E - Eni: Oil Major Opportunity Trading At 12% Shareholders Yield 2x Cash Flow

2023-03-30 04:34:31 ET

Summary

- Eni delivered stellar results in 2022 and generated more than €20.4 billion cash from operations, a 111% year-on-year increase.

- With a bullish medium-term outlook for oil prices, Eni set in its strategic plan to deliver another €69 billion CFFO over the next four years, 150% the current market cap.

- Eni will have the financial strength to pursue an aggressive CAPEX plan and continue its generous shareholders' remuneration, without having to choose between the two.

[Note: article’s financial values will be mostly presented in EUR, and stock, market cap references will be made in relation to Eni’s main listing on the Milan Stock Exchange, rather than the NYSE ADR listing]

In 2023, Brent oil ( CO1:COM ) and gas ( TTF Amsterdam ) prices have weakened. Brent has mostly struggled between $80 and $85 before dropping further towards $70 in recent weeks. The reference price for gas has halved in just three months, from around €80 MWh at the beginning of the year to around €40 MWh currently. Despite the difficult market backdrop, I maintain a bullish outlook for oil prices in the long term, as I believe prices have been influenced by seasonal weakness and market turmoil. Supply has been constrained by a decade of underinvestment, and global demand is expected to continue growing moderately. With this in mind, Eni S.p.A. ( E ), the largest energy player in Italy, is one of my top ideas for 2023. The company operates a highly profitable upstream business, has ambitious investment plans of about $40 billion over the next four years (against a $47 billion market cap), and offers a shareholder yield of >10% in a mix of dividends and buybacks. Eni shares trade at a slight discount to already cheap European peers. At current levels, I rate Eni shares as a strong buy with 100% upside potential to fair value.

Eni at a glance

Eni, founded in 1953 as Ente Nazionale Idrocarburi (National Hydrocarbons Authority), is based in Rome, Italy. Although the name is no longer relevant as an acronym, it reflects that, up until its conversion into a joint-stock company and listing in 1992, Eni was a government-owned economic entity. Eni operates as an integrated energy company with four main segments:

- Oil upstream (E&P) with operations scattered across Africa, the Middle East, the North Sea, and South America.

- Global gas & LNG portfolio ((GGP)) involved in upstream and midstream operations and currently focused on replacing Russian flows.

- Refining and marketing (R&M) which includes Eni's significant downstream presence in Italy with four traditional refineries, two biofuels refineries, and operates the largest network of retail gas stations (about 4,700). Eni also owns a 20% equity interest in ADNOC Refining, purchased in 2019 for €3.3 billion. The Ruwais refining complex operated by ADNOC has a total refining capacity in excess of 900 thousand barrels per day, making it the 4 th largest globally.

- Renewables (Plenitude). In recent years, the company has significantly invested in renewable energy production and distribution. Its green operations, rebranded in 2021 as "Plenitude" ahead of a planned IPO, generated approximately €0.7 billion EBITDA last year, with plans to grow generation capacity from 2.2 GW in 2022 to over 7 GW by 2026 and over 15 GW by 2030.

2022 results highlights

Eni, along with its bigger European peers Shell ( SHEL ), BP ( BP ), and TotalEnergies ( TTE ), delivered stellar results in 2022 . Despite a slight decrease in production from 1.68M BOE/d in 2021 to 1.61M BOE/d in 2022, Eni expects to ramp up production at a CAGR of 3%-4% over the next few years. The company generated more than €20.4 billion in operating profit, a 111% YoY increase. Net profit increased by 237%, from €5.82 billion in 2021 to €13.81 billion in 2022, and EPS followed suit, increasing from €1.6 per share to €3.93 per share. For reference, Eni's ADR listing on the NYSE represents two ordinary shares, and the company currently trades at around €12.7 on the Milan Stock Exchange, resulting in a 3.2x TTM P/E.

Eni carried out a €2.4 billion share repurchase program from June through December 2022, repurchasing 195.5 million shares (5.5% of the total capital). It is important to note that repurchased shares are not automatically canceled but are held by the company in the form of treasury shares. With the newly repurchased shares added to the 31 million already held, Eni now holds approximately 226 million shares, or 6.4% of its own total capital in the form of treasury shares. In addition, €3.0 billion were distributed to shareholders via dividends, resulting in a total shareholder yield of €5.4 billion, a 12.2% shareholder yield against its current capitalization of €44 billion.

In addition to its outstanding financial results, Eni continued with its "satellite" strategy for subsidiaries, creating dedicated entities capable of independently accessing capital markets to fund their growth and reveal the real value of each business. While the Plenitude IPO was not finalized, Eni remains committed to proceeding with Plenitude's IPO, with the unit aiming for an EBITDA of approximately €1.8 billion by 2026, a three-fold increase from 2022. With Plenitude delivering on its 2022 and 2023 targets, proving that its growth ambitions are achievable, it is likely that the market will be in a better position to price the full potential of Plenitude and allow Eni to pocket even more cash from the IPO. Although Plenitude plans were put on hold, Eni successfully concluded the listing of Vår Energi on the Norwegian stock Exchange. Eni retains a 63% ownership of Vår Energi, and at the current share price of 25 NOK, Eni’s share of the subsidiary's value equals approximately €3.5 billion.

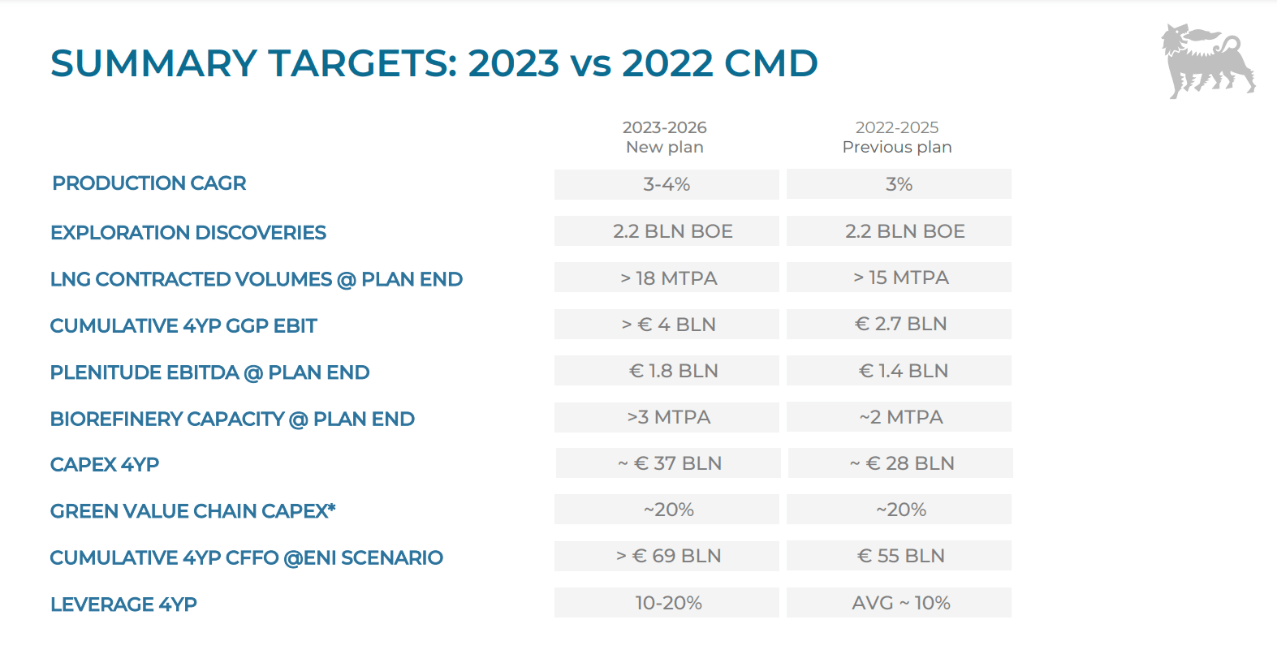

Strategic plan 2023-2026

Last month, Eni presented an ambitious 4-year plan at its capital markets day , upping the ante from the previously disclosed 2022-2025 plan. With a record amount of cash on hand, Eni decided to increase investments by €9 billion, supported by a CFFO 4Y cumulative outlook that increased from €55 billion to €69 billion. Thanks to the significant cash generation, Eni's balance sheet is already in optimal shape, with a gearing ratio of 0.13x. Despite the investments, Eni aims to maintain the gearing ratio in the current 0.1x - 0.2x range over the course of the plan and remain open to increasing shareholder distributions in the case of upside scenarios. 25% of Eni's CAPEX will be reserved for renewables generation, with plans to increase the installed to 7 GW, but upstream and refining will continue to see significant investments of €28 billion.

{kind=link}

Eni capital markets update - Strategic Plan 2023-2026

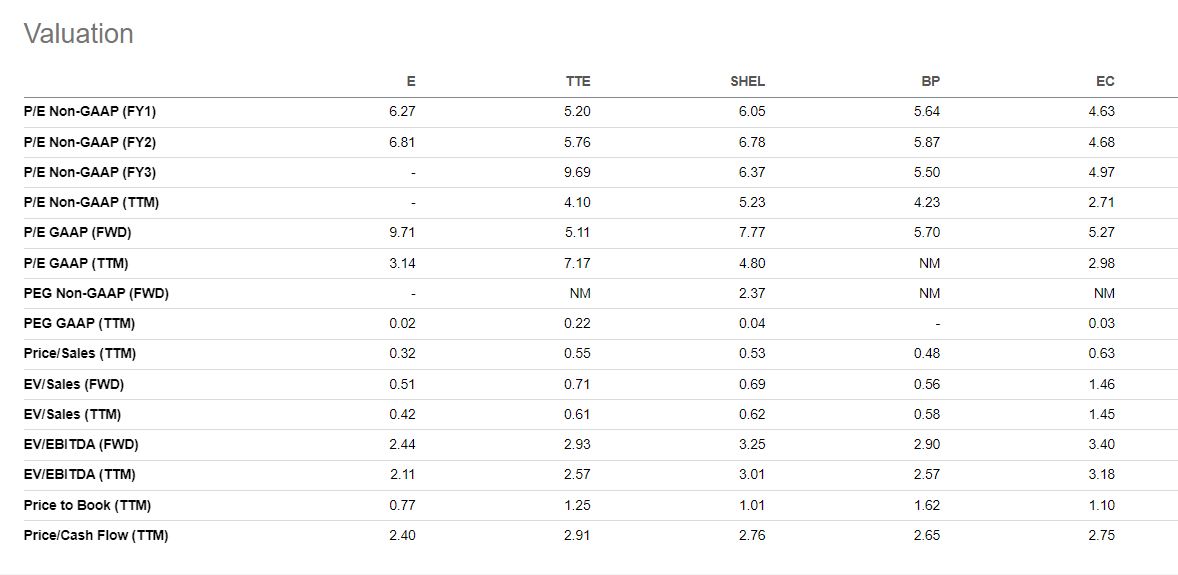

Eni’s relative valuation

I am including Shell, BP, and Total for review, as the whole group is currently trading at a steep discount to US peers. However, the relative weaker valuation has been ongoing for a long time, and despite calls by analysts that the acquisition of a EU oil company would benefit Exxon ( XOM ) or Chevron ( CVX ), I do not see this happening at this time. Furthermore, there does not seem to be a catalyst on the horizon that would help to close the valuation gap. Hence, I do not think comparison with US oil majors makes much sense. Instead, mainly out of curiosity, I have decided to include Ecopetrol ( EC ), a South American player that is arguably lower quality (junk-grade credit rating vs. A- rating for Eni) and is plagued by higher political risks.

{kind=link}

Seeking Alpha

Eni remains the cheapest company of the group on both EV/EBITDA and Price/Cash Flow basis, which I’d point out as the two most relevant metrics. Additionally, Eni has the lowest P/S ratio and is the only member of this group currently trading at a discount to the book value of its assets.

{kind=link}

Seeking Alpha

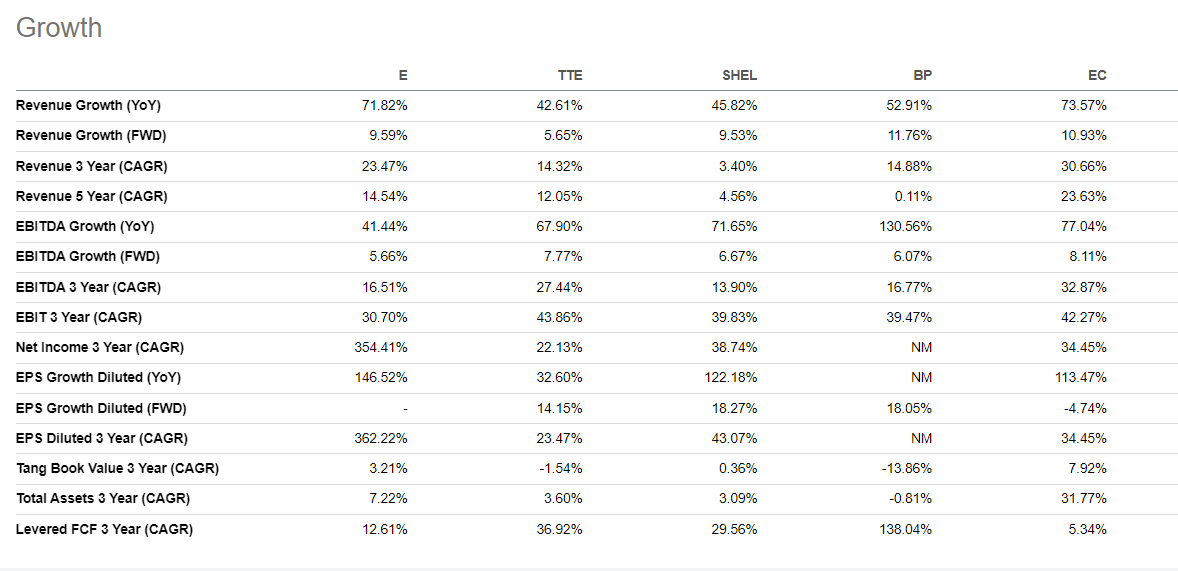

From a growth perspective, Eni registered the highest YoY revenue growth of the whole European group in 2022, matching Ecopetrol. Although EBITDA growth was not on par with peers for the year, it was similar to BP and better than SHELL on a 3-year CAGR basis. Bottom-line growth, however, was again the best of the group.

Regarding FCF growth, the trend for the whole group is basically a function of each company’s CAPEX decisions. The higher the reinvestment rate and hence the company’s total asset base growth or decrease, the lower the Free Cash Flow. I personally view it positively that Eni has the highest total assets growth over the past 3 years, indicating that Eni’s future production should hold up much better than its European peers.

Valuation

To arrive at a fair value for Eni, I am separating the E&P, GGP, and R&M segments from Plenitude. Assuming a successful IPO, Plenitude's valuation should be in line with international peers such as Clearway Energy ( CWEN ) or Atlantica Sustainable Infrastructure ( AY ), with an EV/EBITDA of 10x. Based on Plenitude's projected 2026 EBITDA of €1.8 billion, it could reach an EV of €18 billion. With Eni's leverage set at 3x-4x EBITDA, the company could absorb €6.3 billion in long-term debt and capitalize around €11.7 billion. The debt unloaded on Plenitude should roughly cover the difference between the CFFO generated by Plenitude during the 2023-2026 strategic plan and the additional €9 billion CAPEX investments that Eni is planning for the segment, netting out the difference between the €69 billion CFFO generated under the plan and the €37 billion in CAPEX.

For the legacy O&G operations, a CFFO of €69 (-€2.7 of Plenitude) billion will be generated, and €37 (-€9 of Plenitude) billion will be absorbed by CAPEX, generating a total of almost €38 billion free cash flow under the strategic plan. The cumulative amount averages out at €9.4 billion per year. In the base case, a 12.5% FCF yield would equate to a value of approximately €75.2 billion for the legacy business. Adding back Plenitude's €11.7 billion, we arrive at a fair value of €87 billion or 100% upside from the current trading price, which values Eni at half that amount. A fair valuation that sees Eni trading at less than 6.5x TTM Earnings and 5x TTM Cash Flow is not too farfetched, in my opinion.

Risks

There are two main risks to my bullish thesis. Firstly, there is a commodity risk at play, and Eni shares the same degree of risk as all integrated oil companies. Oil and gas prices could fall well below the company's projected scenarios, damaging profitability and preventing the development of Eni’s reserves. Although Eni's new projects have a low breakeven, their completion still depends on global oil demand. An investment in Eni assumes that, at least until 2030, oil will remain in high demand. For my bullish thesis to play out, I assume that Brent's average price will be $70 or above over the next 5-7 years. While I believe this scenario is likely to play out, those who hold a radically different view may prefer to remain on the sidelines.

The second risk is political. Despite its public listing, the Italian government retains a 30% strategic participation in Eni and, as the largest shareholder, maintains certain rights, most notably the selection of Eni's executive leadership. Six out of nine board members, including the CEO, are nominated by the government's decision. Eni's somewhat hybrid status as an SOE has clear implications that could also weigh on its valuation. However, despite Italy's history of controversial politicians and huge public debt, the risk of South American-style decrees seems minimal at most. Eni's previous strategic plan was executed fairly, and besides the CEO appointment, there was no clear sign of government interference in Eni's operations, goals, or capital allocation.

Final remarks

In my opinion, Eni shares continue to trade at a big discount to their fundamental value. While acknowledging the risks related to commodity prices and government ownership, I believe that the company's diverse business segments, low-cost production, and strategic investments in renewables position it well for future growth in the energy transition.

Eni's strong financials, including robust free cash flow generation, provide a solid foundation for future dividend growth and share buybacks. Eni has already decided to commit approximately 3.2 billion in dividends and 2.2 billion in share buybacks for 2023, the same high level of shareholders remuneration of 2022. Cash from operations is likely to be lower than FY2022, and while the company projects it to remain north of €17 billion, I think that currency headwinds and slightly lower Brent may detract an additional €1.3 - €2.0 billion. However, even at the low-end guidance of €15 billion, the cash generation would still be enough to cover 2023 CAPEX of €9.4 billion and €5.4 billion shareholders’ remuneration without increasing leverage.

I rate Eni shares a STRONG BUY, trading at almost 50% discount to my fair value of €25 per share (equal to about $54 for the ADR).

For further details see:

Eni: Oil Major Opportunity Trading At 12% Shareholders Yield, 2x Cash Flow