E - Eni Is A Buy Ahead Of Q3

2023-10-13 05:21:19 ET

Summary

- Eni plays a vital role in the Mediterranean Eastern region but has no direct implication with the Israel/Hamas conflict.

- A potential Iran involvement with a possible Middle East escalation might result in higher for longer oil prices.

- Eni has a solid balance sheet with a supportive FCF yield. The company also closed the gap with peers, paying the dividend on a quarterly basis.

- The company trades at a low P/E despite a solid oil and gas portfolio. Our buy rating is then confirmed.

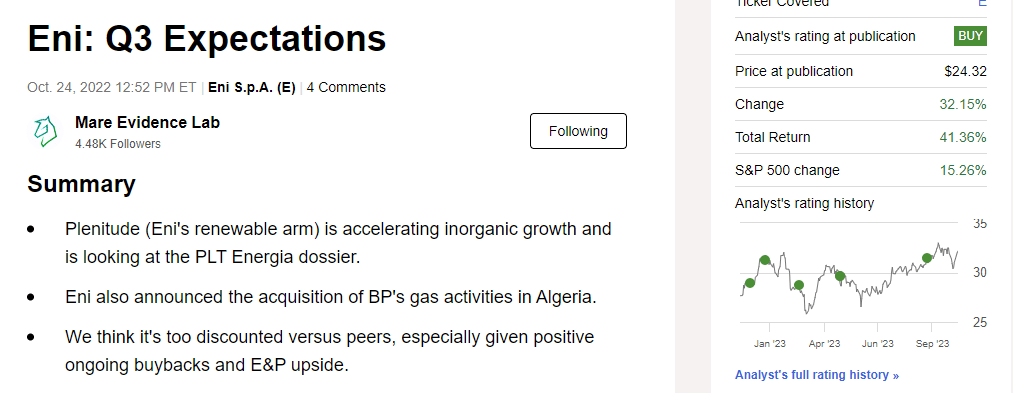

Our readers know that we have long waited to revert our rating target with Eni (E), and last year, with a publication called ' Q3 Expectation ,' we increased our target price and moved the rating to an overweight. This was a good call in a supportive momentum, and one year later, after a > 40% total return, we believe that Eni is still a buy.

{kind=link}

Eni Implication and Israel Update

In the global energy galaxy, Israel occupies a marginal role. However, there are hydrocarbon reserves in the region, and Eni plays an essential role in the Mediterranean Eastern area. Leviathan, Karish, and Tamar are important gas hubs and might be exposed to the war evolution. Tamar offshore field exports gas to Jordan and Egypt for domestic gas consumption and is now closed . At the same time, the Laviathan field remains under special surveillance and continues to operate . Impressive as its name suggests, it is credited with reserves estimated at around 605 billion m3 of gas. In light of the geopolitical implications and based on the duration of the new conflict, the entire plan of transforming the Mediterranean Easter region from a gas-producing province to a natural gas hub could prove to be at risk. Eni exploratory campaigns in Cyprus and Lebanon and the Zohr giant field in Egypt now have an additional potential risk.

This new conflict between Hamas and Israel has not directly impacted oil flows and supply. Although there has been no direct impact, Wall Street is on high-risk alert as the crisis evolves. A significant Middle East escalation, with a potential Iran involvement , a major oil producer and supporter of Hamas, could produce a further stagflation shock on the global economy. These effects could further slow economic growth and, at the same time, keep oil prices higher for longer.

At Q4 numbers, we expect rising profits for big oil companies and might see an upward revision of buybacks and higher special distribution to shareholders. Here at Lab, we believe Wall Street might return to be price-positive on earnings revisions within the sector, and we won't be surprised to see Brent oil over $90 a barrel in the last quarter of the year.

Looking at Eni, there are four catalysts in the next 12 months to price in. First, the company has a strong balance sheet, allowing greater flexibility in rewarding shareholders. Second, here at the Lab, we highlight that Eni has a resilient free cash flow and a continued discipline allocation at the capital level. In our numbers, we anticipate a minimum free cash flow yield of 15% in 2024, which is well above historical averages. Third, as mentioned, we should highlight the last decade of oil underinvestment and supply shortages. Eni has an underpriced oil and gas portfolio in a sector lacking production growth. In addition, Eni has this ' Dual exploration model ,' which involves the sale of a minority oil & gas exploration, immediately monetizing the entire production value. Fourth, there is a substantial earnings dispersion among oil analysts' expectations. Considering oil and gas prices evolution, this might suggest a capital potential upside.

Q3 Forecast with an Updated Valuation

Looking ahead (once again), the Italian energy group will release its third-quarter accounts on the 27th of October . Here at the Lab, we expect a yearly improvement in the adjusted core operating profit and Eni's CFFO (cash flows from operations) targets. However, in Q3, we anticipate lower profits by 15.5% on a sequential basis due to Brent prices and lower chemical margins. We expect a sequentially improving result for E&P (Exploration and Production), Sustainable Mobility, and Refining. Regarding cash flow, our Q3 adjusted CFFO expectation is around €3.2 billion with CAPEX of €2.2 billion and stable leverage due to the supportive quarterly cash generation. We also included the shareholders' remuneration in our estimates: dividend (€0.8 billion) and buyback (€0.6 billion). As a recap, here are our estimates:

- E&P production: 1,630 million barrels of crude oil per day with a +3% year-on-year and a plus 1% quarter-on-quarter (This is also in line with the company's guidance);

- Adjusted Core Operating Profit at €2.83 billion, signing a minus -50.5% on a yearly basis and -15.5% on a quarterly basis;

- Adjusted net income at €1.55 billion with an adjusted CFFO of 3.2 billion, signing a minus -41% and 24% year-on-year and quarter-on-quarter, respectively.

Despite that, we confirm the 2023 earnings per share estimate of around €2.50, and we believe that Eni can improve its 2023 targets since they appear to be somewhat conservative. In our estimates, we arrive at an EBIT of €14 billion with an adjusted CFFO of €16.5 billion. Here at the Lab, we also remain positive on the 2024 estimates (with an average Brent price of 80 dollars). Cross-checking our estimates, Eni trades at an EV/EBITDA ratio of 3x with a P/E lower than 4x (excluding a potential Plentiture IPO) and a dividend yield at current prices of 6.5%. According to our estimates, Eni trades at a valuation gap that cannot be justified. Considering the recent buyback and the new quarterly dividend policy (in line with peers), Oil Investors Should Look At Eni (again). In our estimates, valuing the company with a P/E in line with peers at a 2024 P/E of 7x, we decided to increase our valuation from €16 to €17.5 per share ($37 in ADR).

For further details see:

Eni Is A Buy Ahead Of Q3