EBF - Ennis: Acquisitions Facilitate Strong First Quarter Results

2023-06-30 15:19:26 ET

Summary

- Ennis is growing through strategic acquisitions to expand its product lines and geographical footprint.

- The company's Q1 2023 report shows a 3% YoY revenue increase to $111.3 million, with recent acquisitions contributing to this growth. The company's balance sheet shows no debt and a healthy cash reserve.

- Despite the industry's decline, Ennis maintains a stable position and has announced a dividend of $0.25 per share for shareholders who invest by July 6, 2023.

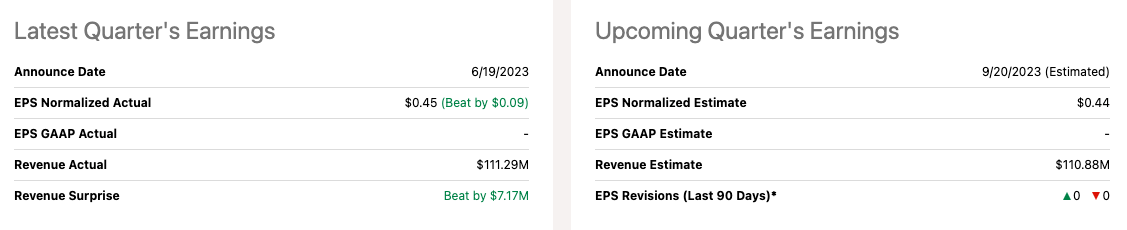

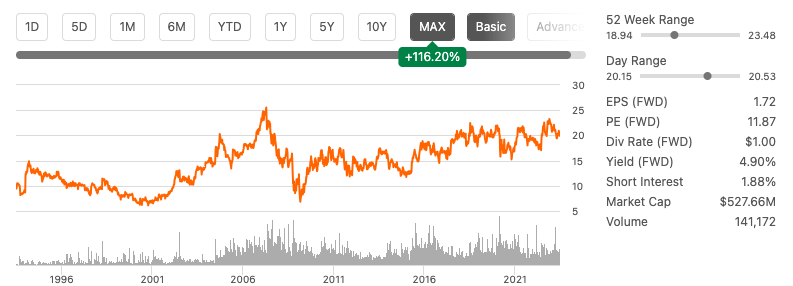

Ennis, Inc. ( EBF ) is a market leader in the declining commercial printing industry, growing its position by acquiring smaller players to increase sales and improve its profitability. The company has started Q1 2024 on a strong note, beating EPS expectations by $0.09 to reach $0.45 per share, and revenue grew YoY by 3.3% to reach $111.3 million. We can see that the stock price has bounced between the high teens to the low twenties over the last five years, not including the COVID-19 impact and recovery period.

{kind=link}

Over the last five years, the company's top and bottom line results have strengthened, revenue increased with a CAGR of 3.37%, and diluted EPS grew with a CAGR of 13.03%. The company has a strong financial position and has been inorganically growing without incurring debt. Investors may want to take a bullish stance on this stock in the current dip and take advantage of the recently announced dividend of $0.25 per share with an ex-div on July 6. I've upgraded my position due to the reduced stock price, dividend potential and the success of its acquisition strategy which have already positively impacted revenue and earnings results in the most recent quarter.

Company update

Ennis is a leading private-label print company product supplier in the USA. They provide a wide range of paper products such as labels, forms, books, post-it notes, and financial reports. Although Ennis may not be a household name, they are a significant player in the industry. In a previous article , I provided an overview of the company and the industry they operate in.

{kind=link}

Ennis is growing through opportunistic acquisitions. As the industry is in decline, smaller players struggle to compete; this creates an opportunity for Ennis to grow through inorganic acquisitions to increase its sales in new markets and channels. Ennis made two significant acquisitions over the last six months, School Photo Marketing in November 2022 and UMC Print in June 2023; this totals seven acquisitions during the previous five years. The acquisitions expand the product lines, increase the geographical footprint and bring new brand strength. The company's acquisition of competitor UMC Print increases locations and capacity to grow through distribution partners.

Q1 2024 update

Ennis may not be experiencing significant growth in sales or profits, but they have a clear and effective strategy for steady, debt-free inorganic growth. In the last quarter, their revenue increased by 3% YoY to $111.3 million, thanks in part to recent acquisitions such as School Photo Marketing and Stylecraft Printing Company, which brought in $4.1 million. While their earnings per share ((EPS)) remained steady at $0.45 compared to the previous year, the acquisitions added $0.04 in diluted EPS for the quarter.

{kind=link}

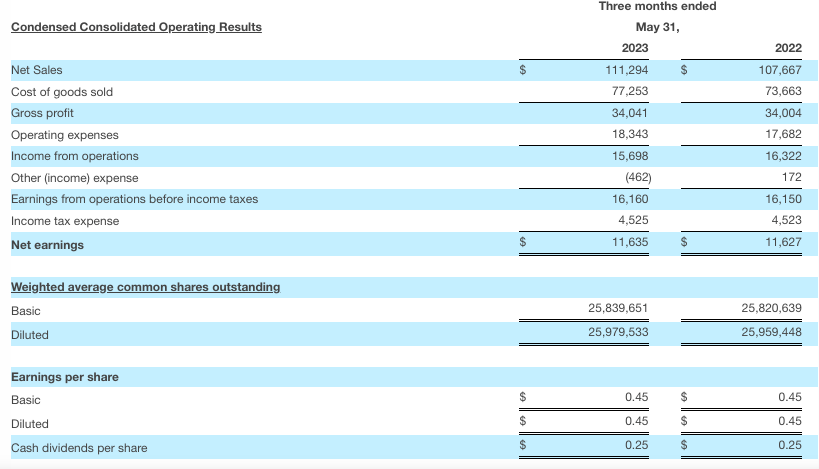

Below we can see that the gross profit margin was $34.0 million; the margin decreased slightly YoY from 31.6% to 30.6% for Q1 2023. The EBITDA was 18.4% of sales at $20.5 million. Expenses were higher this quarter due to once-off events in the form of relocation costs and legal fees, which management has indicated will benefit the business in the future.

{kind=link}

The healthy balance sheet indicates that the company can continue on its acquisition spree of smaller companies without taking on extra debt. Currently, there is $102.11 million in cash available and no debt. It is sufficiently liquid with a current ratio of 5.18 and a quick ratio of 3.88. Positive levered free cash flow was $39.64 million TTM. This gives the company room to reward shareholders. It is paying a dividend of $0.25 per share with an ex-dividend date on 6 July to be paid out in August.

{kind=link}

Ennis is not well covered by analysts but is currently trading below its average target price of $27 . The stock's trading history has never broken through the $25 mark, including years in which the company produced higher top and bottom-line results before FY 2014 . While we may not expect major growth, it could be a steady stock to hold and benefit from the quarterly dividend.

{kind=link}

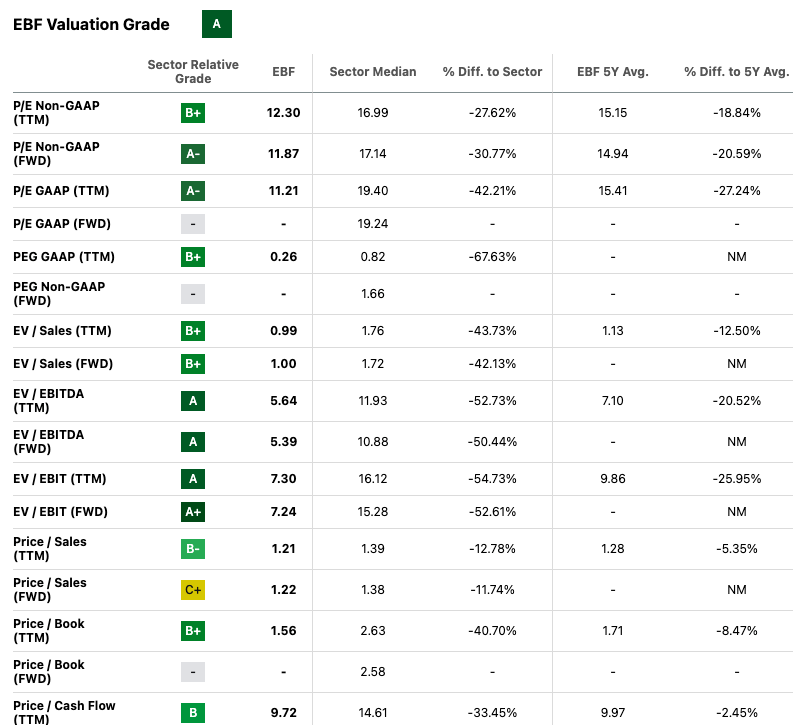

Ennis, according to Seeking Alpha's Quant rating, has a lower FWD price-to-earnings ratio of 11.87 compared to the industrials sector median of 17.14, suggesting that it may be undervalued. The EV-to-sales ratio, which takes into account the company's debt, is also under one at 0.99, making it a potentially attractive investment.

{kind=link}

Risks

Ennis is a company that operates in a declining industry and has been facing challenges for more than five years. Although it has experienced some growth through acquisitions, it is uncertain how long this strategy can continue to be successful. Ennis has not kept up with advancements in technology and digitalisation, which could negatively affect the company in the future. Additionally, while the stock pays dividends, they are not consistent and the company has not seen significant stock price growth in its trading history.

Final thoughts

Ennis delivered a strong Q1 2024 that showed top and bottom-line growth assisted by recent acquisitions. Its inorganic growth strategy is working well for the business. Although this may not be a strategy that the company can maintain for years to come due to the digitisation of the industry, for now, it has strong financials, a healthy balance sheet to keep acquiring smaller competitors, and it has recently announced a dividend. Therefore, investors may want to take a bullish stance on this company.

For further details see:

Ennis: Acquisitions Facilitate Strong First Quarter Results