SHPW - Ennis: Attractively Priced And With A Strong Balance Sheet

2023-09-24 09:35:35 ET

Summary

- Ennis is a profitable company that provides physical solutions for businesses in a digital-dominated era.

- The company has experienced growth in revenue, profits, and cash flows, with a significant portion of the increase coming from acquisitions.

- Ennis is attractively priced and a surplus of cash, making it a logical prospect for investors to consider.

Over the past 20 years, the world has moved more and more in the direction of being focused on all things digital. But whether you love it or hate it, not everything can be turned digital. And while it may not be a great growth market to play in, catering to companies and individuals that still need physical solutions in an era dominated by digital offerings, can still be profitable. One interesting company that pops in my head when I think of this concept is Ennis ( EBF ), a producer and seller of physical solutions for businesses. These solutions include, but are not limited to, business forms, pressure-seal forms, labels, tags, envelopes, and even presentation folders. In recent years, revenue, profits, and cash flows, have all increased nicely. That trend continues to the current day. On top of this, shares of the enterprise look attractively priced, both on an absolute basis and relative to companies that have some similarities to it. Given these factors and the fact that the enterprise has a surplus of cash on its books, I believe that a ‘buy’ rating is appropriate.

Filing through Ennis

The management team at Ennis describes the company as the largest provider of the aforementioned product categories that caters to independent distributors in the us. Through the 54 manufacturing plants that it has across 20 different states nationwide, the company provides customers with countless product lines, including the following brand names: Ennis, Royal Business Forms, Block Graphics, Witt Printing, and more. It also has a product line known as School Photo Marketing, which operates as a one stop shop for more than 1,400 school portrait photographers and professional photo labs across the country, reaching 15 million families and 30,000 schools.

Even though the company provides more product offerings than I can count, it really is easiest to describe it as a provider of printing services. While this might seem like a market that does not have any growth potential behind it, sources indicate otherwise. One source , for instance, estimates that between 2022 and 2032, the annualized growth rate for the global commercial printing market will rise by about 3.2%. If this comes to fruition, it would take the market up to $657.5 billion during that window of time. It would not be wise to focus solely on a forecast like this though. I say this because even management has acknowledged that the specific niche in its space has seen declines in recent years. But that's the difference between the broader commercial printing market and the specific offerings, primarily business forms and related products, sold by Ennis.

{kind=link}

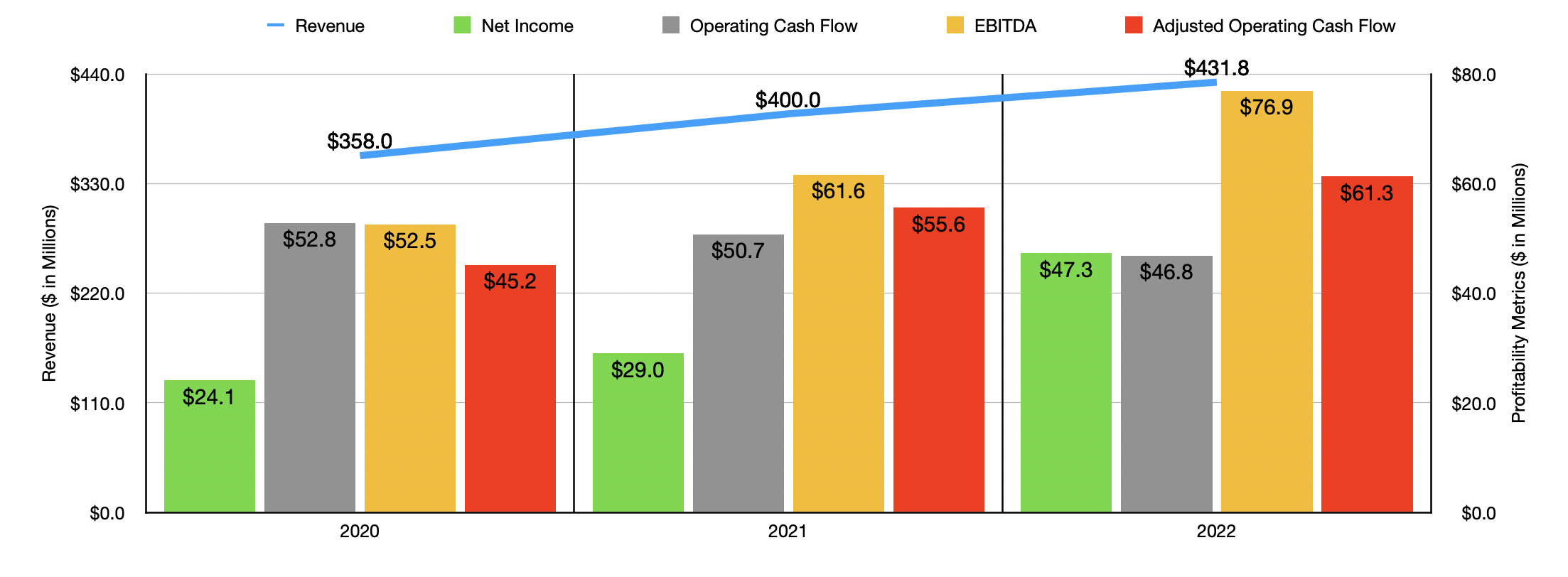

What's really great about Ennis is that, despite market issues, management has succeeded in capturing growth. In fact, in the three years ending in 2022 , growth was even more impressive, averaging about 9.8% per year. This took revenue up from $358 million in 2020 to $431.8 million in 2022. The biggest growth for the company, then, came from a combination of the economy rebounding following the worst days of the COVID-19 pandemic and overall demand growth as the economy and business spending returned to normal. However, from 2020 through 2022, nearly 37% of the increase in sales for the company came from acquisitions that management had made.

The increase in revenue brought with it higher profits as well. Net income, for instance, managed to jump from $24.1 million in 2020 to $47.3 million last year. In addition to benefiting from the higher revenue, Ennis also enjoyed some margin expansion. Its gross profit margin, for instance, grew from 28.7% to 30.2% because of operational efficiency improvements and higher pricing aimed at offsetting inflationary pressures. Selling, general, and administrative costs, also fell from 17.9% of sales to 16.4%. Operational efficiencies were in large part responsible for this. Other profitability metrics for the company followed suit. Operating cash flow did manage to drop from $52.8 million to $46.8 million. But if you adjust for changes in working capital, you get an increase from $45.2 million to $61.3 million. Meanwhile, EBITDA for the company popped from $52.5 million to $76.9 million.

{kind=link}

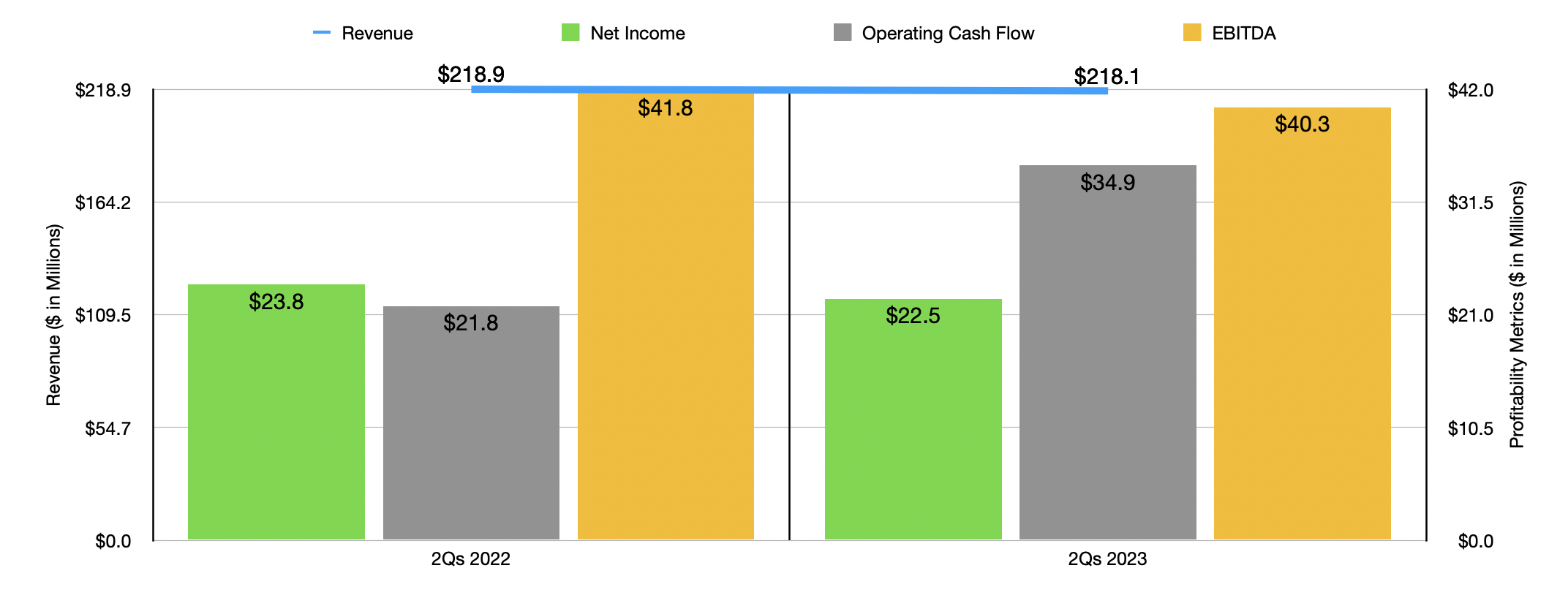

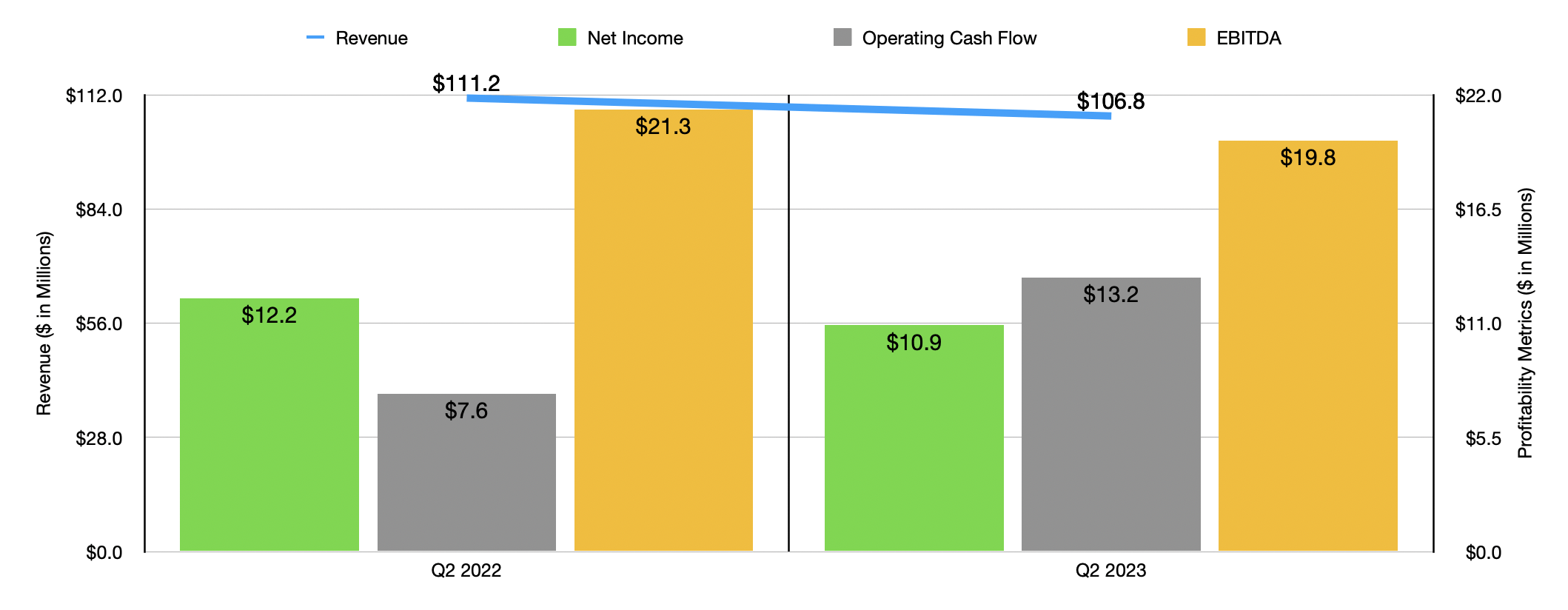

As you can see in the chart above, financial performance for the company has been a bit more mixed so far this year. If you have a keen eye, you might have noticed that I don't include adjusted operating cash flow in the data for this year. And that is because management only recently revealed results for the second quarter of this year and they did not provide enough data to calculate the adjusted figure. Unfortunately, revenue for the quarter missed analysts’ expectations by $4.1 million, while earnings per share missed forecasts by $0.02. The weakness on the top line came in spite of the fact that the company benefited to the tune of $6.5 million from acquisitions, with that benefit growing to $10.6 million if we look at the first half of the year as a whole. Unfortunately, volume declines, caused by some of the company's printer partners experiencing slowness in sales and outsourcing less of their activities to Ennis, more than offset these improvements.

{kind=link}

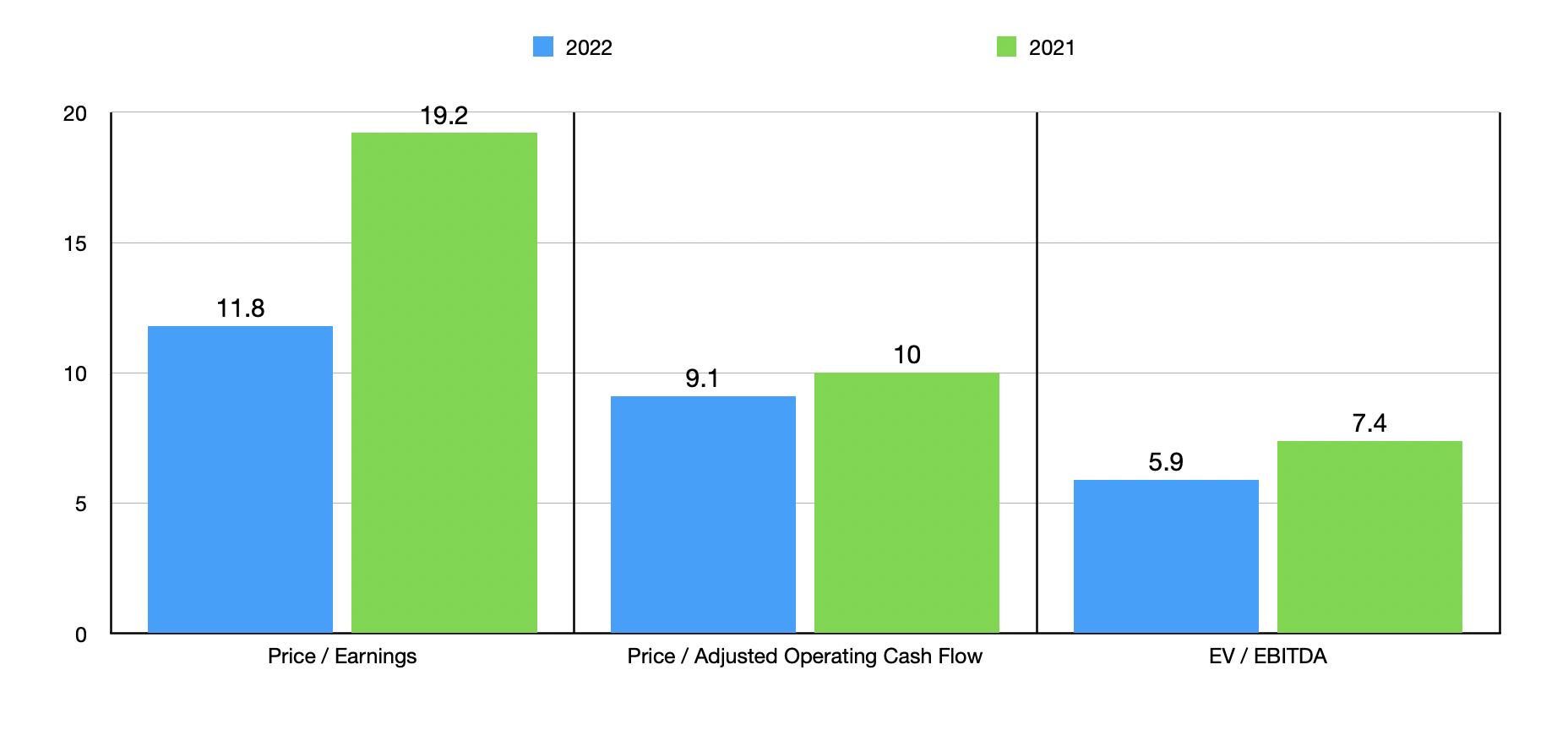

Much to my chagrin, management has not provided any guidance for the current fiscal year. But based on how performance is looking for the first half of this year relative to the same time last year, it's likely that overall financial results for 2023 will not be materially worse on the bottom line than what the company saw for 2022. If this is the case, then, as you can see in the chart below, the stock is trading at a price to earnings multiple of 11.8. The price to adjusted operating cash flow multiple should be 9.1, while the EV to EBITDA should come in at around 5.9. All of these are lower than what we would get using data from 2021. But what's most exciting about this is that, even though this year has been less than ideal, the company has no debt on its books and it enjoys cash and cash equivalents of $100.3 million. The largest reason why the firm is so cheap on an EV to EBITDA basis.

{kind=link}

Relative to other printers, shares do still work to be slightly on the cheap end of the spectrum. In the table below, I compared Ennis to four such firms. On both a price to earnings basis and on an EV to EBITDA basis, only one of the companies was cheaper than our prospect. But when using the price to operating cash flow approach, two of the three companies with positive results were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Ennis |

| 11.8 |

| 9.1 |

| 5.9 |

| Quad/Graphics Inc. ( QUAD ) |

| 24.8 |

| 1.4 |

| 4.6 |

| Deluxe Corp ( DLX ) |

| 16.6 |

| 5.2 |

| 7.0 |

| Shapeway Holdings ( SHPW ) |

| 6.6 |

| N/A |

| N/A |

| Brady Corp ( BRC ) |

| 16.0 |

| 13.4 |

| 9.9 |

Takeaway

No, Ennis is not the most exciting company on the planet. However, management has, partly through acquisitions, achieved growth in revenue, profits, and cash flows. Relative to earnings, I wouldn't say that shares are all that appealing. But when you look at the picture on both a price to adjusted operating cash flow basis and on an EV to EBITDA basis, shares look appealing on an absolute basis and are nearer to the cheap side of the spectrum when stacked up against similar enterprises. Given these factors, I would say that a soft ‘buy’ is logical at this point.

For further details see:

Ennis: Attractively Priced And With A Strong Balance Sheet