EBF - Ennis: Navigating Industry Decline With Resilience (Rating Downgrade)

2023-11-28 18:00:37 ET

Summary

- Ennis, Inc. demonstrates resilience in the declining commercial printing sector by leveraging its strong financials.

- The company focuses on stable dividend yield and potential inorganic growth through acquisitions.

- Ennis maintains a healthy balance sheet and recently acquired Eagle Graphics and Diamond Graphics to augment production capacities.

Ennis, Inc. ( EBF ) operates within an industry facing decline, yet it distinguishes itself amidst the challenging landscape. Despite the downturn in the commercial printing sector, the company exhibits resilience by leveraging its strong financials. Ennis isn't positioned as a growth-centric stock; rather, it offers a stable dividend yield and demonstrates potential for inorganic growth via acquisitions, notably evidenced by its most recent acquisition in October 2023. Although the company witnessed a year-over-year decline in revenue during the initial half of this year , it stood firm on maintaining its dividend . Notably, the stock is presently trading at an elevated level compared to its previous valuation. Considering the current price, my perspective leans towards a hold recommendation, suggesting a prudent approach to await a more favourable entry point rather than advocating for immediate purchase.

Company updates

In my prior article from June with a Buy rating, I delved into the profile of Ennis, a notable player navigating the shrinking commercial printing sector. Renowned for its emphasis on private-label printed business products, the company has strategically expanded through the acquisition of smaller entities, acquiring nine in the last five years, positively affecting sales and profitability. This deliberate acquisition approach, coupled with leveraging economies of scale, has yielded favourable results over the last three financial years, diversifying revenue streams and curbing operational costs.

Annual revenue and gross profit ( SeekingAlpha.com )

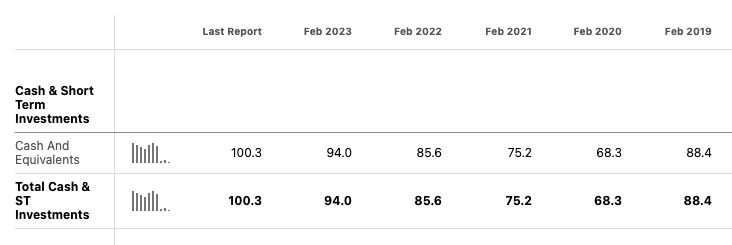

Although, we can see that TTM results for revenue and gross profit are slightly lower than the prior year. The company's appeal lies in its healthy balance sheet with an upward-trending cash position.

Annual cash and equivalents ( SeekingAlpha.com )

{kind=link}

The recent acquisition spree in October, encompassing Eagle Graphics and Diamond Graphics, underscores the company's concerted efforts to improve its production capacities. Buoyed by a substantial cash reserve and a debt-free status, Ennis remains actively engaged in seeking out acquisition opportunities. These endeavours are geared towards delivering profits and returns for its esteemed shareholders.

Financial updates

In the second quarter of 2024, Ennis reported revenues totalling $106.8 million, accompanied by EPS of $0.42. Foreseeing robust expansion isn't the focus here; rather, the emphasis lies on delivering earnings, maintaining a robust balance sheet while consistently rewarding shareholders through its dividend program.

Annual income overview (Marketscreener.com)

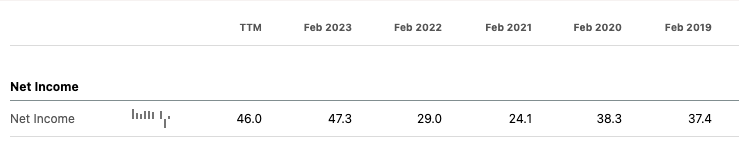

Analysing the financials, the TTM net income stands at $46 million, marginally under the previous year but showcasing an upward trajectory over the last five years.

{kind=link}

Highlighting the levered free cash flow, the TTM figure stands at $41.3 million, marking an upswing from the preceding fiscal year. This upward trend signifies Ennis's capacity to not only sustain its dividend program for investors but also earmark resources for future acquisition ventures.

{kind=link}

Speaking of dividends, the most recent distribution by Ennis amounted to $0.25 per share, resulting in an impressive 4.75% dividend yield, a significant attraction for income-focused investors.

{kind=link}

A noteworthy observation within the balance sheet is the company's minimal debt exposure at $11.94 million, juxtaposed with a substantial cash reserve of $100.34 million in cash and equivalents. This financial solidity plays a pivotal role in Ennis's growth strategy, facilitating sales and profit expansion through strategic acquisitions, even within a market experiencing a decline.

Balance sheet (SeekingAlpha.com)

Valuation

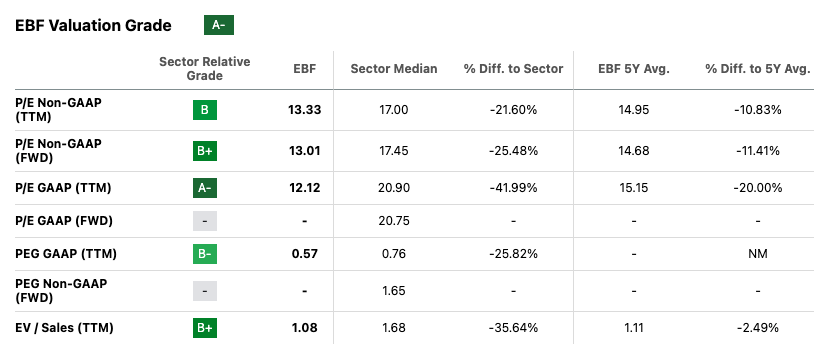

Following my prior analysis, the stock has demonstrated a modest uptick of 5.20%. Although there's been a marginal increase in short interest, currently resting at a low 2.16%, it's worth noting that the stock's forward price-to-earnings ratio stands at 13.01. This figure positions it below the industrial sector median of 17.57, hinting at a potential undervaluation. Moreover, Ennis offers an attractive dividend yield of 4.66%, surpassing the industry average of 1.54%, adding to its appeal. However, it's crucial to highlight the stock's underrepresentation in analyst coverage, with an average price target of $27, a value above its current trading range.

{kind=link}

Delving deeper into financial metrics, Ennis showcases a commendable return on equity [ROE] of 13%, denoting efficient capital utilisation by management. This figure, calculated as net profit ($46 million) divided by shareholder's equity ($343 million), signifies the company's ability to generate $0.13 in profit for every dollar of shareholders' equity-surpassing the industry average of 8.6%. However, juxtaposed against this, the company's earnings growth rate remains modest at an average of 3.3%, notably lower than the industry average of 9.1%. A calculated projection based on this historical trend indicates a stock value per share of $21.17, aligning closely with the current trading range. Consequently, I would advocate a cautious approach, awaiting a more opportune entry point, given this evaluation.

Stock value per share (Moneychimp.com)

Risks

Ennis confronts risks stemming from its stagnant growth trajectory within a declining industry. The escalating prevalence of digital document transmission casts a looming shadow, posing a substantial threat to the company's traditional printing business. Moreover, the broader decline in demand within the printing industry amplifies the challenge, exacerbated by the prevalence of price wars among competitors. These factors collectively underscore the substantial headwinds Ennis encounters, accentuating the uphill battle it faces in navigating a landscape undergoing rapid digital transformation and grappling with a diminishing demand curve.

Final thoughts

Ennis stands resilient amidst an industry in decline, leveraging robust financials and a strategic approach to acquisitions. This is not a stock poised for rapid growth, but one offering stability through dividends and potential expansion opportunities. However, its current price exceeds previous valuations, suggesting a prudent 'hold' stance while awaiting a more favourable entry point. The company's financial strength, emphasized by healthy cash reserves and minimal debt, positions it well for strategic growth initiatives despite facing challenges from the industry's digital transformation and declining demand.

For further details see:

Ennis: Navigating Industry Decline With Resilience (Rating Downgrade)