E - Eni's Success Amid Oil Market Turmoil: A 50% Return Story And What Comes Next

2023-11-25 04:50:31 ET

Summary

- Eni S.p.A. has outperformed its peers and returned around 50% with dividends factored in.

- The war in Ukraine, political unrest in Israel, and Europe's need to diversify gas suppliers make Eni an attractive investment.

- Eni has also developed a profitable renewable energy business - Plenitude - which is supposed to soon IPO, creating additional value.

Introduction

Let's start with a chart. In September 2022, I wrote I shared a piece of research where I disclosed I was locking in some gains from oil stocks but I wasn't selling a single share of Eni S.p.A. (E). Since then, Eni has outperformed its peers and if we factor in its dividends, it has returned around 50%.

Why was I so bullish on Eni? First of all, I was bullish on oil in general. But, more in detail, the Italian oil-major Eni appeared to be trading at a steep and unjustified to its peers. Moreover, the war in Ukraine and the need for Europe to diversify its gas suppliers as it broke ties with Russia made me realize that Eni was in a sweet spot , being one of the largest oil companies with a strong footprint in Africa, and in the Mediterranean Sea , two key areas for gas and oil (with Eni recently being awarded a big license to explore west of the Leviathan basin, off Israel's coast). The Italian government itself has been very active in recent years to approve more and more steps of a big cooperation plan Italy has approved the "Mattei Plan" offering to African countries for two reasons: secure safer energy supplies and creating more favorable economic conditions in Africa to deter illegal immigration.

Oil prices

Now, when we deal with oil stocks, it seems to be on a rollercoaster. Just a year ago, everyone was worried about triple-digit oil prices. Then oil went actually down. But oil is no easy-to-understand commodity as it is also tightly linked to geopolitics. As soon as the conflict in Israel ignited, once again we had forecasts about triple-digit prices. And yet, here we are with recent crude oil prices tumbling once again, following recent news of increasing inventories . Moreover, we know Russia is selling oil at dampened prices, creating downward pressure on Saudi and, more in general, Opec exports. Actually, OPEC members' crude oil production is still rather high and the fact inventories are increasing may actually make us think the recent tumble in prices is linked more to supply excess rather than weak demand. After all, alongside with my readers, we have seen several signs of strong and rebounding economic activity.

As far as we are concerned, Eni is mostly linked to Brent crude oil ( SPGSBR , CO1:COM ), from which two correlated aspects depend: the company's profits and its dividends. In fact, Eni has a shareholder return policy also linked to Brent prices. In fact, the company is committed to returning 25-30% of CFFO through dividends and buybacks which is protected, even in bear scenarios, by the company's use of its balance sheet, if needed. But in case of conditions exceeding the forecasted scenario, the company can apply 35% of incremental cashflow to additional buybacks. Currently, we are closer to this second environment and this makes Eni even more interesting.

Recent financials

After Eni reported its third quarter results , investors were reassured the company is in great shape and has not been idle in an entangled geopolitical environment.

First of all, the company showed it is evolving and strengthening its core businesses such as E&P and GGP while building new energy businesses, such as Plenitude, Enilive, Biochemical and CCUS.

It keeps on being an upstream leader, with the beginning of production of Baleine, offshore Ivory Coast, less than 2 years after discovery; in this way, Baleine already contributes to this quarter's results and it is on track to be an accretive element in the 3-4% growth of Eni's 4-year plan .

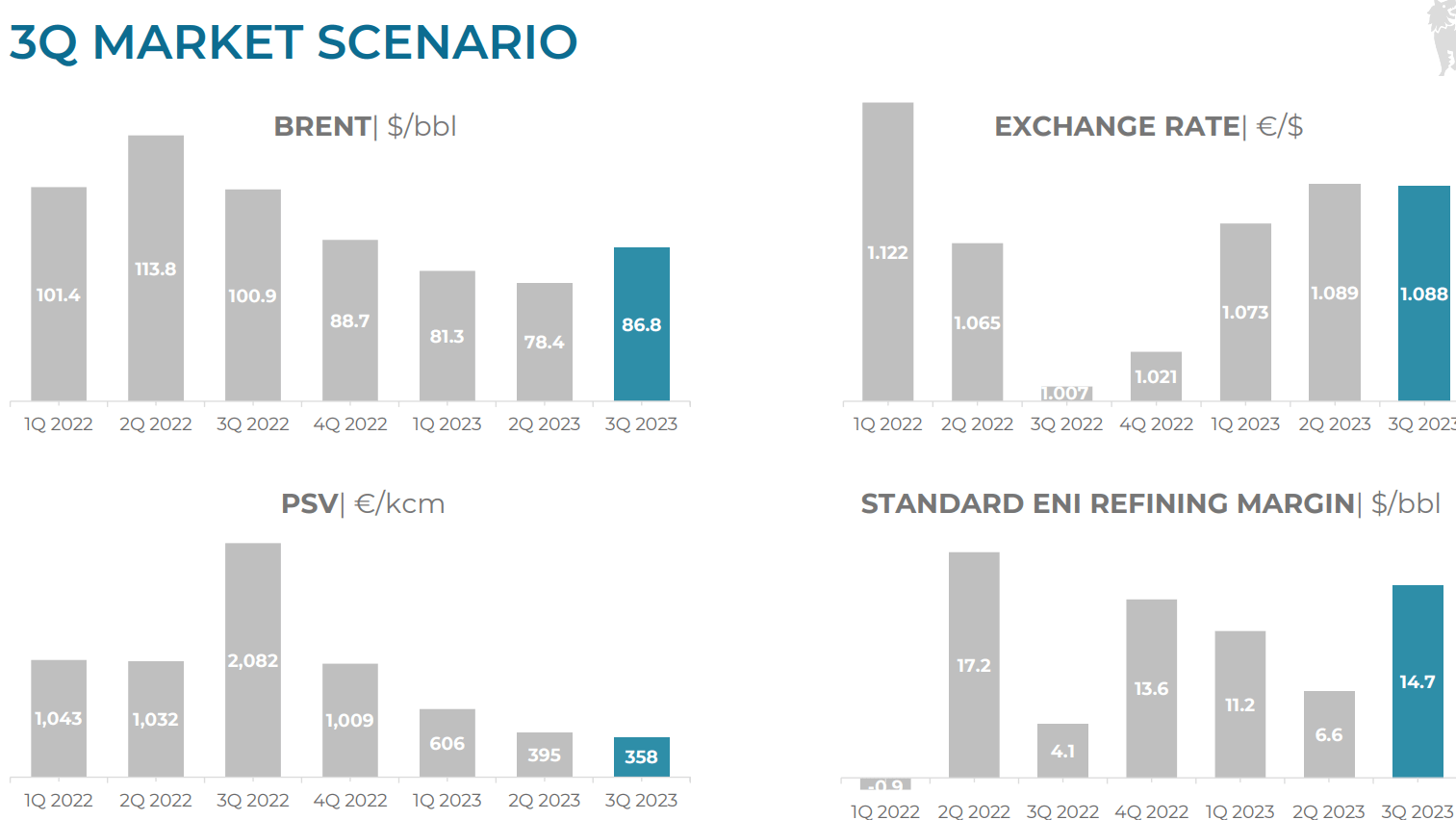

Before we look at the quarterly financial highlights, let's keep in mind the scenario, which is of utmost importance when we deal with commodity-related stocks.

Brent has gone up, as well as the euro over the U.S. dollar. These are both favorable trends for Eni, showing, in fact, a significant increase in refining margin. By looking at this picture we can already be inclined to think massive generation of cash flow is ahead of us.

{kind=link}

Now, the main group results were as follows:

- group EBIT was over €3 billion and €11 billion over the 9 months.

- tax rate continues to be in the mid-40s%, therefore, net income for the quarter was €1.8 billion and €6.6 billion for the first 9 months.

- capex is being correctly managed and will come in lower than expected and should be €9 billion for the FY, thank to 6% cost savings.

- cash conversion keeps on being good: CFFO in Q3 was € 3.4 billion, while for the first 9 months of the year it is already at € 12.9 billion. The € 6.2 billion of organic FCF generated in the first 9 months more than cover Eni's 2023 distributions

- therefore, share buybacks have been accelerated, with share count down 6% YoY.

- Eni's balance sheet keeps on being conservatively managed, with leverage only at 15%.

- shareholder remuneration. Eni now sports a quarterly dividend to make it more attractive for income seeking investors. For fiscal year 2023, the company pays a dividend of €0.94 per share in four instalments: the first payment was made in September 2023 and the second had been just paid in November 2023. The next two payments will happen March 2024 and May 2024. In May the company also started its €2.2 billion share buyback to be completed within April 2024.

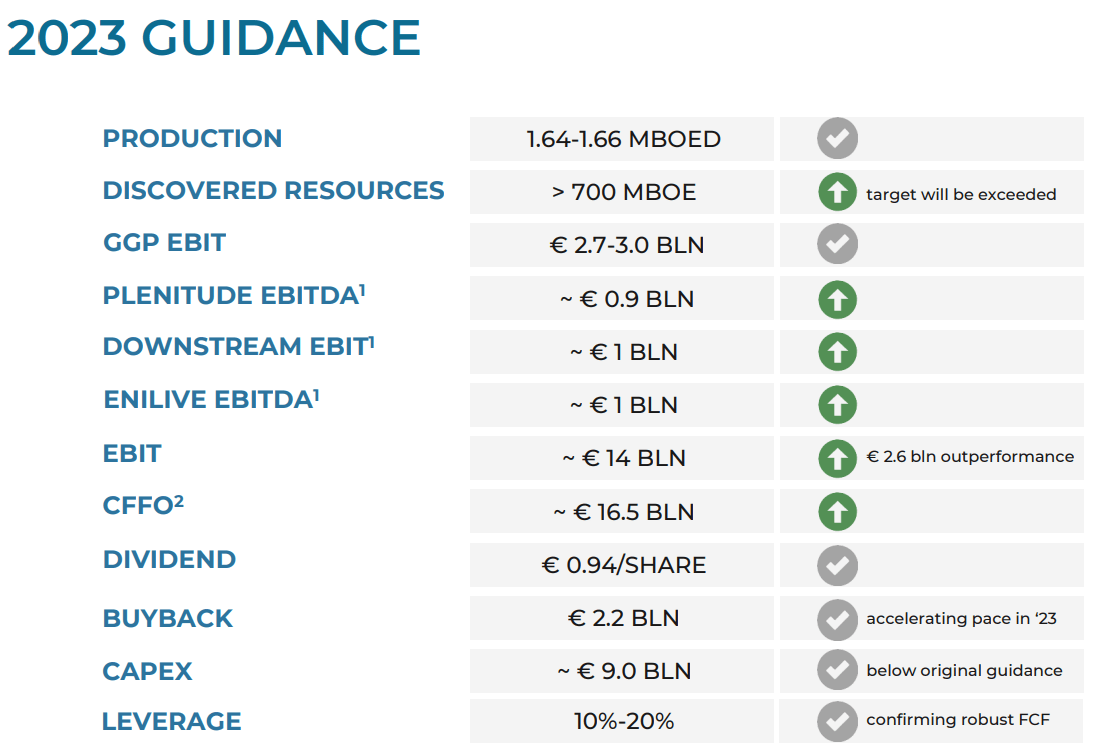

Favorable momentum. These two words give some color on the situation. However, they are not enough to explain Eni's success. After all, a company has to be correctly managed. I believe Eni's healthy balance sheet speaks above everything else from this perspective. The company is not overleveraged and can thus take care both of its capex and its shareholders. Given the situation, Eni upgraded its 2023 guidance as shown below.

{kind=link}

The two main data I want to highlight are the €2.6 billion EBIT outperformance which actually leads to €16.5 billion of CFFO and the Plenitude EBITDA of almost €1 billion, which is already well above the 2025 expected target of €800 million. During the earnings call , Eni did disclose it now expects Plenitude 2023 EBITDA to be 30% higher than the original guidance. By 2026, Eni expects to double Plenitude's EBITDA.

{kind=link}

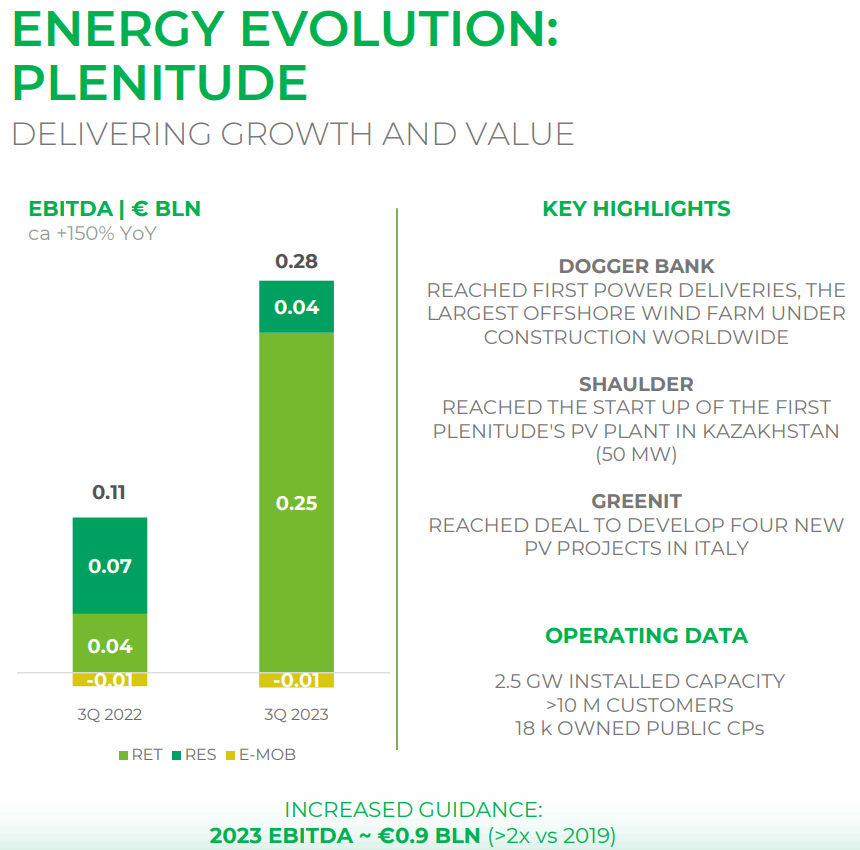

But what exactly is Plenitude? Let's spend two minutes on this topic, which may be lesser known to investors but it is indeed a big part of Eni's investment case right now. Plenitude is a B-corp active in the sale and marketing of gas and electricity for households and businesses. Its main characteristic, however, is that it produces and integrates energy only from renewable sources.

Plenitude was supposed to IPO last year in June, but due to unfavorable market conditions, the IPO was postponed to a yet-to-be defined date.

Plenitude operates in several markets: Italy, Spain, France, Greece, the UK and the U.S. Its capacity is currently around 2.5 GW serving more than 10 million retail customers, mostly in Europe.

{kind=link}

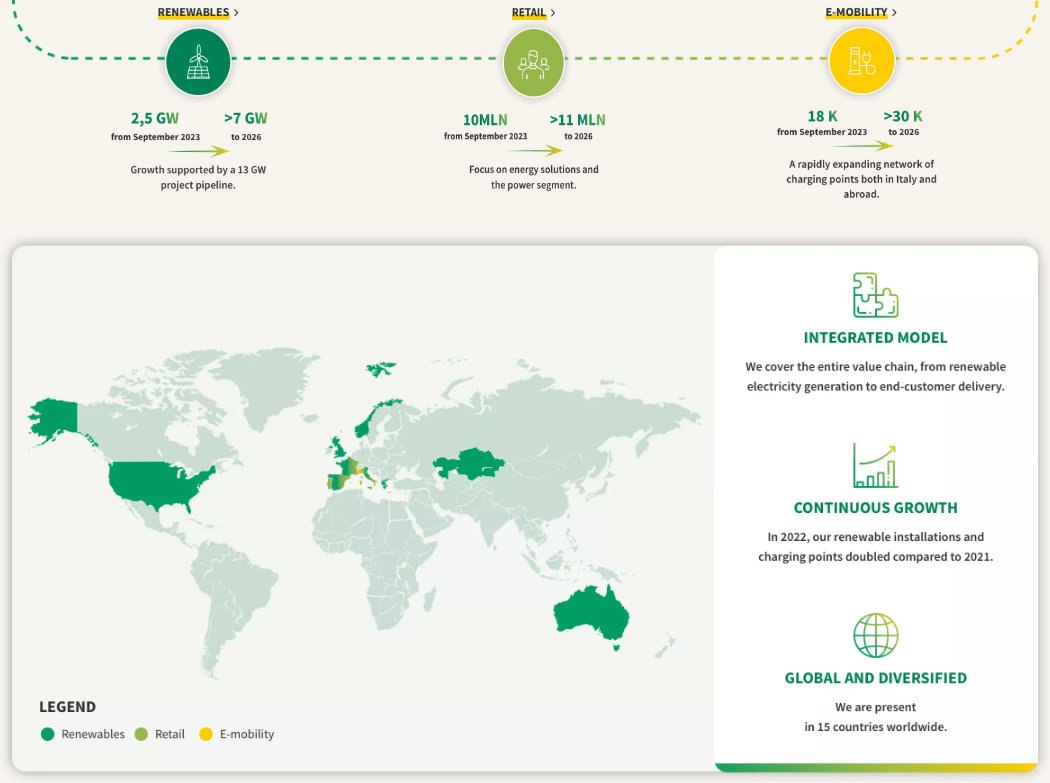

Generally speaking, this IPO is seeing a lot of favor among investors and Eni's shareholders are set to benefit from it once it will be announced. With markets going up and energy prices remaining high, we are now in a more favorable environment for the IPO to take place, so we could expect it to happen in the next few months. So far, it is hard to give a value for Eni Plenitude's business. However, some estimates see it around €8.5 billion, which is an 8.5 EBITDA multiple for a growing renewable-only energy business. Considering Eni trades currently around €50 billion in market cap, we can understand the weight Plenitude may have if its IPO takes place.

Valuation and conclusion

With a fwd PE of 6.7 and a fwd EV/EBITDA of 3, Eni trades at a steep discount to its North-American and European peers. Shell (SHEL), for example, trades at a 8.9 fwd PE and a 3.7 fwd EV/EBITDA. Total (TTE) trades at a fwd PE of 7.1 and a fwd EV/EBITDA of 3.7. Chevron (CVX) and Exxon (XOM) trade at even higher multiples (low double-digit PE and EV/EBITDA above 7).

Therefore, I reiterate my buy rating, with a target price of €18 ($37.2 for ADR) which would come from a fwd PE above 7, more in line with its peers.

For further details see:

Eni's Success Amid Oil Market Turmoil: A 50% Return Story And What Comes Next