view of the deal.

Investment case, valuation, and capital returns

As with other names in the sector, we value Eni using PE multiples and FCF yields. Our mid- and long-term commodity price assumptions have been set forth in our Shell note. We forecast mid and long-term Brent prices at $60-$70/bbl. and natural gas prices at $11-$14/mcf. Our financial forecasts are sensitive to commodity price assumptions and strategists have a wide array of predictions. We remain rather conservative despite current tailwinds.

We forecast €80 billion of sales and €19.5 billion of EBITDA in FY2024e. We then forecast a net profit of €7.8 billion and Free Cash Flow of €6.0 billion, implying a forward PE ratio of 6.6x and an FCF/EV yield of 9.5%. At current prices the valuation metrics are significantly lower: i.e. at $90/bbl. the FCF/EV yield stands at ~ 17%. We forecast around €4 billion of shareholder distributions, i.e. 27.5% (midpoint of guidance) of CFFO, implying nearly 8% of Eni’s current market capitalization will be distributed to shareholders in FY2024.

Eni is trading at more than 40% discount to its 20-year historical multiple and below most European oil and gas peers despite stronger fundamentals. Given Eni’s well-balanced portfolio, cash flow growth, and discount to peers and historicals we believe the stock is undervalued. We conservatively value Eni at 8x forward earnings implying 21% upside. Combined with high single-digit/low double-digit shareholder distribution we forecast a mid-term IRR in the high teens.

Risks

Downside risks include but are not limited to deteriorating macroeconomic conditions, lower oil prices resulting in lower earnings, lower gas and LNG prices resulting in lower earnings, lower than expected production volumes, higher than expected capex in new developments leading to declining returns, delays and unexpected challenges in project execution, suboptimal allocation of capital e.g., to low return renewables projects, lower than expected shareholder distributions, new windfall taxes reducing earnings, energy transition and climate change risks, geopolitical risk, natural disasters, accidents, etc.

Conclusion

Given the appealing valuation and capital returns, underpinned by solid fundamentals, we believe Eni offers double-digit total shareholder returns over the mid-term and we recommend buying Eni shares.

For further details see:

Eni: Cash Flow Growth And Shareholder Distributions Driving Double-Digit Returns